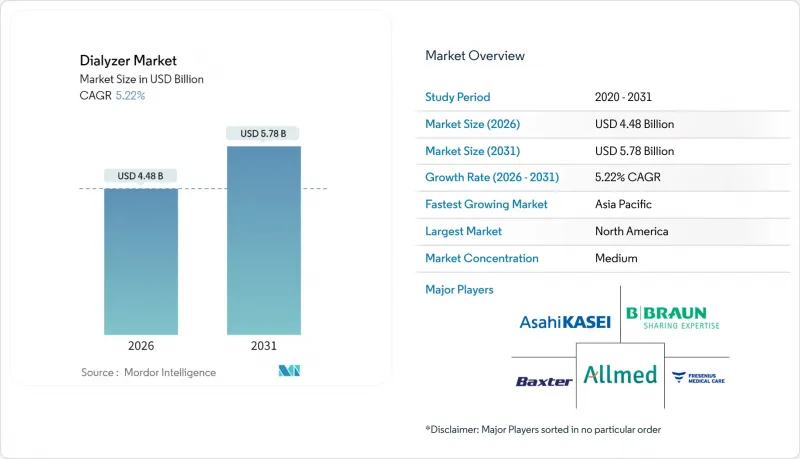

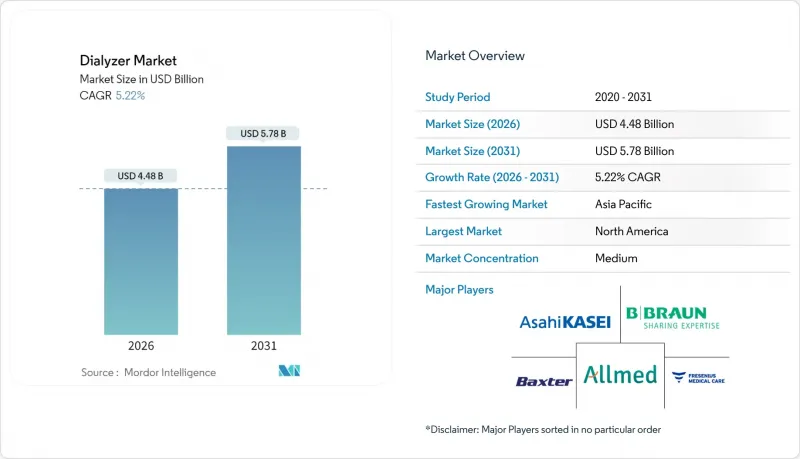

투석기 시장은 2025년 42억 6,000만 달러에서 2026년에는 44억 8,000만 달러로 성장하며, 2026-2031년에 CAGR 5.22%로 추이하며, 2031년까지 57억 8,000만 달러에 달할 것으로 예측됩니다.

이러한 성장은 만성콩팥병(CKD)의 부담 증가, 재택 투석에 대한 급여 범위 확대, 독소 제거 효율과 환자 예후를 개선하는 멤브레인 엔지니어링의 꾸준한 혁신에 뿌리를 두고 있습니다. 고농도 및 중분자량 차단 기술이 새로운 임상 성능 기준을 설정하는 한편, 의료 시스템 인센티브가 재택 치료로의 전환과 가치 기반 의료 보상 체계로 전환을 가속화하고 있습니다. 2025년 공급망 혼란은 다이얼라이저 시장이 다양한 소싱 소스에 의존하고 있다는 것을 드러냈고, 제조업체들이 지역 생산 기지 및 예측 재고 분석에 대한 투자를 촉진했습니다. 일회용 플라스틱에 대한 환경 규제는 복잡성을 더하는 한편, 순환 경제 비즈니스 모델을 지원하는 재료 과학의 혁신을 촉진하고 있습니다.

2025년 전 세계 만성콩팥병(CKD) 환자 수는 6억 7,400만 명에 달하고 사망자 수는 143만 명으로 증가. 이로 인해 투석 서비스에 대한 수요는 탄력적이지 못한 상태가 지속되고 있습니다. 고령화, 당뇨병 발병률 상승, 고혈압 비율 증가는 소득수준에 관계없이 신장기능 저하를 가속화하고 있습니다. 예측에 따르면 미국의 말기신부전(ESRD) 환자 수는 2030년까지 최대 126만 명에 달할 것으로 보입니다. 저소득 국가는 자금 및 인프라 제약으로 인해 미충족 수요가 가장 크며, 의료보험 확대에 따라 수요량 증가가 예상됩니다. 투석은 한번 시작하면 평생 지속되므로 투석기 시장은 구조적으로 안정적인 고객 기반을 가지고 있습니다. 이러한 역학적 추세는 제조업체와 서비스 프로바이더 모두에게 장기적인 매출 전망을 지원하는 기반이 될 것입니다.

