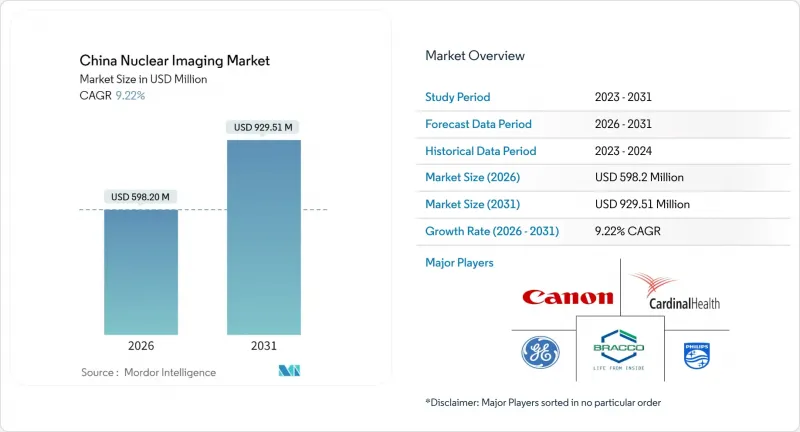

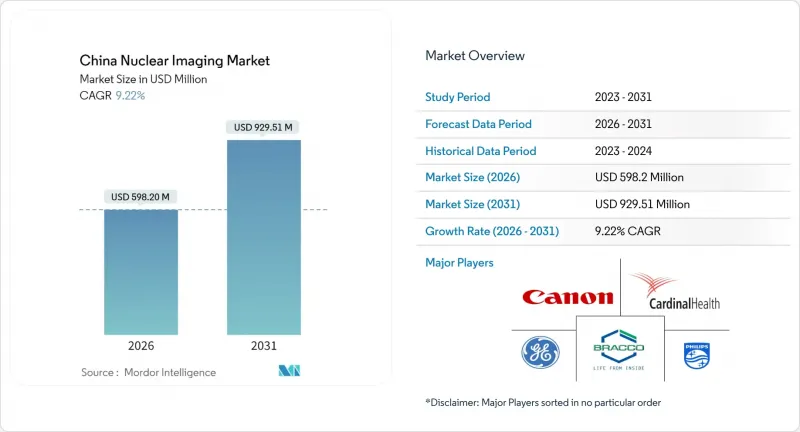

2026년 중국의 핵의학 영상 시장 규모는 5억 9,820만 달러로 추정되며, 2025년 5억 4,771만 달러에서 성장이 전망됩니다.

2031년에는 9억 2,951만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 9.22%의 CAGR로 확대될 전망입니다.

이는 '건강 중국 2030' 구상에 따른 의료 현대화 추진, 공공 지출 증가, 첨단 진단 기술 보급 확대 등을 반영한 것입니다. PET/CT 스캐너 설치 증가, 국내 방사성동위원소 생산 가속화, 혁신 의료기기를 우선시하는 규제 개혁으로 병원 및 외래 진료 환경에서의 수요 전망이 강화되고 있습니다. 중앙정부와 지방정부의 자본 투자 약속과 더불어 민간 의료보험의 보급률이 급증하면서 고부가가치 영상 진단 장비의 자금 조달 경로가 개선되고 있습니다. 한편, uEXPLORER 플랫폼으로 대표되는 전신 PET 기술에 대한 추진은 분자 이미징 연구 및 임상 응용 분야에서 중국의 선도적 위치에 대한 의지를 보여주고 있습니다. 그러나 장비 비용, 동위원소 물류, 숙련된 핵의학 기술자 부족과 같은 구조적 문제는 단기적인 보급 속도를 억제할 수 있는 장벽으로 남아있습니다.

2024년 중국에서 320만 건의 암이 새로 보고되고, 심혈관질환이 여전히 주요 사망 원인으로 작용하고 있어 고정밀 영상 진단에 대한 수요가 증가하고 있습니다. 18F-FAPI-04 PET/CT는 췌장선암에서 기존 18F-FDG를 능가하여 평가 대상 환자의 23%에서 TNM 병기 분류를 개선하여 첨단 방사성의약품에 대한 임상적 근거를 강화했습니다. 전신 PET 시스템은 전립선암 환자의 8.47%에서 기존 시야 외 병변을 발견하여 치료 계획의 재검토를 유도하고, 측정 가능한 임상적 유용성 향상을 시사했습니다. 종합적으로, 암 부담의 증가와 생활습관병 관련 CVD의 증가 추세는 3차 의료기관부터 신생 외래센터까지 정밀의료 전략에서 핵의학 영상 진단이 필수적이라는 것을 보여줍니다.

