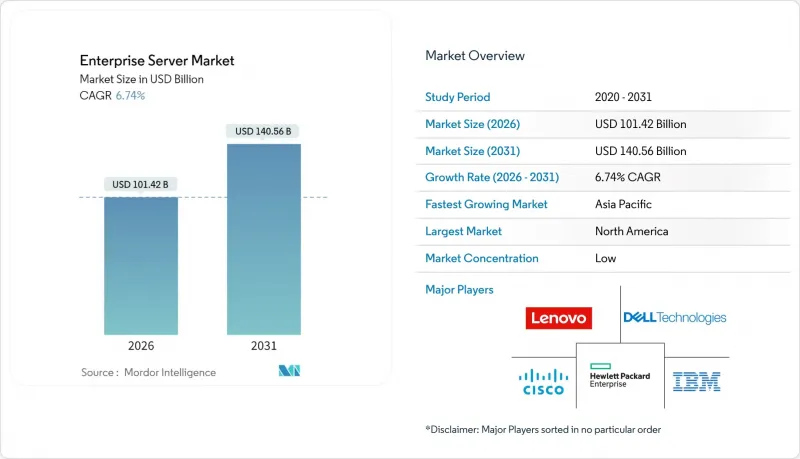

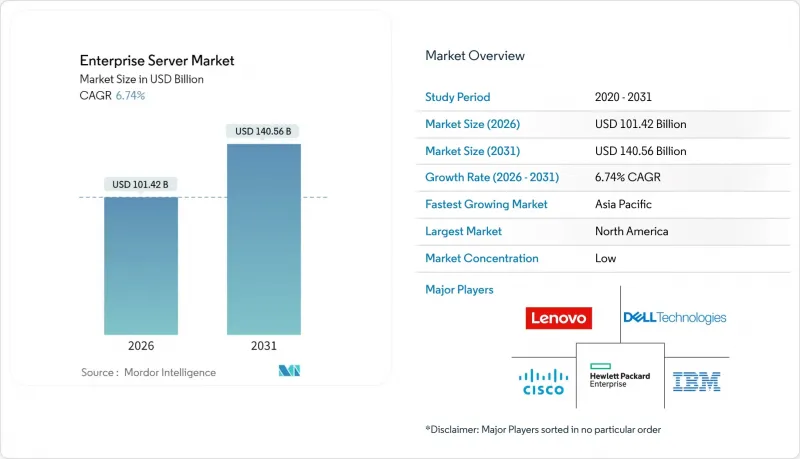

기업 서버 시장은 2025년에 950억 2,000만 달러로 평가되며, 2026년 1,014억 2,000만 달러에서 2031년까지 1,405억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.74%로 예상됩니다.

성장의 배경에는 AI 최적화 서버 클러스터의 기록적인 수주, 하이브리드 클라우드 배포 증가, 대규모 조달 사이클을 지원하는 공공 부문의 경기부양책이 있습니다. 하이퍼스케일러, 독립 소프트웨어 벤더, 규제 대상 기업은 트레이닝 및 추론 워크로드를 지원하는 GPU 고밀도 시스템에 자본 계획을 집중하고 있으며, 이러한 변화는 부품 공급망을 재구성하고 액체 냉각 랙에 대한 수요를 가속화하고 있습니다. 동시에, 5G 지원 엣지 배포와 마이크로 데이터센터는 견고하고 저전력 소모가 적은 서버의 잠재적 시장을 확대하고 있습니다. 또한 구독 가격 설정은 설비투자의 급격한 증가 없이 짧은 갱신 주기를 원하는 기업의 예산 장벽을 완화하고 있습니다. 자체 개발한 실리콘, 고속 인터커넥트, 엔드투엔드 수명주기 서비스를 결합한 벤더들은 턴키 AI 인프라를 원하는 구매자들로부터 시장 점유율을 확보하고 있습니다.

