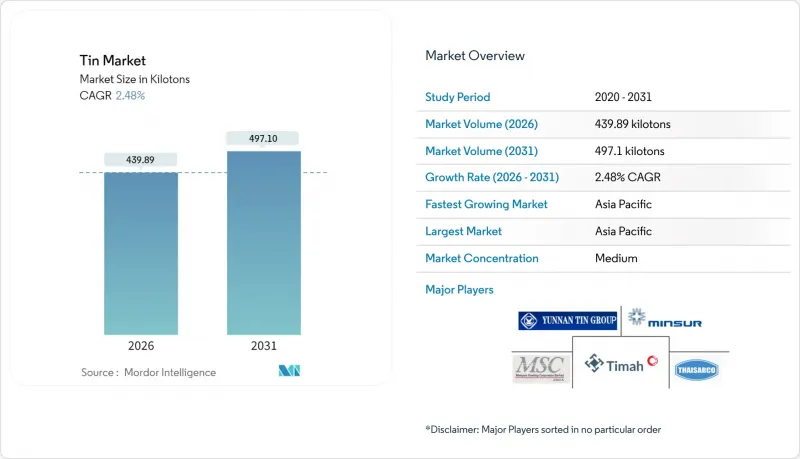

2026년 주석 시장 규모는 439.89 킬로톤과 추정되며, 2025년 429.24 킬로톤으로부터 성장이 전망됩니다. 2031년의 예측치는 497.1 킬로톤으로, 2026-2031년에 CAGR 2.48%로 확대할 전망입니다.

미얀마의 정치 불안으로 인한 공급 부족과 콩고민주공화국공급 리스크가 물량의 완만한 증가에도 불구하고 가격 안정을 지지하고 있습니다. 이 금속이 구리, 납, 아연 채굴에 의존하는 제품별 성질은 1차 금속에 비해 가격 변동성을 약 50% 확대시켜 제조업체에 다양한 공급처 확보를 요구하고 있습니다. 중국의 전자기기 산업과 인도네시아 제련소가 위치한 아시아태평양은 세계 수요의 약 70%를 흡수하며 지역을 선도하는 성장률을 보이고 있습니다. 한편, 북미와 유럽의 바이어들은 공급 중단에 대한 노출을 줄이기 위해 현지 조달 및 재활용 노력을 가속화하고 있습니다.

전자기기용 납땜은 가장 큰 용도이며, RoHS 지침 대응을 위해 무연합금으로의 전환이 진행되면서 2024년 소비량의 48.56%를 차지했습니다. 5세대 무선통신 인프라와 소형 반도체 패키지의 보급으로 단위당 주석 사용량이 증가하고 있습니다. 이는 고급 솔더 합금이 기존의 60-63% 혼합물이 아닌 95-99%의 고순도를 요구하기 때문입니다. 고온 자동차 모듈에서 은 소결로의 전환은 파워 일렉트로닉스 분야에서 솔더의 성장을 제한하고 있지만, 소비자 기기에서는 여전히 주석에 대한 의존도가 높은 상황입니다. GeSn 에피택시용 염화 주석(I) 화학기상증착 전구체는 틈새 시장에서 고매출 시장을 형성하고 전자 등급 주석 가격에 영향을 미칠 수 있습니다. 북미와 유럽의 현지화 프로그램은 국내 납땜 생산에 대한 투자를 촉진하고 아시아 공급업체에 대한 의존도를 완화하는 동시에 주석 시장에 추가 톤수를 공급하고 있습니다.

전기자동차의 파워 일렉트로닉스에서 인버터 및 배터리 팩에 열전도성 합금이 필요하므로 자동차 분야에서의 주석 시장 수요가 가속화되고 있습니다. 실리콘 카바이드 칩을 채택한 모듈은 접합부 온도가 상승하므로 가혹한 열 사이클을 견딜 수 있는 구리-주석 금속 간 결합이 선호됩니다. 과도기적 액상 접합은 기존 솔더와 다른 원료 등급을 소비하므로 합금 개발자들은 순도 수준과 습윤 특성을 개선하기 위해 노력하고 있습니다. 미국 에너지부가 2025년까지 100kW/L의 출력 밀도 목표를 설정함에 따라 발열을 관리하면서 설치 면적을 최소화하는 주석 고함량 솔루션에 대한 관심이 높아지고 있습니다. OEM의 엄격한 인증 주기로 인해 프리미엄 가격이 형성되고, 주석 금속화와 은 소결의 경쟁적 균형이 세계 주석 시장에서 고성능 EV 부문의 장기적인 침투를 좌우할 것입니다.

