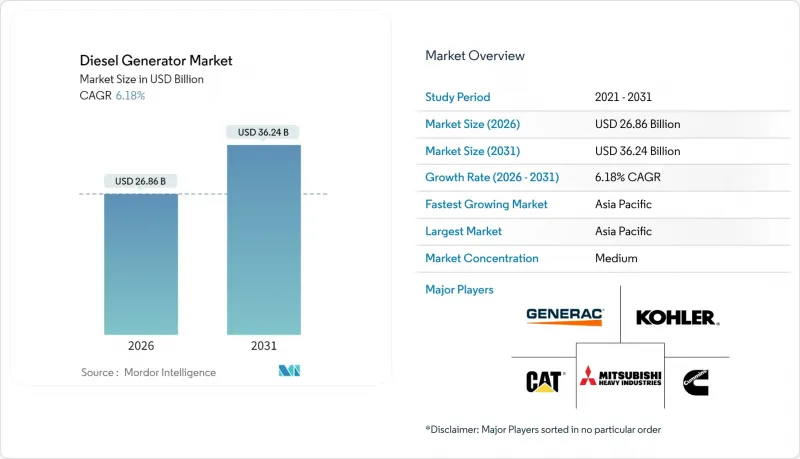

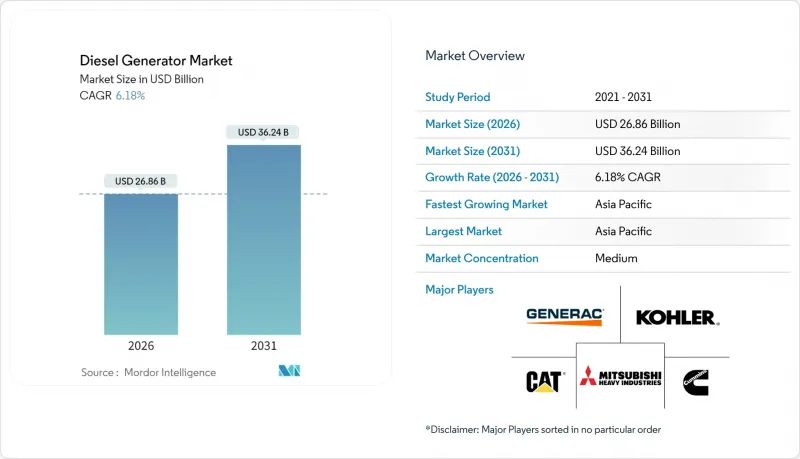

디젤 발전기 시장은 2025년 253억 달러에서 2026년에는 268억 6,000만 달러로 성장하며, 2026-2031년에 CAGR 6.18%로 추이하며, 2031년까지 362억 4,000만 달러에 달할 것으로 예측됩니다.

이 예측은 전력망에 대한 재생에너지 도입 확대와 규제 당국의 배출 규제 강화에도 불구하고 시장의 지속적인 중요성을 지원합니다. 수요는 크게 세 가지 구조적 요인에 의해 지원되고 있습니다. 디지털화된 업무를 보호하기 위한 내결함성 전력의 필요성, 전력망이 정비되지 않은 지역의 급속한 산업 확장, 그리고 미립자 물질과 질소산화물을 크게 감소시키는 첨단 Tier 4 Final 엔진의 보급입니다. 동시에 하이브리드 마이크로그리드는 배터리와 태양광발전을 디젤 발전과 결합하여 가동률 저하 없이 연료 소비를 억제할 수 있습니다. 중형 75-375kVA 세트에는 기존 메가와트급 유닛에 한정되어 있던 원격감시, 후처리 장치, 병렬운전 대응 개폐장치가 탑재되어 대상 사용자층이 확대되고 있습니다.