'건강 중국 2030'은 핵의학을 국가 진단 현대화의 핵심 축으로 삼고 있으며, 이와 보완적으로 '의료용 동위원소 중장기 발전 계획(2021-2035)'은 국내 동위원소 생산능력에 대한 자금 배분을 명시하고 있습니다. 정부의 의료비 지출에서 차지하는 비중은 2000년대 초 17.1%에서 2024년까지 약 30%로 상승할 것으로 예상되며, 거시적 예측에 따르면 2030년까지 상승세가 지속될 것으로 보입니다. 2025년 3월 국무원의 의견은 시급히 필요한 의료기기의 승인 절차를 가속화할 수 있는 길을 제시했으며, 기존 PET/CT 승인을 지연시켰던 절차적 마찰을 해소했습니다. 지역 간 자금 격차는 여전히 존재하지만, 서부지역을 대상으로 한 보조금과 일대일로 수출 프로그램을 통해 자본은 서비스가 잘 제공되지 않는 시장으로 향하고 있습니다.

PET/CT 스캐너의 단가는 보통 200만 달러 이상이며, 정부 지출이 증가하고 있음에도 불구하고 소규모 병원의 경우 자금 조달의 장벽이 되고 있습니다. 공급측 보조금은 부유한 연안 지역의 격차를 줄이는 반면, 개발도상국에서는 수요측 바우처가 더 효과적입니다. 민간보험의 보급으로 접근성이 높아진 반면, 고급 추적자의 상환 일정은 성별로 여전히 불일치하고 있습니다. 전신 PET의 도입으로 위양성률의 증가, 워크플로우의 복잡성, 추가적인 교육 및 품질 관리 비용이 발생하여 소규모 의료기관에서는 그 부담을 감당하기 어려운 상황입니다.

2025년 병원의 PET/CT 도입이 가속화됨에 따라 장비는 중국 핵의학 영상 시장 규모에서 64.12%의 압도적인 점유율을 유지했으며, 설치 대수는 2025년까지 1,600대를 넘어설 것으로 예상됩니다. 유나이티드 이미징 헬스케어의 uMR Jupiter 5.0T와 NeuroEXPLORER 뇌 PET 플랫폼은 국내 업체가 초고자기장 및 서브밀리미터급 영상 진단 분야에 진출했음을 보여줍니다. 경쟁력 있는 가격 책정, 지역 밀착형 서비스 네트워크, 국가 의약품 감독관리국(NMPA) 가이드라인에 따른 신속한 규제가 3차 의료 기관에서 의료기기 부문의 성장을 촉진하고 있습니다.

방사성동위원소는 정책적 지원에 의한 자급자족 추진과 중국동위원소방사선공사가 방사성의약품 공급의 70%를 장악하면서 9.84%의 가장 빠른 CAGR을 기록했습니다. 99mTc와 같은 SPECT 추적자가 수량 측면에서 우위를 점하고 있는 반면, 18F와 68Ga를 포함한 고가대 PET 동위원소가 가치 성장을 주도하고 있습니다. 가속기 생산은 폐기물을 줄이고, 분산화를 지원하여 2차 암 진료 시설로의 보급을 강화하고 있습니다.

중국 핵의학 영상 시장 보고서는 제품별(장비, 방사성동위원소-SPECT : 테크네튬-99m, 탈륨-201, 갈륨, 요오드, 기타 SPECT 방사성동위원소, PET : 불소18, 루비듐82, 기타 PET 방사성동위원소), 용도(심장학, 신경학, 갑상선, 종양학, 기타 용도), 최종사용자(병원, 진단영상센터, 학계, 연구기관), 지역별로 구분하여 분석하였습니다. 갑상선, 종양학, 기타 용도), 최종사용자(병원, 진단영상센터, 학술/연구기관), 지역별로 분류되어 있습니다.