하이퍼스케일러 기업은 기존 범용 노드를 GPU 고밀도 시스템으로 대체하고 있으며, 랙당 40-60kW를 지원할 수 있으며, 이는 기존 데이터센터의 약 5배에 달하는 열 부하에 해당합니다. 기업 조달에서는 현재 AI 전용으로 지정되지 않은 도입 환경에서도 향후 AI 도입 일정 변화에 대비한 기반 강화를 위해 액체 냉각 루프, 실리콘 포토닉스 인터커넥트, 고대역폭 메모리를 표준 사양으로 지정하는 추세입니다. 전력 소비가 급격히 증가함에 따라 버지니아 북부와 더블린의 전력회사는 데이터센터 지역의 전력망 업그레이드를 우선순위에 두고 있으며, 이는 에너지 효율이 높은 서버 설계에 대한 규제 측면의 호재로 작용하고 있습니다. 국가 차원의 AI 안전 프레임워크는 구매자가 거버넌스 모델을 로컬에서 실행 가능한 인프라를 구축하도록 장려하고 있으며, 기존의 워크로드 예측을 넘어서는 수요를 창출하고 연산 가속기의 갱신 주기를 3년 미만으로 단축하고 있습니다.

경영진의 용도 이식성 확보 요구가 On-Premise 랙과 여러 퍼블릭 클라우드를 인프라-즈-코드(Infrastructure-as-a-Code) 파이프라인으로 연동하는 하이브리드 아키텍처를 추진하고 있습니다. 예를 들어 HashCorp의 자동화 스택은 자체 랙과 임대 하이퍼스케일 용량에서 동일한 프로비저닝 로직을 구현하고자 하는 기업에게 사실상 제어 플레인이 되고 있습니다. 이러한 환경을 위해 제공되는 서버는 확장된 PCIe 레인, 듀얼 100GbE 포트, 내장형 인증 모듈을 탑재하여 하이브리드 경계의 양측을 동일한 보안 엔벨로프(envelope)로 보호합니다. GDPR(EU 개인정보보호규정)에 따른 엄격한 데이터 거주 규정으로 인해 많은 유럽 기업은 국가별 데이터베이스를 국내에 배치할 수밖에 없습니다. 한편, 버스트 가능한 분석 작업은 해외 가용성 영역에서 실행되므로 BIOS, 펌웨어, 관리 API의 일관성을 제공하는 벤더에게 유리한 혼합 조달 패턴이 발생하고 있습니다. 종량제는 서버 지출을 계절별 프로젝트 부하에 맞게 조정하여 프로젝트가 정체되었을 때 손실을 줄일 수 있습니다.

VMware, KVM, 컨테이너 오케스트레이션을 운영하는 기업에서는 CPU 사용률이 80-90%에 이르는 것이 일상화되어 있으며, 범용 워크로드를 위해 x86 노드를 추가해도 증분 효과가 크게 떨어집니다. 일부 금융기관은 레거시 용도의 통합 비율이 20:1에 달하고, 물리적 공간과 에너지 소비를 크게 줄였습니다. 그러나 AI 학습 워크로드는 GPU 공유 기술이 성숙하지 않아 이러한 집적화가 어렵습니다. 조직은 기존 가상화 리소스를 최대한 활용하면서도 분리된 가속기 풀을 유지하기 위해 서버 계층 간 수요 편중이 발생합니다. 유럽연합의 에코 디자인 규정 등 정부 주도의 에너지 절약 지침은 가동률이 낮은 랙에 페널티를 부과함으로써 자원의 한계까지 활용하는 행동을 촉진합니다. 이러한 기존 워크로드의 효율성 향상은 시간이 지남에 따라 AI 클러스터로 인한 볼륨 증가분을 일부 상쇄할 수 있을 것입니다.

리눅스는 2025년에도 54.32%의 기반을 유지하며 4년 전보다 8% 상승하여 기업용 서버 시장 점유율의 과반수를 차지했습니다. 오픈소스 라이선스, 컨테이너 호환성, AI 프레임워크 관리 단체의 일류 지원이 6.88%의 예측 CAGR을 지원하고 있습니다. 따라서 리눅스 노드용 기업 서버 시장 규모는 경쟁 OS보다 빠른 속도로 확대될 것이며, 프라이빗 및 퍼블릭 클라우드 환경 모두에서 플랫폼의 우위를 확고히할 것입니다. 업종을 불문하고, 추론 용도로는 Red Hat Enterprise Linux와 Ubuntu LTS가 가장 많이 도입된 변형이며, 규제 환경에서는 Rocky Linux와 같은 견고한 파생 버전이 선호되고 있습니다.

