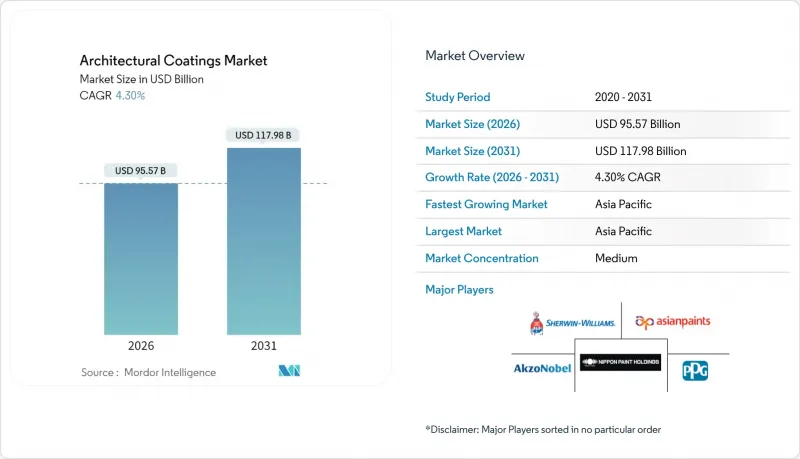

건축용 코팅 시장 규모는 2026년에는 955억 7,000만 달러로 추정되고 있으며, 2025년 916억 2,000만 달러에서 계속 성장하고 있습니다.

2031년까지의 예측에서는 1,179억 8,000만 달러에 달하며, 2026-2031년에 CAGR 4.3%로 확대가 전망됩니다.

저 VOC 배합에 대한 규제 요건, 수성 기술 도입 가속화, 성숙한 주택 재고의 리노베이션 수요가 이러한 안정적인 성장 궤도를 지원하고 있습니다. 미국 고온 기후 주에서 쿨루프 규제 의무화로 반사성 도료의 보급이 촉진되고 있으며, 중국 2, 3급 도시에서는 수성 도료로의 전환이 빠르게 진행되어 전 세계 제품 구성을 지속가능한 화학 기술로 전환하고 있습니다. 한편, 노동력 부족과 에폭시 원료 가격의 변동은 이익률을 압박하고 있으며, 노동력 절약형 도포 툴와 스마트 코팅 기술에 대한 투자를 촉진하고 있습니다.

주택담보대출 금리가 고공행진을 이어가면서 주택 소유주들은 이전보다 리노베이션을 선택하고 있으며, 캘리포니아주 타이틀 24에 의해 의무화된 쿨루프 특성을 갖춘 고급 외장 페인트에 대한 수요가 증가하고 있습니다. 페인트는 건축 허가 워크플로우에 통합되어 있으며, 임의적인 주기가 아니기 때문에 컴플라이언스가 예측 가능한 수요를 창출하고 있습니다. 로스엔젤레스의 녹색건축법은 태양 반사율 지수(SRI) 임계치를 규정하고 있으며, 지역 유틸리티는 평방피트당 0.20달러의 리베이트를 지급하여 고부가가치 배합에 대한 프로젝트 예산 확대를 촉진하고 있습니다. 고령화에 따른 재택 생활 지향 증가로 재도장 주기가 연장되고, 장기 유지보수를 억제하는 장수명 시스템에 대한 투자 의욕이 높아지고 있습니다. 제조업체 입장에서는 개보수 지출이 신축 활동보다 변동성이 적고, 보다 안정적인 생산 계획이 가능하다는 장점이 있습니다. 전문 공급업체들은 소비자의 의사결정을 효율화하는 컬러 시각화 앱과 업체 매칭 서비스를 결합하여 이러한 변화를 활용하고 있습니다.

