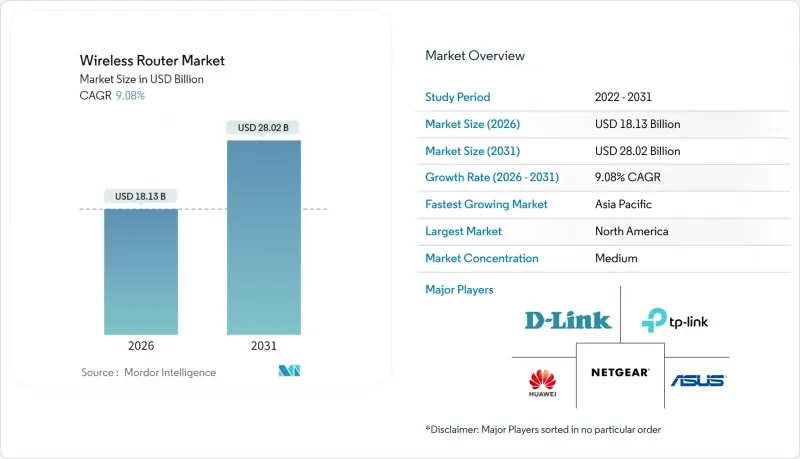

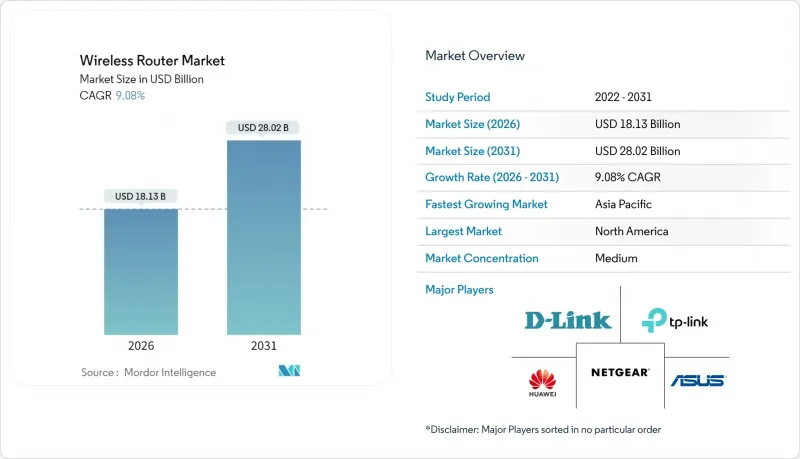

2026년 무선 라우터 시장 규모는 181억 3,000만 달러로 추정되며, 2025년 166억 2,000만 달러에서 성장하며, 2031년에는 280억 2,000만 달러에 달할 것으로 예측됩니다. 2026-2031년의 연평균 성장률(CAGR)은 9.08%에 달할 전망입니다.

이러한 성장은 기업 디지털화의 급격한 확대, 주거용 대역폭 수요 증가, Wi-Fi 7의 빠른 상용화에 기인합니다. Wi-Fi 7 탑재 기기 출하량은 2024년 2억 6,900만 대에 달할 것으로 예상되며, 2028년에는 21억 대를 넘어설 것으로 예상되어 멀티 기가비트 성능에 대한 잠재적 수요 증가를 지원하고 있습니다. 이와 함께 6GHz 대역 Wi-Fi 하드웨어도 빠르게 성장하고 있으며(2024년 출하량 8억 7,500만대), 63개국이 6GHz 대역의 일부를 라이선스 없이 이용할 수 있도록 개방하면서 생태계 구축이 진행되고 있는 것으로 확인되었습니다. 메시 시스템, 고 대역폭 트라이밴드 설계, ISP 관리형 CPE 번들이 잠재적 수요를 확대하는 반면, 고정형 무선 액세스 및 반도체 공급 제약이 국지적 변동 요인으로 작용하고 있습니다. 각 벤더들은 현재 AI를 활용한 관리 기능과 서비스형 네트워크(NaaS) 기능을 경쟁적으로 추가하고 있으며, 이를 통해 가격 결정력을 유지하고 저가의 중국 공급업체와의 경쟁 심화를 완화하기 위해 노력하고 있습니다.