NET 용도과 Active Directory에 의존하는 워크로드를 계속 지원하고 있지만, 모놀리식 시스템을 마이크로서비스로 재구축하는 기업에서는 Windows Server의 점유율이 하락하고 있습니다. UNIX는 고빈도 거래 및 중요 통신 교환기 등의 분야에서 확고한 틈새 시장을 유지하고 있으며, 결정론적 I/O와 인증된 안정성이 현대화 압력을 이겨내고 있습니다. 향후 전망으로는 차기 리눅스 커널에 도입될 기밀 컴퓨팅 확장 기능은 기밀성이 높은 AI 모델 가중치를 다루는 고객층에서 점유율을 확대할 수 있는 새로운 수단이 될 것입니다.

2025년 출하량에서 볼륨급 머신은 66.58%를 차지하며 기업 서버 시장 규모에서 가장 큰 점유율을 유지하고 있습니다. 그러나 향후 성장은 하이엔드 플랫폼으로 기울어질 것이며, CAGR은 7.02%로 예측됩니다. 수요는 양극화되고 있습니다. 컨테이너 팜을 위한 저비용의 스테이트리스 컴퓨팅과 트랜스포머 모델 트레이닝을 위한 8대 이상의 GPU를 탑재한 프리미엄 노드입니다. ERP 및 데이터베이스 클러스터를 위해 제공되던 미드레인지 구성은 이러한 워크로드가 SaaS 환경으로 이동하거나 더 저렴한 스케일아웃 하드웨어로 이동함에 따라 그 중요성을 잃어가고 있습니다.

그 결과, OEM의 로드맵은 이분화되어 있습니다. 양산 모델은 고밀도 가상화를 위해 효율 코어와 E1.S 플래시를 통합하고, 하이엔드 라인은 PCIe CXL 메모리 확장 및 수랭식 퀵 디스커넥트 기능을 추구합니다. 양산 계층에서는 수탁제조 업체가 비용 우위를 점하고 있지만, 주요 벤더들은 펌웨어 검증, 보안 인증, 가속기 보증 할당 등을 번들로 묶어 성능 계층을 보호하고 있습니다. CIO들 사이에서는 스케일 아웃과 스케일 업의 구매 주기가 더욱 괴리되어 양극화 현상이 가속화될 것이라는 전망이 지배적입니다.

북미는 2025년에도 37.35%로 선두를 유지했으며, 애리조나, 아이오와, 퀘벡에 집적된 하이퍼스케일 캠퍼스가 주도했습니다. 주요 시장 전체의 재고는 전년 대비 43% 증가했으며, 북버지니아의 공실률은 1% 이하로 떨어졌고, 테넌트들은 인테리어 공사 2년 전부터 용량을 사전 임대해야 하는 상황입니다. 5,000억 달러 규모의 스타게이트 계획 등 연방정부의 구상으로 인해, CHIPS 법에 따라 원산지 추적을 인증할 수 있는 OEM(Original Equipment Manufacturer)에 대규모 마스터 계약이 집중되고 있습니다. 지역 전력회사는 250MW 규모의 단일 사이트 수요에 대응하기 위해 미활용 발전설비 재사용으로 사업자와의 협력을 강화하고, 재생에너지 PPA를 서버 총소유비용(TCO) 모델에 반영하고 있습니다.

