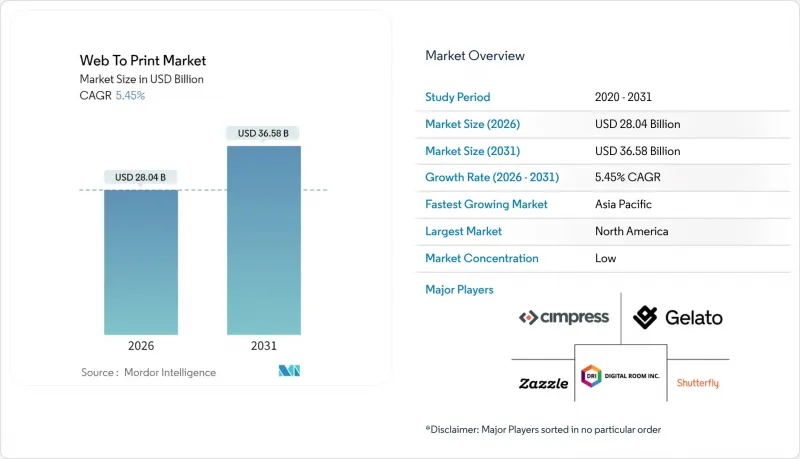

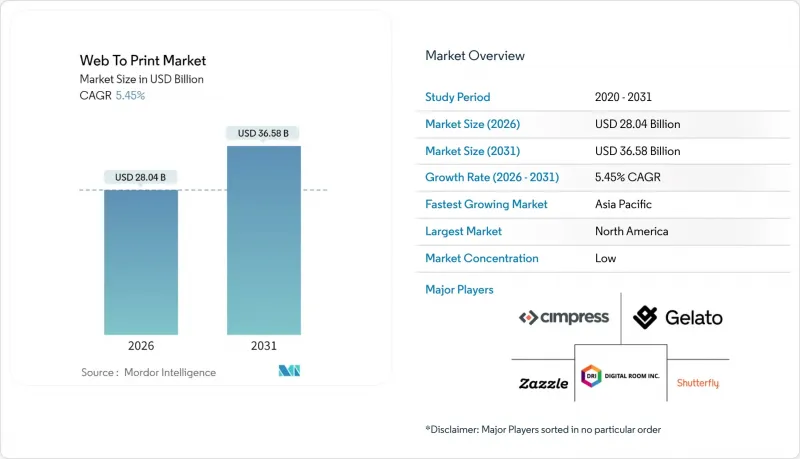

Web To Print 시장은 2025년 265억 9,000만 달러에서 2026년에는 280억 4,000만 달러로 성장하며, 2026-2031년에 CAGR 5.45%로 추이하며, 2031년까지 365억 8,000만 달러에 달할 것으로 예측됩니다.

E-Commerce 활동의 가속화, AI 기반 설계 툴의 성숙, 분산형 제조 네트워크의 보급으로 아날로그 주문에서 소프트웨어 정의 워크플로우로의 구조적 전환이 촉진되고 있습니다. 고객의 기대는 현재 소량 맞춤형 제품의 익일 배송에 집중되어 있으며, 프리프레스 공정 단축과 컬러 관리 자동화를 가능하게 하는 기술 투자를 촉진하고 있습니다. 주요 플랫폼 프로바이더들은 디자인 에디터를 EC 스토어 프론트에 직접 내장하고 결제, 교정, 조달을 한 화면에 통합하여 대응하고 있습니다. 지속가능성에 대한 노력은 지역 생산 기지가 국경을 넘는 화물 운송의 배출량을 줄이고 추적성 목표를 달성할 수 있도록 지원하는 데에도 도움이 될 것입니다. 경쟁 환경은 종이가 아닌 데이터 규모의 경제로의 전환을 반영하고 있으며, 주요 벤더들은 디자인 리포지토리, 배송 API, 분석 대시보드를 번들로 묶어 환승 비용의 확대를 꾀하고 있습니다.

