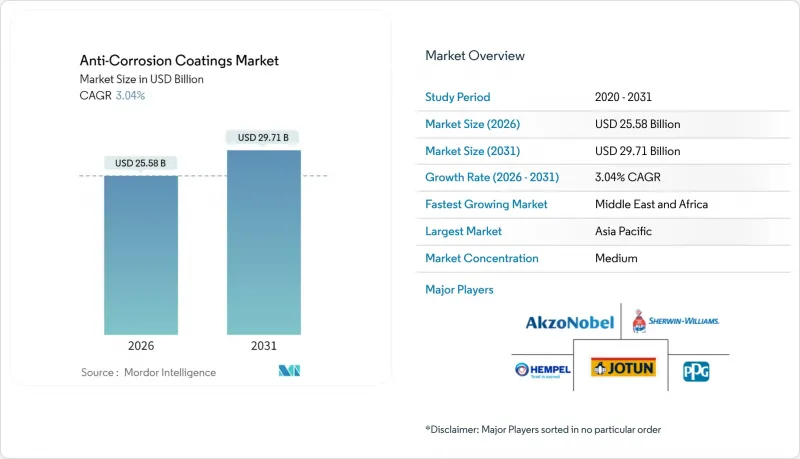

방식 코팅 시장은 2025년 248억 2,000만 달러에서 2026년에는 255억 8,000만 달러로 성장하며, 2026-2031년에 CAGR 3.04%로 추이하며, 2031년까지 297억 1,000만 달러에 달할 것으로 예측되고 있습니다.

공공 부문의 인프라 투자 확대, 해상풍력발전설비 사양 강화, 부유식 생산저장하역설비(FPSO)의 개보수 주기가 길어짐에 따라 부식방지 코팅 시장은 물량 중심에서 성능 중심의 생태계로 전환되고 있습니다. 규제가 엄격한 지역에서는 수성 화학물질이 보급되고 있지만, 고장 위험이 환경에 미치는 영향보다 큰 분야에서는 여전히 솔벤트 기반 시스템이 주류를 이루고 있습니다. 수지 기술도 혁신적으로 발전하고 있으며, 바이오 에폭시 수지와 하이브리드 폴리우레탄 시스템이 지속가능성과 내구성을 겸비한 입찰에서 주목받고 있습니다. LNG 터미널의 단열재 하부 부식 방지 솔루션에 대한 수요 증가는 범용 유지보수용 도료에서 용도별 엔지니어링 코팅으로 시장이 전환되고 있음을 보여줍니다.

대규모 정부 프로그램이 기존의 유지보수 주기를 훨씬 뛰어넘는 수명을 제공하는 고성능 페인트에 대한 수요를 주도하고 있습니다. 미국 '인프라 투자 및 고용법'은 수명이 긴 교량, 철도, 항만 자산의 개보수에 5,500억 달러를 배정했습니다. 유럽 그린딜의 자금 배분은 저VOC, 고내구성 제품을 우선시하며, 설계 사양 담당자를 바이오 에폭시 및 하이브리드 폴리우레탄 시스템으로 유도하고 있습니다. 일본의 국가 복원력 계획은 터널과 해안 방호 시설에 유연성과 내진성을 갖춘 가공제를 요구하고 있으며, 보다 강력한 폴리우레탄 엘라스토머 화학에 대한 연구를 추진하고 있습니다. 이러한 시너지 효과로 인해 기본 알키드 수지 도막에서 25-30년의 보호 간격을 제공하는 엔지니어링 시스템으로 꾸준히 전환되고 있습니다. 소유주가 페인트를 소모품이 아닌 전략적 위험 완화 수단으로 인식하는 가운데, 수명주기 보증과 신속한 현장 기술 지원을 제공할 수 있는 공급업체는 프리미엄 마진을 얻게 됩니다.

