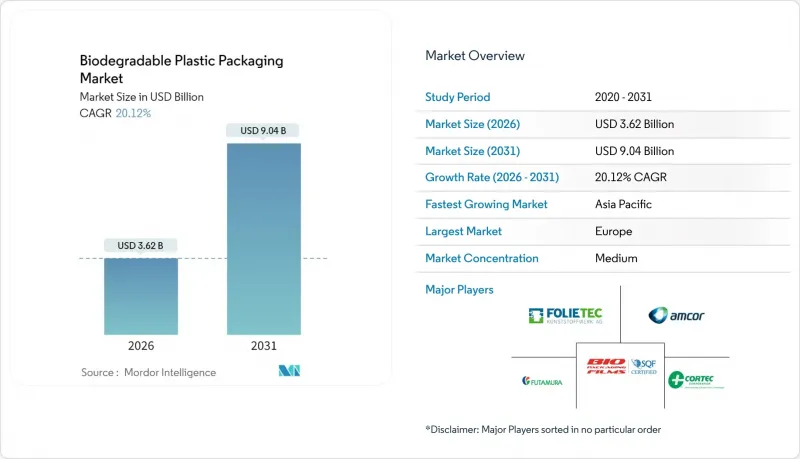

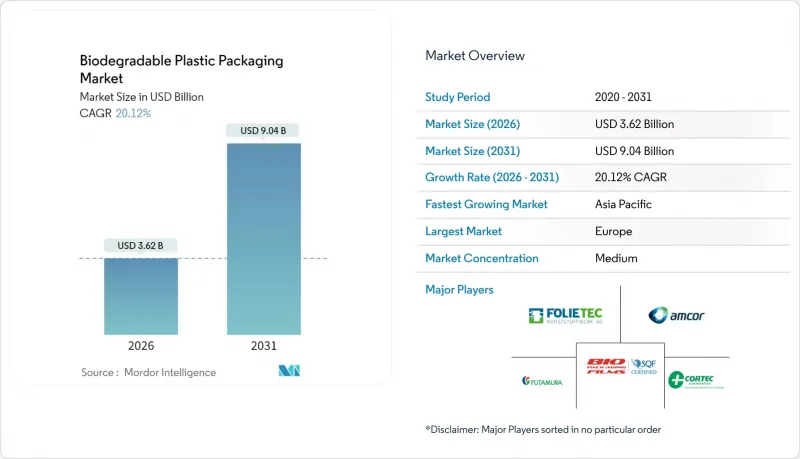

생분해성 플라스틱 포장 시장 규모는 2026년에 36억 2,000만 달러로 추정되고 있습니다.

이는 2025년 30억 1,000만 달러에서 성장한 수치이며, 2031년에는 90억 4,000만 달러에 달할 것으로 예측됩니다. 2026-2031년 연평균 복합 성장률(CAGR) 20.12%로 확대될 것으로 예측됩니다.

이러한 견고한 성장 궤적은 규제 요건의 강화, 기업의 탄소 가격 정책, 바이오 수지 가공 기술의 급속한 발전과 함께 퇴비화 가능한 포장 형태의 경제적 타당성을 높이고 있음을 반영합니다. 브랜드 오너들은 현재 지역별 포장 사양보다 세계 사양을 우선시하고 있으며, 이를 통해 대량 주문이 가능해져 단가 절감 효과를 얻고 있습니다. 재료 혁신으로 인해 기존 폴리머와의 성능 차이가 계속 줄어들고 있으며, 해양 분해성 PHA와 내열성 PBAT 변종은 엄격한 차단성 및 내열성 요구 사항을 충족하게 되었습니다. 이와 함께 지자체들의 쓰레기 감축 목표가 식품 배송 및 소매 부문에서 인증된 퇴비화 솔루션을 채택하도록 장려하고 있으며, 이는 수지 공급업체들에게 예측 가능한 수요를 창출하고 있습니다. 따라서 생분해성 플라스틱 포장 시장은 여전히 변동이 심한 농업 원자재 가격을 보완할 수 있는 명확한 수요 전망을 누리고 있습니다.