캘리포니아주 및 국제에너지절약기준(IECC)은 1-3구역의 저경사 지붕에 대해 경년변화 후 태양반사율 0.55 이상, 열방사율 0.75 이상을 의무화하고 있으며, 건설업체에 CRRC 인증 제품 채택을 권장하고 있습니다. 인증 제도는 경쟁 환경을 좁히고, 고반사성 안료와 내구성 있는 엘라스토머 바인더의 연구개발을 촉진합니다. 허가 신청과 연동하여 공급업체는 수요량을 보다 정확하게 예측하고 장기적인 원자재 계약을 협상할 수 있습니다. 공기층이 있는 지붕 구조에 대한 예외 조치는 건축 설계에 영향을 미치고, 코팅과 통기성 기재를 결합한 하이브리드 시스템의 보급을 촉진할 수 있습니다. 텍사스, 애리조나 등의 주에서도 기준을 개정하고 있으며, 전국적인 도입이 가속화되고 있습니다.

2023년 시행되는 규제로 인해 디이소시아네이트 함량이 제한되고 PFAS 사용이 제한됨에 따라 유럽 제조업체들은 경화제와 방오제의 화학 성분을 재설계해야 합니다. 동등한 저장 안정성을 가진 대체품의 개발이 진행되면서 재배합 비용이 상승하고 있습니다. 농업 분야에서의 크레오소트 금지로 인해 목재 방부제 선택의 폭이 더욱 좁아지고, 범유럽 라인의 기술적 장벽이 높아졌습니다. 다국적 기업의 규격 통일 움직임은 전 세계에서 파급효과를 가져와 컴플라이언스 투자 증가와 제품 개발 주기의 장기화를 초래하고 있습니다.

수성 시스템은 2025년 건축용 도료 시장 점유율의 52.02%를 차지할 것으로 예상되며, 규제 당국의 VOC 배출 규제와 상하이에서 심천에 이르는 지방 자치 단체의 용제 함유 제품 사용 금지로 인해 4.70%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 솔벤트계 제품 대비 50% 이상의 VOC 저감 효과가 입증된 이러한 발전은 수성의 선도적 지위를 확고히 하고 있습니다. 용제 도료는 침투성과 극한의 내습성이 요구되는 틈새 시장에서 살아남는 반면, 분말 및 방사선 경화 기술은 공장 도장 마감 분야에서 점진적인 진전을 보이고 있습니다. 수성 도료가 건축용 도료 시장의 기술적 기반이 되고 있으며, 공급업체들은 규제에 따른 수요 급증에 대응하기 위해 생산 능력과 지역 밀착형 조색 인프라를 확충하고 있습니다.

EU와 북미의 지속적인 규제 강화는 중저가 및 보급형 가격대로의 기술 침투를 가속화하고, 솔벤트 기반 대체품과의 역사적 비용 격차를 축소시킬 것입니다. OEM(Original Equipment Manufacturer)와 도급 시산업체들은 ESG 보고를 준수하고 향후 컴플라이언스 리스크를 줄이기 위해 수성 도료 라인의 지정을 늘리고 있습니다. 그 결과, 대형 업체들은 수성수지 반응장치에 대한 자본투입을 진행하고 있으며, 중견기업은 독자적인 폴리머 플랫폼에 대한 접근을 위한 라이선스 계약 및 합작투자를 검토하고 있습니다. 규모의 경제로 인한 리터당 단가 하락에 따라 수성 도료의 채택은 자기증폭적으로 증가하여 전체 건축용 도료 시장의 성장에 핵심적인 역할을 담당하고 있습니다.

건축용 코팅 보고서는 기술별(수성, 솔벤트, 기타), 수지 유형별(아크릴, 알키드, 에폭시, 폴리에스테르, 폴리우레탄, 폴리우레탄, 기타 수지 유형), 용도별(주거용, 상업용), 지역별(아시아태평양, 북미, 유럽, 남미, 중동/아프리카)로 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

아시아태평양은 2025년 세계 건축용 도료 매출의 46.10%를 차지할 것으로 예상되며, 도시화, 스마트 시티 투자, 주택 건설의 급격한 성장에 힘입어 CAGR 5.52%로 확대될 것으로 예측됩니다. 중국에서는 수성페인트 의무화 시행으로 대규모 기술 전환을 추진하는 한편, 아세안 국가에서는 DIFM 서비스 모델과 가처분 소득 증가를 배경으로 고품질 가공제 채택이 진행되고 있습니다.

