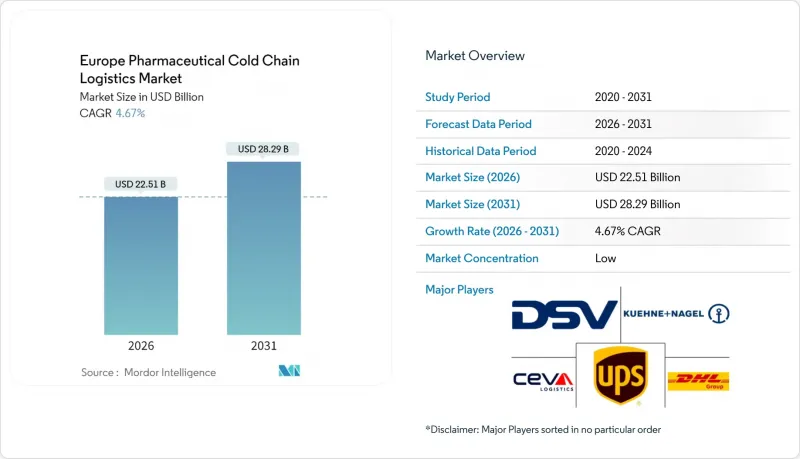

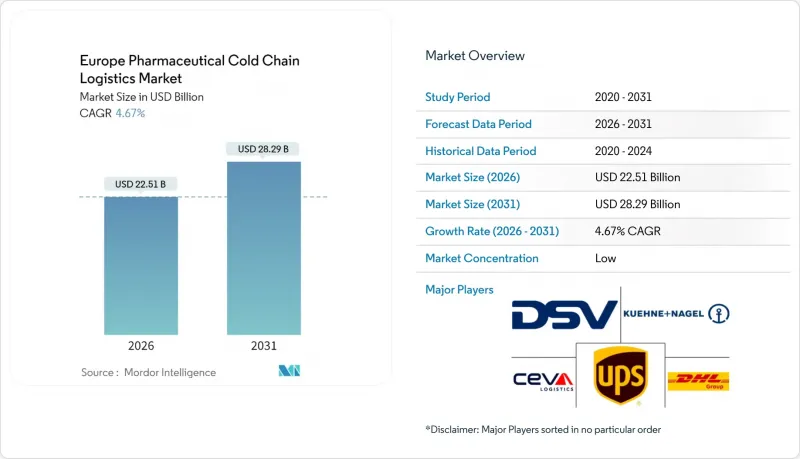

유럽의 의약품 콜드체인 물류 시장은 2025년에 215억 달러로 평가되었으며, 2026년 225억 1,000만 달러에서 2031년까지 282억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.67%로 예상됩니다.

특히 세포 및 유전자 치료를 위한 -120℃ 이하의 초저온 서비스 수요는 이러한 확장의 가장 중요한 촉진요인으로 작용하고 있습니다. 이에 따라 물류기업들은 기존의 2-8℃ 솔루션을 훨씬 뛰어넘는 극저온 냉동고, 드라이시퍼, 이중화 전원 시스템을 도입할 수밖에 없는 상황입니다. 유럽 의약품 콜드체인 물류 시장은 바이오의약품 수요의 지속적 확대, EU의 GDP(의약품 유통 적정성 관리) 및 시리얼라이제이션 의무화 강화, HERA(유럽 의약품 긴급대응법)에 따른 대규모 팬데믹 대응 예산(국가 비축 의약품의 장기적 공급량 증가 요인)의 수혜를 받고 있습니다. 계속되고 있습니다. 그러나 에너지 가격 변동, 운전자 부족, GMP(의약품 제조 및 품질 관리기준) 대응 인력 부족으로 인해 운영비용이 증가하면서 유럽 의약품 콜드체인 물류 시장 전체가 자동화 투자를 가속화하고 있습니다. UPS, DHL, DSV와 같은 세계 통합 기업들이 국경 간 실시간 배치 레벨 온도 보장을 약속하는 인수 및 디지털 시각화 도구에 적극적으로 투자하고 있어 경쟁이 치열해지고 있습니다.