유럽연합(EU)의 2024년 '일회용 플라스틱 지침'은 칼붙이, 조개껍질 용기 등 재활용이 어려운 제품을 대체할 수 있는 인증된 퇴비화 가능한 식품접촉 포장재에 대한 수요를 즉각적으로 불러일으켰습니다. 인도의 주 단위 금지 조치는 18억 명 이상의 소비자들에게도 비슷한 전환을 촉구하고, 다국적 기업에게 세계 규격의 통일을 요구하며, 수지 공장의 규모의 경제를 실현할 수 있는 기회를 제공합니다. 바이오소재의 프리미엄보다 더 큰 페널티가 채용을 더욱 가속화하고 있습니다. 호주의 2024년 금지 조치는 생산자에게 수요량 가시성을 유지하는 연쇄적인 정책 효과를 강화할 것입니다.

주요 도시 지역에서는 주요 집계 플랫폼이 음식점에서 퇴비화 가능한 그릇, 컵, 수저의 사용을 의무화하고 있으며, 이는 2024년에 기록된 지자체의 폐기물 전환 목표와 소비자 선호도 추세에 부합하는 조치입니다. 배송료 체계로 인해 재료비 상승은 은폐되므로 사업자는 브랜드 이미지와 매립처리 비용 절감에 집중하고 있습니다. 체인점에서 시범 도입한 결과, 폐기 비용이 15-20% 절감되어시 조례 준수가 용이해졌습니다. 이러한 요구사항은 클라우드 키친 네트워크에도 영향을 미쳐 소스 및 반찬용 연포장에 대한 수요를 확대하고 있습니다.

최근 아시아태평양과 라틴아메리카에서 바이오수지를 완전히 분해할 수 있는 고온 퇴비화 플랜트의 도입이 매립지 회피와 메탄 배출의 위험을 초래하여 환경 주장을 훼손할 수 있습니다. 지자체의 자금 제한과 인허가 장벽으로 인해 시설 가동이 지연되고 있는 반면, 민간 사업자들은 혼합식품 및 포장폐기물 수용 기준의 명확화를 기다리고 있습니다. 처리 능력이 확대되기 전까지는 적절한 폐기물 처리 옵션이 없는 지역으로의 판매가 제한되어 생분해성 플라스틱 포장 시장의 급속한 보급을 억제하는 요인으로 작용할 것입니다.

소재 유형별 생분해성 플라스틱 포장 시장 규모는 2025년 65.92%의 점유율을 차지한 폴리유산(PLA)에 편중되어 있습니다. 그러나 폴리하이드록시알카노에이트(PHA)는 24.62%로 가장 높은 CAGR 전망을 보이고 있습니다. PHA는 해양 환경에서 생분해성이 인정되어 해안 폐기물 규제 강화에 대응할 수 있으며, 섬 지역 및 항만 도시를 위한 빨대, 수저, 고배리어성 파우치에 최적의 선택이 될 수 있습니다. 제조업체들은 PHA의 넓은 용융 유동 범위를 활용하여 PLA에서는 성형이 어려운 두꺼운 의약품 바이알과 화장품 용기를 생산하고 있습니다. 또한 미국과 태국에서는 식품용 당류 원료가 아닌 농업 잔재물을 활용한 신규 생산 능력을 발표하여 원료 가격 변동으로부터 격리되는 이점도 있습니다.