세계 해상 풍력발전 용량은 2030년까지 380GW를 초과하는 것을 목표로 하고 있으며, 모노파일, 트랜지션 피스, 나셀 보호에 대한 특수한 요구를 주도하고 있습니다. 터빈 부품은 주기적인 염수분무, 부유물에 의한 충격, 음극 박리를 견딜 수 있는 코팅이 요구됩니다. 나노세라믹 강화 에폭시 프라이머와 지방족 폴리우레탄 가공제를 결합한 시스템이 표준 사양으로 부상하고 있습니다. 이는 25년 동안 광택과 차단 성능을 유지하기 위함입니다. 미국 동부 해안 프로젝트에서는 30GW 도입을 목표로 하는 연방정부의 로드맵을 계기로 성능 저하 없이 엄격한 VOC 규제를 충족하는 수성 도료 또는 고형분 도료의 채택이 진행되고 있습니다. 터빈 재킷을 생산하는 아시아 조선소들은 유럽 개발업체 입찰 요건에 부합하기 위해 유사한 시스템 인증을 신속하게 추진하고 있으며, 특수 부식 방지 안료의 세계 원료 공급망에 압박을 가하고 있습니다.

미국 및 EU의 여러 지역에서 VOC 규제치(50g/L)의 개정으로 인해 솔벤트계 폴리우레탄 도료의 판매가 압박을 받고 있습니다. 제조업체들은 수성 도료나 고형분 도료로 기술 전환을 요구받고 있으며, 경화시간의 연장이나 현장의 엄격한 습도 관리가 요구되는 경우가 증가하고 있습니다. 추가 교육, 장비 적응, 제3자 인증 비용이 이익률을 압박하는 한편, 기존 솔벤트 기술과의 성능 차이는 선박 및 중공업 사용자들에게 여전히 우려되는 부분입니다. 이와 함께 디이소시아네이트 라벨링에 관한 새로운 REACH 규정은 이액형 폴리우레탄의 국경 간 운송에 대한 물류 장벽을 높이고 중요한 정비 기간의 리드 타임을 연장하고 있습니다.

에폭시계 도료는 독보적인 접착력과 내화학성(특히 선박 밸러스트 탱크 및 교량 거더에서)으로 인해 2025년 부식 방지 도료 시장 규모의 38.92%를 차지할 것으로 예측됩니다. 최근 개발된 바이오 에폭시계 도료는 염수분무 시험시간(내식성)을 손상시키지 않으면서도 친환경 조달기준을 충족시켜 기존 비스A계 배합제품의 점유율을 빼앗아가고 있습니다. 원료 가격의 변동에도 불구하고 이 부문은 견고한 성장세를 유지하고 있으며, 배합업체들은 희석제 최적화를 통해 납품 가격의 안정화를 꾀하고 있습니다.

폴리우레탄은 해상 풍력발전 타워에서 진동 흡수성과 기계적 박리 저항성을 갖춘 유연한 필름이 개발자의 선택을 받아 3.79%의 연평균 복합 성장률(CAGR)을 보이고, 가장 빠르게 물량을 확대하고 있습니다. 지진 다발 지역인 아시아의 교통 터널에서 폴리우레탄의 채용 확대는 에폭시와의 차이를 더욱 좁히고 있습니다. 알키드, 폴리에스테르, 비닐에스테르는 비용과 극한의 내화학성이 요구되는 틈새 시장에서 존재감을 유지하고 있지만, 장수명 철골 구조물 사양서에서는 에폭시 프라이머와 폴리우레탄 탑코트를 결합한 하이브리드 기술이 주류를 이루고 있습니다.

부식방지 페인트 보고서는 수지 유형(에폭시, 알키드, 폴리에스테르, 폴리우레탄, 폴리우레탄 등), 기술(수성, 솔벤트, 분말, UV 경화), 최종사용자 산업(석유 및 가스, 선박, 전력, 인프라, 산업, 항공우주 및 방위 등), 지역(아시아태평양, 북미, 유럽 등) 별로 구성되어 있습니다. 구성되어 있습니다. 시장 예측은 금액(USD)으로 제시되어 있습니다.