China nuclear imaging market size in 2026 is estimated at USD 598.2 million, growing from 2025 value of USD 547.71 million with 2031 projections showing USD 929.51 million, growing at 9.22% CAGR over 2026-2031.

This expansion mirrors China's drive to modernize healthcare under the Healthy China 2030 blueprint, rising public expenditure, and the widening adoption of advanced diagnostic technologies. Growing installations of PET/CT scanners, accelerating domestic radioisotope production, and regulatory reforms that prioritize innovative medical devices are strengthening the demand outlook across hospital and outpatient settings. Capital investment commitments from both central and provincial authorities, coupled with surging commercial health-insurance penetration, are improving funding pathways for high-value imaging equipment. Meanwhile, the push toward full-body PET technology-highlighted by the uEXPLORER platform-illustrates China's aspiration to lead in molecular imaging research and clinical application. However, equipment cost, isotope logistics, and a shortage of trained nuclear-medicine technologists remain structural obstacles that could temper near-term adoption trajectories.

China recorded 3.2 million new cancer cases in 2024, while cardiovascular disease stayed the top mortality driver, intensifying demand for high-accuracy imaging modalities. 18F-FAPI-04 PET/CT outperformed conventional 18F-FDG in pancreatic adenocarcinoma by upgrading TNM staging in 23% of evaluated patients, reinforcing the clinical case for advanced radiopharmaceuticals. Full-body PET systems uncovered lesions outside conventional fields in 8.47% of prostate-cancer patients, prompting treatment-plan revisions and signaling measurable clinical utility gains. Collectively, the oncology burden and rising lifestyle-related CVD prevalence make nuclear imaging indispensable for precision medicine strategies throughout tertiary hospitals and emerging outpatient centers.

Healthy China 2030 positions nuclear medicine as a core pillar of nationwide diagnostic modernization, complemented by the Mid- and Long-Term Development Plan for Medical Isotopes (2021-2035) that earmarks funds for domestic isotope capacity. Government health-expenditure share in total spending rose from 17.1% in the early 2000s to nearly 30% by 2024, and macro projections suggest continuing uplift toward 2030. March 2025 State Council opinions introduced accelerated pathways for urgently needed medical devices, removing procedural frictions that historically delayed PET/CT approvals. Regional funding gaps persist, but targeted subsidies for western provinces plus Belt-and-Road export programs are tilting capital toward underserved markets.

PET/CT scanners typically exceed USD 2 million per unit, posing financing barriers for smaller hospitals despite rising government expenditure. Supply-side subsidies narrow the gap in affluent coastal regions, whereas demand-side vouchers are more effective in less-developed provinces. Commercial insurance penetration accelerates access, yet reimbursement schedules for advanced tracers remain inconsistent across provinces. Total-body PET deployments highlighted higher false-positive rates, adding workflow complexity and imposing additional training and quality-control costs that smaller institutions struggle to absorb.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Equipment retained a dominant 64.12% share of the China nuclear imaging market size in 2025 as hospitals accelerated PET/CT deployment, with installed bases expected to top 1,600 units by 2025. United Imaging Healthcare's uMR Jupiter 5.0T and the NeuroEXPLORER brain PET platform underline domestic manufacturers' move into ultra-high-field and sub-millimeter imaging niches. Competitive pricing, localized service networks, and regulatory fast-tracks under NMPA guidelines sustain equipment-segment momentum across tertiary facilities.

Radioisotopes posted the fastest 9.84% CAGR, underpinned by policy-backed self-sufficiency drives and China Isotope & Radiation Corporation's 70% grip on radioactive-drug supply. SPECT tracers such as 99mTc dominate volume, while premium-priced PET isotopes-including 18F and 68Ga-lift value growth. Accelerator production cuts waste and supports decentralization, reinforcing penetration into tier-2 oncology clinics.

The China Nuclear Imaging Market Report is Segmented by Product (equipment; Radioisotope-SPECT: Technetium-99m, Thallium-201, Gallium, Iodine, Other SPECT Radioisotopes; PET: Fluorine-18, Rubidium-82, Other PET Radioisotopes), Application (cardiology, Neurology, Thyroid, Oncology, Other Applications), End User (hospitals, Diagnostic Imaging Centres, Academic & Research Institutes), and Geography.