PLA는 산업용 퇴비 처리가 존재하는 지역에서는 여전히 비용 경쟁력을 유지하고 있으며, 서유럽의 베이커리용 필름과 열성형 샐러드 용기를 지원하고 있습니다. 지속적인 연구개발을 통해 105℃의 충진 온도를 견딜 수 있는 내열성 인디오 등급이 개발되어 기존의 성능 차이를 줄였습니다. PBAT와 PBS는 내열성 및 화학물질 접촉 용도와 같은 틈새 시장에서 활용되고 있으며, 전분 기반 복합재는 가격 경쟁이 치열한 식료품 가방 프로그램에서 주류를 차지하고 있습니다. 전체 소재 시장 상황은 1세대 비용 우위에서 2세대 성능 우위로 전환하고 있으며, 생분해성 플라스틱 포장 시장의 장기적인 다변화를 촉진하고 있습니다.

2025년 기준 생분해성 플라스틱 포장 시장의 58.12%는 유연성 포장재가 차지할 것으로 예측됩니다. 이는 EC 및 밀키트 배송에 있으며, 운송 비용을 최소화하는 경량 파우치, 랩, 메일러가 그 기반이 됩니다. 개조 라인에서 가공된 필름은 신선식품에 적합한 산소 투과율을 달성하여 2차 포장 없이도 보존 기간을 연장할 수 있습니다. 프리미엄 스낵 브랜드는 제품의 품질을 강조하기 위해 투명화 PLA로 만든 투명 창을 강조하고 있습니다. 한편, PBAT를 배합한 라미네이트는 펑크 저항성을 향상시켰습니다.

커피 포드, 핫 컵 안감, 전자레인지 트레이를 배경으로 경질 포장은 22.45%의 연평균 복합 성장률(CAGR)로 성장을 가속화하고 있습니다. 네이처웍스와 기계 제조업체인 IMA는 큐리그와 네스프레소의 사양을 충족하고 90일 만에 퇴비화되는 턴키 포드 시스템을 출시하여 대량 음료 채널을 개발했습니다. 외식 체인에서는 폴리스티렌 소재의 클램쉘 용기에서 산업용 컴포스터에 대응하는 PHA 라이닝 섬유 소재의 그릇으로 전환이 진행되어 성능과 브랜드 가치의 양립을 실현하고 있습니다. 급성장하고 있는 경질 용기 부문은 기능성의 향상이 기존 기술의 우위를 잠식하고 생분해성 플라스틱 포장 시장의 잠재적 매출 규모를 확대하는 실례를 보여주고 있습니다.

생분해성 플라스틱 포장 시장 보고서는 재료 유형(전분 기반 복합재, 폴리유산(PLA) 등), 포장 유형(연포장과 경질 포장), 최종 사용 산업(식품, 음료, 외식업 등), 퇴비화 가능성(가정용 퇴비화 가능, 산업용 퇴비화 가능), 지역(북미, 유럽, 아시아, 아시아태평양, 중동, 아프리카, 남미) 태평양, 중동/아프리카, 남미)로 분석되고 있습니다. 시장 예측은 금액(USD)으로 제공됩니다.

유럽의 성숙한 퇴비화 인프라와 종합적인 규제 환경으로 인해 2025년 생분해성 플라스틱 포장 시장에서 35.21%의 점유율을 차지할 것으로 예측됩니다. 지역 수지 제조업체들은 통일된 EN 표준과 확대된 생산자책임제도(EPR) 수수료로 인한 예측 가능한 수요의 혜택을 누리고 있으며, 가공업체들은 파리, 베를린, 마드리드에서 현재 널리 보급되고 있는 고성장 식품 배송 플랫폼에 대한 근접성에서 혜택을 누리고 있습니다. 분리수거 유기성 폐기물 수거에 대한 정부 보조금도 포장재 채택을 더욱 촉진하여 유럽의 단기적인 리더십을 더욱 공고히 하고 있습니다.

