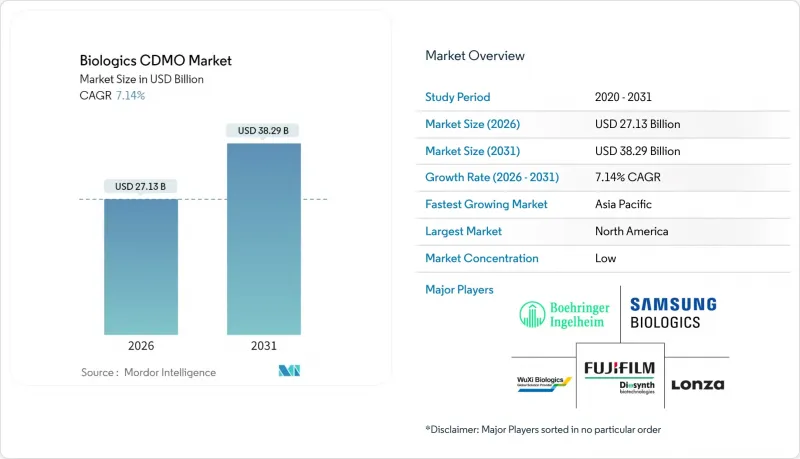

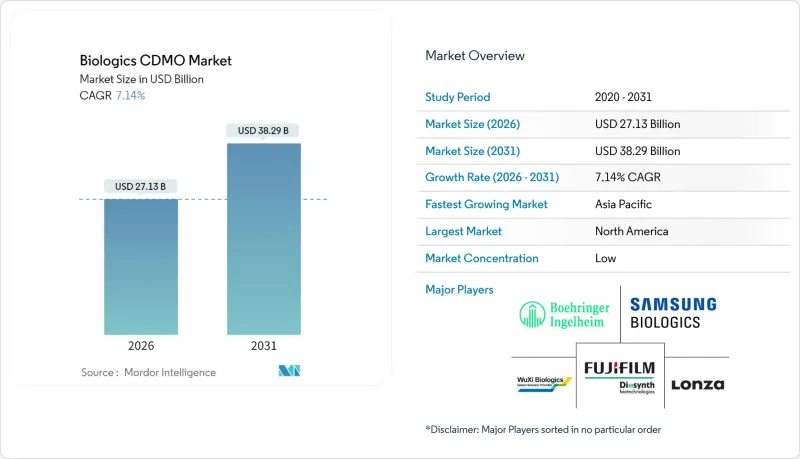

바이오로직스 CDMO 시장은 2025년에 253억 2,000만 달러로 평가되었으며, 2026년 271억 3,000만 달러에서 2031년까지 382억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 7.14%로 예상됩니다.

외주 용량에 대한 견고한 수요, 차세대 치료제의 복잡성, 자체 시설에 대한 자본 요구 사항의 증가는 스폰서 기업을 전문 파트너로 계속 이끌고 있습니다. 연속 제조 기술 및 일회용 기술 도입으로 업무의 민첩성을 높이는 한편, 풀 서비스 제공업체는 분석, 규제 대응, 충전 및 마무리 공정의 서비스 확대로 바이오의약품 CDMO 시장 점유율을 확대하고 있습니다. 삼성바이오로직스의 2024년 362,000L 규모의 바이오리액터 완전 가동 달성, 론자의 12억 달러 규모의 제넨텍 바카빌 공장 인수 등 증설 움직임은 전 세계 생산능력 부족과 경쟁 심화를 보여주고 있습니다. 지역적 트렌드도 성장에 새로운 층을 더하고 있습니다. 수익 측면에서는 북미가 선두를 달리고 있지만, 중국, 한국, 인도의 제조 촉진 정책 인센티브로 인해 아시아태평양이 가장 빠른 성장세를 보이고 있습니다.

평균수명 연장에 따라 암, 자가면역질환, 대사성 질환의 발병률이 급격히 증가하고 있으며, 이는 첨단 바이오의약품의 장기적인 수요를 견인하고 있습니다. 60세 이상 인구는 2050년까지 21억 명으로 두 배로 증가하여 의료 시스템에 지속적인 압력을 가하는 동시에 치료법 혁신을 가속화하는 요인이 될 것입니다. Novo Nordisk의 41억 달러 규모의 미국 충전 및 마무리 프로젝트는 고령층에 대한 고용량 주사제의 안정적인 공급을 보장하기 위한 스폰서의 움직임을 잘 보여주고 있습니다. CDMO 제휴를 통해 혁신기업은 시장 출시 일정을 단축하고 자본 리스크를 줄일 수 있어 바이오의약품 CDMO 시장의 꾸준한 성장을 강화할 수 있습니다.

