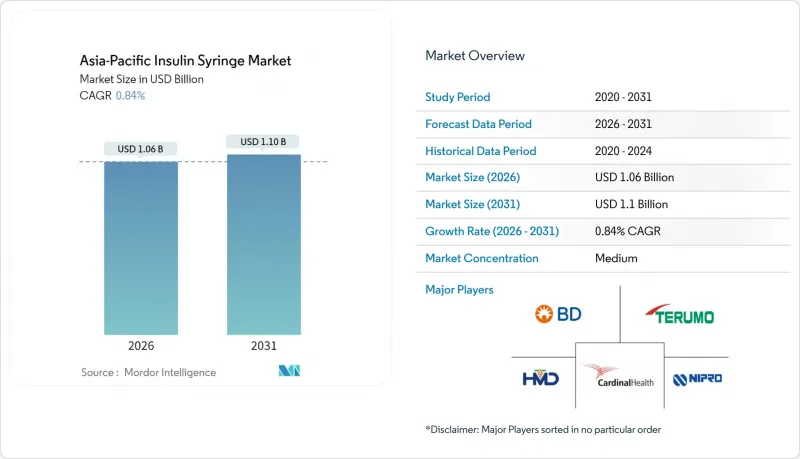

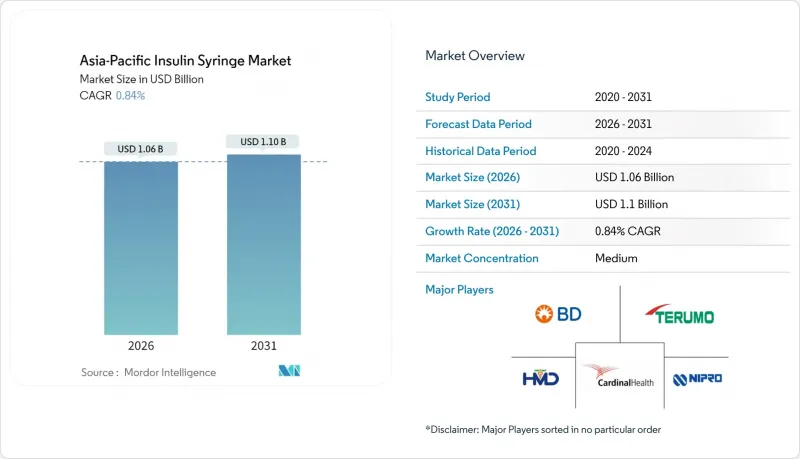

아시아태평양의 인슐린 시린지 시장 규모는 2026년에 10억 6,000만 달러로 추정됩니다.

이는 2025년 10억 5,000만 달러에서 성장한 수치이며, 2031년에는 11억 달러에 달할 것으로 예상됩니다. 2026년부터 2031년까지 연평균 성장률(CAGR) 0.84%로 예상됩니다.

당뇨병 환자 증가, 펜형 주사기를 기피하는 환자에 대한 보험 적용 확대, CGM(연속 혈당 모니터링)에 기반한 기본 및 추가 인슐린 투여 프로토콜, 안전성 중심의 기술 혁신이 수요를 뒷받침하는 반면, 펜형 기기와의 경쟁, 일회용 플라스틱 규제, 가격 동결이 전체 성장을 억제하고 있음. 성장을 억제하고 있습니다. 벡톤디킨슨, 노보노디스크, 텔모 등이 저데드스페이스와 침 찔림 사고 방지 기능에 집중하는 비용 경쟁력 있는 지역 업체들과 점유율 경쟁을 벌이고 있는 가운데, 경쟁의 강도는 중간 정도에 머물고 있습니다. 지방도시(2, 3급 도시)에서는 디지털 약국이 급증하고 있으며, 재고 소진 해소와 물류비용 절감을 통해 환자에게 직접 배송을 실현하고 있습니다. 환경 규제 강화로 재생 가능 또는 생분해성 수지 블렌드의 연구 개발이 가속화되고 있습니다. 컴플라이언스 비용은 증가하는 반면, 친환경 브랜드의 프리미엄화를 촉진하고 있습니다.

2025년 인도의 1형 당뇨병 발병률은 인구 10만 명당 4.9명에 달합니다. 한편, 비만과 관련된 제2형 당뇨병은 계속 증가하고 있으며, 펜형 주사기가 보급되는 가운데 주사기 수요는 지속되고 있습니다. 일본과 호주에서는 고령층이 하루에 여러 번 주사를 맞아야 하고, 신흥국에서는 신규 진단 환자에 대한 보험 적용이 확대되고 있기 때문에 기존 주사기 수요는 지속될 것입니다. 혼합 인슐린 요법에서 0.3mL 및 0.5mL 용량은 정밀한 투여를 위해 필수적입니다. 의료진은 일회용 펜으로는 미세한 눈금이 부족한 복잡한 용량 조절을 위해 주사기를 선호합니다. 따라서 표면적인 성장률은 낮지만 장기적인 수요는 지속될 것입니다.

