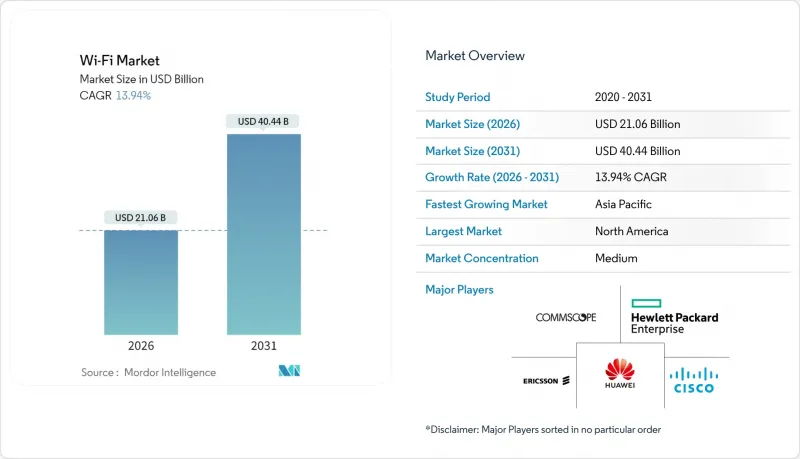

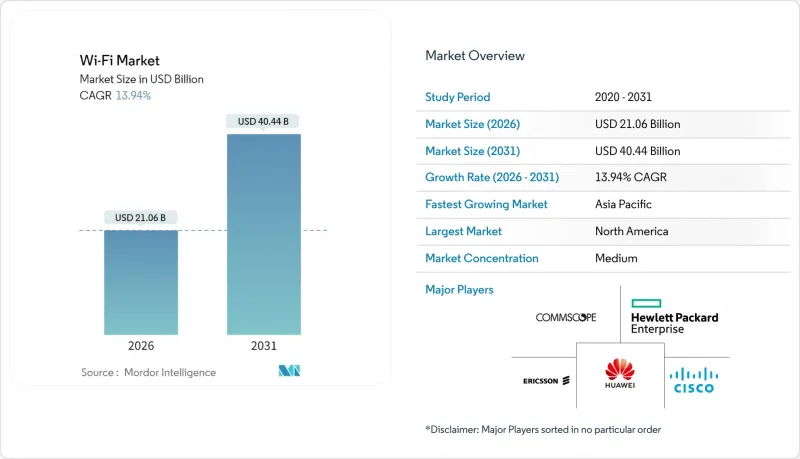

Wi-Fi 시장은 2025년에 184억 8,000만 달러로 평가되었으며, 2026년 210억 6,000만 달러에서 2031년까지 404억 4,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 13.94%로 예상됩니다.

이러한 가속화를 촉진하는 주요 요인은 기업에서 무선 우선 아키텍처에 대한 선호도 증가, Wi-Fi 7의 상용화, OpenRoaming 표준의 채택입니다. 기업들은 하이브리드 작업, 엣지 호스트형 인공지능, 실시간 산업 자동화에 있어 고용량 WLAN이 매우 중요하다는 것을 인식하고 있으며, 이를 통해 업데이트 주기를 8년에서 5년으로 단축하고 있습니다. 주거 환경과 소규모 사무실 환경에서의 메시 네트워크의 급속한 보급은 대상 시장을 더욱 확대시키고 있습니다. 한편, 북미 연방 정부의 광대역 프로그램은 공공 부문의 비즈니스 기회를 촉진하고 있습니다. 6GHz 대역의 주파수 할당은 일시적인 혼잡 완화를 가져오는 한편, 로봇 공학, 원격의료, 몰입형 현실 서비스를 위해 확정적인 지연을 보장할 수 있는 트라이밴드 액세스 포인트에 대한 수요를 불러일으키고 있습니다. 상호운용성 요구사항이 벤더 종속을 방지하고, 서비스 중심의 신규 진입자가 기존 하드웨어 벤더에 도전할 수 있기 때문에 경쟁 구도는 여전히 개방적입니다.