최첨단 항체약물접합체(ADC) 및 다중 특이적 항체 생산 공장은 10억 달러 이상의 비용이 소요됩니다. 이러한 지출은 스폰서의 재정 상태를 압박하고 대규모 GMP 준수 제조 능력을 제공하는 파트너에게 제조 위험을 이전하는 움직임을 촉진하고 있습니다. 삼성바이오로직스는 고객의 설비투자가 필요 없는 턴키 방식의 역량을 제공함으로써 상위 20개 제약사 중 16개사와 총 130억 달러 규모의 장기 생산 계약을 체결한 바 있습니다. 특히 일회용 장비를 중심으로 계속되는 원자재 비용의 인플레이션은 경제적 합리성을 더욱 아웃소싱으로 기울이고 있습니다.

FDA의 배치 균일성에 대한 새로운 지침과 EU의 개정된 규정으로 인해 밸리데이션 및 문서화 작업량이 증가하고 있습니다. 이에 따라 CDMO 기업들은 기존 대형 제약사보다 훨씬 높은 수준인 매출의 12-15%를 품질 보증에 투자해야 하는 상황이 발생했습니다. 바이오시밀러의 비교가능성에 대한 감시 강화는 프로젝트 기간을 연장시키고 바이오의약품 CDMO 시장의 단기적 모멘텀을 둔화시킬 수 있습니다.

2025년 충전 및 포장 서비스는 생물학적 제제 CDMO 시장의 34.96%를 차지했으며, 최종 제품 제조에 있어 무균 및 규제적 중요성이 부각될 것으로 보입니다. 론자의 5억 스위스프랑 규모의 신규 시설 등 대규모 투자가 성장을 견인하고 있습니다. 동시에 엄격한 출하 테스트에 대한 수요가 증가함에 따라 분석 및 품질 관리(QC) 서비스 채택이 가속화되고 있으며, 2031년까지 CAGR 12.24%로 확대될 것으로 예상됩니다.

통합형 개발 기업은 프로세스 개발, GMP 생산, 분석, 규제 대응 지원을 포괄적으로 제공하여 업무 인수인계를 최소화하는 추세가 강화되고 있습니다. Eurofin Biopharma의 45개 GMP 실험실 네트워크는 지리적으로 분산된 종합적인 시험을 통해 출시 주기를 단축하는 추세를 구현하고 있습니다. 이 통합 모델은 더욱 견고한 관계를 구축하여 공급업체에게 바이오의약품 CDMO 시장에서 점유율을 확대할 수 있는 기회를 제공합니다.

포유류 플랫폼은 2025년 생물학적 제제 CDMO 시장 규모의 61.68%를 차지했으며, 이는 단클론항체 및 기타 당쇄 의존성 의약품에 대한 수요를 반영합니다. 삼성의 78만 4,000리터로의 스케일업은 고부가 CHO 생산에 대한 지속적인 투자를 뒷받침하고 있습니다.

미생물 시스템은 간소화된 공정 라인과 비용 우위로 인해 8.22%의 CAGR로 성장하고 있습니다. 써모피셔의 일회용 발효기는 오염 위험을 줄이고 회전율을 단축하여 미생물 시스템의 적용 범위를 펩타이드 및 올리고뉴클레오티드 치료제까지 확장하고 있습니다. 이러한 유연성은 경제적인 초기 단계 생산을 원하는 신흥 스폰서들의 관심을 끌고 있습니다.

북미는 첨단 제조 기술에 대한 밀도 높은 혁신 생태계와 규제적 지원에 힘입어 2025년 매출의 34.12%를 차지하며 선두를 유지할 것으로 예상됩니다. FDA의 연속 처리 및 신속한 심사 절차에 대한 지침은 조기 도입을 촉진하고 현지 CDMO에 혜택을 가져다주었습니다. 노보노디스크가 41억 달러를 투자한 노스캐롤라이나주 공장 등 대규모 투자가 이 지역의 설비 기반을 강화하고 있습니다.

유럽은 독일, 영국, 스위스가 주도하는 정교한 프레임워크를 제공하고 있습니다. 론자가 5억 스위스 프랑을 투자한 슈타인에 위치한 충전 및 마감 허브는 이 대륙의 전문적이고 고수익에 초점을 맞춘 노력의 좋은 예입니다. EMA의 생물학적 제제 가이드라인 업데이트는 기술 이전을 간소화하여 국내 및 대서양 횡단 업무 모두 안정적으로 유입되고 있습니다. 바이오신세스의 독일 내 생체 결합 확장 등 새로운 프로젝트는 틈새 전문 지식에 대한 지속적인 수요를 강조하고 있습니다.

아시아태평양은 적극적인 생산능력 증설과 공공부문의 인센티브에 힘입어 2031년까지 10.48%의 CAGR을 기록할 것으로 예상됩니다. 삼성바이오로직스의 78만 4,000리터 증설, SK바이오팜의 2억 6,000만 달러를 투자한 세종 프로젝트는 한국이 바이오로직스 세계 강국으로 도약하기 위한 전략을 상징합니다. 중국의 NMPA 승인 절차 간소화, 인도의 인프라 보조금도 스폰서 프로젝트를 이 지역으로 유도하는 데 중요한 역할을 하고 있습니다.

