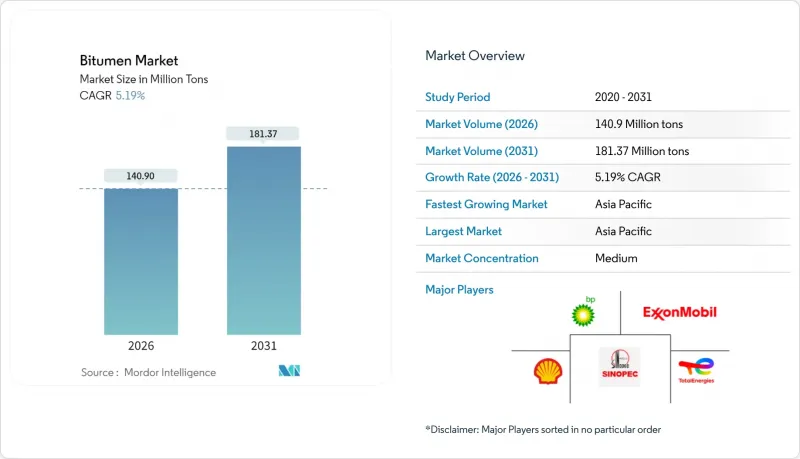

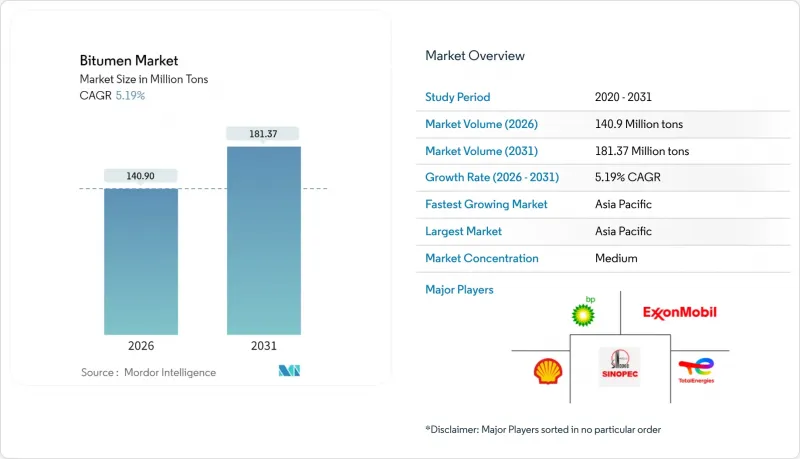

역청 시장은 2025년 1억 3,395만 톤에서 2026년에는 1억 4,090만 톤으로 성장하여 2026년부터 2031년까지 CAGR 5.19%를 기록하며 2031년까지 1억 8,137만 톤에 달할 것으로 예측됩니다.

고속도로, 공항 활주로, 기후변화에 강한 포장에 대한 공공부문의 지출 증가는 장기적인 수요를 뒷받침하고 있으며, 고분자 개질 배합 기술은 고수익 틈새시장을 개척하고 있습니다. 2024년 유가 안정은 원료비 예측 가능성을 가져왔지만, 2026년까지 배럴당 66달러까지 하락할 것으로 예상됨에 따라 생산 마진 확대와 가격 경쟁의 심화가 동시에 발생할 수 있습니다. 아시아태평양은 적극적인 인프라 투자와 중동 산유국의 가격 우위를 활용한 유연한 수입 전략에 힘입어 여전히 주요 소비 거점입니다. 동시에 환경 규제 강화로 인해 저온 에멀전 및 재생 아스팔트 기술로의 전환이 가속화되면서 역청 시장의 공급망과 제품 사양이 미묘하게 변화하고 있습니다.

