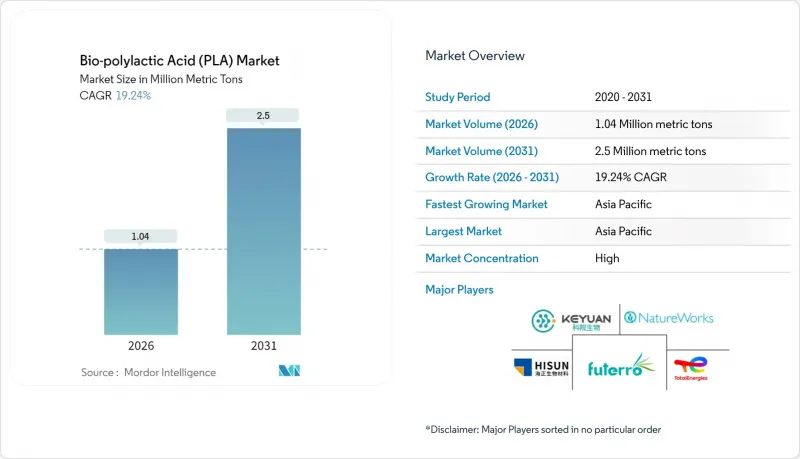

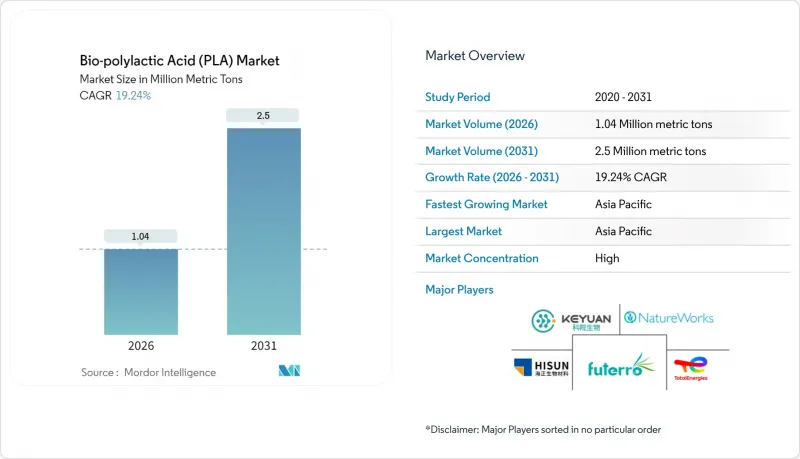

바이오 폴리락트산(PLA) 시장은 2025년에 87만 메트릭톤으로 평가되었으며, 예측 기간(2026-2031년)에서 CAGR 19.24%로 성장하여 2026년 104만 메트릭톤에서 2031년까지 250만 메트릭톤에 달할 것으로 추정되고 있습니다.

일회용 플라스틱에 대한 강력한 법적 규제 압력, 아시아 지역의 생산능력 증가로 인한 급속한 비용 하락, 획기적인 효소 재활용 기술의 발전으로 바이오 폴리락트산 시장은 틈새 시장에서 주류 재료 솔루션으로 전환되었습니다. 수요 증가는 더 이상 경질 및 연질 포장재에 국한되지 않고, 고온 환경에서의 자동차 내장재, 의료기기, 3D 프린팅 전자기기 등에서 석유 유래 폴리머의 성능 기준에 필적하거나 이를 능가하는 고급 등급이 채택되고 있습니다. 원료 대체에서는 옥수수에 비해 탄소강도가 낮고 가격이 더 안정적인 사탕수수와 사탕무 원료가 주도적인 역할을 하고 있습니다. 한편, 지리적으로는 아시아태평양의 생산기지가 원가 우위를 확보하여 세계 경쟁력의 기반을 뒷받침하고 있습니다. 경쟁 환경은 유동적이며, 기존 업체들은 원료 공급원과 가까운 곳에 세계적 수준의 공장을 확장하고, 신규 진입 업체들은 독자적인 탈중합 효소를 활용하여 유럽, 북미, 일본 등지에서 지속가능성을 중시하는 계약을 따내고 있습니다.

일련의 규제로 인해 많은 제품에서 인증된 퇴비화성이 법적 요건이 되면서 바이오 폴리락트산 시장의 수요가 가속화되고 있습니다. 캘리포니아주 AB 1201법(2026년 시행)은 퇴비화 가능 라벨을 미국 농무부(USDA) 국가 유기농 프로그램 기준을 충족하는 재료로 제한하여 사실상 미달하는 바이오플라스틱을 시장에서 퇴출시킬 것입니다. 뉴사우스웨일즈주가 2025년부터 시행하는 광범위한 일회용 규제에 따라 호주 표준 인증이 PLA로 빠르게 대체될 것입니다. 2024년 발표된 백악관 플라스틱 전략은 2027년까지 연방정부의 일회용 플라스틱 조달을 폐지하고, 수십만 톤 규모의 추가 수요에 해당하는 기관용 유통 경로를 개척하는 것을 목표로 하고 있습니다. 남호주에서 2025년 비인증 생분해성 라벨을 금지함에 따라, 규정 준수 프레임워크가 더욱 강화되고 구매 사양이 고순도 PLA 등급으로 전환될 것입니다.

