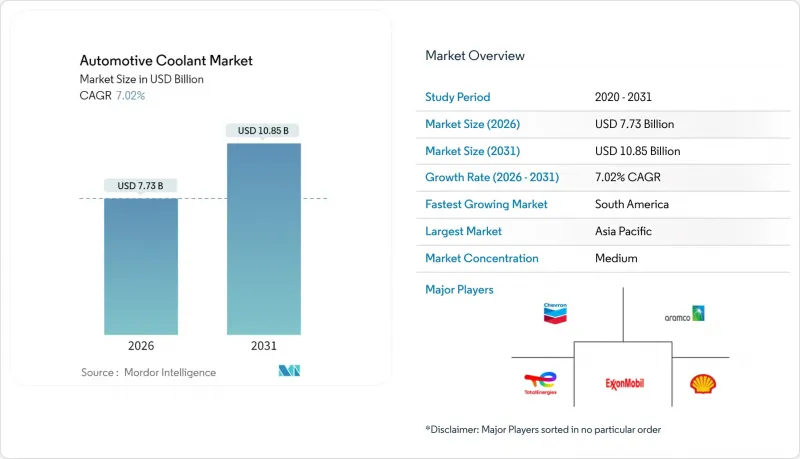

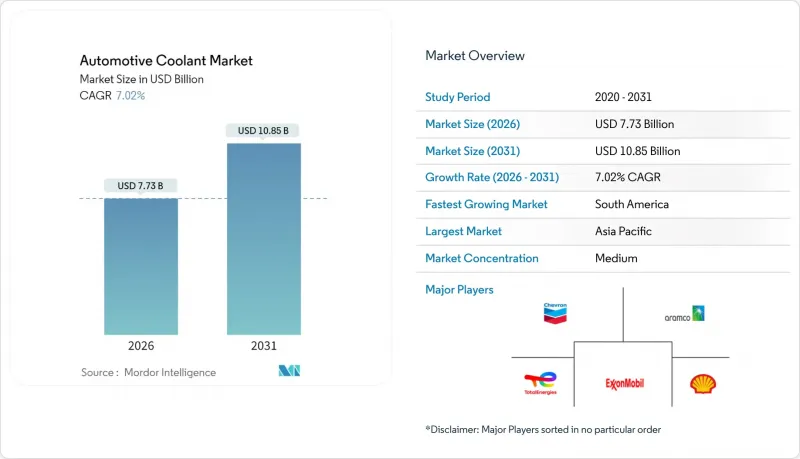

자동차용 냉각액 시장은 2025년 72억 2,000만 달러에서 2026년에는 77억 3,000만 달러로 성장하며, 2026-2031년에 CAGR 7.02%로 추이하며, 2031년까지 108억 5,000만 달러에 달할 것으로 예측됩니다.

전기자동차 생산 증가, 잦은 냉각수 교환이 필요한 내연기관 차량의 노후화, 그리고 강화되는 열관리 규제가 자동차 냉각수 시장의 꾸준한 확대에 기여하고 있습니다. 공급업체는 교체 주기를 연장하는 부가가치 화학 기술로 이익을 얻고, 차량 운영자는 고품질 배합으로 다운타임 비용을 절감할 수 있습니다. 전동화는 저전도성, 유전체 냉각액의 대량생산을 통해 제품 수요를 재구성하고 기존 에틸렌글리콜 계열 제품군 위에 새로운 매출층을 창출하고 있습니다.