각국 정부는 예산을 신규 건설에서 보전에 재분배하고 있으며, 이는 침투성 바인더와 특수 표면처리 재료의 안정적이고 지속적인 소비로 이어지고 있습니다. 미국 인프라 투자 고용법은 이미 6만 개 이상의 건설 프로젝트를 시작했으며, 퀘벡 주정부만 해도 2025-2026년 예산안에 도로 정비에 358억 6,800만 캐나다 달러를 책정했습니다. 관련 기관은 적기 보전에 1달러를 투자할 때마다 4-7달러의 미래 재건 비용을 절감할 수 있다는 것을 인식하고 유지관리 수요의 선순환 구조를 확립하고 있습니다. 독일의 5,000억 유로 규모의 현대화 기금은 자산 최적화에 20%를 할당하고, 기후 적응형 역청 등급의 사양을 더욱 강화하는 내성 기준을 포함하고 있습니다. 포장 관리 시스템이 성숙해짐에 따라, 조달 형태는 주기적인 급등에서 예측 가능한 다년 계약으로 전환되어 전체 역청 시장 조달량을 안정화시키고 있습니다.

활주로 프로젝트에는 높은 휠 하중, 전단 응력, 제트 연료 누출을 견딜 수 있는 고품질 바인더가 요구됩니다. 걸프 지역과 아시아 허브 공항이 주도하는 2030년까지 7,300억 달러 규모의 설비투자 계획은 에너지 인프라와 항공시설 확충이 연계되어 있습니다. 프랑크푸르트 공항에서 수행된 캐슈넛 껍질 바이오 역청을 사용한 2년간의 시험 구간은 성능 저하 없이 저탄소 소재를 추구하는 항공사의 자세를 보여주고 있습니다. 스티렌-부타디엔-스티렌계 폴리머 개질 등급은 15-25%의 가격 프리미엄을 획득하고 있으며, 생산량은 여전히 적지만 부문의 수익성을 높이고 있습니다. 국제민간 항공기구(ICAO) 기준에 부합하는 혼합 설계 인증을 획득할 수 있는 공급업체는 장기적인 프레임워크 계약을 체결할 수 있는 위치에 있으며, 역청 시장에서의 수직 통합 전략을 강화할 수 있습니다.

규제 당국은 휘발성유기화합물(VOC) 및 다환방향족탄화수소(PAH)의 노출 한계치를 강화하고 있습니다. 캐나다에서는 2025년 10월까지 PAH 함량이 1,000ppm을 초과하는 콜타르계 실란트 사용을 금지하여 기존 제품군을 사실상 퇴출하고 재배합을 의무화합니다. 가스 크로마토그래피와 머신러닝을 결합한 예측 분석을 통해 냄새의 원인이 되는 알칸을 식별할 수 있게 되어 규제 대응의 길을 제시하고 있습니다. 그러나 이로 인해 분석 비용이 증가하여 중소 생산자가 그 부담을 떠안게 됩니다. 또한, 각 기관은 포장 온도를 최대 40℃까지 낮추는 온배합 기술을 채택하는 경향이 있습니다. 이로 인해 현장 배출량이 감소하고, 핫믹스 아스팔트의 운영 범위가 좁아져 역청 시장의 수요 확대를 억제할 수 있습니다.

침투급 바인더는 2025년 역청 시장 점유율의 66.52%를 차지할 것으로 예상되며, 기존 핫믹스 플랜트와의 호환성 및 광범위한 기후 적응성으로 인해 2031년까지 CAGR 5.62%로 확대될 것으로 예상됩니다. 산화 등급은 방수 및 지붕재 틈새 분야에서 산화 안정성으로 인해 프리미엄 가격 책정이 정당화되는 용도에 사용됩니다. 전 세계적으로 800만 톤에 달하는 역청 에멀전은 에너지 사용량 감소와 작업 영역의 배출량 감소로 인해 칩 씰링 및 미세 표면처리 응용 분야에서 점점 더 많은 지지를 받고 있습니다.