세계에서 211억 개 이상의 Wi-Fi 기기가 운영되고 있으며, 2024년에는 41억 개가 더 출하될 것으로 예측됩니다. 이로 인해 기존 네트워크는 포화상태에 이르렀고, 멀티 기가비트 라우터로의 업그레이드를 촉진하고 있습니다. 현재 가정용 브로드밴드 사용자의 약 5분의 1이월1TB 이상의 데이터 통신량을 이용하고 있으며, 서비스 품질 한계치에 도달하고 있습니다. 스마트 팩토리, 스마트 시티, 자율주행 자동차 등 IoT의 성장은 Wi-Fi 7의 320MHz 채널이 제공할 수 있는 저지연 처리량에 대한 필요성을 더욱 심화시키고 있습니다. Wi-Fi 6 액세스 포인트가 실용적인 한계에 도달하면 기업은 장치 밀도 문제에 직면하여 차세대 무선 장비에 투자할 수밖에 없습니다. 그 결과, Wi-Fi 7 제품군을 보유한 벤더에게 유리한 업데이트 주기가 빨라지고 있습니다.

이미 45%의 기업이 Wi-Fi 6와 프라이빗 5G를 병행하여 시범 도입하는 등 통합형 무선 기반에 대한 지향이 두드러지고 있습니다. 제조 공장에서는 AI 탑재 로봇, 밀리초 미만의 감시 제어, 머신 비전 분석을 수행하기 위해 Wi-Fi 7을 채택했습니다. 2025년 주요 공급업체들의 AI 인프라 관련 라우터 분기별 수주액이 3억 5,000만 달러를 돌파했습니다. 구독형 서비스형 네트워크(Network-as-a-Service, NaaS) 모델은 설비투자 장벽을 낮추고, 신속한 배포를 가능하게 합니다. 요컨대, 대역폭을 많이 소비하는 용도과 유연한 자금 조달이 결합하여 무선 라우터 시장을 발전시키고 있습니다.

ASUS 라우터 취약점 CVE-2024-3080을 악용한 3.8Tbps 규모의 DDoS 공격은 펌웨어 취약점에 대한 업계의 취약점을 부각시켰습니다. 한편, 통신사들은 특히 새로운 Wi-Fi 7 보안 및 WPA3 설정에 대응할 수 있는 자격을 갖춘 네트워크 엔지니어가 33% 부족하다고 보고하고 있습니다. 기업은 전문가의 컨설팅이 필요하므로 도입 비용이 치솟고, 프로젝트 리드타임이 길어지는 문제에 직면해 있습니다. 중소기업의 경우, 설정이 느슨한 경우가 많아 침해 위험이 높고, 고급 위협 감지 기능을 갖춘 프리미엄 라우터 도입이 제한적입니다.

독립형 라우터는 2025년 기준 43.62%의 점유율을 유지했으나, 사용자들이 벽면 전체에 걸친 커버리지와 자체 최적화 성능을 요구함에 따라 메시 카테고리는 2031년까지 연평균 복합 성장률(CAGR) 11.74%로 확대될 것으로 예측됩니다. 메시 도입 관련 무선 라우터 시장 규모는 멀티 기가비트 광섬유의 보급과 연동하여 확대될 것으로 예측됩니다. ISP의 Aginet 및 eero for Service Providers와 같은 클라우드 관리 플랫폼의 채택이 성장의 모멘텀을 촉진하고 있습니다. 한편, 모바일 핫스팟 공유기는 5G 무선이 내장되어 다시 주목을 받고 있으며, 산업용 모델은 가혹한 환경 요구 사항을 충족합니다.

메쉬 벤더들은 현재 AI 알고리즘, Wi-Fi 7 멀티링크 동작, 320MHz 백홀 채널을 표준으로 장착하고 프리미엄 가격을 유지하고 있습니다. 독립형 설계는 게이머 층을 대상으로 확장되고 있으며, 트라이밴드 무선 및 지연시간 쉐이핑 엔진을 탑재하고 있습니다. 산업용 라우터는 SD-WAN 오버레이를 활용하여 원격 자산을 안전하게 연결합니다. 이러한 하위 부문은 보급형 하드웨어가 상품화되는 가운데서도 혁신적 틈새 시장이 이익률을 지켜내고 있는 현실을 보여주고 있습니다.

Wi-Fi 5는 여전히 저렴한 가격으로 인해 41.55%의 점유율을 차지하고 있지만, Wi-Fi 7의 출하량은 CAGR 24.74%를 기록하며 무선 라우터 시장을 재편할 것으로 예측됩니다. 기업의 6-15Gbps의 유효 처리량 수요가 조기 도입을 촉진하고 있으며, Wi-Fi 7 관련 무선 라우터 시장 규모는 금세기 말까지 Wi-Fi 6를 능가할 것으로 예측됩니다. 인증 제도의 정비로 여러 벤더 간의 상호운용성에 대한 우려는 완화되었지만, 높은 전력 요구 사항으로 인해 PoE 스위치의 업그레이드가 필수적입니다.