아시아태평양은 인도, 중국, 태국이 재활용이 어려운 포장 형태에 대한 단계적 금지를 시행하고 있는 가운데 가장 높은 24.02%의 연평균 복합 성장률(CAGR)을 기록했습니다. 중국에서는 2027년까지 주요 도시의 '비분해성' 플라스틱 규제가 쇼핑백에서 테이크아웃 용기로 확대되고, 카사바나 쌀겨를 원료로 하는 지역 밀착형 공장 설립을 촉진하고 있습니다. 인도에서는 주별 규제가 여전히 분절되어 있지만, 인구 커버리지가 누적됨에 따라 다국적 패스트푸드 체인이 생분해성 코팅 기술의 표준화를 추진하고 있습니다. 호주 및 뉴질랜드도 종합적인 일회용 플라스틱 금지 조치를 도입하여 오세아니아 전역에서 즉각적인 대체 수요를 불러일으키고 있습니다.

북미에서는 식품 배송 의무화 및 포춘지 선정 500대 기업의 내부 탄소 가격 책정을 활용하여 채택을 촉진하고 있지만, 산업 퇴비화의 지역적 보급률은 여전히 불균등합니다. 상파울루, 멕시코시티와 같은 라틴아메리카의 거대 도시에서는 시범 퇴비화 허브를 도입하여 보다 광범위한 성장 기반을 마련하고 있습니다. 중동 및 아프리카에서는 매립지 부족과 관광 산업 주도의 플라스틱 금지로 인해 특히 걸프협력회의(GCC)의 접객업 부문에서 틈새 시장이 형성되고 있습니다. 전반적으로 관할권별 정책 속도와 인프라 투자 패턴이 생분해성 플라스틱 포장 시장의 지역별 성장 차이를 설명합니다.

Biodegradable Plastic Packaging market size in 2026 is estimated at USD 3.62 billion, growing from 2025 value of USD 3.01 billion with 2031 projections showing USD 9.04 billion, growing at 20.12% CAGR over 2026-2031.

The strong trajectory reflects simultaneous regulatory mandates, corporate carbon-pricing policies, and rapid advances in bio-resin processing that together improve economic viability for compostable formats. Brand owners now prefer global rather than regional packaging specifications, allowing large volume contracts that lower per-unit costs. Material innovation continues to cut performance gaps with conventional polymers; marine-degradable PHA and heat-resistant PBAT variants now satisfy demanding barrier and temperature requirements. In parallel, municipal waste-diversion targets push food-delivery and retail sectors to adopt certified compost-ready solutions, creating predictable offtake for resin suppliers. The biodegradable plastic packaging market therefore enjoys clear line-of-sight demand that compensates for still-volatile agricultural feedstock pricing.

The European Union's 2024 Single-Use Plastic Directive immediately raised demand for certified compostable food-contact packs, replacing difficult-to-recycle items such as cutlery and clamshells. India's statewide prohibitions expose more than 1.8 billion consumers to the same shift, forcing multinationals to harmonize global specifications and unlocking scale economies for resin plants. Penalties that exceed the premium on bio-materials further accelerate adoption. Australia's 2024 bans reinforce a cascading policy effect that sustains volume visibility for producers.

Leading aggregators mandate that restaurants use compostable bowls, cups, and cutlery in top metropolitan areas, aligning with municipal diversion goals and consumer preference tracking recorded in 2024. Delivery fee structures hide the material premium, so operators focus on brand perception and landfill fee savings. Chain pilots report 15-20% lower disposal costs and smoother compliance with city ordinances. The requirement has spilled into cloud kitchen networks, amplifying flexible-pack demand for sauces and sides.

Adoption in Asia-Pacific and Latin America recently outpaced the build-out of high-temperature composting plants capable of fully degrading bio-resins, risking landfill diversion and methane release that undermine environmental claims . Municipal funding limitations and permitting hurdles delay facility commissioning, while private operators await clearer acceptance rules for mixed food and packaging waste. Until capacity expands, sales into regions without adequate end-of-life options are capped, tempering the otherwise rapid uptake of the biodegradable plastic packaging market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The biodegradable plastic packaging market size for material types remained skewed toward Polylactic Acid, which held 65.92% share in 2025, yet Polyhydroxyalkanoates posted the strongest 24.62% CAGR outlook. PHA's ability to biodegrade in marine settings satisfies growing coastal-waste legislation, making it the preferred option for straws, cutlery, and high-barrier pouches targeting island and port cities. Manufacturers exploit its broad melt-flow window to mold thicker pharmaceutical vials and personal-care jars that PLA struggles to handle. The segment also benefits from fresh capacity announcements in the United States and Thailand that leverage agricultural residues instead of food-grade sugar sources, insulating it from feedstock swings.