병원, 금융거래소, 반도체 제조 공장에서는 정전이 사이버 공격과 동등한 수준의 비즈니스 연속성 리스크로 인식되고 있습니다. 캘리포니아의 Walsh 데이터센터는 클라우드 워크로드 보호를 위해 96MW의 디젤 백업을 설치했습니다. 이 투자는 사업자가 발전기 용량이 매출 보호와 직결된다는 것을 인식하고 있음을 보여줍니다. 제어기 펌웨어에 내장된 예측 분석 기능은 가동부하를 기반으로 유지보수를 계획하여 수명주기 비용을 절감하고 발전기를 능동적인 시설 자산으로 탈바꿈시켜 줍니다. 많은 디지털 기업에서 시간당 평균 다운타임 비용이 10만 달러가 넘는 상황에서 조달 부서는 자본 지출을 줄이는 것보다 검증된 디젤 신뢰성을 우선시하는 경향이 강해지고 있습니다. 이러한 추세는 원격 진단 기능과 입자상 물질 배출을 99% 줄인 Tier 4 Final 대응 유닛의 높은 가격 책정을 지원하며, 강화된 규제에도 불구하고 디젤 발전기 업계의 가치 제안을 유지하고 있습니다.

동남아시아 및 아프리카의 공장 생산량은 전력회사가 전력망을 강화할 수 있는 속도보다 더 빠른 속도로 증가하고 있습니다. 산업단지에서는 취약한 송전망과 동기화하거나 정전시 독립적으로 운영되는 10-20MW 규모의 현장 발전설비가 자주 도입되고 있습니다. Aggreko와 Cummins가 제공하는 턴키 렌탈 차량은 사하라 사막 이남 아프리카의 신규 광산 운영을 영구적인 송전선로가 설치될 때까지 유지하여 프로젝트 일정을 몇년단축하고 있습니다. 디젤 발전기는 몇 년이 걸리는 송전망 확장에 비해 몇 개월 만에 납품, 시운전, 부하 테스트를 완료할 수 있습니다. 이러한 속도 우위는 산업 성장에 따른 발전 용량 수요 증가로 발전 용량의 추가 확장을 가능하게 하여, 신흥 경제국의 디젤 발전기 산업이 꾸준한 성장 궤도를 유지하는 선순환을 만들어내고 있습니다.

캘리포니아주 대기자원국은 디젤 미립자 및 질소산화물(NOx) 배출 기준을 Tier 4 Final 이하로 낮추는 정책을 추진하고 있으며, 일부 차량 소유주들은 천연가스 유닛이나 하이브리드 마이크로그리드로의 전환을 고려하고 있습니다. 유럽의 Stage V 규제는 19kW 이상의 엔진에 선택적 촉매 환원(SCR)과 미립자 포집 필터(DPF) 장착을 의무화하고 있으며, 이로 인해 도입 비용이 증가하고 유지보수 계획이 복잡해지고 있습니다. 이러한 규제는 역풍으로 작용하고 있으며, 엔진 제조업체들은 냉각식 EGR 연소 기술, 첨단 연료 분사 시스템, 재생 디젤 대응 기술 등에 대응하여 성능 저하 없이 규제에 대응하고 있습니다. 미션 크리티컬한 부하를 가진 시설에서 디젤의 에너지 밀도는 여전히 높은 평가를 받고 있으며, 이로 인해 디젤 발전기 산업은 프리미엄 부문에서 존재감을 유지하고 있습니다.

2025년 기준 75kVA 미만 등급은 디젤 발전기 업계 점유율의 최대 43.25%를 차지하며, 주택, 소규모 상업시설, 통신 사이트 등 소형 발전기가 적합한 중간 부하 수요가 견고하게 유지되고 있음을 반영하고 있습니다. 그러나 375-750kVA 구간은 2031년까지 연평균 복합 성장률(CAGR) 7.55%로 확대되어 다른 모든 구간을 능가하는 속도로 성장하고 있습니다. 공장, 데이터 처리 기지, 대규모 소매 시설이 비용과 내결함성의 균형을 중시하는 솔루션으로 전환하고 있기 때문입니다. 중형 모델에는 기존에는 수 메가와트급 유닛에 한정되어 있던 Tier 4-Final 후처리 장치, 하이브리드 대응 제어 시스템, 클라우드 텔레메트리가 표준으로 장착되어 있습니다.

