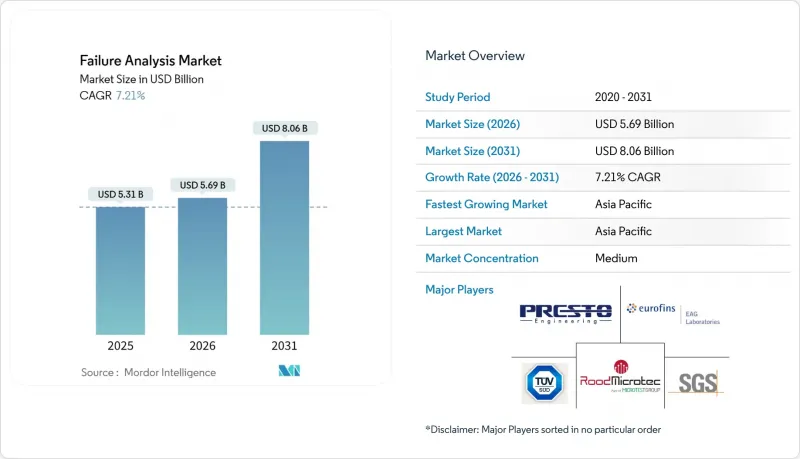

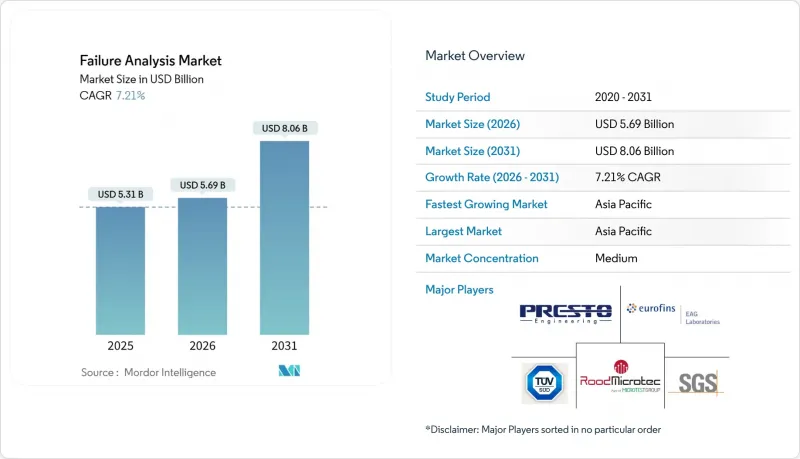

고장 분석 시장은 2025년 53억 1,000만 달러에서 2026년에는 56억 9,000만 달러로 성장하며, 2026-2031년에 CAGR 7.18%로 추이하며, 2031년까지 80억 5,000만 달러에 달할 것으로 예측됩니다.

지속적인 성장은 반도체 제조의 정밀진단에 대한 수요 증가, 보다 심층적인 검사 절차가 필요한 노후화된 산업 인프라, 그리고 기존 테스트 방법으로는 해상도가 부족한 나노 스케일 디바이스로의 꾸준한 전환에 힘입은 바 있습니다. 미국 CHIPS 법과 다른 국가들의 유사한 노력에 따라 눈에 띄게 가속화되고 있는 공급망 현지화는 팹내 자체 분석 실험실 도입을 촉진하고, 소형 자동화 툴에 대한 병행 수요를 창출하고 있습니다. 장비 벤더들은 원인 규명 주기를 단축하는 듀얼 빔 플랫폼과 AI 지원 워크플로우로 대응하고 있습니다. 한편, 석유 및 가스 등 자산 집약적인 분야에서는 고가의 다운타임을 억제하기 위해 예측 유지보수 프로토콜을 채택하고 있습니다. 아시아태평양은 정부 보조금과 촘촘한 주조 네트워크에 힘입어 설비투자의 중심지로 자리매김하고 있습니다. 북미에서는 정책적 인센티브를 활용하여 생산능력의 국내 회귀와 지적재산권 관리를 강화하고 있습니다.