미국에서는 재택투석 이용률이 재택치료를 촉진하는 메디케어 개혁에 따라 2010년 6.8%에서 2020년 13.3%로 거의 두 배로 증가했습니다. ESRD 치료 옵션 모델에 따라 2025년 기본 상환 단가가 1회당 273.82달러로 인상됨에 따라 재택 치료는 공급자와 지불자 모두에게 경제적으로 매력적인 선택이 될 수 있습니다. 휴대용 투석 시스템과 안전한 원격 모니터링 플랫폼은 COVID-19 기간 중 중요성이 재인식된 병원 감염 위험을 줄여줍니다. 그러나 현재 메디케어 인증 시설의 절반 미만이 교육을 제공하고 있으며, 단기적으로 보급을 억제하는 역량 격차가 존재합니다. 사용자 친화적인 인터페이스 설계와 원격 지원 툴의 지속적인 개선으로 남아있는 장벽을 해소하고 수요를 더욱 확대할 수 있을 것으로 기대됩니다.

저소득 국가에서는 연간 평균 19,380달러에 달하는 혈액투석 비용이 1인당 소득을 크게 상회하므로 임상적으로 적합한 환자의 32%만이 투석을 받고 있습니다. 특히 사하라 이남 아프리카와 남아시아의 일부 지역에서는 예산 부족으로 인해 자부담이 치료의 지속성을 저해하고 있습니다. 경제적 부담의 격차는 치료 시작의 지연과 치료 기간의 단축을 초래하고, 역학적 필요성이 뚜렷한 경우에도 대응 가능한 수요를 제한하고 있습니다. 다자간 자금 프로그램이나 성과연계형 자금조달(OBF)의 시범 도입이 검토되고 있지만, 광범위한 시행에는 아직 몇 년이 더 걸릴 것으로 예측됩니다.

고 플럭스 제품은 확고한 임상 성능과 광범위한 공급 기반에 힘입어 2025년에도 투석기 시장 점유율 62.58%를 유지했습니다. 그러나 중분자 클리어런스의 실증적 개선과 진화하는 상환 지원에 힘입어 중분자 컷오프 모델이 5.93%의 가장 빠른 CAGR을 달성할 것으로 예측됩니다. 니프로의 ELISIO-HX와 박스터의 Theranova 시리즈에 대한 임상 평가에서 기존 장치 대비 우수한 독소 제거 능력과 낮은 알부민 손실이 확인되었습니다. 초고 플럭스 설계는 작지만 성장하는 틈새 시장을 형성하고 있으며, 특히 장기 사망률 결과를 적극적으로 추적하는 일본 시설에서 채택이 증가하고 있습니다.

고투과성 층으로의 전환 가속화는 신장학 분야의 정밀의료에 대한 광범위한 노력과 일치합니다. 현재 시설 의사결정권자들은 투석기 사양을 선택할 때 개별화된 용질 제거 특성, 혈관 접근 제약, 세션 빈도 등을 종합적으로 평가했습니다. 이러한 추세는 R&D 비용을 상쇄하고 활발한 교체 주기를 촉진하는 프리미엄 가격 설정의 기반이 되고 있습니다. AI 기반 모니터링을 이러한 첨단 멤브레인에 통합함으로써 동적 클리어런스 목표 설정이 가능해져 경쟁하는 기존 시스템의 성능 기준을 끌어올렸습니다.

2025년 기준 일회용 유닛은 투석기 시장 규모의 78.05%를 차지할 것으로 예상되며, 감염 관리 프로토콜이 강화됨에 따라 이 비중은 더욱 증가할 것으로 예측됩니다. 팬데믹 기간 중 일회용 제품에 대한 선호도가 높아지면서 의료 서비스 프로바이더는 총 비용 평가에 인건비, 멸균 비용, 소송 위험을 포함시키는 경향이 강화되고 있습니다. 비용에 민감한 환경에서는 재사용 가능한 장치가 제한적으로 사용되지만, 검증된 재처리 시설에 필요한 자본 비용이 상대적으로 경제적 매력을 떨어뜨리고 있습니다.

2025년 혈액투석용 튜브 부족 사태는 일회용 제품에 대한 높은 의존도가 초래하는 취약성을 드러내며 공급처 다변화 전략의 중요성을 다시 한 번 강조하고 있습니다. 폐기물 관리에 대한 우려를 줄이기 위해 유럽과 아시아에서는 사용한 다이얼라이저를 회수하여 건설용 골재로 전환하는 시범사업이 시행되고 있으며, 순환경제의 새로운 수입원 창출을 보여주고 있습니다. 생분해성 폴리머를 개발하는 제조업체는 여전히 엄격한 생체 적합성 기준을 충족해야 하지만, 상용화에 성공하면 일회용 디자인의 환경적 신뢰성을 더욱 강화할 수 있을 것입니다.

