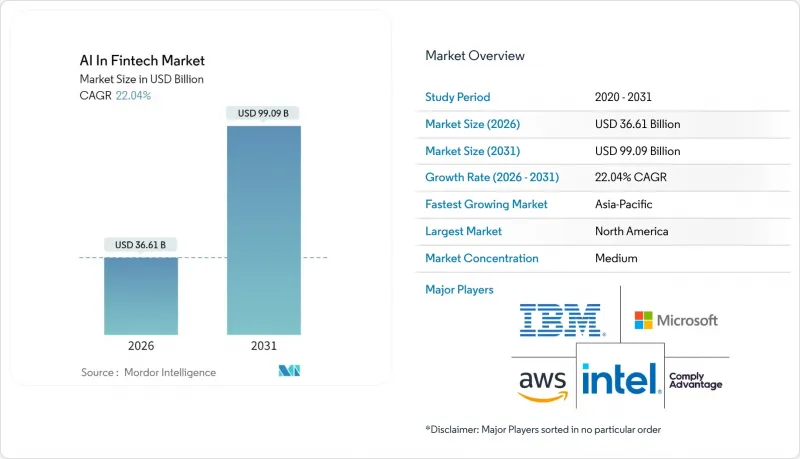

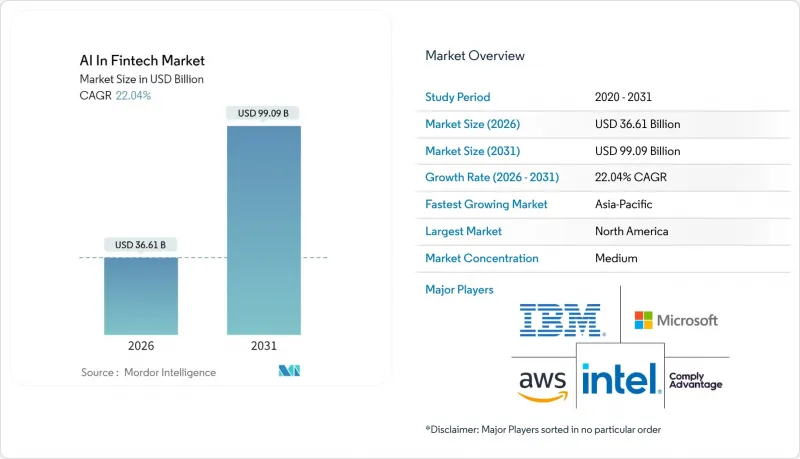

핀테크용 AI 시장 규모는 2025년에 300억 달러로 평가되었고, 2026년 366억 1,000만 달러에서 2031년까지 990억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 22.04%로 예상됩니다.

성장을 견인하는 것은 세분화된 고객 데이터를 개방하는 오픈뱅킹 의무화, 실시간 결제 인프라의 성숙, 그리고 중견은행의 운영비용을 절감하는 클라우드 네이티브 AI 플랫폼입니다. 생성형 AI 코파일럿은 모델 리스크 관리의 타임라인을 몇 개월에서 며칠로 단축하고, 금융기관이 컴플라이언스를 준수하는 리스크 모델을 전례 없이 빠른 속도로 출시할 수 있게 해줍니다. BNY Mellon 등 금융기관에서월9조 달러 이상의 고빈도 결제 데이터가 부정행위 감지 및 유동성 예측을 고도화하는 AI 엔진에 공급되고 있습니다. 이러한 요소들의 융합은 총소유비용의 감소가 보급 확대를 촉진하고, 보급 확대는 더 풍부한 데이터 세트를 생성하여 모델 정확도를 강화하는 선순환을 만들어내고 있습니다.

PSD3(제3차 결제 서비스 지침)와 같은 데이터 공유 의무화로 인해 AI 엔진은 여러 금융기관의 기록에 대한 일관된 권한 기반 접근이 가능해져 실시간 신용점수와 초개인화된 제안을 실현할 수 있게 되었습니다. 2024년 시행된 PSD3에 따라 유럽 은행들은 API 퍼스트 아키텍처를 기반으로 상품 구성 워크플로우를 재설계했습니다. 기존에는 사일로화되어 있던 데이터 세트를 머신러닝 모델에 공급하고 있습니다. 중견 금융기관은 컴플라이언스 투자가 혁신의 촉진요인으로 작용하고, 규제 비용을 수익 성장의 수단으로 전환함으로써 경쟁의 평등성을 확보할 수 있습니다. 오픈뱅킹 도입률이 금융기관의 87%를 넘어선 시장에서는 이미 AI 서비스 보급률이 높은 임베디드니다.