기술 혁신은 점도 제어와 친환경 첨가제에 초점을 맞추고 있습니다. 폴리인산을 1% 첨가하면 고온 안정성이 향상되지만, 2%를 초과하면 저장 안정성이 떨어질 수 있습니다. 이란산 천연 아스팔트 등 바이오 기반 개질제는 점도와 열가소성을 높여 수명을 연장하고 합성 폴리머에 대한 의존도를 낮춥니다. 이러한 점진적인 개선으로 침투성 등급의 우위는 유지되는 한편, 역청 시장 내에서는 특수 배합 제품으로의 가치 전환이 서서히 진행되고 있습니다.

역청 보고서는 제품 유형(침투 등급, 산화 등급, 역청 에멀전, 고분자 개질 역청, 기타 제품), 용도(도로 건설, 지붕재, 접착제 및 실란트, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카) 별로 분류됩니다. 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

아시아태평양은 2025년 45.10%의 점유율로 1위를 차지할 것이며, 중국, 인도, 동남아시아의 동기화된 인프라 계획을 바탕으로 2031년까지 CAGR 6.31%로 확대될 것으로 예상됩니다. 중국의 2023년 원유 처리량 1,480만 배럴/일은 국내 아스팔트 공급과 수출 능력을 모두 뒷받침하고 있습니다.

북미에서는 탄탄한 도로 보수 예산과 진화하는 환경 규제가 균형을 이루고 있습니다. IIJA(인프라 투자 및 고용법)에 따른 파이프라인 수요는 안정적이지만, 캐나다의 PAH 규제는 유화 역청과 콜드 프로세스로의 전환을 촉진하고 있습니다. 유럽에서는 정유공장 합리화가 진행되어 폐쇄로 인해 지역 공급이 타이트한 반면, 바이오 기반 대체품의 시장 기회가 창출되고 있습니다. 유럽의 역청 시장 규모는 톤수 기준으로는 소폭 축소될 가능성이 있지만, 특수 등급이 범용 등급을 상회하기 때문에 금액 기준으로는 확대될 것으로 예상됩니다.

중동지역은 풍부한 원자재와 전략적 해운 루트를 활용하여 아시아에 공급하고 있습니다. 걸프 산유국과 아시아 바이어 간 거래액은 2030년까지 6,820억 달러에 달할 것으로 예상되며, 원유 흐름에 더해 완제품 바인더와 개질제도 유통될 것으로 전망됩니다.

아프리카와 남미는 신흥시장으로 간헐적으로 수요가 급증하는 메가 프로젝트가 특징입니다. 이들 지역이 연결성에 대한 투자를 확대하는 가운데 유연한 물류와 신속한 배포가 가능한 공급업체는 존재감을 높일 수 있습니다.

The Bitumen Market is expected to grow from 133.95 Million tons in 2025 to 140.9 Million tons in 2026 and is forecast to reach 181.37 Million tons by 2031 at 5.19% CAGR over 2026-2031.

Heightened public-sector spending on highways, airport runways, and climate-resilient pavements is sustaining long-run demand, while polymer-modified formulations open higher-margin niches. Stable crude-oil prices in 2024 created predictable feedstock economics, yet the projected slide to USD 66 per barrel by 2026 could both widen production margins and intensify price competition. Asia-Pacific remains the pivotal consumption hub, boosted by aggressive infrastructure outlays and flexible import strategies that exploit Middle-Eastern price discounts. Concurrently, environmental regulations accelerate the transition toward low-temperature emulsions and recycled asphalt technologies, subtly reshaping supply chains and product specifications within the bitumen market.