기업들은 고밀도 센서 네트워크를 구축하고 있으며, 액세스 포인트 당 100개 이상의 연결 엔드포인트가 있는 것이 일반적입니다. 이 프로파일은 Wi-Fi 6E의 OFDMA 스케줄링과 다중 사용자 MIMO 기능을 통해서만 경제적으로 서비스 제공이 가능합니다. 스마트 빌딩 운영자는 Wi-Fi 메시를 통해 HVAC, 조명, 모니터링 시스템을 통합하여 구조화 배선 비용을 40% 절감하고 예지보전 분석을 실현하고 있습니다. 엣지 추론 워크플로우에서 10밀리초 미만의 응답 시간에 대한 요구는 부하가 걸려도 지터 없는 트래픽을 유지하는 Wi-Fi 7의 멀티링크 운용을 매력적으로 만듭니다. 산업 자동화 시범 운영에서 전용 6GHz 채널에서 99.9%의 가동률을 달성한 반면, 혼잡한 5GHz 링크에서는 97.8%에 그쳐, 미션 크리티컬한 로봇 분야에서 새로운 스펙트럼 전환이 얼마나 효과적인지 입증했습니다. 이러한 성과로 인해 조직은 장기적인 생산성 향상에 대한 대가로 더 높은 초기 투자비용을 흡수하려는 의지가 높아졌습니다.

지방정부의 광대역 계획은 광대 한 농촌 지역에서 광섬유보다 설치가 빠르고 자본 집약도가 낮기 때문에 Wi-Fi를 디지털 포용의 주요 매체로 점점 더 중요시하고 있습니다. 필리핀은 2028년까지 17,000개의 바랑가이(행정구역)에 10만 개 이상의 공공 핫스팟을 구축하기 위해 12억 달러를 투자하고 있으며, 이 모델은 여러 신흥 경제국에서도 채택하고 있습니다. 유럽의 '디지털 디케이드'는 2030년까지 기가비트 네트워크 구축을 목표로 하고 있으며, Wi-Fi 7 메시를 산간지역과 섬 지역의 저비용 라스트 마일 대안으로 자리매김하고 있습니다. 도시 지역에서는 교통, 대기질, 비상 대응 시스템용 센서 백홀을 인프라에 겹겹이 쌓아 수익화를 꾀하고, 효율화를 통한 수익으로 자체 자금 조달을 실현하고 있습니다. 오픈 로밍 협정에 따라 와이파이와 5G 무선을 융합한 중립 호스트 구축은 로밍 요금으로 새로운 수익을 창출하는 동시에 원활한 시민 연결을 실현합니다.

맨해튼과 같은 고밀도 도시 지역에서는 Wi-Fi 6E 지원 장비가 도입되어 있어도 피크 시간대에는 처리량이 60% 가까이 감소합니다. 이는 2.4GHz 대역이 구식 디바이스에 의해 점유되고 있기 때문입니다. 전자렌지, 블루투스 단말기, 구형 라우터가 겹쳐서 노이즈를 발생시키며, 적응 알고리즘으로도 완전히 피할 수 없습니다. 기업들은 서비스 수준 목표를 달성하기 위해 5만-20만 달러에 달하는 스펙트럼 컨설턴트를 고용하여 서비스 수준 목표를 달성하기 위한 채널 계획을 설계하는 경우가 증가하고 있습니다. 규제 당국은 중요한 IoT 트래픽이 소비자의 간섭을 받지 않고 작동할 수 있도록 CBRS와 유사한 준면허제를 검토하고 있습니다. 6GHz 대역 할당으로 인해 일시적으로 압력이 완화되겠지만, IoT 엔드포인트가 기하급수적으로 증가함에 따라 5년 이내에 포화상태에 도달할 것으로 예상됩니다.