PLA remains cost-competitive where industrial composting exists, supporting bakery films and thermoformed salad tubs in Western Europe. Continuous R&D produced higher-heat Ingeo grades that withstand 105 °C filling temperatures, narrowing earlier performance gaps. PBAT and PBS serve niche heat-resistant or chemical-contact applications, while starch blends dominate ultra-price-sensitive grocery bag programs. The overall material landscape shows a transition from first-generation cost leadership to second-generation performance leadership, reinforcing the long-term diversification of the biodegradable plastic packaging market.

Flexible formats commanded 58.12% of the biodegradable plastic packaging market share in 2025, underpinned by light-weighted pouches, wraps, and mailers that minimize freight costs for e-commerce and meal-kit delivery. Films processed on retrofitted lines achieve oxygen transmission rates suitable for fresh produce, extending shelf life without secondary wraps. Premium snack brands emphasize transparent windows made from clarified PLA to showcase product integrity, while laminates incorporating PBAT improve puncture resistance.

Rigid formats accelerate at 22.45% CAGR on the back of coffee pods, hot-cup linings, and microwave-ready trays. NatureWorks and machine supplier IMA released a turnkey pod system that meets Keurig and Nespresso specifications and composts in 90 days, opening high-volume beverage channels. Foodservice chains shift from polystyrene clamshells to PHA-lined fiber bowls compatible with industrial composters, satisfying performance and brand-equity goals. The fast-growing rigid segment illustrates how functionality gains erode legacy dominance and broaden total addressable revenue for the biodegradable plastic packaging market.

The Biodegradable Plastic Packaging Market Report is Segmented by Material Type (Starch Blends, Polylactic Acid (PLA), and More), Packaging Type (Flexible Packaging and Rigid Packaging), End-Use Industry (Food, Beverage, Foodservice, and More), Compostability (Home-Compostable and Industrial-Compostable), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

Europe's mature composting infrastructure and comprehensive regulatory backdrop secured 35.21% biodegradable plastic packaging market share in 2025. Regional resin producers benefit from cohesive EN standards and predictable demand created by extended-producer-responsibility fees, while converters profit from proximity to high-growth food delivery platforms now ubiquitous in Paris, Berlin, and Madrid. Government subsidies for separate organic waste collection further aid pack adoption, cementing Europe's near-term leadership.

Asia-Pacific generates the strongest 24.02% CAGR as India, China, and Thailand enforce phased bans on difficult-to-recycle packaging formats. Chinese directives targeting "non-degradable" plastics in tier-one cities escalate from carrier bags to takeaway containers by 2027, spawning localized plants using cassava and rice-husk feedstocks. India's state regulations remain fragmented, yet cumulative population coverage draws multinational quick-service restaurants to standardize compostable coating technologies. Australia and New Zealand also adopted comprehensive single-use plastic prohibitions, driving immediate substitution demand throughout Oceania.

North America leverages food-delivery mandates and internal carbon-pricing at Fortune 500 corporations to propel adoption, although regional coverage of industrial composting remains uneven. Latin American megacities such as Sao Paulo and Mexico City deploy pilot composting hubs, setting the stage for broader growth. In the Middle East and Africa, landfill scarcity and tourism-driven plastic bans create niche opportunities, especially in Gulf Cooperation Council hospitality sectors. Overall, jurisdictional policy cadence and infrastructure investment patterns explain divergent regional growth in the biodegradable plastic packaging market.