바이오 폴리락트산 시장에서 비용 절감의 결정적 국면은 아시아태평양에서 전개되고 있습니다. 네이처웍스는 태국에 7만 5,000톤 규모의 사탕수수 원료 플랜트 건설을 위해 3억 5,000만 달러를 확보해 세계 최고 수준의 경제성을 확보할 수 있는 높은 자본집약도를 보여줬습니다. 에미레이트 바이오텍은 2028년 가동 예정인 UAE의 대형 시설에 설저의 기술을 도입하여 아시아 및 중동 지역에서의 입지를 더욱 확대할 예정입니다. 인도의 설탕 대기업인 발람푸르 치니 밀스(Balampur Chini Mills)는 7만 5,000톤 규모의 PLA 생산라인에 2,000억 인도 루피를 투자하여 지역 원료의 우위를 유지하면서 중국 외 지역으로 다변화를 추진하는 좋은 사례입니다. 대형 플랜트들이 범용 제품 등급에 집중하는 동안, 틈새 제조업체들은 특수 합금 개발 및 인증된 저탄소발자국을 통해 고가 전략을 유지하고 있습니다.

시험 대상 경질 PLA 제품 5개 중 4개 제품만 모의 퇴비화 조건에서 완전 분해가 이루어졌으며, 일부 샘플에서 미세 플라스틱 조각이 검출되었습니다. 이는 퇴비화 환경이 최적이 아닐 경우의 성능 부족을 보여줍니다. 미국의 쓰레기 처리 담당자들은 퇴비화 가능 품목과 비퇴비화 가능 품목을 분리하는 것이 재정적, 운영적으로 비현실적이라고 보고하고 있으며, 소비자의 의도와 상관없이 많은 폐기물이 매립되고 있다고 보고하고 있습니다. 미국 국가 유기농 프로그램(NOP)은 현재 상업용 생분해성 멀칭 필름이 바이오 기반 및 분해 요건을 충족하지 못한다고 판단하여 PLA가 수익성 높은 농업 분야에 진입하는 것을 막고 있습니다. 인프라 부족은 라틴아메리카, 남아시아, 아프리카에서 더욱 두드러지며, 도시 고형 폐기물의 5% 미만이 관리된 퇴비화 처리를 받고 있습니다. 문전수거 시스템이 확대되기 전까지는 생분해성 주장은 정책 입안자와 소비자에게 공허하게 들릴 수 있으며, 바이오폴리락산 시장의 보급 곡선을 주기적으로 둔화시킬 수 있습니다.

2025년 기준, 사탕수수와 사탕무가 바이오 폴리락트산 시장의 62.10%를 차지하며 19.93%의 CAGR로 성장하고 있으며, 이는 원료 조달의 대폭적인 구조조정을 시사합니다. 사탕수수 발효는 옥수수계 원료에 비해 열대지방에서 재배할 경우 비료와 관개를 최소화할 수 있기 때문에 공정 CO2 배출량이 적습니다. 토탈에너지스 코비온의 라욘 공장은 현지에서 생산된 사탕수수 당밀을 활용하여 수입 옥수수 전분 대비 물류 배출량을 15% 절감했습니다. ISCC PLUS 인증을 획득하여 유럽 에코라벨 획득이 가능합니다. 브라질과 태국의 생산자들은 사탕수수 찌꺼기(사탕수수 찌꺼기)의 코제너레이션 도입을 계획하고 있으며, 라이프사이클 분석을 통해 순음성(net negative) 프로파일을 달성할 수 있도록 추진하고 있습니다.

옥수수는 여전히 북미에서 중요한 생산량을 유지하고 있습니다. 기존 습식 제당 설비와 확립된 효소 공급망이 기존 공장의 PLA 생산 전환에 대한 자본 장벽을 낮추기 위함입니다. 카사바는 베트남, 인도네시아, 나이지리아에서 풍부하게 생산되는 비식용 대체 원료로 주목받고 있습니다. 높은 전분 함량과 적당한 농업 투입으로 현지에 건조시설이 갖추어지면 저비용 젖산 생산의 길을 열 수 있습니다. 조사에 따르면 당밀 원료는 10만 톤 규모의 플랜트에서 운영 비용을 37% 절감할 수 있어 수직 통합형 설탕 그룹에게 매력적인 다각화 선택이 될 수 있다고 합니다.