마켓플레이스에 진입하는 기업이들 증가는 플랫폼 통합형 주문형 인쇄 서비스의 주문량을 증가시키고 있습니다. 2024년 말 어도비가 Adobe Express에 Zazzle의 결제 툴을 통합하기로 한 결정이 이를 지원합니다. Gelato는 2023년 25,000명 이상의 신규 점주를 확보하여 현재 184개국에서 서비스를 제공하고 있으며, 마찰 없는 판매자 지원이 잠재적 수요를 확대하는 좋은 예가 되고 있습니다. 마이크로 브랜드가 계절별 SKU 투입을 서두르는 가운데, 디자인과 물류를 통합한 Web To Print 포털은 필수적인 인프라가 되고 있습니다. 그 결과 발생하는 네트워크 효과는 대규모 색조 일관성과 배송의 신뢰성을 유지할 수 있는 공급자에게 보상을 제공합니다.

잉크젯의 생산성 향상과 인라인 품질 모니터링으로 중형 패키지 생산에서 디지털 워크플로우가 오프셋 인쇄와 경쟁할 수 있게 되었습니다. 코니카미놀타는 Industry 5.0 대응 인쇄기가 AI 품질관리와 인간 모니터링을 융합하여 정확성을 유지하면서 생산성을 향상시킬 것으로 예측했습니다. 게라트의 2025년 랜다 디지털 프린팅과의 제휴 등 파트너십은 상업적 합리성을 보여주고 있습니다. 나노그래픽 인쇄기는 오프셋 인쇄에 버금가는 선명도를 제공하며, Gerato의 소프트웨어는 가장 가까운 인증된 노드에 작업을 할당하여 사이클 타임과 폐기물을 줄입니다. 이러한 장비의 발전으로 마케팅 자료, 라벨, 접이식 카톤을 웹 기반 주문으로 전환할 수 있는 경제적 근거가 확대되고 있습니다.

관계를 중시하는 구매 담당자는 단가가 높더라도 실물 교정과 유연한 결제 조건을 제공하는 인근 인쇄소를 선택하는 경향이 있습니다. 어도비와 자즐의 제휴는 중개업체가 배제될 것을 우려하는 독립 인쇄업체들의 반발을 불러일으키며, 플랫폼 보급을 늦추는 문화적 저항을 보이고 있습니다. 촉각적 소재 확인이나 특수 가공이 필요한 프로젝트는 여전히 대면 협업을 선호하며, 온라인 공급업체는 샘플 키트와 색상 보증에 대한 투자로 전통적 충성도를 깨뜨릴 필요가 있습니다.

템플릿 기반 제품(표준 명함부터 풀업 배너까지)은 2025년 매출의 55.02%를 차지할 것으로 예상되며, 디자인 지식이 부족한 사용자들에게 직관적인 도입 수단을 제공합니다. 이 부문은 로고, 텍스트, 이미지를 사전 승인된 그리드에 자동으로 배치하는 AI 레이아웃 엔진의 혜택을 받아 이탈률을 낮추고, 프랜차이즈 사업자의 브랜드 관리 권한을 확장하고 있습니다. 완전 커스터마이징이 가능한 워크플로는 수량은 떨어지지만, 파워유저들이 세밀한 편집 유연성과 가변 데이터 기능을 요구하면서 2031년까지 7.15%의 견고한 CAGR을 나타낼 것으로 예측됩니다. 템플릿 시스템은 AI 제안 레이어를 통합하는 경향이 강해지면서 카테고리 경계를 모호하게 만들고, 브랜드 일관성을 유지하면서 거의 무한한 조합을 가능하게 하고 있습니다. 그 결과, 툴의 고도화로 디자인 시간이 단축됨에 따라 맞춤형 프로젝트에 할당되는 Web To Print 시장 규모는 확대될 것으로 예측됩니다.

반면, 순수 백지 상태의 에디터는 첨단 창의적 기술을 필요로 하며, 디자인 전문가와 틈새 시장 제작자들에게 꾸준히 사랑받고 있습니다. 교차 판매 행동에서 구매자가 템플릿으로 시작하여 자신감이 생기면 첨단 맞춤형 제품으로 이동하는 경향이 분명하며, 이 패턴은 고객 평생 가치를 연장하는 것으로 나타났습니다. 컴플라이언스 관련 분야, 특히 식품 및 의약품 업계에서는 로트 코드와 알레르기 유발 물질 표시를 확실하게 기재하기 위해 구조화된 템플릿을 선호하고 있으며, 이는 가이드 디자인의 장기적인 중요성을 확고히 하고 있습니다.