부식 관련 고장으로 인해 석유 및 가스 산업은 연간 13억 7,200만 달러의 손실을 입고 있으며, 이러한 부담으로 인해 사업자들은 예기치 못한 가동 중단 전에 열화를 감지하는 예측 고장 분석 프로그램을 도입하고 있습니다. 딥러닝을 활용한 유한 요소 모델은 현재 파이프라인 건전성 관리 루틴에 통합되어 지연이 발생하는 수동 검사를 대체하고 열악한 운영 환경에서 진단 시간을 단축하고 있습니다. 노후화된 개별 제조 설비에서도 비슷한 추세를 볼 수 있으며, 나노 스케일 재료 분석을 통해 공구 수명을 연장하고 수백만 달러 규모의 생산 중단을 방지할 수 있습니다. 유틸리티, 정유소, 교통 인프라 소유주들이 계획된 유지보수에 주사전자현미경 검사를 도입하는 사례가 증가하고 있으며, 산업 자산의 수명이 길어짐에 따라 고장 분석 시장 전반에 걸쳐 지속적인 수요가 창출되고 있습니다.

AI 지원 이미지 인식 기술을 통해 복잡한 결함 패턴을 몇 분 안에 분할할 수 있으며, 분석 주기를 몇 주에서 몇 시간으로 단축할 수 있게 되었습니다. 자이스는 자동화 크로스빔 FIB-SEM을 시연하여 3D NAND 스택내 결함을 자율적으로 가공, 이미지화, 분류하여 기존 대비 60%의 처리 시간을 단축했습니다. TESCAN의 대만 사업 확장은 10nm 이하의 해상도를 필요로 하는 첨단 패키징 기술에 대한 장비 제조업체의 진출을 더욱 강조하고 있습니다. 장비에 직접 내장된 실시간 분석 기능을 통해 생산라인 내에서 공정 윈도우의 즉각적인 수정이 가능하여 고장 분석을 독립된 연구소에서 생산 현장으로 효과적으로 전환하고 있습니다. 검출기, 이온 컬럼, 고휘도 광원의 발전으로 해상도를 잃지 않고 시야를 넓혀 2차 이온과 X선 분광 측정을 단일 패스로 통합하는 멀티모달 워크플로우를 촉진하고 있습니다.

최첨단 듀얼 빔 FIB-SEM 장비는 수백만 달러의 가격대를 형성하고 있으며, 엄격한 환경 제어가 가능한 방진실을 필요로 합니다. 여기에 유지보수, 소모품, 시설 개보수 비용까지 고려하면 평생 투자금액은 두 배로 늘어납니다. 예산이 부족한 기업은 아웃소싱에 의존하는 경우가 많은데, 이 경우 물류 지연이나 기밀 유지 문제가 발생할 수 있습니다. 이에 반해 장비 벤더들은 모듈형 시스템, 공유 시설 비즈니스 모델, 구독형 소유권 구조 등을 제안하여 자본 지출을 분산하고 접근을 민주화하고 있습니다.

2025년 기준 고장 분석 시장에서 SIMS는 28.85%의 점유율을 차지했습니다. 이는 한 자릿수 나노미터 수준까지 정밀도가 향상되는 도펀트 프로파일링 능력을 높이 평가했기 때문입니다. 집속 이온빔 장치 관련 고장 분석 시장 규모는 3D 장치 진단시 특정 부위 단면 분석 수요에 힘입어 8.36%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. SIMS, EDX, 비행시간형 질량분석기를 한 스테이지에 통합한 하이브리드 플랫폼은 워크플로우의 공정을 단축하고 데이터 상관성을 향상시켰습니다. 신기술인 상대 이온 에칭은 마스킹에 의한 아티팩트 없이 깊이 분해능을 가진 조성 프로파일링이 필요한 MEMS 및 첨단 재료 프로젝트를 보완합니다. 향후 5년간 AI를 통한 일상적인 분광 데이터 분석이 중견 팹에 대한 적용 범위를 확대하고, SIMS의 대응 가능 기반을 확대하는 동시에 자동화된 결함 격리에 대한 FIB의 견인력을 강화할 것입니다.

