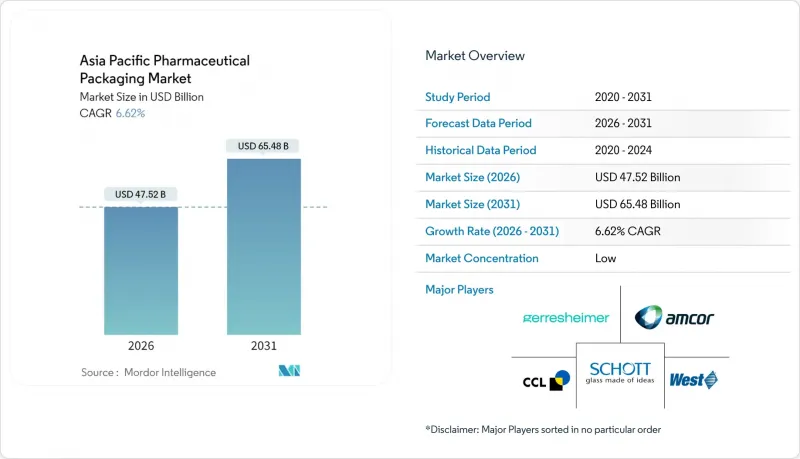

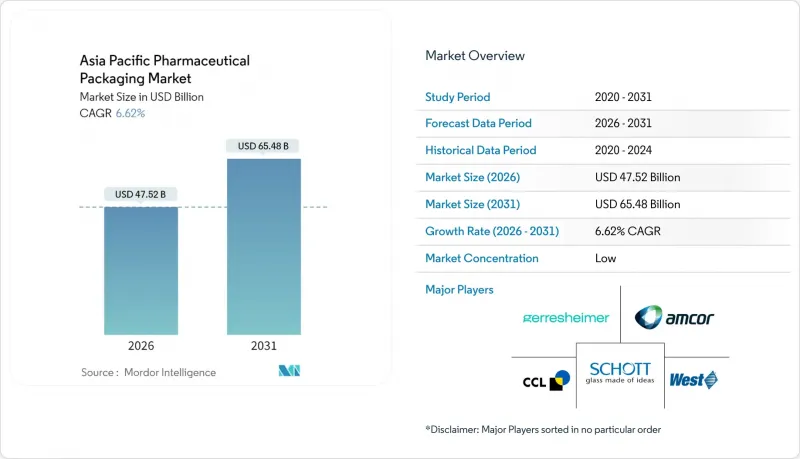

아시아태평양의 의약품 포장 시장은 2025년에 445억 7,000만 달러로 평가되며, 2026년 475억 2,000만 달러에서 2031년까지 654억 8,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 6.62%로 전망됩니다.

이러한 꾸준한 성장은 이 지역이 저비용 생산 기지에서 고부가가치 생물제제, 복잡한 충전 및 포장 서비스, 시리얼라이제이션 대응 포장 라인의 세계 중심지로 전환하고 있음을 반영합니다. 중국의 전자코드 직렬화 시행과 인도의 의약품 인증 검증 용도(DAVA) 확대에 따라 공급망의 모든 계층이 추적 가능하고 변조 방지 기능을 갖춘 형태로 전환하면서 수요가 증가하고 있습니다. 소재의 혁신도 가속화되고 있습니다. 컨버터는 범용 플라스틱에서 세포 및 유전자 치료용 극저온 물류에 견딜 수 있는 환형 올레핀과 바이오플라스틱으로 전환되고 있습니다. 이와 함께 제약 브랜드 소유주들은 단일 복용량 형식과 통합 디지털 식별자를 선호하고 있으며, 아시아태평양의 제약 포장 시장은 지속가능성과 규정 준수에 초점을 맞춘 다년간의 투자 주기에 통합되어 있습니다.

2024년, 바이오로직스는 SCHOTT Pharma의 바이오의약품 매출의 34%를 차지하여 총매출을 10억 5,000만 달러로 끌어올렸습니다. 이는 오염 위험을 최소화하는 사전 멸균된 붕규산 유리 용기로의 구조적 전환을 보여줍니다. 스테바넷 그룹도 비슷한 추세를 보여 2024 회계연도에 12억 1,000만 달러의 매출을 달성했으며, 이 중 38%는 즉시 사용 가능한 바이알 및 카트리지 제품에서 발생했습니다. 양사는 게레스하이머와 공동으로 2024년 9월 'RTU 연합(Alliance for RTU)'을 설립하고, 아시아태평양 의약품 포장 시장에서 즉시 사용 가능한 용기 포맷의 표준화를 추진하고 있습니다. 현재 수탁제조 업체들은 입찰 단계에서 탈피로젠 처리된 바이알과 사전 조립된 클로저를 지정하여 백신 및 단클론 항체 출시를 위한 검증 기간을 단축하고 있습니다. 바이오의약품 파이프라인이 성숙함에 따라 고부가가치 용기에 대한 수요는 최고 수준의 생산 기지를 넘어 확대되고 있으며, 지역 유리 제조업체는 치수 공차를 엄격하게 하고 가시적인 입자가 없는 생산을 위해 용광로를 개조하고 있습니다.