단클론항체, mRNA 백신, 자가 세포 제품 개발 파이프라인의 확대로 유럽에서 신규 승인되는 의약품의 절반이 콜드체인 대상 품목으로 분류되고 있습니다. 이들 중 상당수는 유효성을 유지하기 위해 0-5℃ 또는 -120℃까지 엄격한 환경 관리가 필요합니다. 이 때문에 유럽 의약품 콜드체인 물류 시장에서는 지속적인 전원 백업, 액체 질소실, IoT 센서를 갖춘 GDP 인증 창고에 대한 지속적인 자본 유입이 이루어지고 있습니다. 유럽의약품청(EMA)에 품질 리스크 평가 신청 시, 실시간 운송 경로 적격성 평가와 엔드 투 엔드 감사 추적은 이제 스폰서 기업의 기본 요건이 되었습니다. 기존 2-8℃ 백신 운송을 전문으로 하던 물류 사업자들은 현재 극저온 운송 차량 보유 능력, ±2℃ 이내의 온도 편차 디지털 검증, 21 CFR Part 11 준수 데이터 즉시 생성 등의 측면에서 차별화를 꾀하고 있습니다.

팬데믹 이후 소비자 행동은 처방전 생물학적 제제의 택배를 선호하는 경향이 있으며, 북유럽 국가의 약국 및 원격의료 플랫폼은 배송업체에 구애받지 않는 API를 통합하고 실시간 온도 검증 용량을 기반으로 배송업체에 물량을 할당하도록 장려하고 있습니다. 이러한 추세에 따라 유럽의 의약품 콜드체인 물류 시장에서는 병원 창고로의 대형 팔레트 운송을 대신하여 2-8℃의 안정성을 유지하면서 24시간 자율성을 실현하는 상변화물질(PCM)을 내장한 소형 단열 배송용기의 도입이 요구되고 있습니다. 또한, 환자 단위 배송에 대한 국가별 GDP 라이선스 규정의 차이를 조정하고, 디지털 라벨, 배송 증명 사진, 자동화된 반품 물류를 단일 컴플라이언스 대응 워크플로우로 통합해야 합니다.

주요 산업 클러스터 전체에서 전기요금이 2022년 이전 평균치보다 30-60% 높은 수준이 지속되고 있어 냉장설비 운영비용(OPEX)이 상승하고, 신규 GDP 시설의 투자회수기간(ROI)이 길어지고 있습니다. 동시에 EU 그린딜 지침에 따른 탄소발자국 보고 의무가 부과되어 사업자는 단열 패널 업그레이드, 저GWP 냉매로의 전환, 옥상 태양광 패널 설치가 요구되고 있습니다. 이러한 자본 집약적인 리노베이션은 컴플라이언스 기준이 강화되는 가운데 유럽 의약품 콜드체인 물류 시장의 수익률을 압박하고 있습니다.

2025년 기준, 운송 부문은 유럽 의약품 콜드체인 물류 시장 점유율의 61.40%를 차지했습니다. 이는 조화롭고 엄격한 GDP 규제 하에 200개 이상의 국경 횡단 회랑을 연결하는 대륙의 촘촘한 도로망에 의해 뒷받침되고 있습니다. 도로 화물 운송이 주류인 이유는 팔레트 단위 추적, 검증된 냉동 유닛, 공항에서의 화물 수령을 생략하는 매장 직송 모델을 지원하기 때문입니다. 항공화물 운송은 여전히 고가 및 초저온 운송품에 필수적이지만, 수익성 관리로 인해 안정성 요건이 까다로운 고부가가치 치료제에 대한 제한적인 이용이 진행되고 있습니다. 이와 병행하여 철도 사업자는 스페인과 독일 간 냉장 화물차 시험 운행을 시작했으며, 탄소 저감을 위한 운송 모드의 다양화를 시사하고 있습니다.

