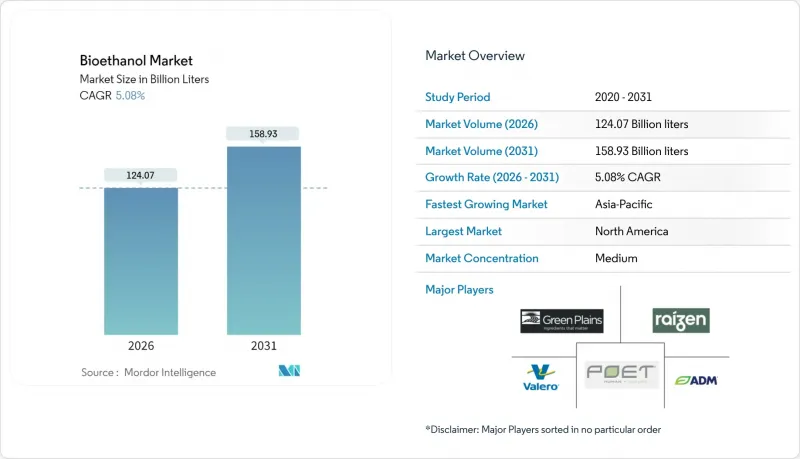

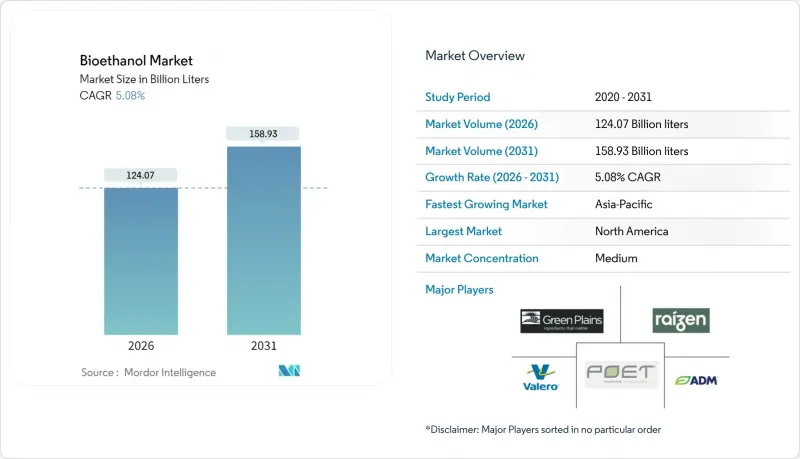

바이오에탄올 시장은 2025년에 1,180억 7,000만 리터로 평가되며, 2026년 1,240억 7,000만 리터에서 2031년까지 1,589억 3,000만 리터에 달할 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 5.08%로 전망됩니다.

소형차의 전동화가 진행되는 가운데, E10-E20 혼합연료에 대한 지속적인 정책적 지원, 에탄올에서 제트연료로의 전환에 대한 관심 증가, 원가 우위의 원료 공급이 이러한 성장 궤도를 지원하고 있습니다. 북미의 옥수수 기반 생산 능력, 브라질의 사탕수수 유연성, 중동 투자자들의 새로운 자본 유입으로 공급 안정성이 강화되고 있습니다. 한편, 아시아태평양 각국 정부는 지역 수요 기반을 확대하는 적극적인 블렌딩 목표를 빠르게 추진하고 있으며, 정유사들은 강화되는 ESG 지표를 충족하기 위해 저탄소 에탄올을 도입하고 있습니다. 이러한 요인들이 결합되어 바이오에탄올 시장은 경쟁적인 운송 부문 탈탄소화 경로에 대한 저항력을 유지하고 있습니다.

강화된 혼합 의무는 예측 가능한 기저부하 수요를 창출하여 바이오에탄올 시장을 원유 가격 변동으로부터 보호하고, 생산 능력 확대를 보장합니다. 일본의 전국적인 E10 도입과 E20 테스트 지역, 브라질의 27% 상한 유연성, 인도의 30% 목표 가속화와 함께 연간 조달량을 늘리고 신규 플랜트 투자를 촉진하고 있습니다. 규제 당국은 연료 품질 기준, 국내 조달 규칙, 수입 규제를 통해 혼합 목표가 서류상의 크레딧이 아닌 실제 공급으로 이어지도록 보장하고 있습니다. 이러한 정책은 전기화가 진행 중임에도 불구하고 바이오에탄올 시장을 국가 에너지 안보 전략의 구조적 요소로 바꾸고 있습니다.