2025년 기준, 액세스 포인트는 Wi-Fi 시장 점유율의 35.92%를 차지하며, 수익 구조의 변화 속에서도 하드웨어의 중요성이 지속되고 있음을 보여줍니다. 한편, 서비스 부문은 2031년까지 CAGR 15.98%로 성장할 것으로 예상되며, 초기 투자를 지속적인 운영 비용으로 전환하는 '서비스로서의 네트워크(Network-as-a-Service)' 프레임워크로의 전환을 반영하고 있습니다. 비용 압박으로 인해 독립형 라우터와 레인지 익스텐더가 상품화되고, 기존 온프레미스 컨트롤러가 담당하던 정책 설정 및 분석 기능은 클라우드 네이티브 오케스트레이션 플랫폼이 대신하게 될 것입니다. 매니지드 서비스 제공업체는 인공지능을 활용하여 채널 할당, 부하 분산, 이상 감지 등을 자동화합니다. 이를 통해 고객이 직접 운영하는 네트워크와 비교하여 계획되지 않은 가동 중단 시간을 75% 절감할 수 있습니다. 2031년까지 성숙 경제권에서는 조직이 자산 소유보다 라이프사이클 유연성을 우선시하기 때문에 소프트웨어 및 서비스에서 발생하는 Wi-Fi 시장 규모가 하드웨어의 기여도를 능가할 것으로 예상됩니다.

이러한 변화는 소유권보다 성과를 중시하는 광범위한 IT 조달 트렌드를 반영하고 있습니다. 종량제를 통해 WLAN 비용은 가동률에 연동되어 예산의 급격한 증가를 억제하고 CFO의 가시성을 향상시킵니다. 벤더는 하드웨어 외의 차별화로 예방적 유지보수, 보안 컴플라이언스, 실시간 체험평가를 패키지로 제공합니다. 엣지 게이트웨이와 내환경형 IoT 브리지는 규모는 작지만 빠르게 성장하는 카테고리로, 진동, 먼지, 극한의 온도가 일반 장비를 무력화시키는 가혹한 산업 환경에서 안정적인 연결성을 제공합니다. AI 칩이 액세스 포인트에 내장되면 범용 하드웨어라도 복잡성을 추상화하고 생산성 달성까지의 시간을 단축하는 관리형 서비스로 제공되어 부가가치를 창출할 수 있습니다.

북미는 2025년 기준 와이파이 시장의 40.55%를 차지했습니다. 이는 650억 달러 규모의 브로드밴드 장려책과 기업의 빠른 리프레시 사이클에 기인합니다. 6GHz 대역에 대한 조기 접근을 통해 이 지역에서는 트라이밴드 구축의 선구자 역할을 하고 있으며, 규제 승인을 기다리는 지역과의 성능 차이를 만들어내고 있습니다. 포춘지 선정 500대 기업은 하이브리드 업무에 대응하는 스마트 오피스 구축을 위해 5년마다 WLAN을 업데이트하고 있으며, 이는 전 세계 평균보다 2년 빠른 속도입니다. 의료 및 교육 분야는 탄탄한 성장 거점이며, 원격의료 및 원격교육은 기업 수준의 신뢰성이 요구됩니다.

아시아태평양은 2031년까지 CAGR 15.12%로 가장 빠른 성장세를 기록할 것으로 예상되며, 이는 무선통신을 보완적 인프라가 아닌 주요 인프라로 인식하는 국가 디지털 전략이 뒷받침하고 있습니다. 중국의 공장 자동화 붐은 국내 칩셋 역량 육성 정책에 의해 증폭되어 산업용 Wi-Fi 6E 장비에 대한 대량 주문으로 이어지고 있습니다. 인도의 '디지털 인디아' 구상은 60만 개의 마을을 와이파이 메시로 연결하여 무선 기술을 농촌 포용의 핵심으로 삼고 있습니다. 동남아시아 국가들은 관광 거점이나 수출 지향형 산업단지에 WLAN을 통합하고, 정부 보조금으로 투자 회수 기간을 단축하여 도입을 가속화하고 있습니다. 자카르타, 방콕, 호치민시의 스마트 시티 펀딩 라운드가 지역 수요를 더욱 증가시키고 있습니다.

