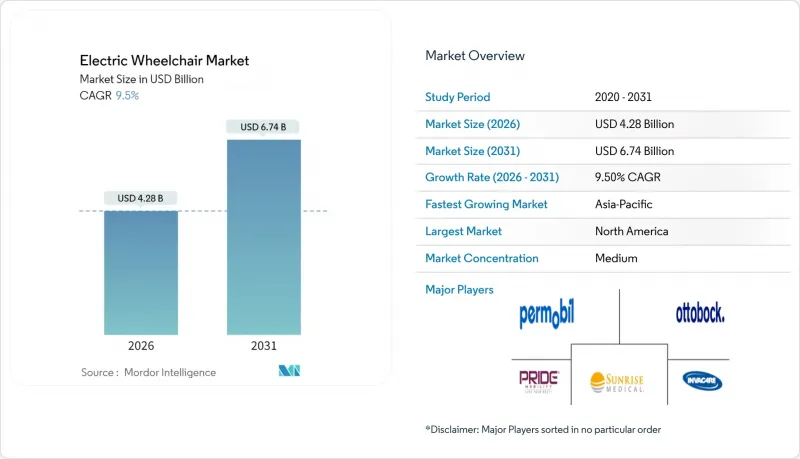

2026년 전동 휠체어 시장 규모는 42억 8,000만 달러로 추정되며, 2025년 39억 1,000만 달러에서 성장이 전망됩니다.

2031년까지 67억 4,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 9.5%로 확대될 것으로 전망됩니다.

이러한 견고한 성장 궤적은 이동 지원의 패러다임을 재구성하는 인구통계학적 요구와 기술적 혁신의 융합을 반영하고 있습니다. 유엔(UN)은 세계 인구가 2080년대 중반에 103억 명으로 정점에 도달할 것으로 예측하고 있으며, 중국과 일본을 포함한 63개국에서는 이미 인구 감소가 시작되어 고도화된 이동성 솔루션에 대한 지속적인 수요를 견인하는 전례 없는 고령화 인구 구조를 만들어내고 있습니다.

유엔의 추산에 따르면 2050년까지 65세 이상 인구가 급격히 증가하여 이동 보조기구에 대한 수요가 급증할 것으로 예상됩니다. 척수 손상, 뇌졸중, 골관절염의 증가로 인해 전 세계적으로 필요한 휠체어 수는 이미 6,500만 대를 넘어섰으며, 향후 10년간 22% 증가할 것으로 예측됩니다. 성숙한 경제 국가에서는 노동력 부족이 간병 자원을 압박하는 병행 압력에 직면하고 있으며, 독립적인 생활을 위해 전동 이동 수단이 필수적입니다. 신흥시장도 비슷한 인구통계학적 변화에 직면하고 있지만, 의료보험 적용 범위가 좁기 때문에 저렴한 수입품에 대한 관심이 높아지고 있습니다. 이러한 요인들이 복합적으로 작용하여 전동 휠체어 시장은 지역 간 견조한 성장세를 유지하고 있습니다.

아르곤 국립 연구소의 추정에 따르면, 2023년 리튬이온 배터리 팩의 평균 비용은 140달러/kWh이며, 2035년까지 86달러/kWh로 하락할 것으로 예상됩니다. 재생에너지 정책의 추진으로 이보다 더 빠른 가격 하락도 예상됩니다. 화학제품 비용의 감소로 OEM 제조업체는 더 큰 용량의 배터리를 탑재할 수 있게 되어 항속거리 연장 및 충전 불안감을 줄일 수 있습니다. 전기자동차 공급망이 가져오는 규모의 경제 효과는 의료기기 분야에도 파급되어 셀, BMS(배터리 관리 시스템), 충전기 단가를 낮추게 됩니다. 자동차를 위해 개발된 첨단 열관리 모듈이 고급 휠체어에 채택되어 안전성과 수명주기가 향상되고 있습니다. 이러한 요인들이 결합되어 평생 운영 비용이 절감되고 전동 휠체어 시장의 잠재적 수요가 확대되고 있습니다.

8,000-3만 달러의 최고급 모델은 보험 적용 범위가 제한적인 사용자들에게는 여전히 부담스러운 가격대입니다. 복잡한 전자장치, 서보 모터, 커스텀 시트로 인해 연간 유지보수 비용은 초기 비용의 15-20%까지 늘어납니다. 메디케어 승인을 위해서는 의사의 상세한 서류작성이 필요한 경우가 많고, 자금 조달이 지연되기 때문에 자금난에 시달리는 구매자는 업그레이드를 미룰 수 밖에 없습니다. 지방에는 공인된 기술자가 부족하고, 소유자는 수리를 위해 장거리 운송을 해야 합니다. 이러한 장벽은 전동 휠체어 시장의 잠재력을 충분히 발휘하지 못하게 하는 요인으로 작용하고 있습니다.