3D 패키징의 보급 확대는 특히 원자 수준의 표면 정밀도가 중요한 양자 소자 개발에서 스캐닝 프로브 조사 기법에 대한 수요를 증가시킬 것입니다. 포토닉스 집적회로의 대량 생산에 따라 자외선 레이저 보조 SIMS는 미약한 신호 결함의 매핑을 담당합니다. 기술 다변화와 함께 고장 분석 시장에서는 두 자릿수 장비 갱신 주기가 지속되어 지속적인 투자 기반이 마련될 것으로 예측됩니다.

아시아태평양은 2025년 전 세계 매출의 46.72%를 차지할 것으로 예상되며, 파운드리 역량 집중과 반도체 자급자족을 위한 국가 보조금에 힘입어 2031년까지 연평균 7.89%의 성장률을 보일 것으로 전망됩니다. 일본은 국내 생산 확대를 위해 3조 9,000억 엔(257억 달러)의 예산을 책정하고, 지역내 장비 도입 및 전문 서비스 수요를 급증시키고 있습니다. 중국의 현지화 전략은 수출규제의 역풍 속에서도 국내 벤더와 해외 공급업체들 수요를 지탱하고 있습니다. 한국의 메모리 분야에서의 선도적 위치와 대만의 첨단 로직 분야에서의 우위는 차세대 분석 플랫폼의 안정적인 조달을 지원하고 있습니다.

북미는 2위를 차지하고 있으며, CHIPS and Science Act(반도체 및 과학 기술 진흥법)에 따른 520억 달러의 보조금 및 세제 혜택이 계획 단계에서 자체 고장 분석 연구소를 포함한 신규 팹 건설을 촉진하고 있습니다. 오대호 지역과 미국 남서부 지역의 전기자동차 공급망 성장으로 인해 전력기기 신뢰성 연구에 대한 지역적 수요가 더욱 확대되고 있습니다. 유럽은 독일의 자동차 및 산업 자동화 클러스터에서 높은 채택률을 보이고 있습니다. ISO 9001 준수는 체계적인 결함 예방 사이클을 추진하고 있습니다. 중동 및 아프리카에서는 석유 및 가스 파이프라인 건전성 프로그램, 사우디아라비아의 '비전 2030' 반도체 허브 정책 등 반도체 생태계 구축을 위한 초기 움직임과 관련하여 새로운 수요가 나타나고 있습니다. 남미는 여전히 작은 시장이지만, 광산 장비의 고장 진단 및 재생에너지 부품 분석 분야에서 유망한 움직임을 보이고 있으며, 다국적 툴 벤더들이 유통업체와의 제휴를 모색하는 계기가 되고 있습니다.

The Failure Analysis market is expected to grow from USD 5.31 billion in 2025 to USD 5.69 billion in 2026 and is forecast to reach USD 8.05 billion by 2031 at 7.18% CAGR over 2026-2031.

Persistent growth rests on rising precision-diagnostics demand in semiconductor manufacturing, aging industrial infrastructure that mandates deeper inspection routines, and the steady shift to nanoscale devices where conventional test methods lose resolution. Intensifying supply-chain localization, most visibly under the U.S. CHIPS Act and similar initiatives elsewhere, accelerates in-house analytical-lab adoption inside fabs, creating parallel demand for compact, automated tools. Equipment vendors are responding with dual-beam platforms and AI-assisted workflows that shorten root-cause cycles, while asset-heavy sectors such as oil and gas adopt predictive protocols to curb costly downtime events. Asia-Pacific remains the epicenter of capital expenditure, helped by government subsidies and its dense foundry network, whereas North America leverages policy incentives to reshore capacity and tighten intellectual-property control.

Corrosion-related failures cost the oil and gas sector USD 1.372 billion each year, a burden that is steering operators toward predictive failure analysis programs that detect degradation before unplanned shutdowns. Deep-learning-enabled finite-element models are now embedded into pipeline-integrity routines, replacing slower manual inspections and cutting diagnostic time in harsh operating zones. Similar patterns appear in aging discrete-manufacturing equipment, where nanoscale materials analysis helps extend tool life and prevent multi-million-dollar production halts. Utilities, refineries, and transportation infrastructure owners increasingly embed scanning-electron-microscopy checks in scheduled maintenance, illustrating how industrial asset longevity fuels recurring demand across the failure analysis market.