유럽의 성장은 질서를 유지하고 있으며, 인더스트리 4.0의 도입과 디지털 디케이드 지침에 따라 2030년까지 가정용 기가비트 연결이 의무화되어 있습니다. 알프스나 그리스 섬과 같은 험준한 지형에서는 Wi-Fi가 비용 효율적인 라스트 마일 솔루션으로 작용할 수 있습니다. EU 디지털 단일 시장이 주도하는 오픈 로밍 협정은 국경을 초월한 원활한 연결을 실현하여 관광 및 원격지 출장을 촉진하고 있습니다. 독일은 산업 분야에서 도입을 주도하고 있으며, 북유럽 국가들은 에너지 효율적인 TWT 스케줄링에 의존하는 스마트 그리드 및 지속가능성 사용 사례에 초점을 맞추고 있습니다. 중동 및 아프리카에서는 경제를 탄화수소에 의존하지 않는 다변화를 꾀하고, 사막과 산악지대 농촌 지역의 디지털 격차를 해소하기 위해 와이파이에 대한 투자가 진행되고 있습니다.

The Wi-Fi Market was valued at USD 18.48 billion in 2025 and estimated to grow from USD 21.06 billion in 2026 to reach USD 40.44 billion by 2031, at a CAGR of 13.94% during the forecast period (2026-2031).

Growing enterprise preference for wireless-first architecture, the commercial debut of Wi-Fi 7, and the adoption of OpenRoaming standards are the primary forces propelling this acceleration . Enterprises view high-capacity WLAN as pivotal for hybrid work enablement, edge-hosted artificial intelligence, and real-time industrial automation, prompting refresh cycles that shorten from eight years to five. Rapid mesh penetration in residential and small-office environments further broadens the addressable base, while federal broadband programs in North America stimulate public-sector opportunities. Spectrum allocations in the 6 GHz band supply temporary congestion relief, yet also spark demand for tri-band access points that can assure deterministic latency for robotics, telemedicine, and immersive reality services. The competitive landscape remains open because interoperability requirements prevent lock-in, allowing new service-centric entrants to challenge incumbent hardware vendors.

Enterprises deploy dense sensor networks that often exceed 100 connected endpoints per access point, a profile economically serviced only by Wi-Fi 6E's OFDMA scheduling and multi-user MIMO capabilities. Smart-building operators integrate HVAC, lighting, and surveillance over Wi-Fi mesh to cut structured-cabling costs by 40% and enable predictive maintenance analytics. Demand for sub-10 ms response in edge inference workflows makes Wi-Fi 7's multi-link operation attractive because it sustains jitter-free traffic under load. Industrial automation pilots report 99.9% uptime on dedicated 6 GHz channels versus 97.8% on congested 5 GHz links, validating the migration to new spectrum for mission-critical robotics. These gains encourage organizations to absorb higher capital outlays in return for long-run productivity .

Municipal broadband programs increasingly favor Wi-Fi as the primary medium for digital inclusion because installation is quicker and less capital-intensive than fiber in sprawling rural territories. The Philippines commits USD 1.2 billion to deploy more than 100,000 public hotspots across 17,000 barangays by 2028, a template mirrored by several emerging economies. Europe's Digital Decade targets gigabit coverage by 2030 and positions Wi-Fi 7 mesh as an affordable last-mile alternative in mountainous and island regions. Cities monetize infrastructure by layering sensor backhaul for traffic, air-quality, and emergency-response schemes that self-fund through efficiency gains. Neutral-host deployments that blend Wi-Fi and 5G radios under OpenRoaming agreements generate fresh revenue as roaming fees while delivering seamless citizen connectivity.