북미는 2025년 투석기 시장의 39.95%를 차지했습니다. 이는 말기신부전증(ESRD) 환자들에 대한 메디케어(Medicare)의 전체 보장 및 1회당 평균 1,287달러(공적 보험의 약 5배)의 상업적 보험 환급에 힘입은 결과입니다. 성숙한 의료 프로바이더 네트워크가 중분자량 차단막과 AI 기반 모니터링 시스템의 빠른 도입을 촉진하고 있지만, 환자 수가 포화 상태에 가까워짐에 따라 성장이 둔화되고 있습니다. 2025년 튜브 부족으로 인해 전략적 비축과 국내 생산 회귀 노력이 촉진되었고, 이 지역공급망 내성 강화에 대한 노력이 강조되었습니다.

아시아태평양은 만성콩팥병(CKD) 유병률 증가, 공공보험 확대, 도시화에 따른 라이프스타일 변화로 인해 6.05%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 현재 많은 아시아 국가에서 투석 접근성이 수요의 34%만 충족하고 있으며, 미개발된 잠재적 수요가 엄청나게 많이 남아 있습니다. 중국 및 인도 정부는 상환 프로그램을 확대하고 있으며, 일본의 기존 기업은 초고투석율(super high-flux) 채택 및 야간 재택 혈액투석 모델을 선도하고 있습니다. 니프로의 노스캐롤라이나 공장 등 현지 생산에 대한 투자는 세계 수요에 대응하는 동시에 물류의 민첩성을 높이고 환리스크 감소에 기여합니다.

유럽은 단일 지불자 의료보험제도의 재정 지원하에 안정적인 한 자릿수 중반의 성장세를 유지하고 있습니다. 이 지역은 지속가능한 투석 정책에서 세계를 선도하고 있으며, 전 세계 제품 개발 로드맵에 영향을 미치고 있습니다. 프레제니우스 메디컬케어의 5008X CAREsystem은 유럽에서 광범위하게 사용된 후 미국에서도 승인을 받아 지역을 넘어선 기술 보급의 좋은 예가 되고 있습니다. 라틴아메리카와 중동 및 아프리카은 여전히 상대적으로 보급률이 낮지만, 브라질, 멕시코, 사우디아라비아, 남아프리카공화국에서는 보험 적용 범위 확대와 민간 부문의 클리닉 시설 투자 증가에 따라 치료 건수가 증가하는 추세입니다. 높은 수입관세와 환율 변동성이 단기적으로 보급을 억제하고 있지만, 거시경제의 역풍이 완화되면 장기적인 펀더멘털은 평균 이상의 성장을 촉진할 것으로 예측됩니다.

The dialyzer market is expected to grow from USD 4.26 billion in 2025 to USD 4.48 billion in 2026 and is forecast to reach USD 5.78 billion by 2031 at 5.22% CAGR over 2026-2031.

Growth is rooted in the rising chronic kidney disease (CKD) burden, expanding reimbursement for home dialysis, and steady innovation in membrane engineering that improves toxin removal efficiency and patient outcomes. High-flux and medium-cut-off technologies now set new clinical performance benchmarks, while health-system incentives accelerate the transition toward home-based modalities and value-based care payment frameworks. Supply chain disruptions in 2025 revealed the dialyzer market's dependence on diversified sourcing, encouraging manufacturers to invest in regional production hubs and predictive inventory analytics. Environmental regulations targeting single-use plastics add another layer of complexity, but they also stimulate material-science breakthroughs that support circular-economy business models.

CKD cases reached 674 million worldwide in 2025, with mortality climbing to 1.43 million deaths, anchoring an inelastic need for dialysis services . Aging populations, increased diabetes incidence, and higher hypertension rates accelerate kidney function decline across income levels. Projections indicate that U.S. end-stage renal disease (ESRD) cases could rise to as much as 1.26 million by 2030. Lower-income economies carry the largest unmet demand due to limited funding and infrastructure, setting the stage for volume growth as coverage improves. Because dialysis becomes lifelong once initiated, the dialyzer market enjoys a structurally stable client base. This epidemiological momentum underpins long-run revenue visibility for manufacturers and service providers alike.