VisaNet+AI는 각 승인 과정에서 98%의 안정성 예측 정확도를 달성하고, Smarter Settlement Forecast는 7일간의 현금 흐름 예측을 추가하여 유동성 버퍼를 축소합니다. 실시간 결제 기반은 일괄 처리 시스템에서는 포착할 수 없는 행동 신호를 전달하고, AI가 부정행위 발생 후 밀리초 단위로 감지할 수 있도록 합니다. 조사에 따르면, 결제 전문가의 94%는 AI가 사기 방지에 필수적이라고 인식하고 있으며, 소비자의 77%는 금융기관의 AI 도입을 기대하고 있습니다. BNY멜론은 결제지시 처리의 90%를 자동화하여 애널리스트를 부가가치 업무로 전환했습니다. 즉각적인 데이터 가용성은 동적 현금 흐름 지표를 기반으로 한 실시간 신용 판단도 실현합니다.

머신러닝 숙련도와 규제 지식을 겸비한 전문가에 대한 수요는 공급보다 2-4배 더 많으며, 74%의 고용주가 채용에 어려움을 겪고 있는 것으로 나타났습니다. 유럽 은행의 25%만이 공식적인 생성형 AI 교육 시스템을 갖추고 있어 역량 격차가 확대되고 있습니다. 기존 금융직보다 40-60% 높은 급여 수준은 테크 대기업과 상위권 은행에 유리한 상황을 만들어내고 있습니다. 중견기업은 인력 부족으로 인해 프로젝트 기간과 비용이 늘어나면서 도입이 지연될 위험이 있습니다.

솔루션 분야는 2025년 214억 4,000만 달러 시장 규모를 기록하며 핀테크용 AI 시장의 71.45%를 차지했습니다. 기업들은 단일 관리 플랫폼 내에서 부정 분석, 고객 지원, 거버넌스를 통합하는 플랫폼을 선호합니다. 2025년 혁신상을 수상한 FICO의 블록체인 지원 거버넌스 스위트는 통합 솔루션이 주류가 될 이유를 보여줍니다. 서비스 부문은 현재 규모가 작지만, 은행들이 복잡한 생성형 AI 파이프라인을 구축하고 하루 234건에 달하는 규제 통지를 관리할 수 있는 자문 파트너를 찾으면서 2031년까지 연평균 복합 성장률(CAGR) 27.95%를 나타낼 것으로 예측됩니다.

컨설팅 기업은 컴플라이언스 의무를 모델 설계로 전환하여 가치 창출 시간을 단축할 수 있습니다. 이러한 수요로 인해 전문 시스템 통합사업자들은 바쁘게 움직이고 있으며, 서비스 수수료는 예측 가능한 수익원으로 자리 잡고 있습니다. 서비스 전문 지식이 확산되는 가운데, 내부 기술력 부족으로 AI 도입을 미뤄왔던 중견기업도 진입하면서 핀테크의 AI 고객 기반이 확대되고 있습니다.

클라우드 환경은 방대한 거래량을 처리하는 탄력적인 컴퓨팅을 배경으로 2025년 도입 수익의 81.35%를 차지할 것으로 예측됩니다. JP모건 체이스의 아키텍처에서 용도의 70%는 퍼블릭 클라우드에 배치되고, 민감한 워크로드는 20억 달러 규모의 프라이빗 시설에 저장되어 있습니다. 규제 당국이 거주지 규정을 강화하고 은행들이 단일 벤더의 장애 위험을 제한하기 위해 노력하는 가운데, 하이브리드 도입은 CAGR 27.4%를 나타낼 것으로 예측됩니다.

하이브리드 모델은 주권 확보를 위해 트레이닝 파이프라인을 On-Premise에 배치하고, 추론 처리를 클라우드에서 수행함으로써 두 가지의 장점을 모두 활용합니다. 이러한 유연성으로 인해 하이브리드는 특히 엄격한 데이터 현지화를 시행하는 관할권에서 지속 가능한 대안으로 자리매김하고 있습니다.

