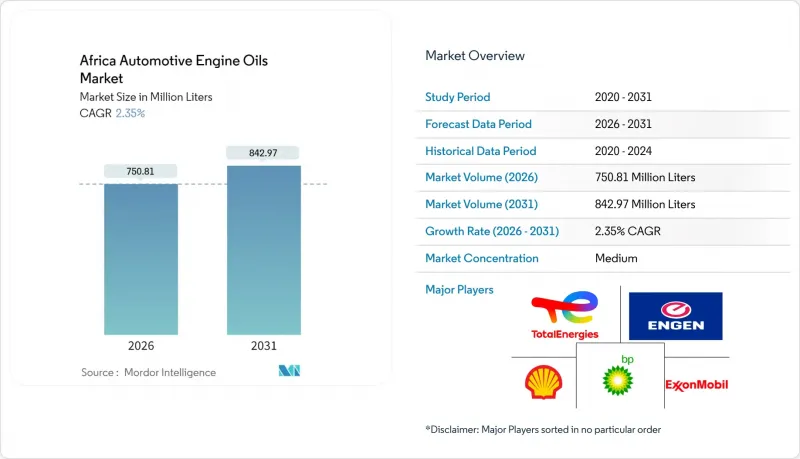

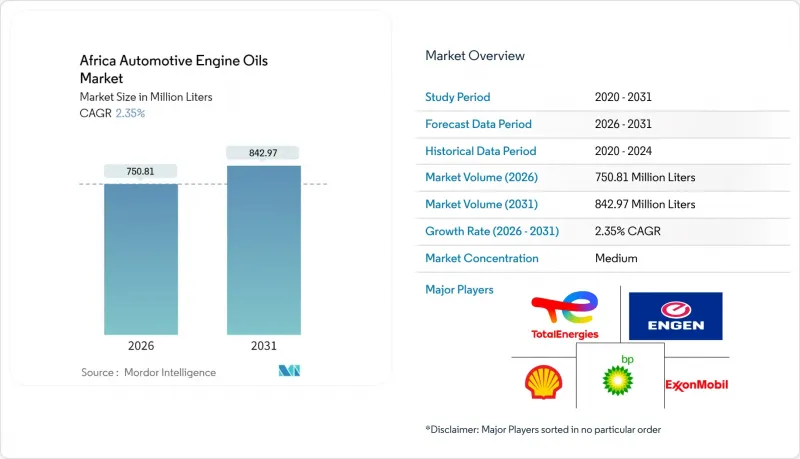

아프리카 자동차 엔진 오일 시장은 2025년에 7억 3,357만 리터로 평가되었으며, 2026년 7억 5,081만 리터에서 2031년까지 8억 4,297만 리터에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 2.35%로 예상됩니다.

시장 확대는 지속적인 차량 대수 증가, 산업화 발전, 제품 구성에서 단일 점도 광물성 오일에서 다점도 합성 오일로의 점진적인 전환에 의존하고 있습니다. 그러나 남아프리카공화국, 케냐, 나이지리아의 정유소 가동 중단이 지속되면서 현지 기유 공급이 타이트해져 수입 의존도가 높아지고 있습니다. 이로 인해 블렌더 업체들은 전 세계 트레이더들과 공급 계약을 재협상해야 하는 상황에 처해 있습니다. 위조품의 유통 경로가 계속적으로 정품 수요를 잠식하고 있어, 주요 브랜드는 시리얼화, 위조 방지 포장, 정비사 교육 시스템에 대한 투자를 해야 합니다. 종합적으로 볼 때, 시장의 안정적인 수요 기반, 확대되는 유통망, 연료 및 배출가스 기준 관련 규제의 정합성으로 인해 인프라 측면의 과제는 있지만 중기적 전망은 양호한 편입니다.

아프리카의 자동차 보급률은 인구 1,000명당 44대로 낮은 편이며, 차량 확대의 여지가 크다는 것을 보여줍니다. 모로코의 수출 지향적 생산 기지 외에도 가나와 르완다의 국내 조립이 증가하면서 공장 출고 및 애프터마켓용 오일 소비가 증가하고 있습니다. 케냐에서는 수입차량의 96%, 에티오피아와 나이지리아에서는 판매량의 80%가 중고차이며, 교체 주기가 짧은 재래식 오일에 대한 수요를 뒷받침하고 있습니다. 인구통계도 마찬가지로 결정적인 요소입니다. 아프리카 인구의 75%가 35세 미만으로 개인 이동수단에 대한 수요를 주도하고 있습니다. 예측 모델에 따르면, 대륙 전체의 차량 보유량은 20년 내에 4,500만 대 규모로 20년 내에 3 배 증가할 수 있으며, 이는 엔진 윤활유 제품에 대한 기준 수요를 직접적으로 증가시킬 수 있습니다.