바이오 폴리락트산 보고서는 원료별(옥수수, 카사바, 사탕수수/ 사탕무, 기타 원료), 형태별(섬유, 필름/시트, 코팅, 기타 형태), 최종사용자 산업별(포장, 의료, 전자기기, 농업, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동. 아프리카)로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

아시아태평양은 2025년 바이오 폴리락트산 시장의 40.50%를 차지할 것으로 예상되며, 22.14%의 CAGR은 이 지역이 가장 큰 소비지이자 가장 낮은 비용의 생산지라는 이중적인 역할을 하고 있음을 보여줍니다. 태국 투자 위원회의 바이오플라스틱에 대한 세제 혜택 정책은 프로젝트 회수 기간을 6년으로 단축하고, 네이처웍스 및 지역 설탕 대기업의 신규 라인 확장을 촉진하고 있습니다. 중국에서는 2025년 플라스틱 오염 목표 달성을 위해 국내 포장 브랜드가 EPS 조가비 용기를 PLA로 대체하고 있습니다. 수출량이 증가하는 가운데 내수 수요가 증가하고 있습니다. 인도에서는 에탄올 혼합 추진으로 사탕수수 생산의 일부를 전환하는 한편, 통합 제당공장에서는 당밀을 발효시켜 젖산을 PLA 원료로 제조하여 부가가치를 창출하고 수익원을 안정화시키고 있습니다.

북미에서는 연방 조달 단계적 폐지, 캘리포니아주의 퇴비화 가능 표시 의무화 등 명확한 규제 추진의 혜택을 누리고 있지만, 해안 대도시 지역 외에는 산업 퇴비화 인프라가 여전히 부족합니다. 중서부 지역의 낮은 매립지 처리 비용으로 인해 상업용 퇴비 업체들의 확장 의지가 약화되어 브랜드 소유주들의 강한 관심에도 불구하고 바이오 폴리락트산 시장의 침투를 억제하고 있습니다. 시애틀과 오스틴에서 PLA 생산자와 폐기물 수거업체가 공동으로 전용 수거 경로를 구축한 것은 순환 루프의 확장 가능한 청사진을 보여주고 있습니다.

유럽은 폐쇄형 루프 파일럿 사업에서 선도적인 위치를 유지하고 있으며, ENZYCLE 프로젝트는 연간 2,000톤 규모의 탈중합 플랜트에서 기술적 타당성을 입증했습니다. EU의 엄격한 포장재 과세 제도는 브랜드 소유주들이 바이오 기반 소재와 재생 가능 소재를 채택하도록 장려하고, 화석 유래 대체품에 대한 가격 프리미엄을 지지하고 있습니다. 남미와 중동 및 아프리카에서 새로운 기회가 창출되고 있습니다. 브라질의 설탕 잉여는 PLA의 경제성에 부합하며, UAE의 대형 시설은 할랄 인증 식품을 위한 저탄소 포장을 원하는 지역 가공업체에 서비스를 제공합니다. 다만, 생활쓰레기 유기물 회수 시스템 미비로 인해 소비자 측면에서의 퇴비화 혜택이 제한되어 완전순환형 도입이 늦어지고 있습니다.

The Bio-polylactic Acid (PLA) Market was valued at 0.87 Million metric tons in 2025 and estimated to grow from 1.04 Million metric tons in 2026 to reach 2.5 Million metric tons by 2031, at a CAGR of 19.24% during the forecast period (2026-2031).

Strong legislative pressure on single-use plastics, rapid cost deflation from Asian capacity additions, and breakthrough enzymatic recycling technologies have moved the Bio-polylactic Acid market from a niche to a mainstream materials solution. Demand growth is no longer confined to rigid and flexible packaging, as high-heat automotive interiors, medical devices, and 3D-printed electronics adopt advanced grades that match or exceed petro-polymer performance benchmarks. Sugarcane and sugar beet feedstocks lead raw-material substitution on the back of lower carbon intensity and more stable pricing compared with corn, while geographically the Asia-Pacific production base secures the cost leadership that underpins global competitiveness. Competitive dynamics remain fluid: incumbent producers scale world-class plants close to feedstock sources, and new entrants leverage proprietary depolymerization enzymes to win sustainability-driven contracts in Europe, North America, and Japan.

A cascade of regulations accelerates the Bio-polylactic Acid market demand by making certified compostability a legal requirement for numerous products. California's AB 1201, effective in 2026, restricts compostable labels to materials that meet USDA National Organic Program standards, effectively removing subpar bioplastics from the shelf. New South Wales' enforcement of extensive single-use restrictions from 2025 prompts rapid substitution toward PLA certified to Australian standards. The White House Plastic Strategy, announced in 2024, eliminates federal procurement of single-use plastics by 2027, opening institutional channels equivalent to several hundred thousand tons of incremental demand. South Australia's 2025 ban on non-certified compostable labels further tightens compliance frameworks and shifts purchasing specifications toward high-purity PLA grades.