The biologics CDMO market was valued at USD 25.32 billion in 2025 and estimated to grow from USD 27.13 billion in 2026 to reach USD 38.29 billion by 2031, at a CAGR of 7.14% during the forecast period (2026-2031).

Robust demand for outsourced capacity, rising complexity of next-generation therapeutics, and mounting capital requirements for in-house facilities continue to steer sponsors toward specialized partners. Uptake of continuous manufacturing and single-use technologies is lifting operational agility, while full-service providers are broadening analytical, regulatory, and fill-finish offerings to capture a larger share of the biologics CDMO market. Expansionary moves-such as Samsung Biologics' 2024 achievement of full utilization across 362,000 L of bioreactors and Lonza's USD 1.2 billion acquisition of Genentech's Vacaville plant-signal tightening global capacity and intensifying competition. Regional dynamics add another growth layer: North America leads on revenue, but Asia-Pacific is posting the fastest gains thanks to pro-manufacturing policy incentives in China, South Korea, and India.

Rising life expectancy is sharply increasing the prevalence of oncology, autoimmune, and metabolic disorders, driving long-run demand for advanced biologics. The global population aged 60+ will double to 2.1 billion by 2050, putting consistent pressure on healthcare systems and triggering accelerated therapeutic innovation. Novo Nordisk's USD 4.1 billion US fill-finish project highlights sponsor moves to ensure secure supply for high-volume injectables that serve older cohorts. CDMO alliances allow innovators to compress launch timelines and mitigate capital exposure, reinforcing steady growth of the biologics CDMO market.

State-of-the-art antibody-drug conjugate or multispecific antibody plants can cost in excess of USD 1 billion. Such outlays strain sponsor balance sheets, encouraging transfer of manufacturing risk to partners offering GMP-compliant capacity at scale. Samsung Biologics secured USD 13 billion in long-term production contracts with 16 of the top 20 pharma firms by providing turnkey capability without client capex. Ongoing material cost inflation, especially for single-use equipment, further tilts economic logic toward outsourcing.

New FDA guidance on batch uniformity and updated EU legislation are escalating validation and documentation workloads, requiring CDMOs to devote 12-15% of revenue to quality assurance, well above traditional pharma norms. Heightened scrutiny around biosimilar comparability can prolong project timelines, tempering near-term momentum of the biologics CDMO market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fill-finish and packaging services captured 34.96% biologics CDMO market share in 2025, underlining the sterility and regulatory stakes of final drug-product preparation. Growth is reinforced by big-ticket investments such as Lonza's CHF 500 million Swiss facility. Parallel demand for robust release testing is accelerating analytical and QC uptake, which is projected to post a 12.24% CAGR through 2031.

Integrated developers increasingly bundle process development, GMP production, analytical, and regulatory support to minimize hand-offs. Eurofins BioPharma's network of 45 GMP labs exemplifies the trend toward geographically diversified, full-scope testing that shortens release cycles. This integrative model embeds stickier relationships and positions suppliers to harvest incremental share of the biologics CDMO market.

Mammalian platforms generated 61.68% of biologics CDMO market size in 2025, reflecting their necessity for monoclonal antibodies and other glycosylation-dependent drugs. Samsung's scale-up to 784,000 L underscores continued investment in high-titer CHO production.

Microbial systems are advancing on an 8.22% CAGR tailwind owing to simplified process trains and cost advantages. Thermo Fisher's single-use fermentors reduce contamination risk and shorten turnovers, broadening microbial applicability to peptide and oligonucleotide therapeutics. The resulting flexibility attracts emerging sponsors seeking economical early-stage production.

The Biologics CDMO Market Report is Segmented by Service Type (Process Development, GMP Manufacturing, and More), Type (Mammalian, Microbial), Product Type (Biologics [Monoclonal Antibodies, Recombinant Proteins, and More], Biosimilars), Scale (Pre-Clinical and Clinical, Commercial), End-User (Small/Mid-size Biotech, Large Pharma), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained leadership with 34.12% of 2025 revenue, propelled by dense innovation ecosystems and regulatory support for advanced manufacturing. FDA guidance on continuous processing and expedited review pathways fosters early adoption curves that benefit local CDMOs. Large-scale investments such as Novo Nordisk's USD 4.1 billion North Carolina plant reinforce the region's installed base.

Europe offers a sophisticated framework dominated by Germany, the United Kingdom, and Switzerland. Lonza's CHF 500 million fill-finish hub in Stein exemplifies the continent's specialized, high-margin focus. Updated EMA biologics guidelines simplify technology transfers and sustain steady inflows of both domestic and trans-Atlantic work. Emerging projects such as Biosynth's German bioconjugation expansion underscore persistent demand for niche expertise.

Asia-Pacific is the growth engine, set to post a 10.48% CAGR through 2031 on the back of aggressive capacity builds and public-sector incentives. Samsung Biologics' expansion to 784,000 L and SK pharmteco's USD 260 million Sejong project typify South Korea's strategy to become a global biologics powerhouse. China's streamlined NMPA approval procedures and India's infrastructure grants are equally pivotal in channeling sponsor projects into the region.