아시아태평양은 7.38%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있으며, 베이징의 국가 AI 지침과 도쿄-시드니-서울의 건설 붐에 힘입어 가장 빠른 성장세를 보이고 있습니다. 싱가포르의 엄격한 건설 규제로 인해 건설이 조호르와 바탐으로 이동하는 반면, 뭄바이의 토지 부족으로 인해 오프사이트 조립식 모듈형 데이터홀에 대한 관심이 높아지고 있습니다. 현지 언어 지원 클라우드 프로바이더들은 물 사용량 제한을 피하기 위해 공기가 없는 침지 탱크를 지정하고 있으며, 이러한 움직임으로 인해 절연액 지원 머더보드 사전 인증 업체로 지출이 이동하고 있습니다. 인도와 인도네시아의 국가 데이터 보호법은 조달을 더욱 현지화하여 OEM(Original Equipment Manufacturer)가 국내 조립을 위한 보세 창고 시설을 설치하도록 의무화하고 있습니다. 유럽은 전력 사용량 할당제와 탄소세의 영향으로 다른 지역보다 엄격한 PUE 기준이 적용되고 있으며, 꾸준한 수요 증가가 예상됩니다. 프랑크푸르트 도시권에서는 70MW 이상의 신규 건설이 금지되어 헤센주 지방으로 수요가 유출되고 있습니다. 파리는 국가 클라우드 헌장을 배경으로 원자력 기저부하를 통한 탄소 제로 구역을 보장하고 있으며, 유럽 구매자에게 천연가스 연동 요금에 대한 비용 안정적 대안을 제공합니다. 암스테르담은 지역 난방 회수를 입증하는 프로젝트에 한해 데이터센터 건설 중단 조치를 해제했으며, 이 규정은 주택 블록의 열교환 루프에 온수 서버를 통합하는 공급업체를 우대하는 것입니다. 유럽 전역에서는 에너지 절약형 하드웨어에 대한 부가가치세 면제로 인해 액체 냉각 랙의 초기 도입 비용의 일부가 상쇄되고 있습니다.

The enterprise server market was valued at USD 95.02 billion in 2025 and estimated to grow from USD 101.42 billion in 2026 to reach USD 140.56 billion by 2031, at a CAGR of 6.74% during the forecast period (2026-2031).

Growth stems from record orders for AI-optimized server clusters, rising hybrid-cloud adoption, and public-sector stimulus packages that underwrite large procurement cycles. Hyperscalers, independent software vendors, and regulated enterprises are aligning capital plans around GPU-dense systems that support training and inference workloads, a shift that is reshaping component supply chains and tipping demand toward liquid-cooled racks. Simultaneously, 5G-enabled edge deployments and micro-data centers are broadening the addressable base for ruggedized, low-power servers, while subscription pricing is easing budget hurdles for firms that want short refresh cycles without CapEx spikes. Vendors that combine in-house silicon, high-speed interconnects, and end-to-end lifecycle services are capturing wallet share as buyers seek turnkey AI infrastructure.

Hyperscalers are replacing conventional general-purpose nodes with GPU-dense systems that can support 40-60 kW per rack, roughly five times the thermal load seen in legacy data centers. Enterprise procurement now specifies liquid-cooling loops, silicon-photonics interconnects, and high-bandwidth memory as standard-even for deployments not earmarked for AI-in order to future-proof footprints against shifting AI adoption schedules. Power draw is escalating so quickly that utilities in Northern Virginia and Dublin are prioritizing grid upgrades for data-center zones, lending a regulatory tailwind to energy-efficient server designs. National AI safety frameworks encourage buyers to build infrastructure that can run governance models locally, driving demand beyond traditional workload forecasts and shortening refresh cycles to under three years for compute accelerators.

C-suite mandates for application portability are fueling hybrid architectures in which on-premises racks interoperate with multiple public clouds via infrastructure-as-code pipelines. HashiCorp's automation stack, for instance, has become a de-facto control plane for enterprises that want identical provisioning logic across their own racks and rented hyperscale capacity. Servers shipped into these estates ship with expanded PCIe lanes, dual 100 GbE ports, and embedded attestation modules so that the same security envelope covers both sides of the hybrid boundary. Strict data-residency rules under GDPR compel many European firms to place stateful databases on domestic soil, while burstable analytics jobs run in foreign availability zones, creating mixed procurement patterns that favor vendors offering consistent BIOS, firmware, and management APIs. Consumption-based pricing further aligns server spend with seasonal project loads, reducing write-offs when projects stall.

Enterprises running VMware, KVM, and container orchestration routinely hit 80-90% CPU utilization, slashing the incremental benefit of adding more x86 nodes for general workloads. Some banks report consolidation ratios of 20:1 for legacy applications, a feat that materially cuts real-estate and energy consumption. Yet AI training workloads resist such aggregation because GPU sharing is still nascent; organizations therefore maintain isolated accelerator pools while sweating existing virtualized fleets, resulting in uneven demand across server tiers. Government-backed energy-efficiency directives, such as the European Union's EcoDesign rules, reinforce capacity-stretching behavior by penalizing low-utilization racks. Over time, these efficiency gains in conventional workloads will offset a portion of the volume growth generated by AI clusters.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Linux retained a 54.32% foothold in 2025, a position eight points stronger than four years prior and equal to more than half of total enterprise server market share. Its open-source licensing, container compatibility, and first-class support from AI framework maintainers underpin a 6.88% forecast CAGR. The enterprise server market size devoted to Linux nodes will therefore expand faster than that of any rival OS cohort, cementing the platform's dominance for both private and public cloud estates. Across sectors, Red Hat Enterprise Linux and Ubuntu LTS remain the most-deployed variants for inference, while hardened derivatives such as Rocky Linux are gaining favor in regulated environments.