전동 휠체어 시장에서 후륜구동 부문은 2025년 전체 시장의 47.02%를 차지하며 2031년까지 CAGR 10.05%로 가장 빠르게 성장하는 부문으로 부상할 것으로 예상됩니다. 후륜구동 시스템은 뛰어난 실외 성능과 험로에서의 안정성으로 인해 주류가 되었습니다. 한편, 센터 구동방식은 주거용에 필수적인 작은 회전 성능으로 실내 이동에 대한 요구를 충족시켜 줍니다.

전륜구동 모델은 특히 작업치료 및 재활 환경에서 전방 시야를 극대화하고 장애물 회피가 필요한 사용자를 위한 특수한 틈새시장을 차지하고 있습니다. 전륜구동 및 하이브리드 구동 시스템은 다양한 환경에서 성능을 최적화하기 위해 여러 추진 방식을 결합한 새로운 카테고리이지만, 복잡성과 비용 측면에서 채택이 제한적입니다. 기본적인 이동 보조를 넘어 레크리에이션 활동과 사회적 교류에 참여할 수 있는 기기를 원하는 사용자가 증가함에 따라, 구동 방식 선택은 의료적 요구 사항보다 라이프스타일 선호도를 반영하는 경향이 강해지고 있습니다.

2025년 기준 병원이 시장 점유율의 60.85%를 차지하고 있습니다. 그러나 개인용 부문은 2031년까지 CAGR 9.55%로 가장 빠르게 성장하고 있으며, 전통적인 의료 용도를 넘어서는 확장성을 보이고 있습니다. 이러한 다양화로 인해 제조업체는 의료기기 규제와 활동적인 사용 환경에서의 성능 요구 사항의 균형을 맞추는 제품 개발이 과제로 대두되고 있습니다.

병원이나 진료소에서는 다중 사용자 대응 및 고빈도 사용을 견딜 수 있는 업무용 장비에 대한 수요가 꾸준히 증가하고 있습니다. 한편, 재활시설에서는 치료 단계에 따라 설정 변경이 가능한 고도화된 모델을 지정하는 경우가 증가하고 있습니다. 장기요양시설은 안정적이고 성숙한 시장이며, 구매 결정은 첨단 기능보다는 내구성과 유지보수성을 중시합니다. 스포츠 및 어드벤처 용도의 증가는 견고한 부품과 고성능을 겸비한 전문 제품 라인의 기회를 창출하고, 프리미엄 가격 책정 가능성과 함께 기존 의료 채널을 넘어 시장을 확대할 수 있는 기회를 제공합니다.

북미는 38.55%의 시장 점유율로 가장 큰 수익 기반을 차지하고 있으며, 이는 성숙한 의료 인프라와 종합적인 상환 제도를 반영하고 있습니다. 그러나 주요 인구통계학적 부문의 시장 침투율이 포화상태에 가까워짐에 따라 성장이 둔화되고 있습니다. 이 지역은 잘 구축된 유통망과 FDA 의료기기 승인 경로를 통한 규제 명확성의 혜택을 누리고 있으며, 기술 혁신을 빠르게 도입할 수 있는 여건이 조성되어 있습니다. 메디케어의 적용 가이드라인은 복잡하지만, 예측 가능한 자금 조달 메커니즘을 제공하여 대상 사용자의 고가 기기 도입을 지원하고 있습니다.