Governments are reallocating budgets from new builds toward preservation, leading to steady recurrent consumption of penetration-grade binders and specialty surface treatments. The U.S. Infrastructure Investment and Jobs Act has already launched more than 60,000 construction projects, and Quebec alone earmarked CAD 35.868 billion for roads in its 2025-2026 budget. Agencies recognize that every dollar invested in timely preservation avoids USD 4-7 in future reconstruction costs, locking in a virtuous cycle of maintenance demand. Germany's EUR 500 billion modernization fund assigns 20% to asset optimization, embedding resilience criteria that further elevate specifications for climate-adaptive bitumen grades. As pavement management systems mature, procurement shifts from cyclical surges to predictable multi-year contracts, stabilizing volume offtake across the bitumen market.

Runway projects require premium binders that tolerate high wheel loads, shear stresses, and jet-fuel spills. Gulf and Asian hubs are leading a USD 730 billion capex wave through 2030, intertwining energy infrastructure with aviation build-outs. Frankfurt Airport's two-year test strip using cashew-shell bio-bitumen illustrates airlines' push for lower-carbon materials without performance sacrifice. Polymer-modified grades with styrene-butadiene-styrene command price premiums of 15-25%, lifting segment profitability even though volumes remain modest. Suppliers capable of certifying mix designs to International Civil Aviation Organization standards are positioned to capture long-run framework agreements, reinforcing vertical integration strategies within the bitumen market.

Regulators are tightening exposure limits for volatile organic compounds and polycyclic aromatic hydrocarbons. Canada will prohibit coal-tar sealants exceeding 1,000 ppm PAHs by October 2025, effectively removing a traditional product class and forcing reformulations. Predictive analytics using gas chromatography coupled with supervised learning now pinpoint odor-causing alkanes, offering compliance pathways but raising analytical costs that smaller producers must absorb. Agencies also favor warm-mix technologies that lower placement temperatures by up to 40 °C, reducing on-site emissions and tightening the operating envelope for hot-mix asphalt, thereby constraining volume expansion in the bitumen market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Penetration-grade binders held 66.52% of the bitumen market share in 2025 and are projected to grow at a 5.62% CAGR through 2031, sustained by compatibility with conventional hot-mix plants and broad climatic tolerance. Oxidized grades occupy niche waterproofing and roofing roles where oxidation stability justifies premium pricing. Bitumen emulsions, totaling 8 million tons globally, are gaining favor for chip seals and microsurfacing because they reduce energy use and lower work-zone emissions.

Innovation centers on viscosity control and ecological additives. Polyphosphoric acid at 1% dosage improves high-temperature stability, though concentrations beyond 2% can undermine storage stability. Bio-based modifiers such as Iranian natural asphalt enhance viscosity and thermoplasticity, extending service life and reducing reliance on synthetic polymers. These incremental gains sustain penetration-grade primacy but gradually shift value toward specialty formulations inside the bitumen market.

The Bitumen Report is Segmented by Product Type (Penetration Grade, Oxidized Grade, Bitumen Emulsions, Polymer-Modified Bitumen, and Other Products), Application (Road Construction, Roofing, Adhesives and Sealants, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific led with 45.10% share in 2025 and is advancing at a 6.31% CAGR to 2031, anchored by synchronized infrastructure programs across China, India, and Southeast Asia. China's processing of 14.8 million barrels per day of crude in 2023 underpins both domestic asphalt supply and export capabilities.

North America balances robust rehabilitation budgets with evolving environmental mandates. The IIJA pipeline stabilizes demand, but Canada's impending PAH restrictions catalyze a shift to emulsions and cold processes. Europe confronts refinery rationalization; closures tighten regional supply yet open market space for bio-based alternatives. The bitumen market size in Europe could contract marginally in tonnage yet expand in value as specialty grades outpace generic ones.

The Middle East leverages abundant feedstock and strategic shipping lanes to supply Asia. Trade between Gulf producers and Asian buyers is forecast to touch USD 682 billion by 2030, with finished binders and modifiers joining crude flows.

Africa and South America remain emergent, characterized by episodic megaprojects that create demand surges. Suppliers attuned to flexible logistics and rapid deployment can gain traction as these regions scale connectivity investments.