투자자들의 감시와 엄격한 탄소 기준에 직면한 정제업체들은 저탄소 강도 바이오에탄올을 단순한 컴플라이언스 요소가 아닌 전략적 차별화 요소로 인식하기 시작했습니다. 캘리포니아주의 2024년 저탄소 연료 기준 개정으로 탄소 기준이 강화되고, ISCC 등 인증제도에 따른 공급이 우대됩니다. EU의 개정된 재생에너지 지침도 마찬가지로 추적 가능하고 지속가능한 조달 경로를 가진 에탄올을 우대하고 있습니다. 이에 대응하여 BP 등은 밴지 바이오에너지아를 14억 달러에 인수하여 업스트림 공정을 수직계열화했습니다. 원료 확보와 수명주기 배출 관리를 한 번에 실현했습니다. 재생 연료 함량이 의무화 기준보다 낮은 시장에서는 프리미엄 수요가 발생하여 저탄소 생산자에게 유리한 가격 차이가 유지되고 있습니다.

전기자동차(EV)의 보급 확대는 주요 시장에서 휘발유 수요의 상한선을 낮출 것입니다. 노르웨이에서는 2024년 신차 판매량의 94%가 전기자동차이며, 중국에서도 35%를 넘어섰습니다. 국제에너지기구(IEA)는 2030년까지 세계 소형차 시장에서 전기자동차 점유율이 30%를 나타낼 것으로 전망하고 있습니다. 그 결과, 정제업체는 혼합원료 공급원 감소에 직면하고, 바이오에탄올 생산업체는 항공연료, 대형 운송 및 수출 주도 전략으로 전환해야 하는 상황입니다. 신흥 국가의 차량 전동화가 늦어지면서 지역별 수요 격차가 지속되고 있으며, 바이오에탄올 시장의 지역적 다변화를 위한 기회로 작용하고 있습니다.

2025년 기준 바이오에탄올 시장 규모에서 옥수수 유래 생산량은 58.12%를 차지했습니다. 이는 미국 중서부, 브라질 마투그로소 주에서의 확장, 그리고 잘 구축된 철도 및 내항선을 통한 물류망에 힘입은 것입니다. 생산자들은 효소 기술의 발전과 제품별 가치 향상(특히 가축 사료용 증류 찌꺼기 및 음료용 CO2 포집)을 활용하여 단위 비용 절감과 탄소 점수를 개선하고 있습니다. 중서부 지역의 탄소 포집 및 지하 저장 클러스터에 대한 지속적인 투자는 수명주기 성능에 대한 신뢰성을 더욱 높이고 있습니다.

밀 에탄올은 2031년까지 연평균 복합 성장률(CAGR) 5.45%를 나타낼 것으로 예측되며, 주요 원료 중 가장 빠른 성장이 예상됩니다. 유럽 사업자들은 국내 곡물 다양화를 위한 정책적 인센티브를 활용하고, 호주의 풍작 사이클은 수출 기회를 제공합니다. 단백질 프리미엄의 상승으로 밀 증류 찌꺼기는 가축 사료로 매력적이어서 전분 비용 상승을 상쇄할 수 있습니다. 고비중 발효와 분별 증류를 가능하게 하는 기술 혁신은 공장 가동률을 향상시키고, 바이오에탄올 시장에서 밀의 경쟁력을 강화합니다.

사탕수수, 카사바, 신흥 리그노셀룰로오스 원료 등 다른 원료들은 틈새 시장이지만 전략적인 공급량을 담당하며 날씨에 따른 작황 변동에 대한 헤지 기능을 수행합니다. 브라질 사탕수수는 사탕수수 연소 코제너레이션을 통해 구조적 비용 우위를 유지하고, 인도네시아의 니파야자, 멕시코의 아가베 시범사업은 미활용지 생산 개발을 목표로 하고 있습니다. 이러한 다각화는 가격 변동을 완화하고 식량 작물 대체를 최소화하려는 정책 입안자들의 요구와도 부합합니다.