175℃ 이상의 접합 온도에서 작동하는 자동차 파워 모듈에서 은 소결 및 알루미늄 와이어 본딩은 점차 주석계 합금을 대체하고 있습니다. 고신뢰성 용도의 경우, 구리 직접 본딩 및 압력 접촉 시스템을 통해 장치당 주석 사용량을 더욱 줄일 수 있습니다. 그러나 도입은 여전히 자본 비용, 공정의 복잡성 및 기존의 주석 함량이 높은 솔더를 선호하는 긴 자동차 인증 주기로 인해 제한되고 있습니다. 가전기기 분야에서 주석은 더 비싼 은계 시스템에 비해 비용 대비 성능의 최적 균형을 유지하고 있으며, 주석 시장 수요의 대부분을 차지하고 있습니다. 장기적인 경쟁 압력은 대체 금속화 방법의 비용 차이를 줄이고 처리량을 향상시키는 공정 혁신에 달려 있습니다.

2025년 현재 합금은 주석 시장의 59.68%를 차지하고 있으며, 정밀한 조성 제어는 납땜, 베어링, 특수 금속 재료의 광범위한 적용을 지원하고 있습니다. 합금 부문은 범위의 경제성을 누리고 있으며, 제련소는 대규모 설비 투자 없이도 주석 납, 주석은 주석 구리의 혼합을 조정할 수 있으며, 광석 시장 변동 시에도 이익률을 유지할 수 있습니다. 순금속 카테고리는 99.95%의 순도를 자랑하며, 반도체, 배터리, 태양광발전 용도에 대응. 2031년까지 연평균 복합 성장률(CAGR) 3.05%로 확대되어 전체 주석 시장 규모에 대한 기여도를 높일 것으로 예측됩니다.

오로비스 등 생산업체는 다금속 재활용 공정을 활용하여 연간 정제 주석 처리 능력을 1만 톤 이상으로 확대. 양극 슬러지 및 복합 스크랩에서 금속 회수를 실현하면서 ISO 9001 및 ISO 14001 인증을 획득했습니다. 이러한 통합 흐름은 공급원 다변화, Scope 3 배출량 감소, 순 제로 밸류체인을 추구하는 자동차 제조업체 수요를 불러일으키고 있습니다.

본 주석 시장 보고서는 제품 유형(금속, 합금, 화합물), 용도(납땜, 주석 도금, 화학, 납축전지, 기타 용도), 최종사용자 산업(자동차, 전자기기, 포장, 유리, 기타 최종사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동/아프리카)별로 분석했습니다. 분석했습니다. 시장 예측은 톤 단위로 제공됩니다.

2025년에는 아시아태평양이 68.85%의 소비량을 차지할 것으로 예상되며, 중국의 전자제품 제조와 인도네시아의 광업 능력에 의해 주도될 것으로 보입니다. 지역별 주석 시장 규모는 CAGR 3.12%로 확대되고 있으며, 중국의 전기자동차 생산에 대한 정부 지원책과 아세안 지역내 배터리 공급망 구축이 성장을 촉진하고 있습니다. 중국에서는 광둥성 광시좡족자치구 광산의 환경 규제와 자원 고갈의 영향으로 제련소가 고급 광석 수입에 나서는 한편, 인도네시아의 PT Timaha사는 부패 조사로 인해 일시적으로 수출이 제한되었습니다.

북미의 주석 시장은 국내 재활용을 촉진하는 공급망 보안 조치로 인해 발전하고 있습니다. 오로비스는 조지아주 리치몬드 복합금속 공장에 8억 달러를 투자하여 연간 18만 톤의 복합 스크랩 처리 능력을 확보했습니다. 이를 통해 미국의 주요 자동차 및 항공우주 제조업체에 안정적인 공급이 가능해졌습니다.

유럽에서는 성숙하면서도 지속가능성에 초점을 맞춘 주석 소비가 이루어지고 있습니다. 독일은 EV용 파워 일렉트로닉스 분야에서 주석 채택을 주도하고 있으며, 오로비스사의 함부르크 단지에서는 양극 진흙을 주석 및 특수 금속으로 정제하는 고급 슬러지 처리 장치를 통해 고순도 공급을 강화하고 있습니다.

중동 및 아프리카은 여전히 소규모 소비 지역이지만, 인프라 확장 및 신흥 자동차 조립 산업으로 인해 수요가 점차 증가할 가능성이 있습니다. 콩고민주공화국의 정치적 리스크는 풍부한 자원 잠재력에도 불구하고 업스트림 투자를 억제하고 있으며, 이 지역은 세계 주석 시장 공급 안정성의 변동 요인으로 작용하고 있습니다.

Tin Market size in 2026 is estimated at 439.89 kilotons, growing from 2025 value of 429.24 kilotons with 2031 projections showing 497.1 kilotons, growing at 2.48% CAGR over 2026-2031.

