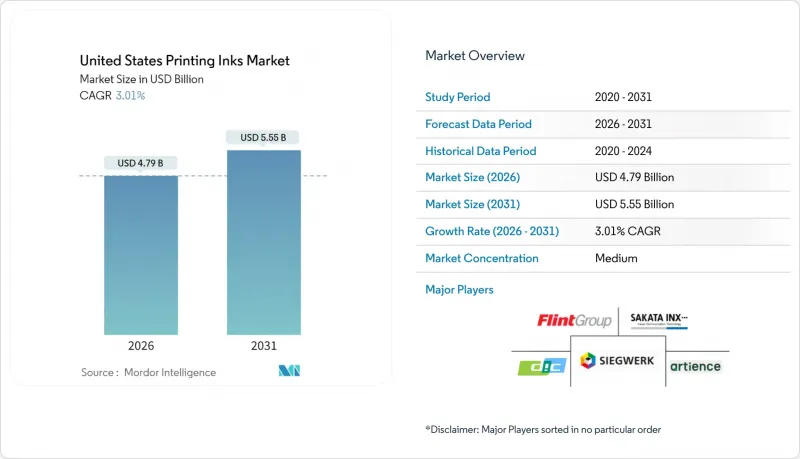

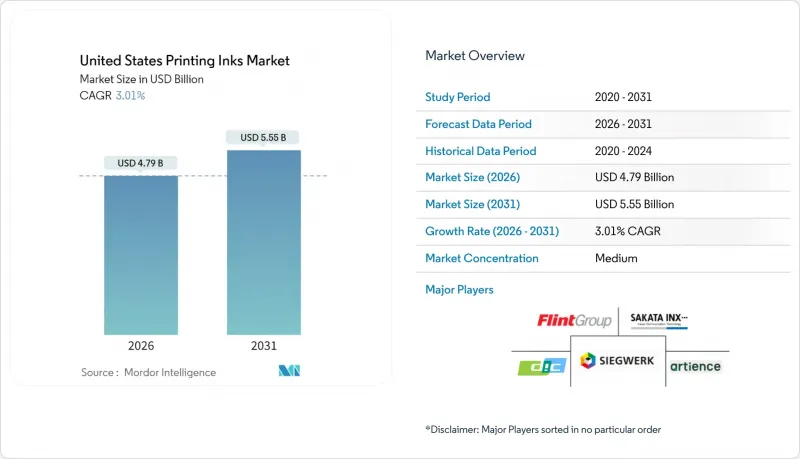

미국의 인쇄 잉크 시장 2026년의 시장 규모는 47억 9,000만 달러로 추정되며, 2025년 46억 5,000만 달러에서 성장이 전망됩니다.

2031년까지 55억 5,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 3.01%로 확대될 것으로 전망됩니다.

완만한 성장률의 이면에는 포장 및 디지털 지속가능성 관련 분야의 급격한 성장이 여전히 축소되고 있는 상업용 인쇄의 수요를 능가하고 있습니다. 고수익률의 특수 잉크를 필요로 하는 E-Commerce용 골판지 상자, 식음료 라벨, 소량 판촉물 등 수요가 견조하게 유지되고 있습니다. 또한, 기업의 지속가능성 목표 달성을 지원하는 저전이성 UV/LED 잉크, 수성 잉크, 바이오 기반 화학제품에 대해 브랜드 소유주가 프리미엄 가격을 지불함으로써 조제 제조업체의 수익률 향상에 기여하고 있습니다. 공급 측면의 동향은 안료 및 수지 생산능력의 국내 회귀, 관세로 인한 아시아 의존도 분산, 중견 공급업체들 간의 꾸준한 통합으로 형성되고 있습니다. 휘발성 유기 화합물(VOC) 규제와 작업장 안전에 대한 압력으로 인해 에너지 경화형 및 수성 시스템으로의 전환이 가속화되고 있으며, 디지털 인쇄기는 판재 및 설치 폐기물을 제거하여 비용 곡선을 재구성하고 있습니다.

잉크젯 인쇄기는 판과 그에 따른 설치 비용을 없애고, 컨버터가 수만 단위가 아닌 수백 단위의 SKU가 난립하는 생산을 수익성 있게 생산할 수 있게 해줍니다. 브랜드 소유자는 한정판 디자인, 지역 언어 버전, 최종 단계의 개인화 등 기존 오프셋 인쇄로는 수익성이 떨어지는 유연성을 활용하고 있습니다. UV 경화형 잉크젯 화학제품은 순간적으로 경화되어 비다공성 필름에서도 색조 일관성을 유지하며, 범용 열경화성 잉크의 2-3배의 가격대를 실현합니다. 인쇄기 제조업체들은 더 넓은 인쇄 바, 더 빠른 드롭 배치 정확도를 목표로 개선을 거듭하여, 총 레인 수가 감소하는 가운데 잉크 사용량을 늘리는 선순환을 만들어내고 있습니다. 노즐 친화적인 점도, 저발포성, 안정된 분산성을 보장할 수 있는 공급업체는 주요 컨버터 공장에 도입이 진행되고 있는 디지털 인쇄기군에서 다년간 우선 공급업체로 자리매김하고 있습니다.