아시아태평양은 예측 기간 동안 11.62%의 CAGR로 가장 빠르게 성장하여 2026년부터 2031년까지 전동 휠체어 시장 규모에 11억 달러의 증가를 가져올 것입니다. 중국 지방도시 확대 전략으로 현지 대리점이 대상 인구로부터 150km 이내 거리에 보증 서비스 거점을 설치하여 두 자릿수 물량 성장을 실현하고 있습니다. 일본의 급속한 고령화 사회에서는 홈 오토메이션 시스템과 통합된 고급 스마트 휠체어가 선호되고 있으며, 이 부문은 연간 15%의 성장률을 보이고 있습니다. 호주와 한국에서는 구매 비용을 최대 4,000달러까지 보조하는 정부 지원 바우처 제도가 도입되어 중저가형 리튬이온 모델에 대한 수요를 촉진하고 있습니다. 그러나 규제 체계의 분절화와 변동하는 상품 및 서비스세(GST) 세율로 인해 성공적인 시장 진입을 위해서는 적응형 가격 책정 및 인증 전략이 필요합니다. 유럽은 기술적으로 정교한 소비자 기반을 유지하고 있습니다. EU 배터리 규정 2023/1542는 배터리 구동 장비의 지속가능성 요구사항에 대한 세계 선례를 확립하고, 환경 규정 준수 역량을 갖춘 제조업체에게 경쟁 우위를 제공합니다. 독일과 스페인에서는 도시 지역의 종량제 플랫폼이 널리 보급되어 있으며, 일반 사용자들은 소유의 부담 없이 프리미엄 기기를 이용할 수 있습니다. 동유럽에서는 EU의 결속기금으로 재활병원과 노인요양센터가 현대화되어 그 수가 증가하고 있습니다. 중동 및 아프리카는 현재 전 세계 가치의 5% 미만을 차지하고 있습니다. 그럼에도 불구하고, 걸프협력회의 회원국들은 공공부문 병원 확장 및 주요 스포츠 이벤트에 앞서 종합적인 도시 계획으로 인해 조달이 가속화되고 있습니다. 남아프리카공화국에서는 장애인 수당 인상으로 가구의 구매력이 향상되고 있지만, 애프터서비스 물류는 여전히 병목현상이 발생하고 있습니다. 이러한 추세를 종합하면 전동 휠체어 시장에서 마케팅 믹스의 중요한 결정 요인으로 지리적 세분화가 부각되고 있습니다.

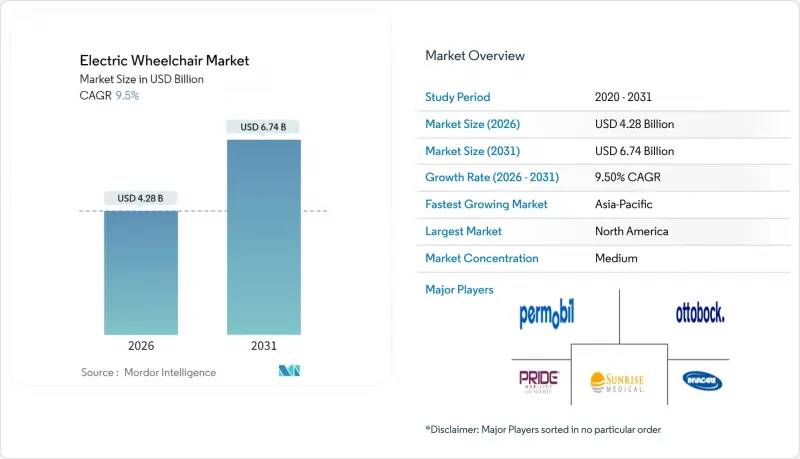

Electric wheelchair market size in 2026 is estimated at USD 4.28 billion, growing from 2025 value of USD 3.91 billion with 2031 projections showing USD 6.74 billion, growing at 9.5% CAGR over 2026-2031.

This robust growth trajectory reflects the convergence of demographic imperatives and technological breakthroughs reshaping mobility assistance paradigms. The United Nations (UN) projects the global population will peak at 10.3 billion by the mid-2080s, with 63 countries, including China and Japan, already experiencing population decline, creating an unprecedented aging demographic that drives sustained demand for advanced mobility solutions.

UN projections show a steep climb in the global cohort aged 65+ through 2050, ensuring unrivalled demand for mobility aids. The number of wheelchairs needed already exceeds 65 million people worldwide and is forecast to rise 22% this decade, propelled by spinal cord injuries, stroke, and osteoarthritis. Mature economies face parallel pressure as labour shortages stretch caregiving resources, making powered mobility vital for independent living. Emerging markets encounter similar demographic shifts but lack reimbursement depth, driving interest in affordable imports. Together, these forces underpin resilient, cross-regional growth for the electric wheelchair market.

Argonne National Laboratory pegs average lithium-ion pack costs USD 140/kWh in 2023 and foresees a slide to USD 86/kWh by 2035, with faster drops possible under green-energy incentives. Falling chemistry costs let OEMs fit bigger batteries, extending range and reducing charge anxiety. Electric-vehicle supply chains offer scale economies that spill into medical devices, shrinking unit costs for cells, BMS, and chargers. Advanced thermal-management modules originally designed for cars now appear in premium wheelchairs, boosting safety and lifecycle. Combined, these factors cut lifetime operating expense, widening the addressable demand for the electric wheelchair market.