차량의 노후화는 현대의 장수명 화합물에 비해 오래된 차량일수록 냉각수 서비스 간격이 짧아지기 때문에 지속적인 애프터마켓 수요를 창출합니다. 특히 신흥 시장에서의 세계 자동차 보유대수 확대는 신차 판매 증가보다 더 많은 교체 수요를 창출하고 있습니다. 인도 자동차 애프터마켓은 국내 차량 생산을 촉진하는 PLI(생산 연동형 보조금), PM E-DRIVE(PM E-DRIVE) 등 정부 정책에 힘입어 내연기관차(ICE) 차량의 대규모 운행을 유지하면서 큰 규모에 도달할 것으로 예측됩니다. 이러한 추세는 북미와 유럽의 노후화된 차량이 주요 서비스 주기에 기존 냉각 시스템에서 장수명 냉각 시스템으로 전환하는 과정에서 특히 애프터마켓 냉각수 공급업체에 도움이 될 것입니다. 대형 상용차는 이러한 추세를 가장 잘 보여주고 있으며, 차량 운영자들은 더 많은 차량을 관리하면서 유지보수 비용을 절감하기 위해 장수명 냉각수 채택을 확대하고 있습니다.

OEM 업체들은 15만 마일(약 24만km) 이상의 서비스 주기를 달성하기 위해 유기산 기술(OAT) 및 하이브리드 배합을 표준화하고 있으며, 이로 인해 냉각수 수요 패턴이 '양'에서 '가치'에 기반한 소비로 근본적으로 변화하고 있습니다. 제너럴 모터스(GM)의 DexCool 채택이 그 시초로, 기존 냉각수의 3만 마일(약 4만 8천km) 간격에 비해 서비스 수명을 15만 마일(약 24만km)로 연장했습니다. 이러한 변화로 인해 차량 수명주기 동안 총 냉각수 소비량은 감소하는 반면, 단위당 냉각수의 가치와 복잡성은 증가하고 있습니다. 메르세데스-벤츠 등 유럽 OEM 업체들은 특정 용도에 대해 15년의 서비스 주기를 지정하고 있으며, 이는 안정성과 부식 방지 성능이 강화된 프리미엄 냉각수 화학 성분에 대한 수요를 창출하고 있습니다. 이러한 전환은 호환되지 않는 냉각수 유형을 혼합하면 부품 고장을 가속화할 수 있으므로 서비스 기술자에게 호환성 요구 사항에 대해 교육하는 동시에 여러 화학 성분 유형을 재고로 보유해야 하는 과제를 추적 시장 공급업체에 안겨주고 있습니다.

에틸렌글리콜 가격 변동은 냉각수 생산 비용에 직접적인 영향을 미치고, 공급망 혼란은 냉각수 제조업체의 이익률을 압박하는 동시에 가격에 민감한 부문 시장 성장을 제한할 수 있습니다. 세계 에틸렌 글리콜 가격의 변동은 냉각수 제조업체의 안정적인 가격 유지 능력에 영향을 미치며, 특히 비용 민감도가 높은 신흥 시장 진출에 부정적인 영향을 미칩니다. 이러한 문제는 친환경 바이오 글리세린 대체품이 비용에 민감한 애프터마켓 분야에서 채택을 제한하는 높은 가격대로 인해 더욱 심화되고 있습니다. 수입 의존도와 환율 변동에 따른 리스크를 줄이기 위해 알테코와 같은 제조업체들이 중국에 현지 생산기지를 설립하는 등 공급망 탄력성이 중요해지고 있습니다. 특히 수직 통합이나 장기 공급 계약이 없는 중소 냉각액 제조업체의 경우, 원자재 제약은 산업 구조조정을 가속화할 수 있습니다.

에틸렌 글리콜은 검증된 성능 특성과 탄탄한 공급망을 바탕으로 2025년 기준 자동차 냉각제 시장의 51.92%를 차지하며 시장 리더의 지위를 유지할 것으로 예측됩니다. 한편, 글리세린은 2031년까지 연평균 복합 성장률(CAGR) 9.01%로 가장 빠르게 성장하는 부문으로 부상하고 있으며, 이는 환경적 지속가능성에 대한 요구와 바이오 화학의 채택을 반영하고 있습니다. 에틸렌글리콜 부문은 특히 규모의 경제가 경쟁력 있는 가격 책정을 지원하는 아시아태평양의 생산 기지에서 성숙한 제조 인프라와 비용 우위의 이점을 누리고 있습니다.