과거 오프셋 인쇄의 경제성을 살리기 위해 과잉인쇄를 할 수밖에 없었던 출판사는 이제 판매되지 않은 재고를 운영자금의 부담으로 여기고 있습니다. 고속 잉크젯 라인과 전자동 제본 라인을 결합하면 300페이지 분량의 소설도 몇 분 안에 완성할 수 있으며, 책 한 권 단위로 리필이 가능합니다. 교육 기관은 맞춤형 교재 팩에 이 모델을 채택하고 있으며, 자체 출판사는 위험 부담 없는 물리적 유통 경로를 찾고 있습니다. 짙은 흑색 표현, 경량 용지에서의 번짐 감소, 제본에 적합한 내마모성을 실현하는 잉크 제조업체는 온디맨드 인쇄 네트워크에서 우선적으로 채택하고 있습니다. 이 분야는 잡지 산업의 축소로 인한 빈 생산능력을 흡수하고 레거시 공장의 고용 감소를 완화하기 위해 야간 가동으로 구식 상업용 인쇄기를 유지하고 있습니다.

미국 마케터들은 커넥티드 TV의 노출을 실시간으로 측정하고 타겟팅할 수 있게 됨에 따라 인쇄 매체에 대한 예산 배분을 줄였습니다. 2024년에는 잡지-카탈로그 발행부수가 9% 더 감소하고, 웹 오프셋용 잉크의 수요도 연동하여 감소할 것으로 예상됩니다. 인쇄공장의 잉여 생산능력으로 인해 중소 인쇄업체들은 파산과 합병을 강요당하고 있으며, 범용 열전사 잉크의 고객 기반이 축소되고 있습니다. 살아남은 인쇄업체들은 포장 및 간판 분야로 전환을 시도하고 있지만, 작업자 재교육과 인쇄기 개조에는 많은 자금이 필요하고, 많은 업체들이 자금 조달에 어려움을 겪고 있습니다. 잉크 제조업체들은 전통적인 상업용 인쇄 분야에서 주문량 감소와 미수금 회수 주기의 장기화를 경험하고 있으며, 이는 전반적인 수익 성장을 둔화시키는 요인으로 작용하고 있습니다.

2025년 기준, 유성 제품은 미국 인쇄 잉크 시장 점유율의 40.05%를 유지했습니다. 이는 기업 마케팅 자료 및 고급 카탈로그의 오프셋 인쇄 워크플로우가 정착되었기 때문입니다. 한편, 수성 화학제품은 저 VOC 규제를 중시하는 골판지 및 접이식 카톤 라인에서 점유율을 확대. 솔벤트 기반 블렌드는 극도의 내마모성이 요구되는 틈새 산업 그래픽 분야에서 여전히 필수적인 요소였습니다. 전자빔, 스크린, 전도성 잉크 등 '기타 유형'의 미국 인쇄 잉크 시장 규모는 5.02%의 높은 CAGR로 확대되었습니다.

디지털 기술을 통한 변화는 제품 구성의 경제성을 재구성하고 있습니다. UV 및 LED 잉크는 생산량 기준으로는 여전히 10% 미만이지만, kg당 단가가 범용 페이스트 잉크의 2배에 달하기 때문에 가장 높은 기여 수익률을 창출하고 있습니다. 대시보드 센서 필름 및 플렉서블 RFID용으로 50만 달러/kg 내외의 고가대에 공급되는 전도성 은 플레이크 페이스트는 소량 생산이지만 수익에 큰 영향을 미치고 있습니다. 우수한 유변학 제어 기술과 서브마이크론 입자 전문 지식을 보유한 공급업체는 전자제품 OEM 제조업체에서 게이트키퍼 역할을 수행하며 진입장벽을 높이고 있습니다. 예측 기간 동안 브랜드 소유주들이 순환 경제 스코어카드를 채택하여 소비자 제품을 차별화하는 가운데, 바이오 기반 매체와 새로운 무금속 안료가 석유 기반 시스템에서 더 많은 점유율을 차지할 것으로 예상됩니다.