Dense urban precincts such as Manhattan experience throughput drops near 60% during peak usage, even when Wi-Fi 6E hardware is present, because legacy devices crowd the 2.4 GHz spectrum. Microwave ovens, Bluetooth handsets, and older routers create overlapping noise that adaptive algorithms cannot fully evade. Enterprises increasingly hire spectrum consultants, a service costing USD 50,000-200,000 on expansive campuses, to engineer channel plans that meet service-level objectives. Regulators consider quasi-licensed regimes akin to CBRS so that critical IoT traffic can operate free of consumer interference. Although the 6 GHz allocation temporarily alleviates pressure, forecasts show saturation within five years as IoT endpoints grow exponentially.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2025, access points contributed 35.92% to the Wi-Fi market share, underlining hardware's continuing relevance even as revenue mix shifts. The services segment, however, is projected to compound at 15.98% through 2031, reflecting the pivot to Network-as-a-Service frameworks that convert upfront capital into recurring operating expense. Cost pressures commoditize standalone routers and range extenders, while cloud-native orchestration platforms take over the policy and analytics roles previously executed by on-premises controllers. Managed service providers leverage artificial intelligence to automate channel allocation, load balancing, and anomaly detection, ultimately delivering 75% fewer unplanned-outage minutes than customer-operated networks. By 2031, the Wi-Fi market size attributed to software and services is expected to eclipse hardware contribution in mature economies as organizations prioritize life-cycle flexibility over asset ownership.

The shift mirrors broader IT procurement trends that favor outcomes over ownership. Consumption-based pricing aligns WLAN costs with occupancy levels, flattening budget spikes and improving CFO visibility. Vendors bundle proactive maintenance, security compliance, and real-time experience scoring to differentiate beyond hardware. Edge gateways and ruggedized IoT bridges constitute a small but fast-rising category, supplying deterministic connectivity in harsh industrial zones where vibration, dust, and temperature extremes invalidate consumer-grade gear. As AI chips embed inside access points, even commodity hardware gains value when offered as a managed experience that abstracts complexity and accelerates time to productivity.

The Wi-Fi Market Report is Segmented by Component (Hardware, Solutions, Services), End-User Vertical (Consumer, Enterprise/Corporate Campuses, Education, Healthcare, Hospitality and Retail, Industrial and Logistics), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America accounts for 40.55% of the Wi-Fi market in 2025, owing to USD 65 billion in broadband incentives and rapid enterprise refresh cycles. Early access to 6 GHz spectrum allows institutions to pioneer tri-band deployments, creating a performance gap over regions still seeking regulatory clearance. Fortune 500 companies refresh their WLAN every five years, two years faster than the global average, to equip smart offices tailored for hybrid work. Healthcare and education pillars represent robust growth nodes as telehealth and distance learning require enterprise-grade reliability.

Asia Pacific records the fastest trajectory with a 15.12% CAGR through 2031, enabled by national digital strategies that treat wireless as primary rather than complementary infrastructure. China's factory-automation boom, amplified by policy to cultivate domestic chipset capability, translates to bulk orders for industrial-grade Wi-Fi 6E equipment. India's Digital India mission envisions connecting 600,000 villages via Wi-Fi mesh, making wireless the linchpin of rural inclusion. Southeast Asian economies integrate WLAN across tourism hubs and export-oriented manufacturing parks, while government subsidies shrink payback periods and accelerate deployments. Smart-city funding rounds across Jakarta, Bangkok, and Ho Chi Minh City further elevate regional demand.

Europe's growth remains orderly as Industry 4.0 uptake and Digital Decade mandates require gigabit household coverage by 2030. Wi-Fi serves as the cost-effective last-mile solution in rugged topographies like the Alps and the Greek islands. OpenRoaming agreements spearheaded by the EU Digital Single Market create frictionless cross-border connectivity, bolstering tourism and remote business travel. Germany leads industrial adoption, whereas Nordic nations focus on smart-grid and sustainability use cases that rely on energy-efficient TWT scheduling. The Middle East and Africa invest in Wi-Fi to diversify economies beyond hydrocarbons and to bridge digital divides in rural deserts and mountainous terrain.