캐터필러의 컴팩트한 설계는 설치 공간을 31% 줄임과 동시에 EPA 규정을 완벽하게 준수합니다. 이러한 설계 혁신으로 총 설치비용이 절감되어 기존 시설에서의 도입이 가속화되고 있습니다. 상위 모델인 750-2,000kVA 및 2,000kVA 이상 세트는 광산 및 하이퍼스케일 데이터센터용으로 설계되었으며, 전력회사 수준의 전압 조정 기능을 갖춘 장시간 가동이 요구됩니다. 엔트리 모델과 고성능 모델 간의 성능 격차가 확대되는 것은 디젤 발전기 산업의 성숙도를 보여줍니다. 가격뿐만 아니라 용도 요건이 구매 기준을 결정하고, OEM(Original Equipment Manufacturer)에게 프리미엄 포지셔닝의 기회를 제공합니다.

본 디젤 발전기 시장 보고서는 용량별(75kVA 미만, 75-375kVA, 375-750kVA, 750-2,000kVA, 2,000kVA 이상), 용도별(비상용/예비전원, 주전원/연속전원, 피크컷/부하관리), 최종사용자별(주거용, 상업용, 산업용), 지역별(북미, 아시아, 유럽, 아시아태평양, 중동, 아프리카, 중동, 유럽, 일본, 중국) 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다.

아시아태평양은 2025년 디젤 발전기 산업에서 48.55%로 가장 큰 점유율을 차지하고 있으며, 2031년까지 연평균 복합 성장률(CAGR) 7.12%로 확대될 것으로 예측됩니다. 공장 생산 호조, 새로운 교통망 구축, 클라우드 지출 급증으로 수요는 지역 전력망 업그레이드를 크게 상회하고 있습니다. 중국과 인도가 설치 대수의 대부분을 차지하고 있으며, 제조업체는 전압 변동으로부터 생산을 보호하기 위해 현장 설치형 발전기에 의존하고 있습니다. 이 지역의 데이터센터용량은 현재 12,206MW에 달하며, 14,338MW가 추가로 건설 중입니다. IT 부하 1MW당 약 1MW의 예비 전력을 확보하고 있습니다. 싱가포르의 신규 서버팜 건설 중단 조치로 인해 투자가 조호르 주와 자카르타 대도시권으로 옮겨가면서 발전기 판매의 지역적 범위가 확대되고 있습니다. 5G의 빠른 보급을 위해서는 수천 개의 통신탑 증설이 필요하며, 소형이면서도 신뢰성이 높은 유닛이 요구됩니다. 한편, 호주와 동남아시아의 외딴 광산에서는 고비용의 송전망 확장을 피하기 위해 대형 디젤-태양광 하이브리드 패키지를 지정하고 있습니다.

북미는 매출 2위 지역으로, 전력회사들이 기상재해로 인한 정전을 줄이기 위해 네트워크를 강화하는 가운데 꾸준한 성장세를 보이고 있습니다. 주거용 출하량은 2027년까지 연평균 복합 성장률(CAGR) 5.82%로 증가할 것으로 예측됩니다. 이는 허리케인, 산불, 얼음 폭풍으로 인한 장기 정전에 대비하기 위해 주택 소유자가 보호 수단을 구입하고 있기 때문입니다. 캘리포니아주의 엄격한 배출가스 규제는 Tier 4 Final 엔진과 재생 디젤 혼합 연료를 선호하고 있으며, 가격뿐만 아니라 규제 준수를 중시하는 프리미엄 하위 부문을 형성하고 있습니다. 버지니아, 텍사스, 캘리포니아 북부 수요 증가도 디젤 발전기 산업에 호재로 작용하고 있습니다. 이들 지역에는 하이퍼스케일 데이터센터가 밀집해 있으며, 96MW 규모의 Walsh 시설과 같은 단일 캠퍼스에서도 클라우드 서비스 가동 시간을 보장하기 위해 수십 대의 중속 발전기를 주문하는 경우가 있습니다. 유럽에서는 탄소 감축 목표에 따라 미립자 및 질소산화물(NOx) 배출을 줄이는 하이브리드 발전기와 스테이지 V 호환 후처리 시스템을 선택하는 구매자가 증가하고 있습니다.