이 부문의 동향은 산업 전반의 변화를 반영하고 있으며, 전통적 화학 분야의 리더십이 지속가능성을 추구하는 혁신에 의한 변화에 직면하고 있습니다. 이로 인해 바이오 기술을 보유한 공급업체에게는 기회가 생기는 반면, 기존 에틸렌글리콜 생산업체는 재생한 대체품 개발에 나서지 않으면 시장 점유율 침식 위험에 직면하게 될 것입니다.

승용차는 2025년 기준 자동차 냉각수 시장에서 45.52%의 점유율을 차지할 것으로 예측됩니다. 이는 E-Commerce의 확대와 라스트 마일 배송의 전동화로 인해 특별한 열 관리 요구 사항이 발생했기 때문입니다. 소형 상용차는 2031년까지 연평균 복합 성장률(CAGR) 7.12%로 가장 빠르게 성장하는 부문입니다. 승용차 부문은 대량 생산과 표준화된 냉각수 사양의 혜택을 누리고 있지만, 장수명 냉각수 도입으로 교체 수요가 감소하여 성장이 둔화될 것으로 예측됩니다. 상용차 용도에서는 연장된 서비스 간격과 가혹한 운전 조건에 대응할 수 있는 고성능 냉각수가 요구됩니다. 대형 부문에서는 100만 마일(약 160만km)의 서비스 수명 달성을 위해 OAT(옥시메틸렌계) 배합의 채택이 확대되고 있습니다. 중대형 상용차는 차량의 구매력과 전문적인 유지보수 관행으로 인해 기존 대체품보다 프리미엄 냉각수 배합이 선호되는 이점이 있습니다.

이 부문의 변화는 보다 광범위한 운송의 전동화 추세를 반영하고 있습니다. 상업용 차량은 총소유비용의 이점 때문에 EV 도입을 주도하고 있으며, 특수 배터리 열 관리 냉각액에 대한 수요를 창출하고 있습니다. 2032년까지 PEV의 대폭적인 보급을 의무화하는 EPA 규제는 특히 중형 배송 차량에 영향을 미칩니다. 아마존, 페덱스 등 차량 구매자들이 전용 열 관리 솔루션을 필요로 하는 전기 파워트레인의 조기 도입을 추진하고 있는 분야입니다.

아시아태평양은 2025년 기준 자동차 냉각수 시장의 34.53%를 차지하며 가장 규모가 큰 지역 점유율을 차지할 것으로 예측됩니다. 이는 중국의 엄격한 EV 열관리 규제와 정부의 제조 장려책에 힘입은 인도의 자동차 생산 급증에 힘입은 것입니다. 중국 GB 표준은 EV용 냉각수에 특정 전기 전도도 제한을 요구하고 있으며, 이는 열 성능과 전기 안전 요구 사항의 균형을 맞추는 특수 배합에 대한 수요를 창출하고 있습니다. 인도에서는 PLI(생산 연동형 보조금) 및 PM E-DRIVE 정책에 힘입어 자동차 애프터마켓이 성장하면서 국내 OEM들이 열 관리 공급망을 구축하는 가운데, 기존 및 EV 전용 냉각수 배합에 대한 지속적인 수요가 발생하고 있습니다. 일본과 한국은 첨단 EV 기술 개발에 기여하고 있으며, 배터리 및 파워 일렉트로닉스 냉각 용도의 특수 유전체 냉각액을 필요로 하고 있습니다.