로터스 파마슈티컬의 FDA, EMA, PMDA 인증 네트워크는 2025년 상반기 사상 최대 매출을 달성하며, 유럽과 미국 공장에서 이전한 복잡한 충전 및 마무리 공정을 흡수할 수 있는 인도의 능력을 입증했습니다. 싱가포르와 한국은 바이오의약품 전문기술로 경쟁하고 있으며, 중국은 비용 효율적인 멸균설비로 계절성 백신 생산 리드타임을 단축하고 있습니다. 그 결과, 아시아태평양의 의약품 포장 시장에서 중첩형 주사기, 듀얼 챔버 카트리지, 직렬화 2차 포장 상자의 처리량이 증가하고 있습니다. 기술이전 계약에서 포장적격성 시험과 의약품 제조가 통합된 사례가 증가하고 있으며, 현지 컨버터는 단순한 제품 공급업체에서 솔루션 파트너로 위상을 높이고 있습니다. 이러한 모멘텀은 ISO 규격의 클린룸 인프라 도입에 박차를 가하고 있으며, 라벨링, 검사, 어그리게이션 서비스에도 파급효과를 가져오고 있습니다.

윈팩의 2024년 실적 발표에 따르면 나일론과 알루미늄 포일 가격이 전년 대비 9-13% 하락한 것으로 나타났습니다. 이는 이전 급등 후의 반동으로, 컨버터 기업이 직면한 상품 가격의 급격한 변화를 강조하고 있습니다. 포장업체들은 헤지 전략과 유연한 가격 조항에 재정 자원을 투입하고 있지만, 중소기업은 급등세를 흡수할 수 있는 신용 한도가 부족합니다. 재고가 더 엄격하게 관리되므로 공급업체가 할당량을 제한할 경우 라인이 중단될 위험이 높아집니다. 비용 흡수력의 불균형은 통합형 다국적 기업에 우위를 가져와 아시아태평양의 의약품 포장 시장에서의 경쟁의 균형을 연간 원자재 계약을 협상할 수 있는 대형 업체로 기울게 하고 있습니다.

플라스틱은 주요 제약 제조 클러스터에 근접한 압출 및 사출성형 능력을 바탕으로 2025년 아시아태평양 제약 포장 시장에서 46.78%의 압도적인 점유율을 유지했습니다. 그러나 이 부문의 한 자릿수 중반대의 성장률은 첨단소재가 기록한 8.22%의 연평균 복합 성장률(CAGR)과는 대조적으로, 극저온 저장 및 고활성 의약품에 대한 내성이 우수한 사이클로올레핀, 바이오 고분자, 특수 유리로의 전환이 진행되고 있음을 보여줍니다. 생물제제 파이프라인이 확대되고 부속서 1의 클린룸 기준이 강화됨에 따라 아시아태평양의 환형 올레핀 공중합체에 의한 의약품 포장 시장 규모는 두 자릿수 성장이 예상됩니다.

미쓰이화학의 APEL(TM)은 사이클로올레핀 기술 혁신이 감마선 멸균과의 호환성을 유지하면서 방습성 요건을 충족하는 것으로 입증되어 프리필드 시린지 배럴의 채용 확대가 가능해졌습니다. 유리 제조업체들도 기존 바이알의 박리 위험을 피하면서 주사제 충진 및 봉입 시장의 성장에 대응하기 위해 Type I 붕규산 유리용 용해로 개조를 추진하고 있습니다. 지속가능성 측면에서는 필름 가공업체가 PLA-나노셀룰로오스 복합재 실험을 진행하고 있으며, 퇴비화성을 확보하면서 약전에서 요구하는 추출물 한계치를 충족시킬 수 있을 것으로 기대하고 있습니다. 지역 규제 당국은 재활용 가능성과 탄소발자국 공개를 우선시하는 지침을 발표하고, 재료 선택 체크리스트에 환경 지표를 포함시킴으로써 이러한 전환을 지원하고 있습니다.