U.S. home-based dialysis utilization nearly doubled from 6.8% in 2010 to 13.3% in 2020 under Medicare reforms that incentivize in-home treatments. The ESRD Treatment Choices Model raises the 2025 base reimbursement rate to USD 273.82 per session, making home therapy financially attractive for both providers and payers . Portable dialysis systems and secure tele-monitoring platforms reduce hospital exposure risk, a priority reinforced during the COVID-19 period. However, fewer than half of Medicare-certified facilities currently offer training, leaving a capacity gap that tempers near-term uptake. Continuous improvement in user-friendly interface design and remote support tools is expected to remove remaining barriers and unlock an additional wave of demand.

Only 32% of clinically eligible patients in low-income nations receive dialysis because annual hemodialysis costs, averaging USD 19,380, greatly exceed per-capita income levels. Governments face budget strains, and out-of-pocket payments deter adherence, especially in sub-Saharan Africa and parts of South Asia. Affordability gaps delay initiation and shorten treatment duration, limiting addressable demand even when epidemiological need is pronounced. Multilateral funding programs and outcomes-based financing pilots are under discussion, but widespread implementation remains a multi-year prospect.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

High-flux products retained 62.58% dialyzer market share in 2025, supported by established clinical performance and widespread availability. Medium cut-off models, however, are projected to secure the fastest 5.93% CAGR, fueled by demonstrable improvement in middle-molecule clearance and evolving reimbursement support. Clinical assessments of Nipro ELISIO-HX and Baxter Theranova lines show superior toxin removal and lower albumin loss versus traditional units. Super high-flux designs constitute a smaller yet growing niche, particularly in Japanese centers actively tracking long-term mortality outcomes.

The accelerating migration toward higher permeability tiers aligns with nephrology's broader precision-medicine agenda. Facility decision-makers now weigh individualized solute-clearance profiles, vascular-access constraints, and session frequency when selecting dialyzer specifications. This trend underpins premium pricing that offsets R&D cost and stimulates brisk replacement cycles. Integrating AI-based monitoring into these advanced membranes enables dynamic clearance targeting, raising the performance bar for competing legacy systems.

Disposable units accounted for 78.05% of dialyzer market size in 2025, a share expected to rise as infection-control protocols tighten. Pandemic-era guidance solidified single-use preference, and providers increasingly incorporate labor, sterilization, and litigation risk into total-cost assessments. Although reusable devices remain in limited use within cost-conscious settings, the capital required for validated reprocessing suites diminishes their relative economic appeal.

The 2025 shortage of hemodialysis tubing exposed the vulnerability created by high disposable dependence and placed renewed emphasis on supplier-diversification strategies. To mitigate waste-management concerns, pilot initiatives in Europe and Asia collect spent dialyzers for conversion into construction aggregates, illustrating emerging circular-economy revenue streams. Manufacturers pursuing biodegradable polymers must still satisfy stringent biocompatibility thresholds, but successful commercialization would reinforce the environmental credentials of single-use designs.

The Dialyzer Market Report is Segmented by Type (High-Flux Dialyzer, Medium Cut-Off Dialyzer, Low-Flux Dialyzer), Usage Type (Disposable, Reusable), Membrane Material (Cellulose-Based, Synthetic, PMMA, Others), End User (Hospitals and Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America held 39.95% dialyzer market share in 2025, underpinned by universal ESRD coverage through Medicare and an average commercial reimbursement of USD 1,287 per session-nearly five times the public rate. Mature provider networks support rapid adoption of medium-cut-off membranes and AI-embedded monitoring systems, though growth decelerates as prevalence approaches saturation. The 2025 tubing shortage prompted strategic stockpiling and onshoring initiatives, underscoring the region's focus on supply-chain resilience.

Asia-Pacific is projected to post the fastest 6.05% CAGR, driven by rising CKD incidence, expanding public insurance, and urbanized lifestyle shifts. Dialysis access today meets only 34% of need across many Asian countries, leaving large untapped potential. Governments in China and India are scaling reimbursement programs, while Japanese incumbents pioneer super high-flux adoption and nocturnal home-hemodialysis models. Local manufacturing investments, such as Nipro's North Carolina facility to serve global demand, improve logistics agility and reduce currency risk exposure.

Europe maintains steady mid-single-digit expansion under single-payer health-system funding. The region leads in sustainable-dialysis policy, influencing worldwide product-development roadmaps. Fresenius Medical Care's 5008X CAREsystem received U.S. clearance after extensive European use, illustrating cross-regional technology diffusion. Latin America and Middle East & Africa remain comparatively underpenetrated but show rising procedure volumes in Brazil, Mexico, Saudi Arabia, and South Africa as coverage widens and private-sector investment builds clinic capacity. Elevated import tariffs and currency volatility temper short-term uptake, yet longer-term fundamentals favor above-average growth once macro-economic headwinds moderate.