아시아태평양은 중국의 일대일로(一帶一路) 구상에 따른 항만 확장, 인도의 해상풍력발전소 수주, 일본의 내진 인프라 정비 계획에 힘입어 2025년 매출의 46.60%를 차지했습니다. 국내 제조업체는 리드타임 단축과 환리스크 감소로 이어지는 수지 생산 통합 거점의 혜택을 누리고 있지만, 현지 환경 규제 강화로 인해 연안 지역에서는 수성 도료의 채택이 증가하고 있습니다. 동남아시아 조선소들은 EU 선적 선박의 수주 확보를 위해 국제해사기구(IMO) PSPC 승인 도료 시스템에 대한 대응을 추진하고 있으며, 이로 인해 세계 프리미엄 브랜드에 대한 수요가 더욱 증가하고 있습니다.

북미 시장은 여전히 높은 점유율을 유지하고 있으며, 이는 인프라 투자 및 일자리 창출법에 따른 교량 및 터널 개보수 프로젝트 파이프라인과 미국 멕시코만 연안의 석유화학 플랜트 유지보수 비용 증가에 기인합니다. 사양 수립자는 교통량이 많은 주간 고속도로의 차선 폐쇄 기간을 최소화하기 위해 조기 복구가 가능한 고형분 에폭시 도료로 전환을 추진하고 있습니다.

유럽에서는 그린딜 보조금이 저VOC, 바이오, 재생 소재 함유 페인트에 대한 자금 지원과 연계된 고도 시장이 형성되어 있습니다. 북해의 선박 수리 공장에서는 강화된 건강 규제에 대응하기 위해 속건성 무용제 탑코트와 호환되는 고급 아연 규산염계 프라이머를 채택하고 있습니다.

중동 및 아프리카에서는 사우디아라비아의 NEOM, 나이지리아의 해양 허브와 같은 메가 프로젝트로 인해 2031년까지 연평균 복합 성장률(CAGR) 3.36% 상승할 것으로 예측됩니다. 높은 자외선량, 모래에 의한 마모, 높은 염분 농도로 인해 유리 플레이크 에폭시 수지와 결합된 고품질 불소 수지 탑코트가 요구되고 있으며, 가격보다 기술적 우위가 계약 체결의 주요 기준이 되고 있습니다. 오만과 카타르에서 정유소 용량이 확대됨에 따라 수 킬로미터에 달하는 단열 배관 전체에 걸쳐 CUI(부식 방지 코팅) 내식성 라이닝에 대한 수요가 꾸준히 증가하고 있습니다.

The Anti-Corrosion Coatings Market is expected to grow from USD 24.82 billion in 2025 to USD 25.58 billion in 2026 and is forecast to reach USD 29.71 billion by 2031 at 3.04% CAGR over 2026-2031.

Strong public-sector infrastructure spending, more demanding offshore wind specifications, and the expanding refurbishment cycle for floating production storage offloading (FPSO) vessels are shifting the anti-corrosion coatings market from a volume-led arena to a performance-driven ecosystem. Water-borne chemistries are advancing in regulatory-sensitive regions, yet solvent-borne systems still dominate where failure risk outweighs environmental trade-offs. Resin innovation is also accelerating, with bio-based epoxies and hybrid polyurethane systems gaining traction in bids that score sustainability alongside lifetime durability. Greater demand for corrosion-under-insulation solutions at LNG terminals highlights the market's transition from generalized maintenance paints toward application-specific engineered coatings.

Massive government programs are steering demand toward high-performance coatings that extend service life well beyond conventional maintenance cycles. The Infrastructure Investment and Jobs Act in the United States earmarked USD 550 billion for upgrades that prioritize long-life bridge, rail, and port assets. European Green Deal allocations link funding to low-VOC, high-durability products, nudging specifiers toward bio-based epoxy and hybrid polyurethane systems. Japan's national resilience plan requires flexible, seismic-resistant finishes for tunnels and coastal defenses, propelling research into tougher polyurethane elastomer chemistries. The combined effect is a steady replacement of basic alkyd films with engineered systems offering 25-30-year protection intervals. Suppliers capable of lifecycle assurance and rapid on-site technical support are capturing premium margins as owners view coatings as strategic risk mitigators rather than consumables.