Asia-Pacific hosts the pivotal cost-down phase of the Bio-polylactic Acid market. NatureWorks secured USD 350 million to build a 75,000-ton sugarcane-based plant in Thailand, illustrating the capital intensity required to achieve globally competitive economics. Emirates Biotech selected Sulzer technology for a UAE mega-facility that will commence operations in 2028, further enlarging the Asian and Middle-East footprint. Indian sugar player Balrampur Chini Mills is investing INR 2,000 crores in a 75,000 ton PLA line, exemplifying diversification beyond China while retaining regional feedstock advantages. As larger plants focus on commodity grades, niche producers defend premium pricing through specialty alloy development and certified low-carbon footprints.

Only four out of five tested rigid PLA items achieved full disintegration under simulated composting, and some samples emitted microplastic fragments, revealing performance shortfalls when compost envelope conditions are sub-optimal. Municipal waste managers in the United States report that separating compostable from non-compostable items is financially and operationally unworkable, forcing many loads into landfills despite consumer intentions. The U.S. National Organic Program currently finds that no commercial biodegradable mulch film meets its biobased and degradation requirements, blocking PLA entry into a potentially lucrative agricultural segment. Infrastructure scarcity is even more pronounced in Latin America, South Asia, and Africa where less than 5% of municipal solid waste passes through controlled composting. Until curbside systems scale, claims of biodegradability may ring hollow for policymakers and consumers, periodically slowing the Bio-polylactic Acid market adoption curve.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Sugarcane and sugar beet supplied 62.10% of the Bio-polylactic Acid market share in 2025, rising on a 19.93% CAGR trajectory that signals a deep realignment of raw-material sourcing. Sugarcane fermentation yields lower process CO2 than corn variants because crop cultivation requires minimal fertilizer and irrigation inputs in tropical geographies. TotalEnergies Corbion's Rayong line leverages local cane syrup, trimming logistics emissions by 15% compared with imported corn starch and ensuring ISCC PLUS certification that unlocks European eco-label access. Producers in Brazil and Thailand plan to integrate bagasse cogeneration to push life-cycle analysis toward net-negative profiles.

Corn retains meaningful volume in North America because existing wet-milling assets and established enzyme supply chains reduce capital barriers for brownfield PLA retrofits. Cassava obtains attention as a non-food alternative plentiful in Vietnam, Indonesia, and Nigeria; its high starch content and moderate agronomic inputs present a path to low-cost lactic acid when local drying capacity is available. Research demonstrates that molasses feedstocks can cut operating costs by 37% at 100,000-ton scale plants, giving vertically integrated sugar groups a compelling diversification option.

The Bio-Polylactic Acid Report is Segmented by Raw Material (Corn, Cassava, Sugarcane and Sugar Beet, and Other Raw Materials), Form (Fiber, Films and Sheets, Coatings, and Other Forms), End-User Industry (Packaging, Medical, Electronics, Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific commanded 40.50% Bio-polylactic Acid market share in 2025, and its 22.14% CAGR underscores the region's dual role as the largest consumer and the lowest-cost producer. Thailand's policy of Board of Investment tax breaks for bioplastics cuts project payback periods to six years, encouraging NatureWorks and regional sugar conglomerates to scale new lines. China's domestic packaging brands substitute PLA for EPS clamshells to meet 2025 plastic-pollution targets, lifting local demand even as export volumes grow. India's ethanol-blending push diverts some sugarcane output, but integrated mills capture additional value by fermenting molasses into lactic acid for PLA, stabilizing revenue streams.

North America benefits from clear regulatory impetus, such as the federal procurement phase-out and California's compostability labeling, yet industrial composting infrastructure remains patchy outside coastal metros. Landfill tipping fees in the Midwest remain low, reducing economic incentives for commercial composters to expand, which tempers Bio-polylactic Acid market penetration despite strong brand owner interest. Collaboration between PLA producers and waste haulers to establish dedicated pickup routes in Seattle and Austin demonstrates scalable blueprints for circular loops.

Europe maintains leadership in closed-loop pilots, with the ENZYCLE project proving technical feasibility at 2,000 ton annual capacity depolymerization plants. Stringent EU packaging levy structures push brand owners to adopt bio-based and recyclable content, thereby supporting a price premium over fossil alternatives. South America and the Middle East and Africa present nascent opportunities: Brazil's sugar surplus aligns well with PLA economics, while the UAE mega-facility will serve regional converters seeking low-carbon packaging for halal certified foods. Absence of curbside organics collection, however, restricts consumer-side composting benefits, delaying full-cycle adoption.