북미는 리노베이션 주기와 규제 중심의 쿨루프 수요로 인해 꾸준한 성장세를 유지하고 있습니다. 캘리포니아주 Title 24 및 IECC 규정에 따라 주택 착공 건수가 전반적으로 침체된 상황에서도 고반사율 도료에 대한 안정적인 수요가 창출되고 있습니다. 그러나 숙련된 도장공의 부족과 인건비 상승이 단기적인 확대를 억제하고 있으며, 시공능력을 유지하기 위해 노동력 절감형 스프레이 장비와 속경화형 도료의 도입이 진행되고 있습니다.

유럽의 성숙한 시장에서는 VOC(휘발성유기화합물), 살균제, PFAS(과불화알킬물질)에 대한 규제 기준이 강화되는 복잡한 환경 속에서 사업을 운영하고 있습니다. 재합성 비용이 수익성을 압박하는 문제도 있지만, 이 지역의 지속가능성 및 순환 경제 원칙에 대한 노력은 프리미엄 저VOC 수성 솔루션에 힘을 실어주고 있습니다. 동유럽은 인프라 프로젝트와 개보수 보조금으로 평균 이상의 성장이 예상되는 반면, 서유럽은 탄소 감축 목표 달성을 위한 고성능 외관 개보수에 집중하고 있습니다. 라틴아메리카, 중동 및 아프리카는 여전히 작은 시장이지만, 경제 다변화 및 대규모 주택 계획에 따른 성장 여력이 있으며, 산고반의 멕시코 오브니벨 그룹 인수와 같은 전략적 인수를 유치하고 있습니다.

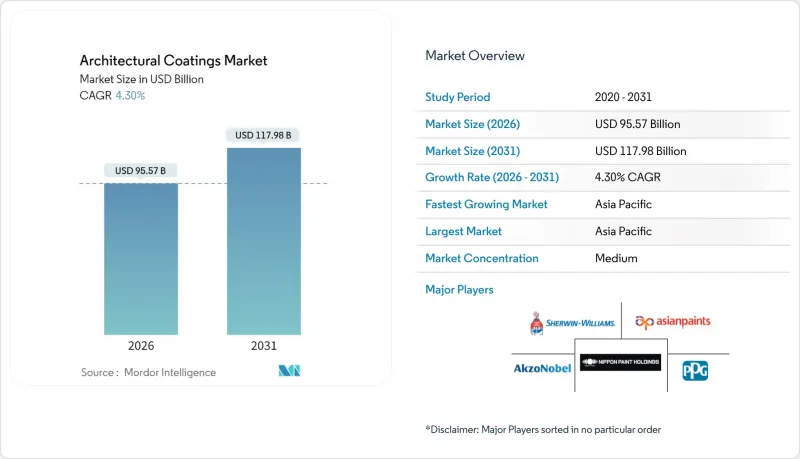

Architectural Coatings market size in 2026 is estimated at USD 95.57 billion, growing from 2025 value of USD 91.62 billion with 2031 projections showing USD 117.98 billion, growing at 4.3% CAGR over 2026-2031.

Regulatory mandates for low-VOC formulations, rapid water-borne technology adoption, and renovation-led demand in mature housing stocks underpin this steady trajectory. Mandatory cool-roof codes in U.S. hot-climate states are accelerating reflective-coating uptake, while China's Tier-2 and Tier-3 cities are fast-tracking water-borne conversions that shift global product mix toward sustainable chemistries. At the same time, labor shortages and epoxy-raw-material volatility are tightening margins, fostering investment in labor-saving application tools and smart-coating technologies.

Homeowners are choosing upgrades over relocation as high mortgage rates persist, lifting volumes of premium exterior paints with cool-roof properties mandated by California Title 24. Compliance drives predictable demand because coatings are embedded in building-permit workflows rather than discretionary cycles. Los Angeles' Green Building Code stipulates Solar Reflectance Index thresholds, while local utilities pay USD 0.20 per ft2 rebates that widen project budgets for higher-value formulations. Aging-in-place preferences extend repaint cycles, increasing willingness to invest in long-life systems that curb long-term maintenance. Manufacturers benefit as renovation spending is less volatile than new-build activity, allowing steadier production planning. Specialty suppliers leverage the shift by bundling color-visualization apps and contractor-matching services that streamline consumer decisions.