미국 인쇄 잉크 시장 보고서는 유형별(솔벤트 기반, 수성, 유성, UV, UV LED, 기타), 인쇄 공정별(윤전 오프셋 인쇄, 평판 오프셋 인쇄, 플렉소 인쇄, 플렉소 인쇄, 그라비어 인쇄, 기타), 용도별(포장, 상업용 인쇄 및 출판, 섬유, 기타)로 분류되어 있습니다. 시장 예측은 금액(달러) 및 수량(단위)으로 제공됩니다.

United States Printing Inks Market market size in 2026 is estimated at USD 4.79 billion, growing from 2025 value of USD 4.65 billion with 2031 projections showing USD 5.55 billion, growing at 3.01% CAGR over 2026-2031.

Moderate growth hides rapid substitution effects as packaging, digital, and sustainability-linked niches outpace still-shrinking commercial print volumes. Demand resilience stems from e-commerce corrugated boxes, food and beverage labels, and short-run promotional items that all require higher-margin specialty formulations. Formulator margins benefit from the premium that brand owners pay for low-migration UV/LED, water-based, and bio-derived chemistries that support corporate sustainability targets. Supply-side dynamics are shaped by the onshoring of pigment and resin capacity, tariff-driven diversification away from Asia, and steady consolidation among mid-tier suppliers. Regulatory pressure on volatile organic compounds and workplace safety continues to accelerate the shift toward energy-curable and water-based systems, while digital presses rewrite cost curves by eliminating plates and makeready waste.

Inkjet presses remove plates and associated setup costs, letting converters profitably produce SKU-proliferated runs measured in hundreds rather than tens of thousands. Brand owners exploit the agility for limited-edition designs, regional language versions and late-stage personalization that would cripple conventional offset economics. UV-curable inkjet chemistries cure instantly, maintain color consistency on non-porous films, and command price points 2-3 times higher than commodity heatset alternatives. Press OEMs iterate toward wider print bars and faster drop-placement accuracy, creating a virtuous cycle that lifts ink volumes even as overall lane counts fall. Suppliers able to guarantee nozzle-friendly viscosity, low foam, and stable dispersion secure multi-year preferred-supplier status with digital press fleets that now populate every major converter plant.

Book publishers, once forced to over-print to exploit offset economies, now view unsold inventory as a working-capital drag. High-speed inkjet lines paired with fully automated binding finish a 300-page novel in minutes, allowing replenishment in batches of one. Educational institutions embrace the model for custom course packs, while self-publishers find a risk-free path to physical distribution. Ink makers that deliver deep black density, reduced feathering on lightweight stocks, and binding-friendly rub resistance gain preferred approval from print-on-demand networks. The segment keeps older commercial presses running at night, absorbing capacity vacated by magazine decline and thereby slowing employment attrition in legacy plants.

U.S. marketers tilted budgets away from print as connected-TV impressions became addressable and measurable in real time. Magazine and catalog volumes fell another 9% in 2024, taking web offset ink demand down in lockstep. Surplus pressroom capacity forced smaller printers into bankruptcy or fire-sale mergers, eroding the customer base for commodity heatset blends. Surviving shops pivot to packaging and signage, yet retraining operators and retooling presses require capital that many cannot access. Ink makers see shrinking order sizes and longer receivable cycles in the legacy commercial segment, dampening overall revenue growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Oil-based products retained 40.05% of the United States printing inks market share in 2025, thanks to entrenched offset workflows in corporate marketing collateral and high-end catalogs. Water-based chemistries captured incremental share in corrugated and folding carton lines that favor low-VOC compliance, while solvent blends remained critical for niche industrial graphics needing extreme abrasion resistance. The United States printing inks market size for Other Types, including electron beam, screen, and conductive formulations, expanded at a brisk 5.02% CAGR.

Digital disruption reshapes product-mix economics. UV and LED variants, though still under 10% by tonnage, generate the highest contribution margins thanks to per-kilo pricing that can double commodity paste inks. Conductive silver-flake pastes priced near USD 500 kg underpin dashboard sensor films and flexible RFID, creating an outsized revenue impact despite low volume. Suppliers with strong rheology control and sub-micron particle expertise command gatekeeper status with electronics OEMs, erecting formidable entry barriers. Over the forecast horizon, bio-based vehicles and novel metal-free pigments are expected to pull further share from petroleum-derived systems as brand owners embrace circular-economy scorecards to differentiate consumer offerings.

The United States Printing Inks Report is Segmented by Type (Solvent-Based, Water-Based, Oil-Based, UV, UV LED, and Other Types), Printing Process (Lithographic Web Printing, Lithographic Sheetfed Printing, Flexographic Printing, Gravure Printing, and More), Application (Packaging, Commercial and Publication, Textiles, and Others). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).