Wi-Fi 6는 예산 제약이 있는 구매층에게 OFDMA 효율성을 제공하는 교량 기술로 계속 사용될 것입니다. 레거시 Wi-Fi 4 디바이스는 비용과 전력이 속도를 능가하는 틈새 IoT 환경에서 살아남을 수 있습니다. 선진 지역에서는 조달 로드맵에 단계적인 Wi-Fi 7 도입과 엣지 컴퓨팅 투자를 포함시켜 대규모 시스템 개편 없이도 미래 지향적인 용량을 확보할 수 있도록 하고 있습니다.

아시아태평양은 2025년 5G 구축, 스마트 시티 계획, 제조업의 디지털화 추진으로 전 세계 매출의 33.55%를 차지할 것으로 예측됩니다. 싱가포르와 한국의 국가 구상이 Wi-Fi 7 기간망 연결에 대한 수요를 지원하는 반면, 중국 업체들은 보안 심사에 따른 해외 규제의 역풍에 대응하고 있습니다. 지역 전반의 하이퍼스케일 데이터센터 확장으로 인해 기업용 고처리량 라우터 주문이 더욱 증가하고 있습니다.

북미는 적극적인 광섬유 정비와 서비스 소외지역에 대한 장비 공급을 목적으로 한 대규모 BEAD 자금으로 인해 여전히 중요한 위치를 차지하고 있습니다. 고정형 무선 액세스는 2024년 1,200만 가입자를 돌파할 것으로 예상되며, 하이브리드형 셀룰러-와이파이 게이트웨이를 통해 라우터 판매에 압박과 보완의 영향을 미치고 있습니다. 기업용은 이미 Wi-Fi 7 액세스 포인트 출하량의 2%를 차지하고 있으며, 이 수치는 2025년까지 5배로 증가할 것으로 예측됩니다.

유럽에서는 멀티 기가비트 광섬유와 6GHz 대역의 단계적 개방을 배경으로 꾸준한 성장세를 보이고 있습니다. 프랑스는 Wi-Fi 7 도입을 주도하고 있으며, 프리미엄 CPE가 브로드밴드 계층을 차별화하는 사례가 되고 있습니다. 독일과 영국은 인더스트리 4.0과 보안 네트워킹을 우선시하며, WPA3 및 AI 기반 위협 분석 기능을 갖춘 트라이밴드 라우터에 대한 수요를 주도하고 있습니다. 브렉시트 이후 규제 차이는 여전히 인증 일정을 복잡하게 만들고 있으며, 벤더들은 지역별 물류 전략으로 전환해야 하는 상황입니다.

남미는 FTTH(광섬유 가정내 설치) 확대와 지방 연결 보조금으로 인해 10.47%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장 궤도를 기록하고 있습니다. 브라질이 도입을 주도하고 있는 가운데, 지역 통화의 변동성이 창의적인 가격 책정 모델을 요구하고 있습니다. 중동 및 아프리카의 신흥 시장에서는 스마트 시티 구상을 활용하여 호텔, 교육, 공공 부문 환경에서 Wi-Fi 7을 시범 도입하여 장기적인 수요 기반을 마련하고 있습니다.

Wireless router market size in 2026 is estimated at USD 18.13 billion, growing from 2025 value of USD 16.62 billion with 2031 projections showing USD 28.02 billion, growing at 9.08% CAGR over 2026-2031.

Growth springs from surging enterprise digitalization, rising residential bandwidth needs, and rapid commercialization of Wi-Fi 7. Device shipments for Wi-Fi 7 totaled 269 million units in 2024 and are projected to exceed 2.1 billion by 2028, underscoring pent-up demand for multi-gigabit performance. A parallel boom in 6 GHz Wi-Fi hardware-807.5 million units shipped in 2024-confirms strong ecosystem readiness as 63 nations free portions of the 6 GHz band for unlicensed use. Mesh systems, higher-bandwidth tri-band designs, and ISP-managed CPE bundles are expanding total addressable demand, while fixed-wireless access and semiconductor supply constraints create pockets of volatility. Vendors now race to add AI-powered management and network-as-a-service features to preserve pricing power and mitigate intensifying price competition from low-cost Chinese suppliers.

More than 21.1 billion Wi-Fi devices are active worldwide, and another 4.1 billion are expected to ship in 2024, saturating legacy networks and prompting upgrades to multi-gigabit routers. Roughly one-fifth of residential broadband users now exceed 1 TB of monthly data, stressing quality-of-service thresholds. IoT growth in smart factories, smart cities, and autonomous mobility deepens the need for low-latency throughput that Wi-Fi 7's 320 MHz channels can deliver. Enterprises face device-density headaches when Wi-Fi 6 access points hit practical limits, forcing investment in next-generation radios. The result is an accelerated refresh cycle favoring vendors with Wi-Fi 7 portfolios.

