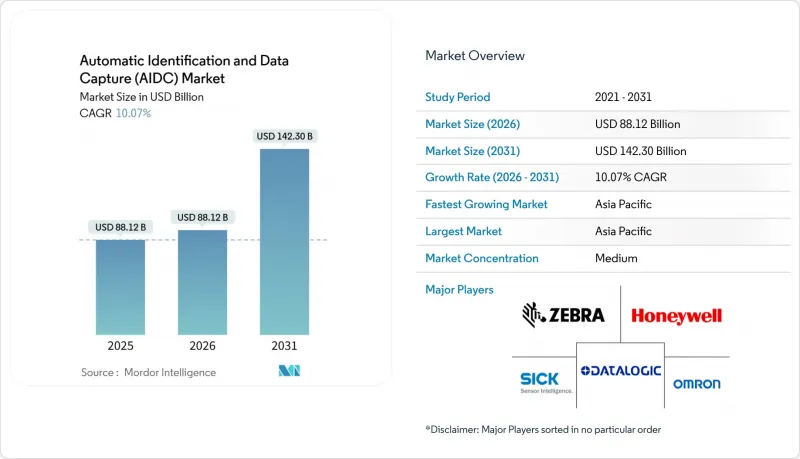

자동 식별 및 데이터 캡처(AIDC) 시장 규모는 2026년에는 881억 2,000만 달러로 추정되고 있으며, 2025년 800억 5,000만 달러에서 계속 성장하고 있습니다.

2031년의 예측에서는 1,423억 달러에 달하며, 2026-2031년에 CAGR 10.07%로 확대할 것으로 전망되고 있습니다.

62.7%의 누적 성장률은 제조, 소매, 의료 분야의 구조적 디지털화를 반영하고 있으며, 자동 식별은 처리 능력, 규정 준수 및 오류 제거에 필수적인 요소로 자리 잡고 있습니다. 인력 부족, 규제 강화, 실시간 가시성을 통한 입증된 ROI와 함께 자동 식별 및 데이터 캡처(AIDC) 시장은 재량적 지출이 아닌 인프라로 자리매김할 수 있는 수요 환경을 형성하고 있다(biometricupdate.com). 2D 코드, 패시브 UHF-RFID, 국가 전자 ID 프로그램의 도입 확대로 인해 솔루션 프로바이더가 디바이스, 미들웨어, 클라우드 분석을 통합한 일관된 생태계를 구축할 수 있는 기회가 확대되고 있습니다.

세계 소매업체들은 GS1 Sunrise 2027 기한에 대비하여 2D/QR코드로의 전환을 추진하고 있습니다. 이를 통해 유효기간, 로트 번호, 마케팅 링크를 하나의 고밀도 심볼에 포함시킬 수 있습니다. 초기 도입 기업은 풍부한 데이터로 자동 할인과 역동적인 고객 참여를 지원함으로써 음식물 쓰레기 감소와 옴니채널 경험을 촉진하고 있다고 보고하고 있습니다. 투자 효과는 수작업 감소, 판매 시점의 스캔 정확도 향상, 소비자의 스마트폰을 활용한 새로운 인터랙티브 마케팅 기법의 출현을 통해 나타나고 있습니다. 소매업체들이 기존의 1차원 스캐너를 다중 기호 해독이 가능한 이미저로 대체함에 따라 하드웨어 공급업체들은 판매량이 증가할 것으로 예측됩니다. 한편, 소프트웨어 프로바이더는 POS 펌웨어 업데이트에 따른 업그레이드 비용을 얻고 있습니다.

월마트가 2024년 도입을 의무화한 품목별 RFID 태그는 소매 업계 전반의 채택을 촉진하고 있으며, 공급업체들은 소매 체인이 수취장, 창고, 선반에서 읽을 수 있는 인레이를 내장하도록 장려하고 있습니다. 패시브 태그 단가가 0.04달러 이하로 떨어지면서 의류, 가정용품 등 주요 카테고리에서도 실시간 재고 가시성 도입을 정당화할 수 있는 수준까지 도달했습니다. 도입으로 재고 정확도가 최대 25% 향상되고 품절 발생이 크게 감소. 지속적인 판독 데이터는 방범 분석에도 활용되며, RFID는 이익률 확대와 재고 감소 대책이라는 두 가지 효과를 가져옵니다.

1990년대 ERP 시스템을 운영하는 기업에서는 RFID 데이터나 이미지 데이터를 네이티브하게 도입하기 어려워 프로젝트 비용을 최대 40%까지 증가시키는 미들웨어 계층을 도입해야 하는 경우가 많습니다. 따라서 자동 식별 및 데이터 캡처(AIDC) 시장은 통합, 테스트 및 마이그레이션 비용을 예산에 포함시켜야 하므로 판매 주기가 길어지는 문제에 직면해 있습니다. 다중 거점 네트워크에서 서로 다른 스키마는 복잡성을 증폭시키고, 약속된 ROI를 저해하는 데이터 사일로를 생성합니다. 벤더들은 사전 구축된 커넥터나 컨설팅 계약을 제공함으로써 리스크를 줄이고 있지만, 기존 시스템 도입에 있어서는 여전히 큰 장벽으로 작용하고 있습니다.