California and the International Energy Conservation Code now require aged solar-reflectance levels more than or equal to 0.55 and thermal-emittance more than or equal to 0.75 for low-slope roofs in zones 1-3, compelling builders to select CRRC-listed products. Certification narrows the competitive field and pushes formulation research and development toward high-reflectance pigments and durable elastomeric binders. Compliance linkage to permitting enables suppliers to forecast volume more accurately and negotiate longer-term raw-material contracts. Exception pathways for air-gap roof assemblies influence architectural design and may spur hybrid systems combining coatings with vented substrates. States such as Texas and Arizona are amending codes, escalating nationwide adoption momentum.

Regulations enacted in 2023 cap diisocyanate content and restrict PFAS, forcing European producers to redesign hardeners and stain-repellent chemistries. Reformulation costs rise as suppliers search for drop-in alternatives with equivalent shelf stability. Creosote bans in agriculture further squeeze wood-preservative ranges, raising technical hurdles for pan-European lines. The ripple extends globally as multinationals harmonize specifications, increasing compliance investments and elongating product-development cycles.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Water-borne systems generated 52.02% of the architectural coatings market share in 2025 and are growing at a 4.70% CAGR as regulators curb VOC emissions and municipalities from Shanghai to Shenzhen outlaw solvent-rich products. These advances, combined with demonstrated VOC reductions of more than 50% versus solvent lines, cement water-borne leadership. Solvent-borne coatings persist in niche uses requiring penetration or extreme moisture tolerance, whereas powder and radiation-curable technologies make incremental gains in factory-applied finishes. Adoption momentum positions water-borne as the technology backbone of the architectural coatings market, with suppliers scaling capacity and localized tinting infrastructure to meet code-driven demand surges.

Continued legislative tightening in the EU and North America will accelerate the technology's penetration into mid-tier and entry-level price points, narrowing historical cost gaps with solvent alternatives. OEM and contract applicators increasingly specify water-borne lines to align with ESG reporting and to mitigate future compliance liabilities. Consequently, tier-one producers channel capital toward water-borne resin reactors, while second-tier firms explore licensing or joint ventures to access proprietary polymer platforms. As economies of scale lower per-liter costs, water-borne adoption becomes self-reinforcing, underpinning its central role in overall architectural coatings market growth.

The Architectural Coatings Report is Segmented by Technology (Water-Borne, Solvent-Borne, Others), Resin Type (Acrylic, Alkyd, Epoxy, Polyester, Polyurethane, and Other Resin Types), End-Use (Residential and Commercial), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific generated 46.10% of worldwide architectural coatings revenue in 2025 and is climbing at a 5.52% CAGR, powered by urbanization, smart-city investments, and rapid residential construction. China's enforcement of water-borne mandates is propelling large-scale technology switching, while ASEAN nations leverage DIFM service models and rising disposable incomes to adopt higher-quality finishes.

North America delivers steady growth through renovation cycles and regulatory-driven cool-roof demand. California Title 24 and IECC provisions convert code compliance into steady volumes of high-reflectance coatings, even as overall housing starts moderate. However, skilled-painter shortages and escalating labor rates temper near-term expansion, prompting uptake of labor-saving spray rigs and quick-set formulations to sustain application capacity

Europe's mature market navigates a complex regulatory environment that tightens VOC, biocide, and PFAS thresholds. Reformulation costs challenge profitability, yet the region's commitment to sustainability and circular-economy principles favors premium, low-VOC water-borne solutions. Eastern European infrastructure projects and renovation subsidies offer pockets of above-average growth, while Western Europe focuses on high-performance envelope upgrades to meet carbon-reduction targets. Latin America, the Middle East, and Africa remain smaller segments but present upside tied to economic diversification and large-scale housing initiatives, attracting strategic acquisitions such as Saint-Gobain's purchase of Mexico's Ovniver Group .