Forty-five percent of enterprises already trial both Wi-Fi 6 and private 5G in parallel, highlighting a preference for converged wireless fabrics. Manufacturing plants adopt Wi-Fi 7 to run AI-enabled robotics, sub-millisecond supervisory control, and machine-vision analytics. Quarterly router orders tied to AI infrastructure surpassed USD 350 million among leading suppliers in 2025. Subscription-based network-as-a-service models lower capex barriers, allowing faster rollouts. In short, bandwidth-hungry applications and flexible financing coalesce to push the wireless router market forward.

A 3.8 Tbps DDoS attack exploiting the ASUS router CVE-2024-3080 illustrated the sector's exposure to firmware vulnerabilities. Meanwhile, telecom operators report a 33% shortfall in qualified network engineers, particularly for emerging Wi-Fi 7 security and WPA3 configurations. Enterprises face higher deployment costs due to specialist consulting needs, stretching project lead times. Small firms often default to lax settings, heightening breach risks and limiting the adoption of premium routers with advanced threat detection.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Standalone routers retained a 43.62% share in 2025, yet the mesh category is on track for an 11.74% CAGR through 2031 as users seek wall-to-wall coverage and self-optimizing performance. The wireless router market size tied to mesh deployments is forecast to expand in tandem with multi-gigabit fiber rollouts. ISP adoption of cloud-managed platforms such as Aginet and eero for Service Providers reinforces growth momentum. In contrast, mobile hotspot routers gain renewed relevance by embedding 5G radios, while industrial models address harsh-environment requirements.

Mesh vendors now bake in AI algorithms, Wi-Fi 7 multi-link operation, and 320 MHz backhaul channels to sustain premium pricing. Standalone designs increasingly target gamers, featuring tri-band radios and latency-shaping engines. Industrial routers leverage SD-WAN overlays to connect remote assets securely. Collectively, these sub-segments illustrate how innovation niches defend margin even as entry-level hardware commoditizes.

Wi-Fi 5 still commands 41.55% share thanks to mass-market affordability, but Wi-Fi 7 shipments are set for a 24.74% CAGR that will reshape the wireless router market. Enterprise demand for 6-15 Gbps real-world throughput pushes early adoption, and the wireless router market size linked to Wi-Fi 7 could surpass Wi-Fi 6 by the decade's end. Certification has eased multi-vendor interoperability concerns, although higher power requirements necessitate PoE switch upgrades.

Wi-Fi 6 remains a bridge technology, offering OFDMA efficiency to budget-constrained buyers. Legacy Wi-Fi 4 devices persist in niche IoT settings where cost and power trump speed. In advanced regions, procurement roadmaps now include phased Wi-Fi 7 rollouts paired with edge-compute investments, ensuring future-proof capacity without forklift overhauls.

The Wireless Router Market Report is Segmented by Product Type (Standalone Routers, Mesh Wi-Fi Systems, and More), Wi-Fi Standard (802. 11n, 802. 11ac, 802. 11ax, 802. 11be), Frequency Band (Single-Band, Dual-Band, Tri-/Quad-Band), End-User Industry (Residential, Enterprise), Distribution Channel (Online Retailers, Offline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 33.55% of global revenue in 2025, buoyed by 5G rollouts, smart-city programs, and ongoing manufacturing digitization. National initiatives in Singapore and South Korea anchor demand for Wi-Fi 7 backbone connectivity, while Chinese vendors navigate overseas regulatory headwinds tied to security scrutiny. Hyperscale data-center expansion throughout the region further bolsters enterprise orders for high-throughput routers.

North America remains pivotal, thanks to aggressive fiber builds and sizable BEAD funding that directs equipment to underserved rural zones. Fixed-wireless access surpassed 12 million subscribers in 2024, simultaneously pressuring and complementing router sales via hybrid cellular-Wi-Fi gateways. Enterprises already account for 2% of Wi-Fi 7 AP shipments, a figure expected to quintuple by 2025.

Europe posts steady gains behind multi-gigabit fiber and phased 6 GHz clearance. France leads Wi-Fi 7 adoption, showcasing how premium CPE differentiates broadband tiers. Germany and the U.K. prioritize Industry 4.0 and secure networking, driving demand for tri-band routers with WPA3 and AI-powered threat analytics. Regulatory nuances post-Brexit still complicate certification timetables, nudging vendors toward localized logistics strategies.

South America registers the fastest trajectory at 10.47% CAGR on the back of fiber-to-the-home expansion and rural-connectivity subsidies. Brazil spearheads rollouts, while regional currency volatility forces creative pricing models. Emerging markets in the Middle East and Africa are leveraging smart-city ambitions to pilot Wi-Fi 7 in hospitality, education, and public-sector environments, laying groundwork for long-term demand.