휴대폰 보급률이 65%를 넘어서면서 5억 명 이상의 가입자에게 제품 정보를 전달할 수 있게 되었고, 운전자의 윤활유에 대한 지식이 향상되고 있습니다. 정비소에서는 소셜 미디어와 SMS 캠페인을 활용하여 오일 교환 알림 및 브랜드 홍보를 추진합니다. 이에 따라 소비자의 취향은 진품 여부를 확인할 수 있는 기능을 갖춘 고급 포장 제품으로 점차 옮겨가고 있습니다. 케냐의 윤활유 소비량 5만 3,500톤은 국내 수요의 87%가 상용차 및 자가용 차량용으로 사용되고 있는 현실을 보여줍니다. 소비자들이 적절한 오일 선택과 차량 총 운영비 절감을 연결시키기 시작하면서 브랜드 소유주들은 정비사들을 위한 로열티 프로그램을 개발했습니다. 교육, 판촉물, 소용량 패키지 인센티브를 결합하여 수익성이 높은 멀티 그레이드 오일로 교체하도록 장려하고 있습니다.

밀수품이나 가짜 윤활유는 품질 검사를 피하고 정품을 최대 40%까지 낮게 판매하여 정품을 판매하는 판매자의 수익률을 떨어뜨립니다. 나이지리아 윤활유 블렌더 협회에 따르면, 고황 위조 오일이 일반 시장과 공식 서비스 센터 모두에 유입되어 엔진의 조기 마모를 초래하고 브랜드 신뢰도를 떨어뜨리고 있습니다. 탄자니아 규제 당국은 2017년 소비된 3,700만 리터 중 3분의 1이 위조된 인증 스티커를 부착한 무허가 업자에 의한 것임을 밝혀냈습니다. 이러한 유출은 수요 예측을 왜곡하고, 재고 계획을 복잡하게 만들고, 브랜드 소유자가 대중 홍보 캠페인과 법적 집행 지원에 자금을 투입하도록 강요하는 결과를 초래했습니다.

승용차용 엔진오일(PCMO)은 2025년 기준 아프리카 자동차 엔진오일 시장에서 54.92%의 점유율을 유지했습니다. 이 부문은 5,000-8,000km의 비교적 짧은 교체 주기와 비공식 정비소에서 정비되는 차량을 포함한 광범위한 소비자층의 혜택을 누리고 있습니다. 반면, 대형차 엔진오일(HDMO)은 차체 1대당 사용량이 불균형적으로 많아(연결트럭의 경우 최대 40리터), 차량 대수가 적더라도 시장에 크게 기여하고 있습니다. 이륜차 엔진오일은 케냐, 우간다, 나이지리아의 이륜차 보급과 라스트 마일 배송 생태계를 배경으로 2.58%의 CAGR로 가장 높은 성장세를 보이고 있습니다. 점도 등급의 변화는 점진적인 현대화를 보여줍니다. 단일점도 SAE40의 점유율은 2026년까지 37%까지 하락할 것으로 예상되며, 승용차 및 상용차 모두에서 다점도 15W-40의 채택이 확대되고 있습니다. 프리미엄 OEM 인증 5W-30 합성유는 주요 대도시에서 공식 딜러가 보증을 준수할 수 있는 기반이 되는 프리미엄 OEM 인증 5W-30 합성유가 부상하고 있습니다. 자동차 엔진오일 시장 규모의 대부분은 PCMO(승용차), HDMO(상용차), 이륜차 엔진오일이 차지하고 있으며, 차종 구성과 정비 관행의 차이가 성장의 역동성을 반영하고 있습니다.

항만과 내륙 소비 거점을 연결하는 상업 운송 회랑에서는 2차적 영향이 두드러집니다. 과적 트럭, 분진 환경, 변동하는 연료 품질로 인해 윤활유에 대한 산화 스트레스가 증가함에 따라 차량 운영자는 CI-4 및 CK-4 카테고리에 공통적으로 적용되는 강력한 첨가제 패키지를 선호하는 경향이 있습니다. 이와 동시에 Bolt, Uber 등 차량 공유 서비스는 도시 지역의 고빈도 사용 주기를 증가시켜 엄격한 휘발성 및 퇴적물 제어 매개 변수를 충족하는 PCMO에 대한 수요를 증가시키고 있습니다. 정부의 차량 교체 계획이 현지 조립 버스를 우선시하는 가운데, 수요 탄력성은 대량 소비형 HDMO(중유)로 이동하고 있으며, 아프리카 자동차 엔진오일 시장에서 PCMO(경유)의 양적 우위에도 불구하고 HDMO의 전략적 중요성이 강화되고 있습니다. 교체 주기를 연장하는 합성유 블렌드는 필터 패키지 및 데이터 로깅 서비스 계약과 함께 번들로 판매되는 경우가 증가하여 라이프사이클 관리 제안의 기반을 마련하고 있습니다.

아프리카 자동차 엔진오일 시장 보고서는 수지 종류(승용차 엔진오일, 대형차 엔진오일, 이륜차 엔진오일), 기유(광유, 합성유, 반합성유, 바이오 기반 오일), 지역(남아프리카, 이집트, 나이지리아, 기타 아프리카 국가) 별로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 리터 단위로 제공됩니다.