바이오에탄올 시장 보고서는 원료 유형(사탕수수, 옥수수, 옥수수, 밀, 기타 원료), 용도(자동차 및 운송, 식품 및 음료, 제약, 화장품 및 퍼스널케어, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카) 별로 분류되어 있습니다. 시장 예측은 수량(리터) 단위로 제공됩니다.

북미는 잘 구축된 옥수수 인프라, 안정적인 재생 연료 기준(RFS) 목표, 주정부 차원의 저탄소 연료 구상의 지원으로 2025년에도 전 세계 물량의 55.10%를 유지했습니다. 생산자는 탄소 포집, 직접 공기 회수, 파이프라인 네트워크를 통합하여 옥수수 에탄올의 탄소 강도를 낮추어 고부가가치 크레딧 시장에 적응하고 있습니다. 캐나다는 밀과 옥수수의 원료 클러스터를 활용하고, 멕시코 수요 증가는 미국의 수출을 흡수하여 지역 균형을 안정화시키는 대륙 간 무역 흐름을 강화하고 있습니다.

아시아태평양은 2031년까지 5.74%의 가장 높은 예측 CAGR을 나타낼 것입니다. 인도의 30% 혼합 목표와 중국의 수입 수요가 소비를 확대하기 때문입니다. 지역 정부는 바이오에탄올 확대를 농촌 소득 지원 및 외화 절약 방안으로 인식하고, 다원료 바이오 정제 시설에 대한 현지 투자를 촉진하고 있습니다. 태국, 필리핀, 베트남은 농업 현대화 계획에 따라 혼합 의무화를 추진하고 있으며, 인도네시아는 식량 작물 제약을 피하기 위해 니파 야자 유래 에탄올 경로를 시범 도입 중입니다.

유럽에서는 지속가능성 인증을 중요시하며, 엄격한 온실가스 감축 기준을 충족하는 잔류성 에탄올을 우선시하고 있습니다. 독일과 프랑스의 할당제도가 수요를 지원하고, 영국의 재생 수송연료 의무화(RTFO)는 SAF를 우선시함으로써 에탄올에서 제트연료로의 전환 경로를 간접적으로 촉진하고 있습니다. 브라질이 주도하는 남미에서는 특히 UAE의 135억 달러 투자 등 사탕수수-옥수수 코제너레이션을 통합한 자산 확대를 위해 해외 자본이 유입되고 있습니다. 아프리카은 여전히 틈새 시장이지만, 에탄올을 가정용 에너지 대안으로 자리매김하고 있는 FAO의 청정 조리 솔루션 프로그램을 계기로 성장세를 이어가고 있습니다.

The Bioethanol Market was valued at 118.07 billion litres in 2025 and estimated to grow from 124.07 billion litres in 2026 to reach 158.93 billion litres by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

Continued policy backing for E10-E20 blends, growing interest in ethanol-to-jet fuel, and cost-advantaged feedstock supply underpin this trajectory even as light-duty vehicle electrification advances. North American corn-based capacity, Brazilian sugarcane flexibility, and fresh capital inflows from Middle Eastern investors reinforce supply security. Meanwhile, Asia-Pacific governments fast-track aggressive blending targets that deepen regional demand pools, and refiners pursue low-carbon ethanol to satisfy tightening ESG metrics. Together, these factors sustain the bioethanol market's resilience against competing transport decarbonization pathways.

Strengthened blending requirements are creating predictable baseload demand that insulates the bioethanol market from crude price swings while locking in capacity expansion. Japan's nationwide E10 roll-out and pilot E20 zones, Brazil's 27% ceiling flexibility, and India's accelerated 30% target together lift annual offtake volumes and encourage new plant investment. Regulatory agencies back compliance through fuel-quality standards, domestic content rules, and import controls, ensuring blend targets translate into physical deliveries rather than paper credits. These policies turn the bioethanol market into a structural element of national energy security strategies even as electrification gains momentum.