중동 및 아프리카은 전력망에서 떨어진 공항, 철도 회랑, 광산 건설에 대한 정부 투자로 한 자릿수 후반의 높은 성장률을 보이고 있습니다. 개발업체들은 사막이나 고산지대에서 연료비 절감과 물류 간소화를 위해 디젤 발전과 태양전지판 및 축전지를 결합하는 경우가 많습니다. 칠레, 페루, 아르헨티나의 구리 및 리튬 광산에서는 송전망 정비가 프로젝트 진행을 따라잡지 못해 컨테이너형 프라임급 유닛을 도입하는 등 남미도 비슷한 추세를 보이고 있습니다. 브라질과 아르헨티나의 디젤 발전기 산업은 식품 가공 및 석유화학 산업을 위한 용량을 추가하고 있으며, 고객 기반이 광산 산업을 넘어 확장되고 있습니다. 국제에너지기구(IEA)의 2025년 보고서에서 제시된 세계 디젤 공급의 안정적 전망은 신흥 지역 전체의 발전기 공급과 가격 책정을 지원하고 있습니다. 이러한 요인들이 결합되어 디젤의 신뢰성과 재생에너지 입력을 결합한 통합 솔루션이 주목을 받고 있으며, 다양한 수요 구조가 형성되고 있습니다.

The Diesel Generator market is expected to grow from USD 25.30 billion in 2025 to USD 26.86 billion in 2026 and is forecast to reach USD 36.24 billion by 2031 at 6.18% CAGR over 2026-2031.

The forecast underscores the market's continued relevance even as grids add more renewables and regulators tighten emission limits. Demand pivots on three structural forces: the need for resilient power to protect digitalized operations, the rapid industrial build-out in regions where grids cannot keep pace, and the availability of advanced Tier 4 Final engines that sharply cut particulate matter and nitrogen oxides. At the same time, hybrid microgrids combine batteries and photovoltaics with diesel generation, enabling operators to limit fuel consumption without compromising availability. Mid-range 75-375 kVA sets now incorporate remote monitoring, aftertreatment, and parallel-ready switchgear once reserved for megawatt-class units, widening the addressable user base.

Hospitals, financial exchanges, and semiconductor fabs now categorise power loss as a business-continuity risk on par with cyberattacks. The Walsh Data Center in California installed 96 MW of diesel backup to protect cloud workloads, an investment illustrating how operators equate generator capacity with revenue protection. Predictive analytics embedded in controller firmware schedule maintenance around live loads, lowering lifecycle costs and turning generators into active facility assets. As average downtime costs exceed USD 100,000 per hour for many digital businesses, procurement teams increasingly prioritize proven diesel reliability over capital expenditure savings. This trend supports premium pricing for Tier 4 Final sets that combine remote diagnostics with 99% lower particulate emissions, preserving the diesel generator industry's value proposition even under stricter regulations.

Factory output in Southeast Asia and Africa rises faster than utilities can reinforce transmission. Industrial parks frequently integrate 10-20 MW of on-site generation that synchronises with weak grids or runs islanded during outages. Turnkey rental fleets supplied by Aggreko and Cummins keep green-field mines in Sub-Saharan Africa operational until permanent lines arrive, shortening project schedules by several years. Diesel generators are delivered, commissioned, and load-tested in months, compared with multi-year grid-extension timelines. This speed advantage fuels a virtuous cycle where industrial growth demands more generation capacity, enabling further expansion and keeping the diesel generator industry on a steady upward trajectory in emerging economies.