Top-tier models priced between USD 8,000 and USD 30,000 remain out of reach for underinsured users. Complex electronics, servo motors, and custom seating inflate annual maintenance to 15-20% of upfront outlay. Medicare approval often entails lengthy physician documentation that delays funding, prompting cash-strapped buyers to postpone upgrades. In rural zones, certified technicians are scarce, forcing owners to ship their units long distances for repairs. Such hurdles moderate adoption speed and suppress the full potential of the electric wheelchair market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The rear-wheel drive segment of the electric wheelchair market accounted for 47.02% of the market in 2025 and emerged as the fastest-growing segment, with a 10.05% CAGR through 2031. Rear-wheel drive systems dominate due to their superior outdoor performance and stability on uneven terrain. In contrast, center-wheel drive configurations serve indoor navigation requirements with tight turning radii, which is essential for residential use.

Front-wheel drive models occupy specialized niches for users requiring maximum forward visibility and obstacle navigation, particularly in occupational therapy and rehabilitation settings. All-wheel and hybrid drive systems represent emerging categories that combine multiple propulsion methods to optimize performance across diverse environments, though adoption remains limited by complexity and cost considerations. The drive type selection increasingly reflects lifestyle preferences rather than medical requirements, as users seek devices that enable participation in recreational activities and social engagement beyond basic mobility assistance.

Hospitals commanded 60.85% of the market share in 2025. However, the personal segment represents the fastest-growing at 9.55% CAGR through 2031, signaling expansion beyond traditional medical applications. This diversification challenges manufacturers to develop products that balance medical device regulations with performance requirements for active use environments.

Hospitals and clinics maintain steady demand for institutional-grade devices designed for multiple users and intensive daily operation. At the same time, rehabilitation centers increasingly specify advanced models with programmable settings for therapeutic progression. Long-term care facilities represent a stable but mature segment, with purchasing decisions driven by durability and maintenance considerations rather than advanced features. The emergence of sports and adventure applications creates opportunities for specialized product lines incorporating ruggedized components and enhanced performance capabilities, potentially commanding premium pricing while expanding the addressable market beyond traditional healthcare channels.

The Electric Wheelchair Market Report is Segmented by Drive Type (Front-Wheel Drive, Centre-Wheel Drive, Rear-Wheel Drive, and More), End User (Personal/Homecare, Hospitals and Clinics, and More), Battery Technology (Sealed Lead-Acid, Lithium-Ion, and More), Distribution Channel (Dealer/Offline Retail, Online/E-commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

North America commands the largest revenue pool with a market share of 38.55%, reflecting mature healthcare infrastructure and comprehensive reimbursement systems. However, growth moderates as market penetration approaches saturation levels in key demographic segments. The region benefits from established distribution networks and regulatory clarity through FDA medical device pathways, enabling rapid adoption of technological innovations. Medicare coverage guidelines, despite complexity, provide predictable funding mechanisms that support premium device adoption among qualifying users.

Asia-Pacific is the fastest growing with a CAGR of 11.62% over the forecast period, adding incremental USD 1.1 billion to the electric wheelchair market size over 2026-2031. China's Tier-2 expansion campaign yields double-digit volume growth as local distributors open warranty depots within a 150 km radius of target populations. Japan's fast-ageing demographic prefers premium smart-wheelchairs integrated with home-automation systems, a segment growing 15% annually. Australia and South Korea see government-backed voucher schemes subsidizing up to USD 4,000 of purchase cost, directing demand toward mid-range lithium-ion models. Nevertheless, fragmented regulatory regimes and variable GST rates require adaptable pricing and certification tactics for successful entry. Europe retains a technologically sophisticated consumer base. The EU Battery Regulation 2023/1542 establishes global precedent for sustainability requirements in battery-powered devices, creating competitive advantages for manufacturers with established environmental compliance capabilities. Urban pay-as-you-go platforms in Germany and Spain proliferate, giving casual users access to premium devices without ownership burdens. Eastern Europe records higher unit growth as EU cohesion funds modernize rehabilitation hospitals and elder-care centers. The Middle East and Africa account for under 5% of global value today. Still, Gulf Cooperation Council states exhibit accelerating procurement driven by public-sector hospital expansion and inclusive-city initiatives ahead of major sporting events. South Africa's disability-grant uplift boosts household purchasing power, yet after-sales logistics remain a bottleneck. Collectively, these patterns highlight geographic segmentation as a key determinant of the marketing mix within the electric wheelchair market.