Refiners facing investor scrutiny and stringent carbon standards now view low-intensity bioethanol as a strategic differentiator instead of a mere compliance component. California's 2024 Low Carbon Fuel Standard update tightened carbon benchmarks, rewarding supplies certified under schemes such as ISCC. The EU's revised Renewable Energy Directive likewise privileges traceable, sustainably sourced ethanol. In response, companies like BP vertically integrated upstream via the USD 1.4 billion acquisition of Bunge Bioenergia, securing feedstock and lifecycle emission control in one step. Premium demand emerges in markets where renewable-content uptake exceeds mandate floors, sustaining price spreads favorable to lower-carbon producers.

Soaring EV adoption trims gasoline demand ceilings in core markets. Norway hit 94% EV penetration for 2024 new car sales, China surpassed 35%, and the IEA forecasts a 30% global light-vehicle share by 2030. As a result, refiners face shrinking blend pools, compelling bioethanol producers to pivot toward aviation, heavy-duty transport, and export-led strategies. Regional demand divergence persists because emerging economies lag in vehicle electrification, creating opportunities for geographic diversification within the bioethanol market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Corn-based output contributed 58.12% of the bioethanol market size in 2025, anchored by the U.S. Midwest, Brazil's Mato Grosso expansion, and well-established rail and barge logistics. Producers leverage enzyme advances and co-product valorization, notably distillers' grains for livestock feed and captured CO2 for beverages, to compress unit costs and improve carbon scores. Continuing investments in carbon capture and underground storage clusters across the Midcontinent further enhance lifecycle performance credentials.

Wheat ethanol is projected to record a 5.45% CAGR through 2031, the fastest growth among mainstream feedstocks. European players harness policy incentives for domestic grain diversification, while Australia's bumper wheat cycles offer export opportunities. Rising protein premiums make wheat distillers' grains attractive to livestock feeders, offsetting higher starch costs. Technology breakthroughs enabling high-gravity fermentation and fractional distillation improve plant utilization rates, strengthening wheat's competitiveness within the bioethanol market.

Other feedstocks, such as sugarcane, cassava, and emerging lignocellulosic sources, supply niche but strategic volumes that hedge against weather-induced crop swings. Brazilian sugarcane retains a structural cost edge via bagasse-fired cogeneration, while Indonesia's nipa palm and Mexico's agave pilots aim to unlock marginal-land production. Such diversification dampens price volatility and aligns with policymakers' pressure to minimize food-crop displacement.

The Bioethanol Market Report is Segmented by Feedstock Type (Sugarcane, Corn, Wheat, and Other Feedstock), Application (Automotive and Transportation, Food and Beverages, Pharmaceutical, Cosmetics and Personal Care, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Liters).

North America maintained 55.10% of global volume in 2025 thanks to entrenched corn infrastructure, stable Renewable Fuel Standard targets, and supportive state-level Low Carbon Fuel initiatives. Producers integrate carbon capture, direct air capture, and pipeline networks that compress the carbon intensity of corn ethanol, qualifying it for high-value credit markets. Canada leverages wheat and corn feedstock clusters, whereas Mexico's demand uptick absorbs U.S. exports, reinforcing continental trade flows that stabilize regional balance.

Asia-Pacific records the highest forecast CAGR at 5.74% through 2031 as India's 30% blend target and China's import appetite amplify consumption. Regional governments frame bioethanol expansion as rural income support and foreign-exchange savings, encouraging local investment in multi-feedstock biorefineries. Thailand, the Philippines, and Vietnam advance blend mandates aligned with agricultural modernization plans, while Indonesia pilots nipa-to-ethanol routes to sidestep food-crop constraints.

Europe emphasizes sustainability certification and favors residue-based ethanol that fulfills stringent greenhouse-gas savings thresholds. Quota systems in Germany and France anchor demand, and the United Kingdom's Renewable Transport Fuel Obligation prioritizes SAF, indirectly boosting ethanol-to-jet pathways. South America, dominated by Brazil, attracts foreign capital, notably the UAE's USD 13.5 billion commitment, to expand integrated assets that marry sugarcane, corn, and cogeneration. Middle East and Africa remain niche but rising, catalyzed by FAO programs for clean cooking solutions that position ethanol as a household energy alternative.