중국 국가 약가 기준(NVBP)은 인슐린 가격의 중앙값을 42.08% 인하하여, 1.63일치 급여에서 0.68일치 급여로 인하하여, 비용에 민감한 사용자 계층의 기존 주사기 접근성을 확대했습니다. 인도와 일본도 중앙집중형 입찰을 모방하여 절감된 비용을 유연한 투약량을 필요로 하는 소아 및 노인층에 투입하고 있습니다. 특히 일시적인 치료가 필요한 임신성 당뇨병 환자가 혜택을 받고 있습니다. 2027년까지 정책 추진으로 저소득층의 자부담 비용이 감소하여 아시아태평양의 인슐린 주사기 시장을 뒷받침할 것입니다. 지역무역협정을 통한 아세안으로의 파급효과로 판매량 증가는 더욱 확대될 것입니다.

인도 국내 제조업체는 2025년 전년 대비 13% 성장한 저렴한 가격대의 펜형 주사기를 앞세워 국내 인슐린 매출의 25%를 차지했습니다. 이는 주사기로부터의 영구적인 점유율 전환을 의미합니다. 일본의 내분비 전문의들은 현재 용량의 정확성과 낮은 사회적 편견으로 인해 펜형 주사기를 1차 선택으로 권장하고 있으며, 이로 인해 병원에서 30G 주사바늘을 재주문하는 빈도를 억제하고 있습니다. GLP-1 제제가 인간 인슐린을 능가하는 가운데, 펜형 최적화 카트리지는 규제 및 마케팅 측면에서 지원을 받고 있으며, 2020년대 후반까지 아시아태평양 도시 지역에서 기존 제품의 매출을 더욱 잠식할 것으로 예상됩니다.

0.5mL 포맷은 성인용 기저 및 추가 요법에서 범용성을 반영하여 2025년 아시아태평양 인슐린 주사기 시장 점유율의 45.67%를 차지했습니다. 아시아태평양의 0.5mL 단위 인슐린 주사기 시장 규모는 2026년 4억 8,400만 달러에서 2031년까지 4억 9,100만 달러로 소폭 증가하여 연평균 0.28%로 성장할 것으로 예상됩니다. 한편, 0.3mL 수요는 임신기 및 소아 투여 수요를 배경으로 연평균 1.22%의 CAGR로 확대될 것으로 예상됩니다.

각 제조사들은 저용량에서도 ±1IU의 정밀도를 유지하기 위해 보다 엄격한 공차 성형과 실리콘 처리 스토퍼에 대한 투자를 진행하고 있습니다. 이는 인도와 태국의 신생아 클리닉에서 중요한 요구 사항입니다. 산부인과 병원을 통한 인식개선 활동으로 소형 주사기 보급이 진행되어 비용에 민감한 지역에서도 보급이 촉진되고 있습니다. 인슐린 저항성이 있는 제2형 당뇨병 환자에게는 여전히 1mL 주사기가 필요하지만, 펜형 주사기로의 대체가 진행되면서 그 점유율은 정체된 상태입니다. 특수 용도의 '기타' 포맷은 희석 인슐린 연구에 활용되며, 틈새 수요를 유지하고 있습니다.

30G 부문은 2025년 38.35%의 시장 점유율을 차지하여 아시아태평양의 인슐린 주사기 시장 규모에 4억 7천만 달러를 기여했으며, 31G 이상의 변형은 2031년까지 CAGR 1.39%로 상승할 것으로 예상됩니다. 소비자 조사에서 국내에서는 바늘이 가늘수록 12개월 후 추적조사에서 복약순응도가 12% 더 높은 것으로 확인되었습니다.

마이크로 테이퍼 연삭 및 전해 연마에 대한 투자로 펑크 압력이 15% 감소하여 펜 바늘의 편안함 표준에 필적하는 수준을 달성했습니다. 공급망은 더 높은 게이지의 스테인리스 스틸 와이어로 전환하고 있으며, 주로 점성 인슐린 아날로그에 사용되는 28G-29G 라인에 대한 수요가 타이트한 상태입니다. 더 얇은 게이지가 피하 조직 무결성에 대한 규제 승인을 획득함에 따라, 병원에서는 환자의 거부감을 줄이고 퇴원 절차를 가속화하기 위해 대량 계약으로 전환하고 있습니다.