Global offshore wind capacity is targeted to exceed 380 GW by 2030, driving specialized needs for monopile, transition-piece, and nacelle protection. Turbine components demand coatings that withstand cyclical salt spray, impact from floating debris, and cathodic disbondment. Nano-ceramic-reinforced epoxy primers topped with aliphatic polyurethane finishes are emerging as a standard stack because they retain gloss and barrier integrity for 25-year service windows. U.S. East Coast projects, galvanized by a federal roadmap for 30 GW of installations, are specifying water-borne or high-solids variants to honor strict VOC caps without compromising performance. Asian yards fabricating turbine jackets are fast-tracking qualification of similar systems to stay compliant with European developer tenders, tightening global raw-material supply chains for specialty anticorrosive pigments.

Revised limits of 50 g/L VOC in several U.S. and EU districts are squeezing solvent-borne polyurethane sales. Manufacturers must invest in water-borne or high-solids upgrades, often accepting slower cure times and stricter humidity controls on job sites. The added training, equipment adaptation, and third-party certification expenses erode margins while the performance gap relative to legacy solvent technologies still worries marine and heavy-industrial users. In parallel, new REACH rules on di-isocyanate labeling raise logistical hurdles for shipping two-pack polyurethanes across borders, extending lead times in critical maintenance windows.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Epoxy systems accounted for 38.92% of the anti-corrosion coatings market size in 2025, thanks to unmatched adhesion and chemical resistance, especially in marine ballast tanks and bridge girders. Recent bio-based epoxy variants satisfy green-procurement scoring without sacrificing salt-spray hours, pulling share from conventional bis-A formulations. The segment remains resilient despite raw-material cost swings, as formulators lean on diluent optimization to keep delivered prices stable.

Polyurethane volumes are expanding fastest, supported by a 3.79% CAGR as developers choose flexible films that absorb vibration and resist mechanical chipping on offshore wind towers. Growing polyurethane acceptance in seismic-prone Asian transport tunnels further narrows the gap to epoxy. Alkyd, polyester, and vinyl ester niches maintain relevance where cost sensitivity or extreme chemical resistance dictates, but hybrid technology blending epoxy primers with polyurethane topcoats now dominates specification sheets for long-life steel infrastructure.

The Anti-Corrosion Coatings Report is Segmented by Resin Type (Epoxy, Alkyds, Polyester, Polyurethane, and More), Technology (Water-Borne, Solvent-Borne, Powder, and UV-Cured), End-User Industry (Oil and Gas, Marine, Power, Infrastructure, Industrial, Aerospace and Defense, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 46.60% of 2025 revenue, driven by China's Belt and Road port expansions, India's offshore wind farm orders, and Japan's seismic infrastructure initiatives. Domestic manufacturers benefit from integrated resin production hubs that compress lead times and reduce currency risk, yet rising local environmental rules are pushing waterborne adoption in coastal provinces. Southeast Asian shipyards, eager to win EU-flag vessel contracts, are aligning with IMO PSPC-approved coating systems, adding further pull for global premium brands.

North America's share remains sizeable owing to the Infrastructure Investment and Jobs Act pipeline of bridge and tunnel rehabilitation, combined with elevated maintenance spending on U.S. Gulf Coast petrochemical plants. Specifiers are pivoting toward high-solids epoxies with rapid return-to-service properties to minimize lane-closure durations on busy interstates.

Europe hosts a sophisticated market where Green Deal subsidies tie funding to low-VOC, bio-based, or recycled-content coatings. Ship repair yards in the North Sea embrace advanced zinc-silicate primers compatible with fast-flush solvent-free topcoats to rebalance stricter health regulations.

The Middle East and Africa is projected to rise at a3.36% CAGR through 2031 due to mega-projects such as Saudi Arabia's NEOM and Nigeria's offshore hubs. High UV levels, sand abrasion, and salinity demand premium fluoropolymer topcoats paired with glass-flake epoxies, positioning technical superiority over price as the chief contract award criterion. Rising refinery capacity in Oman and Qatar fuels steady demand for CUI-resistant linings across kilometers of insulated piping.