남미는 2031년까지 연평균 복합 성장률(CAGR) 6.67%로 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 아르헨티나와 브라질의 자동차 통합 정책으로 차량 인증 및 부품 승인 절차가 간소화되는 동시에 증가하는 E-Commerce 수요에 대응하기 위한 상용차 생산이 확대되고 있기 때문입니다. 이 지역의 성장 가속화는 두 주요 시장에 공급되는 냉각수 제조업체의 규제 장벽을 낮추는 상호 승인 협정으로 인해 지역 사업에서 규모의 경제 효과를 창출하고 있습니다.

북미와 유럽은 성숙한 시장이며, 성장률은 완만합니다. 이는 장수명 냉각수 채택으로 교체 빈도가 감소하는 한편, 규제 요건이 프리미엄 배합으로 사양 업그레이드를 촉진하고 있기 때문입니다. 특히 유럽 시장에서는 REACH 규제와 PFAS 규제에 따른 변화 압력에 직면하여 바이오 냉각제 대체품이 유리한 상황입니다. 이는 지속가능한 화학 기술을 가진 공급업체에게 기회를 창출하고 있습니다. 북미의 차량 운영자들은 유지보수 비용 절감을 위해 장기 사용 냉각제 도입을 가속화하고 있으며, 이는 애프터마켓의 물량 성장에 구조적인 역풍으로 작용하는 반면, OEM 충전 용도에는 혜택을 가져다주고 있습니다.

The automotive coolant market is expected to grow from USD 7.22 billion in 2025 to USD 7.73 billion in 2026 and is forecast to reach USD 10.85 billion by 2031 at 7.02% CAGR over 2026-2031.

Rising electric-vehicle production, aging internal-combustion fleets that require frequent fluid changes, and stricter thermal-management regulations all contribute to the steady expansion of the automotive coolant market. Suppliers gain from value-added chemistry that lengthens drain intervals, while fleet operators reduce downtime costs through premium formulations. Electrification reshapes product needs by pushing low-conductivity, dielectric coolants into volume production, creating a fresh revenue layer atop traditional ethylene-glycol lines.

Fleet aging dynamics create sustained aftermarket demand as older vehicles require more frequent coolant service intervals compared to modern extended-life formulations. The global vehicle parc expansion, particularly in emerging markets, generates replacement demand that outpaces the growth of new vehicle sales. India's automotive aftermarket is projected to reach a significant scale, driven by government policies such as PLI and PM E-DRIVE that incentivize domestic vehicle production while maintaining substantial ICE fleet operations. This trend particularly benefits aftermarket coolant suppliers as aging fleets in North America and Europe transition from conventional to long-life coolant systems during major service intervals. Heavy-duty commercial vehicles demonstrate this pattern most clearly, where fleet operators increasingly adopt extended-life coolants to reduce maintenance costs while managing larger vehicle populations.

Original equipment manufacturers are standardizing on organic acid technology and hybrid formulations to achieve service intervals exceeding 150,000 miles, fundamentally altering coolant demand patterns from volume-based to value-based consumption. General Motors' DexCool adoption established the template, with service life extending to 150,000 miles compared to conventional coolants' 30,000-mile intervals. This shift reduces total coolant volume consumption per vehicle over its lifetime while increasing per-unit coolant value and complexity. European OEMs, such as Mercedes-Benz, specify 15-year service intervals for certain applications, creating demand for premium coolant chemistries with enhanced stability and corrosion protection. The transition challenges aftermarket suppliers to stock multiple chemistry types while educating service technicians on compatibility requirements, as mixing incompatible coolant types accelerates component failures.