Structural tightness caused by Myanmar's political instability and supply risks in the Democratic Republic of Congo underpins price stability despite modest volume growth. The metal's by-product nature-where production depends on copper, lead, and zinc mining-magnifies price swings by nearly 50% versus primary metals and forces manufacturers to secure diverse sources. Asia-Pacific, home to China's electronics complex and Indonesia's smelters, absorbs close to seven-tenths of global demand and posts region-leading growth, while North American and European buyers accelerate local sourcing and recycling initiatives to cut exposure to supply disruptions.

Electronics solder remained the largest application, accounting for 48.56% of 2024 consumption as manufacturers transitioned to lead-free alloys to meet RoHS mandates. Fifth-generation wireless infrastructure and smaller semiconductor packages drive higher tin loading per unit because advanced solder alloys require 95-99% purity rather than legacy 60-63% blends. The migration to silver sintering in high-temperature automotive modules limits solder growth in power electronics, yet leaves consumer devices largely dependent on tin. Stannic chloride chemical vapor deposition precursors for GeSn epitaxy create a niche, high-margin outlet that can influence electronic-grade tin prices. Localization programs in North America and Europe fuel investment in domestic solder production, tempering dependence on Asian suppliers while adding incremental tonnage to the tin market.

Automotive demand for tin market volumes accelerates as electric-vehicle power electronics need thermally conductive alloys for inverters and battery packs. Modules using silicon carbide chips push junction temperatures higher, favoring copper-tin intermetallic bonding that withstands extreme thermal cycling. Transient liquid-phase joining consumes different feedstock grades than conventional solder, prompting alloy developers to refine purity levels and wetting characteristics. Department of Energy density targets of 100 kW/L by 2025 intensify interest in tin-rich solutions that manage heat while minimizing footprint. Premium pricing arises from stringent OEM qualification cycles, and the competitive balance between tin metallization and silver sintering will shape long-term penetration in high-performance EV segments across the global tin market.

Silver sintering and aluminum wire bonding increasingly displace tin-based alloys in automotive power modules that operate above 175 °C junction temperatures. Copper direct bonding and pressure-contact systems further reduce tin per device in high-reliability applications. Uptake, however, remains limited by capital cost, process complexity and lengthy automotive qualification cycles that favor legacy tin-rich solders. In consumer electronics, tin maintains a cost-performance sweet spot against pricier silver systems, preserving a large portion of tin market demand. Long-term competitive pressure will depend on process innovation that narrows cost gaps and enhances throughput for alternative metallization methods.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Alloys held 59.68% tin market share in 2025 as precise composition control underpinned widespread solder, bearing, and specialty-metal formulations. The alloy segment benefits from economies of scope because smelters can tailor tin-lead, tin-silver, and tin-copper blends without major capital outlays, sustaining margins even during volatile ore markets. The pure metal category recorded 99.95% purity output that caters to semiconductor, battery, and photovoltaic uses and is set to register a 3.05% CAGR through 2031, lifting its contribution to the overall tin market size.

Producers such as Aurubis leverage multimetal recycling streams to exceed 10,000 metric-ton annual refined tin capacity, recovering metal from anode sludge and complex scrap while meeting ISO 9001 and ISO 14001 certifications. Such integrated flows diversify supply, reduce Scope 3 emissions, and appeal to automakers that pursue net-zero value chains.

The Tin Report is Segmented by Product Type (Metal, Alloy, and Compounds), Application (Solder, Tin Plating, Chemicals, Lead-Acid Batteries, and Other Applications), End-User Industry (Automotive, Electronics, Packaging, Glass, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific dominated with 68.85% consumption in 2025, driven by China's electronics manufacturing and Indonesia's mining capacity. Regional tin market size growth at 3.12% CAGR leverages government incentives for electric-vehicle production in China and battery supply-chain build-out across the ASEAN bloc. Chinese concentrate output faced environmental curbs and resource depletion at Yunnan and Guangxi deposits, prompting smelters to import higher-grade ore, while Indonesia's PT Timah battled corruption probes that temporarily restricted exports.

North America's tin market advances on supply-chain security initiatives that reward domestic recycling. Aurubis invested USD 800 million in its Richmond, Georgia multimetal plant capable of processing 180,000 tons of complex scrap annually, ensuring a reliable supply for U.S. automotive and aerospace primes.

Europe shows mature yet sustainability-focused tin consumption. Germany leads uptake in EV power electronics, and Aurubis's Hamburg complex boosts high-purity supply through its Advanced Sludge Processing unit that refines anode mud into tin and specialty metals.

The Middle-East and Africa remains a minor consumer, although infrastructure expansion and nascent automotive assembly may lift demand incrementally. Political risks in the Democratic Republic of Congo restrain upstream investment despite sizable resource potential, keeping the region a swing factor in global tin market supply stability.