북미는 2025년 전 세계 매출의 41.20%를 차지했습니다. 이는 판촉물에 턴키 인쇄 포털에 의존하는 중소기업의 밀집 클러스터가 존재하기 때문입니다. 이 지역의 성숙한 소포 네트워크, 매력적인 배송비, 높은 광대역 보급률, 빈번한 재주문 및 마무리 업그레이드 업셀링을 촉진하고 있습니다. 식품 포장에 대한 규제 주도의 추적성(FDA의 기한 내에 시행)은 가변 데이터 라벨의 도입을 가속화하고 평균 주문 빈도를 향상시키고 있습니다. 캐나다에서는 동일한 자산의 현지화 버전이 필요한 이중 언어 포장 의무로 인해 점진적인 성장이 이루어지고 있으며, 멕시코에서는 니어쇼어링(near-shoring) 추세로 인해 국경 간 브랜드에 대응할 수 있는 웹 지원 공급업체로 포장 프로토타입이 이동하고 있습니다.

아시아태평양은 2031년까지 7.25%의 예상 CAGR을 기록하며 인도와 동남아시아의 비약적인 디지털화를 반영하고 있습니다. 중국에서는 국가가 지원하는 E-Commerce 생태계와 광범위한 디지털 결제 기반이 광둥성, 절강성 등 지역 거점으로 업무를 유도하는 매장 프런트 플러그인의 비옥한 토양을 형성하고 있습니다. 인도의 중소기업(MSME)은 저비용 스마트폰과 UPI 결제를 통해 마케팅 리플렛과 배송용 봉투를 조달하기 위해 지역 특화 포털을 점점 더 많이 활용하고 있습니다. 일본 바이어들은 색상의 정확성과 FSC 인증 소재를 중시하며, 공급업체에 색 영역의 일관성과 지속가능한 조달 증명서를 요구하는 경향이 강해지고 있습니다.

유럽에서는 적시 생산 모델을 평가하는 엄격한 환경지침을 기반으로 완만하게 확대되고 있습니다. EU의 삼림파괴 방지 규정에 따라 인쇄업체는 종이 원재료의 원산지를 추적해야 하는 의무가 발생하며, 관리 연쇄 문서를 자동화하는 클라우드 연결형 MIS가 우대받고 있습니다. 독일, 프랑스, 영국이 시장의 대부분을 차지하고 있으며, GDPR(EU 개인정보보호규정)에 따른 데이터 흐름부터 브렉시트 이후 통관 서류까지 각 지역 특유의 세밀한 현지화가 요구되고 있습니다. 스칸디나비아 국가에서는 탄소 회계가 우선시되고 있으며, 주문별 CO2 계산 기능을 내장한 플랫폼이 틈새 시장을 형성하고 있습니다. 동유럽의 인쇄 공장은 원가 경쟁력과 기술력 향상으로 유럽산 제품을 원하는 서유럽 바이어들의 계약 초과분을 끌어들이고 있습니다.

The web-to-print market is expected to grow from USD 26.59 billion in 2025 to USD 28.04 billion in 2026 and is forecast to reach USD 36.58 billion by 2031 at 5.45% CAGR over 2026-2031.

Accelerating e-commerce activity, the maturation of AI-driven design tools, and the spread of distributed manufacturing networks reinforce a structural migration away from analog job intake and toward software-defined workflows. Customer expectations now center on next-day delivery of short-run, personalized pieces, stimulating technology investments that compress pre-press cycles and automate color management. Major platform providers respond by embedding design editors directly into e-commerce storefronts, consolidating payment, proofing, and procurement on one screen. Sustainability commitments add further momentum, as local production nodes reduce cross-border freight emissions and support the objectives of traceability. Competitive dynamics reflect a pivot toward scale economies in data, not paper, with leading vendors bundling design repositories, shipping APIs, and analytics dashboards to widen switching costs.

The widening pool of marketplace entrepreneurs fuels order volumes for platform-integrated print-on-demand services, as evidenced by Adobe's decision to embed Zazzle checkout tools inside Adobe Express in late 2024. Gelato on-boarded more than 25,000 new store owners in 2023 and now serves 184 countries, illustrating how friction-free seller enablement amplifies addressable demand. As microbrands rush to publish seasonal SKU drops, web-to-print portals that combine design and logistics become indispensable infrastructure. The resulting network effects reward providers that can uphold color consistency and shipping reliability at scale.