본 '핀테크의 AI' 보고서는 유형별(솔루션 및 서비스), 도입 형태별(클라우드 및 On-Premise), 용도별(부정 및 리스크 관리, 챗봇, 가상비서 등), 조직 규모별(대기업, 중소기업, 네오뱅크), 최종 사용자별(리테일, 보험, 은행, 보험 등), 지역별로 구분하여 분석하였습니다. 뱅킹, 보험 등), 지역별로 분류되어 있습니다.

북미는 2025년 37.60%의 매출 점유율을 차지할 것으로 예상되며, 성숙한 금융 인프라와 명확하지만 단편적인 규제 지침에 힘입어 성장하고 있습니다. JP모건 체이스는 2,000명의 AI 전문가와 400개 이상의 사용사례를 보유하고 있어 현지의 기술 깊이를 보여주고 있습니다. 캐나다의 네오파이낸셜과 같은 신생 은행들은 AI를 서비스 미흡한 분야로 확장하고 있으며, 멕시코는 금융 포용을 위해 AI를 활용하고 있습니다. 민관의 지속적인 투자는 북미를 혁신의 실험장으로서 지원하고 있으며, 세계 모범사례를 핀테크용 AI 시장에 환원하고 있습니다.

아시아태평양은 2031년까지 33.1%의 가장 빠른 CAGR을 나타낼 것으로 예측됩니다. 중국은 2024년 생성형 AI에 21억 달러를 투입하고, 기업 활용률은 83%에 달하고, 유럽과 미국의 보급률을 크게 웃돌고 있습니다. 인도와 일본은 AI 엔진에 의존하는 종합적인 대출과 정량적 거래 데스크를 통해 모멘텀을 확장하고 있습니다. 이 지역의 핀테크 수익은 2021년 2,450억 달러에서 2030년까지 1조 5,000억 달러로 확대될 가능성이 있으며, 은행의 87%가 핀테크 제휴를 계획하고 있습니다. 싱가포르는 모바일 결제에서 선도적인 위치에 있으며, 호주 및 뉴질랜드는 GDP 대비 불균형적인 AI 가치 획득을 예상하고 있습니다.

유럽에서는 컴플라이언스 부담으로 인해 도입 속도가 느려지고 있습니다. EU AI법은 리스크 계층화 시스템을 도입하여 거버넌스 비용을 증가시키는 한편, 윤리적 도입을 보장합니다. 영국에서는 제너럴 AI의 활용률이 70%에 달하며, 브렉시트 후의 기동성을 활용하여 은행용 샌드박스를 커스터마이징하고 있습니다. 독일과 프랑스는 국내 주요 기업 내에 AI 우수 센터를 설립했고, 북유럽 국가들은 녹색금융 평가 프레임워크를 시범운영하고 있습니다. 동유럽 시장에서는 국경을 초월한 임금 송금에 AI를 활용하는 실험이 이루어지고 있으며, 기존의 서비스 경계가 재구성되고 있습니다.

The AI in Fintech market was valued at USD 30 billion in 2025 and estimated to grow from USD 36.61 billion in 2026 to reach USD 99.09 billion by 2031, at a CAGR of 22.04% during the forecast period (2026-2031).

Growth is being propelled by open-banking mandates that liberate granular customer data, the maturation of real-time payment rails, and cloud-native AI platforms that trim operating costs for mid-tier banks. Generative AI copilots are compressing model-risk-management timelines from months to days, letting institutions release compliant risk models at unprecedented speed. High-frequency payment data, more than USD 9 trillion monthly at institutions such as BNY Mellon, feeds AI engines that sharpen fraud detection and liquidity forecasts. Convergence of these forces sustains a flywheel in which lower total cost of ownership invites wider adoption, and wider adoption produces richer datasets that reinforce model accuracy.

Mandatory data-sharing rules such as PSD3 grant AI engines consistent, permissioned access to multi-institution bank records, enabling real-time credit scoring and hyper-personalized offers. PSD3 went live in 2024, prompting European banks to redesign product origination workflows around API-first architectures that feed machine-learning models with previously siloed datasets. Mid-tier institutions gain competitive parity because compliance investments double as innovation enablers, turning regulatory cost into revenue growth levers. Markets where open-banking adoption exceeds 87% of institutions already display elevated AI service penetration.