AI-assisted image-recognition now segments complex defect patterns in minutes, slashing analysis-cycle time from weeks to hours. ZEISS demonstrated an automated Crossbeam FIB-SEM that can autonomously mill, image, and classify faults in 3D NAND stacks, shaving 60% off typical turnaround schedules. TESCAN's expansion in Taiwan further underscores toolmakers' push into advanced-packaging nodes that require resolution below 10 nm. Real-time analytics embedded directly on the tool allow immediate process-window corrections inside fab lines, effectively relocating failure analysis from separate laboratories to production floors. Advancements in detectors, ion columns, and high-brightness sources also extend the field-of-view without compromising resolution, fostering multimodal workflows that merge secondary-ion and X-ray spectrometry in a single pass.

A state-of-the-art dual-beam FIB-SEM can command several million USD and requires vibration-isolated rooms with strict environmental controls, doubling the lifetime investment once maintenance, consumables, and facility retrofits are factored in. Budget-constrained enterprises often resort to outsourcing, introducing logistics delays and potential confidentiality issues. Tool vendors are countering with modular systems, shared-facility business models, and subscription-based ownership structures that spread capital outlays and democratize access.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

SIMS held 28.85% of the failure analysis market share in 2025, favored for dopant-profiling accuracy that scales into single-digit nanometers. The failure analysis market size tied to Focused Ion Beam tools is on course for an 8.36% CAGR, propelled by demand for site-specific cross-sectioning during 3D-device diagnostics. Hybrid platforms that merge SIMS, EDX, and time-of-flight mass spectrometry on the same stage now shorten workflow steps and improve data correlation. Emerging Relative Ion Etching complements MEMS and advanced-materials projects that need depth-resolved compositional profiling without masking artifacts. Over the next five years, AI-assisted routine-spectra interpretation will extend usability to mid-tier fabs, expanding the addressable base for SIMS while reinforcing FIB traction in automated defect isolation.

Wider 3D packaging adoption also lifts scanning-probe methodologies, especially for quantum-device development that hinges on atomic-scale surface fidelity. As photonics-integrated circuits enter mass production, ultraviolet laser-assisted SIMS steps in to map low-signal defects. Collectively, technology diversification will sustain double-digit tool refresh cycles and anchor continuous investment in the failure analysis market.

The Failure Analysis Market Report is Segmented by Technology (Secondary ION Mass Spectrometry, Energy Dispersive X-Ray Spectroscopy, and More), Equipment (Scanning Electron Microscope, Focused Ion Beam System, and More), End-User Industry (Automotive, Oil and Gas, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 46.72% of global revenue in 2025 and is forecast to grow at 7.89% CAGR through 2031, bolstered by concentrated foundry capacity and national subsidies that target semiconductor self-sufficiency. Japan earmarked JPY 3.9 trillion (USD 25.7 billion) to lift domestic output, sparking a surge in regional tool installations and specialized-service inquiries. China's localization strategy keeps domestic tool vendors and overseas suppliers occupied, even amid export-control headwinds. South Korea's memory leadership and Taiwan's advanced-logic dominance reinforce steady procurement of next-generation analytical platforms.

North America ranks second as the CHIPS and Science Act allocates USD 52 billion in grants and tax incentives, motivating new fabs that embed in-house failure analysis laboratories during planning phases. Electric-vehicle supply-chain growth around the Great Lakes and U.S. Southwest further increases regional demand for power-device reliability studies. Europe follows with strong adoption in Germany's automotive and industrial-automation clusters, where ISO 9001 compliance drives systematic defect-prevention cycles. Middle East and Africa exhibit emerging traction, primarily tied to oil-and-gas pipeline integrity programs and early moves to build semiconductor ecosystems under policy umbrellas such as Saudi Arabia's Vision 2030 semiconductor hub. South America remains a smaller market but shows promise in mining-equipment fault diagnostics and renewable-energy component analysis, leading multinational tool vendors to explore distributor partnerships