Inkjet productivity gains and inline quality monitoring now allow digital workflows to compete against offset for mid-length packaging runs. Konica Minolta projects that Industry 5.0 press configurations will merge AI quality control with human oversight to raise throughput without sacrificing precision. Partnerships, such as Gelato's 2025 tie-up with Landa Digital Printing, demonstrate the commercial rationale: Nanographic presses provide offset-comparable vibrancy, while Gelato's software allocates jobs to the nearest certified node, reducing cycle time and waste. These equipment advances broaden the economic case for shifting marketing collateral, labels, and folding cartons to web-based ordering.

Relationship-centric buyers often choose neighborhood print shops that offer tangible proofing and flexible payment terms, even when unit costs are higher. Adobe's venture with Zazzle sparked backlash among independent printers who fear being disintermediated, illustrating cultural resistance that slows platform penetration. Projects requiring tactile substrate reviews or specialty embellishments still favor in-person collaboration, obliging online vendors to invest in sample kits and color guarantees to erode legacy loyalties.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Template-based items, ranging from standard business cards to pull-up banners, delivered 55.02% of 2025 revenue, providing an intuitive on-ramp for users with limited design expertise. The segment benefits from AI layout engines that auto-fit logos, text, and images into pre-approved grids, lowering abandonment rates and extending brand governance controls for franchisors. Fully customizable workflows trail in volume but register a healthy 7.15% CAGR to 2031 as power users demand granular editing flexibility and variable-data functionality. Template systems are increasingly incorporating AI suggestion layers, blurring categorical lines and enabling nearly limitless permutations while maintaining brand consistency. Consequently, the web-to-print market size allocated to bespoke projects is set to escalate as tool sophistication reduces design time.

In contrast, purely blank-canvas editors require higher creative skill and remain favored by design professionals and niche manufacturers. Cross-selling behaviors reveal that purchasers start with templates but migrate to advanced custom products as confidence builds, a pattern that lengthens customer lifetime value. Compliance-linked sectors, notably food and pharmaceutical, prefer structured templates to ensure the inclusion of lot codes and allergen statements, thereby cementing the long-term relevance of guided designs.

The Web To Print Market Report is Segmented by Product Type (Fully Customizable, and Template-Based), Application (Apparel, Marketing Materials, Business Cards, Packaging, Photo Books and Albums, Labels and Stickers, and More), Deployment Model (On-Premise, and Cloud-Based), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 41.20% of global revenue in 2025, driven by the presence of dense clusters of small businesses that rely on turnkey print portals for promotional materials. The region's mature parcel networks, attractive shipping rates, and high broadband penetration encourage frequent re-orders and upsell of finishing upgrades. Regulation-driven traceability for food packaging, enforced within FDA timelines, accelerates the adoption of variable-data labels, thereby boosting the average order frequency. Canada contributes incremental growth through bilingual packaging mandates that necessitate localized versions of the same asset, while Mexican near-shoring trends pull packaging prototypes toward web-enabled suppliers serving cross-border brands.

Asia Pacific stands out with a 7.25% forecast CAGR through 2031, reflecting leapfrog digitization in India and Southeast Asia. China's state-supported e-commerce ecosystem and extensive digital payment rails create fertile ground for storefront plug-ins that route jobs to regional hubs in Guangdong and Zhejiang. Indian MSMEs, empowered by low-cost smartphones and UPI transactions, increasingly use localized portals to procure marketing leaflets and courier sleeves. Japanese buyers emphasize color accuracy and FSC-certified substrates, pushing suppliers to prove gamut consistency and sustainable sourcing credentials.

Europe registers moderate expansion anchored in stringent environmental directives that reward just-in-time production models. The EU Deforestation Regulation compels printers to trace paper inputs back to origin, favoring cloud-connected MIS that automate chain-of-custody documentation. Germany, France, and the United Kingdom make up the lion's share, each demanding nuanced localization, whether GDPR-compliant data flows or post-Brexit customs documentation. Scandinavia prioritizes carbon accounting, creating niches for platforms offering embedded CO2 calculators per order. Eastern European print plants bind cost competitiveness with growing technical sophistication, attracting contractual overflow from Western buyers seeking continentally sourced merchandise.