California's Air Resources Board is pushing diesel particulate and NOx thresholds below Tier 4 Final, motivating some fleet owners to switch to natural-gas units or hybrid microgrids. The European Stage V rule set mandates the use of selective catalytic reduction and particulate filters on engines exceeding 19 kW, thereby increasing acquisition costs and complicating maintenance schedules. While these standards pose a headwind, engine manufacturers have responded with cooled-EGR combustion strategies, advanced fuel injection, and renewable diesel compatibility that meet compliance without eroding performance. Facilities with mission-critical loads continue to value diesel's energy density, thereby preserving the diesel generator industry's relevance in premium segments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The below-75 kVA class retained the largest 43.25% slice of the diesel generator industry share in 2025, reflecting strong uptake in residential, small commercial, and telecom sites where modest loads warrant compact sets. Yet the 375-750 kVA band is advancing at a 7.55% CAGR to 2031, outpacing every other bracket as factories, data-processing hubs, and large retail footprints migrate to solutions that balance cost and resiliency. Mid-range models now ship with Tier 4-Final aftertreatment, hybrid-ready controls, and cloud telemetry once reserved for multi-megawatt units.

Caterpillar's compact architecture reduces installation space by 31% while maintaining full EPA compliance, a design leap that lowers total installed costs and accelerates adoption in brownfield facilities. At the top end, 750-2,000 kVA and >2,000 kVA sets power mines and hyperscale data centers, which require extended runtime with utility-grade voltage regulation. The widening performance gap between entry-level and feature-rich models signals a maturing diesel generator industry, in which application demands, rather than price alone, dictate buying criteria and open premium positioning for OEMs.

The Diesel Generator Market Report is Segmented by Capacity (Below 75 KVA, 75 To 375 KVA, 375 To 750 KVA, 750 To 2, 000 KVA, and Above 2, 000 KVA), Application (Stand-by/Backup Power, Prime/Continuous Power, and Peak-shaving/Load Management), End User (Residential, Commercial, and Industrial), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

The Asia-Pacific region holds a leading 48.55% share of the diesel generator industry in 2025 and is projected to expand at a 7.12% CAGR through 2031. Strong factory output, new transport links, and a sharp rise in cloud spending keep demand well ahead of local grid upgrades. China and India account for the majority of installations, as manufacturers rely on on-site sets to protect production from voltage fluctuations. Regional data-center capacity now totals 12,206 MW, with another 14,338 MW under construction, each megawatt of IT load matched by roughly one megawatt of standby power. Singapore's moratorium on new server farms has redirected investment to Johor and Greater Jakarta, widening the geographic spread of generator sales. A rapid 5G rollout requires the addition of thousands of telecom towers, which necessitate small but reliable units. Meanwhile, remote mine sites in Australia and Southeast Asia specify larger hybrid diesel-solar packages to avoid costly grid extensions.

North America is the second-largest region by revenue and exhibits steady growth as utilities enhance their networks to mitigate weather-driven outages. Residential shipments rise 5.82% CAGR to 2027 because homeowners buy protection from longer blackouts caused by hurricanes, wildfires, and ice storms. California's strict emission rules favor Tier 4 Final engines and renewable diesel blends, creating premium sub-segments that value compliance as much as price. The diesel generator industry also benefits from rising demand in Virginia, Texas, and Northern California. They host clusters of hyperscale data centers, and a single campus, such as the 96 MW Walsh facility, can order dozens of medium-speed generators to guarantee uptime for cloud services. In Europe, carbon-reduction goals are prompting buyers to opt for hybrid sets and Stage V-compliant aftertreatment systems that reduce particulate matter and NOx emissions.

The Middle East and Africa are experiencing high single-digit growth as governments invest in building airports, rail corridors, and mines that are far from reliable grids. Developers often pair diesel with solar arrays and batteries to trim fuel costs and simplify logistics in desert or high-altitude terrain. South America mirrors this pattern: copper and lithium miners in Chile, Peru, and Argentina deploy containerized, prime-rated units because grid connections often lag behind project timelines. The diesel generator industry in Brazil and Argentina also adds capacity for food processing and petrochemicals, widening the customer base beyond extractive industries. A stable outlook for global diesel supply, outlined in the International Energy Agency's 2025 report, supports generator availability and pricing across emerging regions. Together, these factors create a diverse demand landscape where integrated solutions that combine diesel reliability with renewable inputs gain traction.