VisaNet +AI processes each authorization with 98% stability prediction accuracy, while its Smarter Settlement Forecast adds seven-day cash-flow projections that shrink liquidity buffers. Real-time rails broadcast behavioral signals that batch systems miss, letting AI flag fraud milliseconds after initiation . Surveys show 94% of payments professionals view AI as indispensable for fraud mitigation, and 77% of consumers expect institutions to deploy it. BNY Mellon automated 90% of back-office payment instruction handling, freeing analysts for value-added tasks. Instant data availability also powers live credit decisions based on dynamic cash-flow metrics.

Demand for professionals who blend machine-learning mastery with regulatory fluency exceeds supply by 2-4 times, with 74% of employers reporting hiring struggles. European banks note that only 25% have formal GenAI training pipelines, widening capability gaps. Salary premiums of 40-60% over traditional finance roles tilt the playing field toward tech giants and tier-one banks. Mid-tier firms risk stalled deployments as talent scarcity inflates project timelines and costs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions generated USD 21.44 billion in 2025, equal to 71.45% of the AI in Fintech market. Enterprises favor platforms that unify fraud analytics, customer support, and governance within a single control plane. FICO's blockchain-enabled governance suite, which won a 2025 innovation award, illustrates why integrated offerings dominate. The services segment is smaller today but is projected to grow at 27.95% CAGR through 2031 as banks seek advisory partners to configure complex GenAI pipelines and manage the daily swell of 234 regulatory notices.

Consultancies help translate compliance obligations into model design, accelerating time to value. This demand keeps specialized system integrators busy and cements service fees as a predictable revenue stream. As service expertise proliferates, mid-tier firms that once delayed AI adoption due to limited internal skill sets now jump in, broadening the AI in Fintech market customer base.

Cloud environments delivered 81.35% of deployment revenues in 2025 on the back of elastic compute that processes massive transaction volumes. JPMorgan Chase's architecture shows 70% of applications in public cloud while sensitive workloads reside in USD 2 billion private facilities. Hybrid deployments are forecast to advance at 27.4% CAGR as regulators tighten residency rules and banks look to limit exposure to single-vendor outages.

Hybrid models place training pipelines on-premise for sovereignty yet run inference in cloud, unlocking the best of both worlds. This flexibility positions hybrid as a durable choice, particularly in jurisdictions enforcing strict data localization.

The AI in Fintech Market Report is Segmented by Type (Solutions and Services), Deployment (Cloud and On-Premise), Application (Fraud and Risk Management, Chatbots and Virtual Assistants, and More), Organization Size (Large Enterprises and SMEs and Neo-Banks), End-User (Retail Banking, Insurance, and More), and Geography.

North America held 37.60% revenue share in 2025, supported by a mature financial stack and clear though fragmented regulatory guidance. JPMorgan Chase fields 2,000 AI specialists and over 400 live use cases, underscoring local skill depth. Canada's challenger banks such as Neo Financial scale AI to underserved segments, and Mexico leverages AI for financial inclusion. Continued public-private investment sustains North America as an innovation laboratory, feeding global best practices back into the AI in Fintech market.

Asia-Pacific is projected to register the fastest 33.1% CAGR through 2031. China poured USD 2.1 billion into generative AI in 2024 and records 83% enterprise usage, dwarfing western penetration rates. India and Japan extend momentum through inclusive credit and quantitative trading desks that rely on AI engines. The region's fintech revenue could move from USD 245 billion in 2021 to USD 1.5 trillion by 2030, with 87% of banks planning fintech partnerships. Singapore leads in mobile payments, while Australia and New Zealand expect disproportionate AI value capture relative to GDP.

Europe demonstrates strong adoption tempered by compliance overhead. The EU AI Act imposes a risk-tier system that elevates governance costs but assures ethical deployment. The UK reports 70% GenAI usage, leveraging post-Brexit agility to tailor banking sandboxes. Germany and France fund AI centers of excellence inside national champions, and the Nordics pilot green-finance scoring frameworks. Eastern markets experiment with AI for cross-border wage remittances, redrawing traditional service boundaries.