Behind the headline numbers, Windows Server still anchors workloads tethered to .NET applications and Active Directory but is losing share where firms are rewriting monoliths into microservices. UNIX retains durable niches in high-frequency trading and critical telecom exchanges where deterministic I/O and certified stability outweigh modernization pressures. Looking ahead, confidential computing extensions arriving in the next Linux kernel will give the platform another lever for share capture among customers handling sensitive AI model weights.

Volume class machines accounted for 66.58% of shipments in 2025, the single largest slice of enterprise server market size, yet forward growth tilts toward high-end platforms at 7.02% CAGR. Demand is coalescing around two extremes: low-cost, stateless compute for container farms and premium nodes equipped with eight or more GPUs for transformer model training. Mid-range configurations that once served ERP and database clusters are becoming less relevant as those workloads either move to SaaS environments or migrate onto cheaper scale-out hardware.

Consequently, OEM roadmaps now bifurcate: volume units integrate efficiency cores and E1.S flash for dense virtualization, whereas high-end lines target PCIe CXL memory expansion and liquid-coolant quick-disconnects. Contract manufacturers hold a cost advantage in the volume tier, but tier-one vendors defend the performance layer by bundling firmware validation, security attestation, and guaranteed accelerator allocations. The prevailing view among CIOs is that scale-out and scale-up purchase cycles will diverge further, reinforcing the two-track dynamic.

The Enterprise Server Market Report is Segmented by Operating System (Linux, Windows, UNIX, and More), Server Class (High-End Server, Mid-Range Server, and Volume Server), Server Type (Blade, Multi-Node, Tower, and Rack Optimized), End-User Vertical (IT and Telecommunication, BFSI, Manufacturing, Retail, Healthcare, Media and Entertainment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America kept its 37.35% lead in 2025, propelled by hyperscale campuses clustering in Arizona, Iowa, and Quebec. Inventory across the region's primary markets expanded 43% year over year, yet vacancy slid below 1% in Northern Virginia, forcing tenants to pre-lease capacity two years ahead of fit-out. Federal initiatives such as the USD 500 billion Stargate program funnel large master contracts to OEMs that can certify origin tracking under CHIPS Act guardrails. Regional utilities, grappling with 250 MW single-site requests, are partnering with operators on stranded-generation reclamation, weaving renewable PPAs into server TCO models.

Asia Pacific is the fastest-growing theater at 7.38% CAGR, buoyed by Beijing's sovereign AI mandates and a construction wave across Tokyo, Sydney, and Seoul. Tight moratoria in Singapore divert builds to Johor and Batam, while Mumbai's land-bank constraints propel interest in modular, stackable data halls assembled off-site. Local-language cloud providers are specifying air-free immersion tanks to sidestep water-usage caps, a move that shifts spend toward vendors pre-qualifying motherboards for dielectric fluids. National data-protection statutes in India and Indonesia further localize procurement, requiring OEMs to establish bonded warehouse facilities for in-country assembly. Europe contributes steady incremental demand, albeit under the shadow of power-usage quotas and carbon levies that impose stricter PUE thresholds than any other region. Frankfurt's metro ring now prohibits new 70 MW-plus builds within city limits, pushing overspill into Hesse's rural districts. Paris, backed by a sovereign cloud charter, is underwriting zero-carbon zones fueled by nuclear baseload, giving European buyers a cost-stable alternative to natural-gas-pegged tariffs. Amsterdam lifts its data-center pause only for projects demonstrating district-heating recovery, a rule that favors vendors integrating warm-water servers into heat-exchange loops for residential blocks. Across the continent, VAT exemptions on energy-efficient hardware partially offset the upfront premium of liquid-cooled racks.