The Africa Automotive Engine Oils Market was valued at 733.57 Million Liters in 2025 and estimated to grow from 750.81 Million Liters in 2026 to reach 842.97 Million Liters by 2031, at a CAGR of 2.35% during the forecast period (2026-2031).

Market expansion hinges on sustained fleet growth, progressive industrialization, and a gradual shift in product mix from monograde mineral oils to multigrade synthetic formulations. Ongoing refinery shutdowns in South Africa, Kenya, and Nigeria, however, have tightened local base-oil availability, prompting greater reliance on imports and pushing blenders to renegotiate supply contracts with global traders. Parallel counterfeit trade channels continue to erode legitimate demand, compelling leading brands to invest in serialization, tamper-evident packaging, and mechanic-level training schemes. On balance, the market's steady demand base, broadening distribution networks, and regulatory alignment on fuel and emissions standards create favorable medium-term prospects despite infrastructural headwinds.

Africa's low motorization rate of 44 vehicles per 1,000 inhabitants underscores substantial room for fleet enlargement. Morocco's export-oriented manufacturing hubs, together with rising domestic assembly in Ghana and Rwanda, accelerate vehicle additions that consume factory-fill and aftermarket oil volumes. Used-vehicle imports comprise 96% of Kenya's inflows and 80% of sales in Ethiopia and Nigeria, sustaining demand for conventional formulations that require shorter drain intervals. Demographic momentum is equally decisive; 75% of Africans are under 35, driving personal mobility aspirations. Projection models indicate that the continent's 45 million-unit fleet could triple within two decades, directly translating into increased baseline demand for engine lubrication products.

Mobile penetration above 65% enables the delivery of product information to more than 500 million subscribers, thereby elevating lubricant literacy among motorists. Workshops leverage social media and SMS campaigns to promote oil-change reminders and branded promotions, gradually shifting consumer preference toward premium packaging with verifiable authenticity features. Kenya's finished lubricant consumption of 53,500 metric tonnes illustrates how 87% of national demand is accumulated from commercial and private automotive applications. As consumers begin to equate proper oil selection with lower total vehicle operating costs, brand owners deploy mechanic loyalty programs that bundle training, point-of-sale materials, and small-pack incentives, stimulating trade-up to higher-margin multigrade oils.

Smuggled or adulterated lubricants evade quality inspection protocols and undercut branded pricing by as much as 40%, undermining the margins of legitimate distributors. Nigeria's association of lubricant blenders reports that high-sulfur counterfeit oils are infiltrating both open markets and formal service centers, inducing premature engine wear and eroding brand trust. Tanzania's regulator traced one-third of 37 million liters consumed in 2017 to unlicensed traders applying falsified certification stickers. Such leakage distorts demand estimates, complicates inventory planning, and forces brand owners to fund public-education campaigns and legal enforcement support.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Passenger car motor oil (PCMO) retained 54.92% of the Africa Automotive Engine Oils market share in 2025. The segment benefits from relatively short drain intervals of 5,000 - 8,000 km and a broad consumer base, with vehicles serviced through informal workshops. Heavy-duty motor oil (HDMO), however, accounts for a disproportionately higher volume per sump-up to 40 liters for articulated trucks-ensuring a material contribution even at lower vehicle counts. Motorcycle engine oil, albeit starting from a smaller base, displays the highest forward momentum with a 2.58% CAGR, propelled by two-wheeler proliferation in Kenya, Uganda, and Nigeria's last-mile delivery ecosystems. Viscosity-grade evolution illustrates gradual modernization: the share of monograde SAE 40 is sliding toward 37% by 2026, as multigrade 15W-40 gains traction in both passenger and commercial categories. Premium OEM-approved 5W-30 synthetics are emerging in Tier-1 metro areas where authorized dealerships anchor warranty compliance. Collectively, PCMO, HDMO, and motorcycle oils account for the bulk of Africa Automotive Engine Oils market size, with differentiated growth dynamics reflecting varied fleet compositions and service practices.

Second-order effects are pronounced in commercial haulage corridors that connect ports with inland consumption hubs. Overloaded trucks, dusty environments, and variable fuel quality heighten oxidative stress on lubricants, driving fleet operators to favor robust additive packages common in CI-4 and CK-4 categories. In parallel, ride-hailing services such as Bolt and Uber increase high-frequency urban use cycles, raising demand for PCMO meeting tight volatility and deposit-control parameters. As government fleet-renewal schemes prioritize locally assembled buses, demand elasticity shifts toward volume-draining HDMO, reinforcing its strategic relevance despite PCMO's numeric supremacy within Africa automotive engine oils market. Synthetic blends marketed under extended drain promises are increasingly bundled with filter packages and data-logging service contracts, setting the stage for life-cycle-management propositions.

The Africa Automotive Engine Oils Market Report is Segmented by Resin Type (Passenger Car Motor Oil, Heavy Duty Motor Oil, and Motorcycle Engine Oil), Base Stock (Mineral, Synthetic, Semi-Synthetic, and Bio-Based), and Geography (South Africa, Egypt, Nigeria, and Rest of Africa). The Market Forecasts are Provided in Terms of Volume (Liters).