Asia-Pacific insulin syringes market size in 2026 is estimated at USD 1.06 billion, growing from 2025 value of USD 1.05 billion with 2031 projections showing USD 1.10 billion, growing at 0.84% CAGR over 2026-2031.

Rising diabetes prevalence, expanded reimbursement for pen-averse patients, CGM-guided basal-bolus protocols and safety-engineered innovations underpin demand, while pen-device cannibalization, single-use-plastic legislation and flat pricing temper overall growth. Competitive intensity remains moderate as Becton Dickinson, Novo Nordisk and Terumo defend share against cost-competitive regional players focused on low-dead-space and needlestick-prevention features. Digital pharmacies proliferate across tier-2 and tier-3 cities, mitigating stock-outs and enabling direct-to-patient fulfillment at lower logistics cost. Environmental mandates accelerate R&D into recyclable or biodegradable resin blends, adding compliance costs but fostering premium positioning for eco-conscious brands.

Type 1 incidence reached 4.9 cases per 100,000 in India during 2025, while obesity-linked Type 2 keeps rising, sustaining syringe demand even as pens gain favor. Aging cohorts in Japan and Australia require multiple daily injections, and emerging economies expand coverage for newly diagnosed populations, prolonging relevance of traditional syringes. Precision dosing for mixed insulin regimens makes 0.3 mL and 0.5 mL volumes indispensable. Providers favor syringes for complex titration where disposable pens lack fine-scale graduations. Long-term demand thus persists despite low headline growth.

China's NVBP cut median insulin prices 42.08%, lowering affordability thresholds from 1.63 to 0.68 days' wage and broadening access to conventional syringes for cost-sensitive users. India and Japan replicate centralized tenders, channeling savings toward pediatric and geriatric cohorts needing flexible dosing. Programs especially benefit gestational diabetes cases requiring temporary therapy. Policy momentum through 2027 supports the Asia-Pacific insulin syringes market by cushioning out-of-pocket costs in low-income groups. Spillover to ASEAN through regional trade pacts amplifies volume upside.

Domestic Indian makers captured 25% of national insulin revenue by pushing affordable pens that grew 13% YoY in 2025, signaling permanent share shift away from syringes. Japanese endocrinologists now recommend pens as first-line due to dosing accuracy and lower social stigma, suppressing hospital reorder frequencies for 30G syringes. As GLP-1 injectables eclipse human insulin, pen-optimized cartridges gain regulatory and marketing support, further cannibalizing legacy volumes across urban APAC by late decade.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The 0.5 mL format held 45.67% of Asia-Pacific insulin syringes market share in 2025, reflecting versatility for adult basal-bolus regimens. Asia-Pacific insulin syringes market size for 0.5 mL units is projected to edge from USD 484 million in 2026 to USD 491 million by 2031, growing 0.28% annually. Meanwhile 0.3 mL demand grows 1.22% CAGR, underpinned by gestational and pediatric dosing needs.

Manufacturers invest in tighter tolerance molding and siliconized stoppers to maintain +-1 IU accuracy at lower volumes, a critical requirement for neonatal clinics in India and Thailand. Educational outreach via maternity hospitals normalizes smaller barrels, supporting penetration even in cost-sensitive provinces. Although 1 mL syringes remain necessary for insulin-resistant Type 2 cases, their share plateaus amid pen substitution. Specialty "others" formats serve diluted insulin research and retain niche relevance.

The 30G segment commanded 38.35% market share in 2025 and contributes USD 407 million to Asia-Pacific insulin syringes market size, yet 31G & above variants are forecast to climb 1.39% CAGR to 2031. Consumer surveys link thinner needles with 12% higher adherence at 12-month follow-up in Korea.

Investment in micro-taper grinding and electropolishing delivers 15% lower penetration force, matching pen-needle comfort benchmarks. Supply chains shift to higher gauge stainless wire, tightening demand for 28G-29G lines primarily used for viscous insulin analogs. As thinner gauges gain regulatory clearance for sub-cutaneous integrity, hospitals transition bulk contracts to reduce patient refusals and accelerate discharge throughput.

The Asia-Pacific Insulin Syringes Market Report is Segmented by Product Type (0. 3 ML, 0. 5 ML, 1 ML, and Others), Needle Gauge (28G, 29G, and More), Diabetes Type (Type 1, Type 2, and Gestational), End User (Hospitals & Clinics, Home Healthcare, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (China, India, and More). The Market Forecasts are Provided in Terms of Value (USD).