The Asia Pacific pharmaceutical packaging market was valued at USD 44.57 billion in 2025 and estimated to grow from USD 47.52 billion in 2026 to reach USD 65.48 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031).

This steady climb reflects the region's transition from a low-cost production base into a global center for high-value biologics, complex fill-finish services, and serialization-ready packaging lines. Demand intensifies as China enforces e-code serialization and India scales its Drug Authentication and Verification Application, pushing every tier of the supply chain toward traceable, tamper-evident formats. Material innovation also quickens: converters move from commodity plastics toward cyclic olefins and bioplastics that withstand deep-cold logistics for cell-and-gene therapies. In parallel, pharmaceutical brand owners favor single-dose formats and integrated digital identifiers, locking the Asia Pacific pharmaceutical packaging market into a multi-year investment cycle focused on sustainability and compliance.

Biologics represented 34% of SCHOTT Pharma's biopharmaceutical revenue in 2024, lifting total sales to USD 1.05 billion and signaling a structural pivot toward pre-sterilized borosilicate formats that minimize contamination risk.Stevanato Group echoed this trend, generating USD 1.21 billion in fiscal 2024 with 38% of revenue from ready-to-use vials and cartridges. The two firms, together with Gerresheimer, formed the Alliance for RTU in September 2024 to standardize ready-to-use container formats across the Asia Pacific pharmaceutical packaging market. Contract manufacturers now specify depyrogenated vials and pre-assembled closures at bid stage, compressing validation timelines for vaccine and monoclonal antibody launches. As biologics pipelines mature, high-value container demand expands beyond top-tier sites, encouraging regional glass makers to retrofit furnaces for tighter dimensional tolerances and visible-particle-free output.

Lotus Pharmaceutical's FDA-, EMA- and PMDA-certified network earned a record first-half 2025 revenue, reinforcing India's ability to absorb complex fill-finish work relocated from Western plants. Singapore and South Korea compete on biologics expertise, while cost-efficient sterilization suites in China shorten lead times for seasonal vaccine production. The Asia Pacific pharmaceutical packaging market consequently records higher throughput for nested syringes, dual-chamber cartridges, and serialized secondary cartons. Technology transfer contracts increasingly bundle packaging qualification with drug-product manufacture, elevating local converters into solution partners rather than commodity suppliers. This momentum accelerates adoption of ISO -compliant clean-room infrastructure and creates a ripple effect on labelling, inspection, and aggregation services.

Winpak's 2024 earnings call revealed a 9-13% quarter-over-quarter drop in nylon and aluminum foil prices after earlier spikes, underscoring the commodity whiplash confronting converters. Packaging producers devote treasury resources to hedging strategies and flexible pricing clauses, yet smaller firms lack the credit lines to buffer sudden surges. Inventory runs leaner, raising the risk of line stoppages when suppliers ration allocations. Uneven cost absorption places integrated multinationals at an advantage, tilting competitive balance within the Asia Pacific pharmaceutical packaging market toward scale players that negotiate annual raw-material contracts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic maintained a commanding 46.78% share of the Asia Pacific pharmaceutical packaging market in 2025 thanks to established extrusion and injection-molding capacity close to major drug-manufacturing clusters. Yet the segment's mid-single-digit growth contrasts with the 8.22% CAGR logged by advanced materials, underscoring a pivot toward cyclic olefins, bio-based polymers, and specialty glass that better withstand cryogenic storage and high-potency drugs. The Asia Pacific pharmaceutical packaging market size attributable to cyclic-olefin copolymers is projected to climb in double digits as biologics pipelines deepen and Annex 1 clean-room standards tighten.

Mitsui Chemicals' APEL(TM) demonstrates how cyclic-olefin innovation satisfies moisture-barrier demands while remaining compatible with gamma sterilization, enabling wider adoption in pre-filled syringe barrels. Glass producers also renovate furnaces for Type I borosilicate, aiming to capture injectable fill-finish growth without the delamination risks of legacy vials. On the sustainability front, film converters experiment with PLA-nanocellulose blends that promise compostability yet meet extractables limits required by pharmacopeias. Regional regulators support this shift by issuing guidance prioritizing recyclability and carbon-footprint disclosure, embedding environmental metrics into material-selection checklists.

The Asia Pacific Pharmaceutical Packaging Market Report is Segmented by Material (Plastic, Paper and Paperboard, Glass, Aluminum Foil, Other Advanced Materials), Type (Ampoules, Blister Packs, Plastic Bottles, Syringes, Vials, IV Fluids, Stick Packs, Pouches and Sachets, Caps and Closures), Drug Delivery Mode (Oral, Injectable, Pulmonary, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).