Ethylene glycol price fluctuations directly impact coolant manufacturing costs, with supply chain disruptions creating margin pressure for coolant producers while potentially limiting market growth in price-sensitive segments. Global ethylene glycol pricing volatility affects coolant manufacturers' ability to maintain stable pricing, particularly impacting the penetration of emerging markets, where cost sensitivity remains high. The challenge intensifies as bio-based glycerin alternatives, while environmentally preferred, command premium pricing that limits adoption in cost-conscious aftermarket segments. Supply chain resilience becomes critical as manufacturers like Arteco establish local production facilities in China to mitigate risks associated with import dependency and currency fluctuations. Raw material constraints, particularly for smaller coolant manufacturers lacking vertical integration or long-term supply contracts, can accelerate industry consolidation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Ethylene glycol maintains its market leadership with a 51.92% of the automotive coolant market share in 2025, driven by its proven performance characteristics and established supply chains. Meanwhile, glycerin emerges as the fastest-growing segment, with a 9.01% CAGR through 2031, reflecting environmental sustainability mandates and the adoption of bio-based chemistry. The ethylene glycol segment benefits from mature manufacturing infrastructure and cost advantages, particularly in Asia-Pacific production hubs where scale economies support competitive pricing.

The segment dynamics reflect a broader industry transformation, where traditional chemistry leadership faces disruption from sustainability-driven innovation, creating opportunities for suppliers with bio-based capabilities while challenging established ethylene glycol producers to develop renewable alternatives or risk erosion of their market share.

Passenger cars maintain a 45.52% of the automotive coolant market share in 2025, as e-commerce expansion and last-mile delivery electrification create specialized thermal management requirements. Light commercial vehicles represent the fastest-growing segment, with a 7.12% CAGR through 2031. The passenger car segment benefits from volume production and standardized coolant specifications; however, growth moderates as extended-life coolants reduce the need for replacement. Commercial vehicle applications require higher-performance coolants that can support extended service intervals and severe-duty operation. The heavy-duty segments are increasingly adopting OAT formulations to achieve a 1,000,000-mile service life. Medium- and heavy-duty commercial vehicles benefit from the purchasing power of fleets and professional maintenance practices that favor premium coolant formulations over conventional alternatives.

The segment transformation reflects broader transportation electrification trends, where commercial fleets lead EV adoption due to total cost of ownership benefits, creating demand for specialized battery thermal management coolants. EPA regulations mandating substantial PEV penetration through 2032 particularly impact medium-duty delivery vehicles, where fleet purchasers like Amazon and FedEx drive early adoption of electric powertrains requiring dedicated thermal management solutions.

The Automotive Coolant Market Report is Segmented by Product Type (Ethylene Glycol, Propylene Glycol, Glycerin, Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Technology (IAT, OAT, HOAT), End User (OEM, and Aftermarket), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

The Asia-Pacific region maintains the largest regional market share, accounting for 34.53% of the automotive coolant market in 2025. This is driven by China's stringent EV thermal management regulations and India's rapid expansion of automotive production, which is supported by government manufacturing incentives. China's GB standards mandate specific electrical conductivity limits for EV coolants, creating demand for specialized formulations that balance thermal performance with electrical safety requirements. India's automotive aftermarket growth, supported by PLI and PM E-DRIVE policies, generates sustained demand for both conventional and EV-specific coolant formulations as domestic OEMs establish thermal management supply chains. Japan and South Korea contribute to advanced EV technology development, which requires specialized dielectric coolants for battery and power electronics cooling applications.

South America emerges as the fastest-growing region, with a 6.67% CAGR through 2031, benefiting from Argentina-Brazil automotive integration policies that streamline vehicle homologation and component approval processes, while expanding commercial vehicle production to meet growing e-commerce demand. The region's growth acceleration stems from mutual recognition agreements that reduce regulatory barriers for coolant suppliers serving both major markets, creating economies of scale for regional operations.

North America and Europe represent mature markets with moderate growth rates, as the adoption of extended-life coolants reduces replacement frequency, while regulatory requirements drive specification upgrades toward premium formulations. European markets are facing particular transformation pressure from REACH regulations and PFAS restrictions, which favor bio-based coolant alternatives, creating opportunities for suppliers with sustainable chemistry capabilities. North American fleet operators increasingly adopt extended-life coolants to reduce maintenance costs, creating structural headwinds for aftermarket volume growth while benefiting OEM fill applications.