부가가치 서비스는 CAGR 4.03%로 가장 높은 성장률을 보였으며, 직렬화, GDP 감사, 운송 경로 적격성 컨설팅에 대한 수요 증가를 반영하고 있습니다. 현재 의약품 화주들은 유럽 의약품 콜드체인 물류 시장에서 진입 장벽을 높이고, 수수료 기반 수익원을 창출하고, 표준 작업 절차(SOP) 설계, 온도 맵 포장, 실시간 대시보드 기능을 통합할 수 있는 원스톱 파트너를 원하고 있습니다. 이 분야는 또한 데이터 무결성에 대해 물류 사업자에게 공동 책임을 부과하는 규제 조항의 혜택을 누리고 있으며, 몇 초 만에 관리 체인(CoC) 준수를 증명할 수 있는 블록체인 지원 플랫폼에 대한 투자를 촉진하고 있습니다.

냉장화물(0-5℃)은 2025년 유럽 의약품 콜드체인 물류 시장 규모의 40.55%를 차지할 것으로 예상되며, 백신, 인슐린, 단클론항체 등을 포함합니다. 이들 화물은 연중 안정적인 물동량으로 창고 가동률 안정화에 기여하고 있습니다. 사업자는 +15℃, 2-8℃, -20℃의 온도대를 유지할 수 있는 멀티챔버 트럭을 도입하여 배송의 집약화를 꾀하고 있습니다. 이를 통해 배송 밀도를 높이고 킬로미터당 비용을 절감할 수 있습니다.

초저온 부문은 2031년까지 4.48%의 가장 높은 CAGR을 기록할 것으로 예상됩니다. 세포 치료 스폰서 기업은 드라이아이스 팔레트를 피하고, 외부 전원 없이 -10℃를 10일간 유지할 수 있는 액체 질소 드라이시퍼를 채택하고 있습니다. 이를 통해 대륙 간 자가 이식이 가능합니다. 이 틈새 시장은 물류 기업들이 내부 압력 및 경사 이벤트를 모니터링하는 물방울 디지털 추적 시스템에 대한 투자를 장려하여 유럽 의약품 콜드체인 물류 시장 전체의 위험 감소를 강화하고 있습니다.

The Europe Pharmaceutical Cold Chain Logistics Market was valued at USD 21.5 billion in 2025 and estimated to grow from USD 22.51 billion in 2026 to reach USD 28.29 billion by 2031, at a CAGR of 4.67% during the forecast period (2026-2031).

Demand for ultra-low-temperature services-particularly below -120 °C for cell and gene therapies-remains the single most influential driver of this expansion, pressing logistics firms to deploy cryogenic freezers, dry-shippers, and redundant power systems that go far beyond conventional 2-8 °C solutions. The Europe pharmaceutical cold chain logistics market continues to benefit from sustained biologics uptake, stricter EU GDP and serialization mandates, and sizable pandemic-preparedness budgets under HERA that add long-term volume to national stockpiles. However, energy-price volatility, driver shortages, and GMP-skilled labor gaps have raised operating costs and accelerated automation investments across the Europe pharmaceutical cold chain logistics market. Competitive intensity has sharpened as global integrators such as UPS, DHL, and DSV spend aggressively on acquisitions and digital visibility tools that promise real-time, batch-level temperature assurance across borders.

A growing pipeline of monoclonal antibodies, mRNA vaccines, and autologous cell products has pushed half of all new European drug approvals into cold-chain categories, many of which require controlled environments at 0-5 °C or down to -120 °C to preserve potency. The Europe pharmaceutical cold chain logistics market, therefore, sees sustained capital inflows into GDP-certified warehouses fitted with continuous power backups, liquid nitrogen chambers, and IoT sensors. Real-time lane qualification and end-to-end audit trails are now baseline expectations for sponsors submitting to EMA quality-risk assessments. Logistics providers that previously specialized in 2-8 °C vaccines now differentiate on their ability to host cryogenic fleets, digitally verify temperature excursions within +-2 °C, and generate 21 CFR Part 11-compliant data in seconds.

Post-pandemic consumer behavior favors home delivery of prescription biologics, prompting pharmacies and tele-health platforms across the Nordics to integrate carrier-agnostic APIs that allocate shipments to couriers based on real-time temperature-validated capacity. This trend forces the Europe pharmaceutical cold chain logistics market to deploy smaller insulated parcel shippers with phase-change materials engineered for 24-hour autonomy while maintaining 2-8 °C stability, replacing bulk pallet moves to hospital warehouses. Providers must also reconcile diverse national GDP licensing rules for patient-level distribution, bringing digital labeling, photo proof-of-delivery, and automated return logistics into a single compliant workflow.

Electricity tariffs remain 30-60% higher than pre-2022 averages across key industrial clusters, raising refrigeration OPEX and elongating ROI on new GDP facilities. Simultaneously, EU Green Deal mandates require carbon-footprint reporting, pushing operators to upgrade insulation panels, switch to low-GWP refrigerants, and install rooftop solar arrays. These capital-intensive retrofits compress margins in the Europe pharmaceutical cold chain logistics market even as compliance standards climb.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Transportation accounted for 61.40% of Europe's pharmaceutical cold chain logistics market share in 2025, underpinned by the continent's dense road network linking more than 200 cross-border corridors under a harmonized but stringently policed GDP umbrella. Road freight dominates because it supports pallet-level tracking, validated reefer units, and direct store delivery models that remove airport hand-offs. Airfreight remains indispensable for high-value, ultra-low shipments, yet yield management drives selective use to premium therapies with rigid stability profiles. In parallel, rail operators test refrigerated wagons between Spain and Germany, signaling modal diversification aimed at carbon reduction.

Value-added services posted the fastest growth at 4.03% CAGR, reflecting mounting demand for serialization, GDP auditing, and lane-qualification consulting. Pharma shippers now seek one-stop partners able to integrate SOP design, temperature-map packaging, and real-time dashboarding-capabilities that elevate barriers to entry and generate fee-based revenue streams within the Europe pharmaceutical cold chain logistics market. The segment also benefits from regulatory clauses that hold logistics providers jointly liable for data integrity, incentivizing investment in blockchain-ready platforms that can prove chain-of-custody compliance in seconds.

Chilled cargo (0-5 °C) represented 40.55% of the Europe pharmaceutical cold chain logistics market size in 2025, encompassing vaccines, insulins, and monoclonals whose volume streams stabilize warehouse utilization throughout the year. Operators adopt multi-chamber trucks capable of holding +15 °C, 2-8 °C, and -20 °C zones to consolidate deliveries, sharpening drop density and decreasing cost per kilometer.

Deep-frozen/ultra-low segments record the highest CAGR at 4.48% through 2031. Cell therapy sponsors bypass dry ice pallets in favor of liquid nitrogen dry-shippers that maintain -150 °C for 10 days without external power, enabling intercontinental autologous transfers. This niche compels logistics firms to invest in droplet-digital tracking that monitors internal pressure and tilt events, thereby enhancing risk mitigation across the Europe pharmaceutical cold chain logistics market.

The Europe Pharmaceutical Cold Chain Logistics Market Report is Segmented by Services (Transportation, Warehousing and Distribution, and More), Temperature Type (Chilled, Frozen, Ambient, and More), Product (Generic Drugs, Branded Drugs, and More), End User (Pharmaceutical Manufacturers, Biotech & Biosimilar Manufacturers, and More), Country (Germany, France, and More). The Market Forecasts are Provided in Terms of Value (USD).