2025년 매출의 62.50%는 소매업과 의료 분야의 기반 시설 업데이트로 인해 하드웨어가 차지했습니다. 그러나 가격 압축, 표준화, 공급망 불안정성이 이익률을 압박하여 고매출 컨설팅 및 지원 계약으로의 전환을 가속화하고 있습니다. 서비스형 하드웨어(Hardware-as-a-Service, 이하 HaaS)를 번들로 제공하는 벤더들은 판매량을 유지하면서 구성 비율을 바꾸고 있습니다. 그 결과, 자동 식별 및 데이터 캡처(AIDC) 시장의 경쟁 우위는 자본 설비와 지속적인 서비스 체계를 통합하는 하이브리드 매출 모델을 습득한 공급자에게 기울어지고 있습니다.

서비스 계층은 CAGR 11.64%로 하드웨어보다 높은 성장세를 보이고 있습니다. 이는 기업이 통합, 유지보수, 클라우드 분석을 포괄하는 성과 기반 계약을 점점 더 많이 채택하고 있기 때문입니다. 많은 대형 소매업체들이 장비 투자형 조달에서 스캐너, 프린터, RFID 포털의 가동 시간을 보장하는 관리 서비스로 전환하고 있습니다. 서비스 사업자는 엣지부터 클라우드까지 오케스트레이션, 사이버 보안 강화, 다중 거점 구축에 대한 전문성으로 차별화를 꾀하고 있으며, 하드웨어 OEM은 수명주기 매출을 확보하기 위해 시스템 통합사업자를 인수하고 있습니다.

바코드는 옴니채널 운영을 지원하는 보편적인 결제 및 컴플라이언스 식별자로서 46.20%의 매출 점유율을 유지하고 있습니다. 바코드 프린터, 이미저, 라벨 관련 자동 식별 및 데이터 캡처(AIDC) 시장 규모는 소매점 면적 확대에 따라 완만한 성장세를 이어가고 있습니다. 그러나 패시브 UHF-RFID는 12.05%의 연평균 복합 성장률(CAGR)로 확대되고 있으며, 이는 여러 상품의 동시 스캔과 실시간 재고 확인이 가능한 상품 단위 도입 의무화가 반영된 것으로 분석됩니다. ROI는 상품 분실률 감소와 배송 정확도 향상에서 비롯되며, 패션, 스포츠용품, 가전제품 카테고리에서 도입이 진행되고 있습니다.

패시브 RFID의 비용 곡선 하락과 미들웨어의 성숙은 RFID가 업스트림 밸류체인 업무를 연결하고 매장에서 바코드가 소비자 표시를 유지하는 하이브리드 도입에 도움이 됩니다. 액티브 RFID는 고부가가치 자산 모니터링, 특히 항공우주 및 의료기기 분야에서 틈새 역할을 유지합니다. AI를 접목한 OCR 시스템은 물류 및 제조 현장에서 영숫자 데이터 추출이 가능하여 라벨 분실 및 손상시 적용 시나리오를 확대합니다.

북미는 2025년 매출의 34.00%를 차지했습니다. 이는 초기 도입 지역으로 품목단위 RFID와 디지털 환자 안전관리가 제도화되었기 때문입니다. 월마트의 도입 의무화로 인레이 변환업체, 프린터 인코더, 미들웨어 통합업체로 구성된 탄탄한 공급업체 생태계가 형성되었습니다. 한편, 미국은 생체인식 국경관리를 우선시하며 다중 기술 채택을 강화하고 있습니다. 자동 식별 및 데이터 캡처(AIDC) 시장에 진출한 기업은 캐나다와 멕시코의 국경 간 공급망을 연결하고, 업데이트 주기와 높은 수준의 창고 자동화를 활용하고 있습니다.

아시아태평양은 제조업 자동화 및 국가 ID 프로젝트에 힘입어 세계에서 가장 빠른 11.44%의 연평균 복합 성장률(CAGR)을 기록했습니다. 세계 최대 RFID 태그 생산국인 중국은 규모의 경제 효과를 수출함으로써 세계 태그 가격을 억제하고 있습니다. 한국, 일본, 인도에서는 생체 인증을 통합한 전자 ID 프로그램이 시행되어 스마트카드와 센서 수요를 견인하고 있습니다. E-Commerce 대기업의 창고 로봇화가 가속화되면서 자동 식별 및 데이터 캡처(AIDC) 시장의 도입 확대가 더욱 가속화되고 있습니다.

유럽에서는 규제 준수에 힘입어 꾸준한 성장을 지속하고 있습니다. EU 의료기기 규정은 표준화된 UDI 표시를 의무화하고, 디지털 ID 프레임워크 규정은 시민 지갑의 기반을 구축합니다. 프랑스와 스위스에서는 통합 ID 및 의료 솔루션의 발전으로 생체인증과 스마트카드에 대한 수요가 강화되고 있습니다. AIDC 시장 기업은 엄격한 데이터 보호 표준을 준수하는 동시에 혁신적 도입을 실현하고 있습니다.

Automatic Identification And Data Capture (AIDC) market size in 2026 is estimated at USD 88.12 billion, growing from 2025 value of USD 80.05 billion with 2031 projections showing USD 142.3 billion, growing at 10.07% CAGR over 2026-2031.

The projected 62.7% cumulative expansion reflects structural digitization across manufacturing, retail, and healthcare, where automated identification has become mission-critical to throughput, compliance, and error elimination. Labor-scarcity, increasing regulatory specificity, and proven ROI for real-time visibility collectively shape a demand environment in which the Automatic Identification And Data Capture (AIDC) market is viewed as infrastructure rather than discretionary spend biometricupdate.com. Heightened adoption of 2D codes, passive UHF-RFID, and national e-ID programs widens the opportunity set for solution providers able to integrate devices, middleware, and cloud analytics within cohesive ecosystems.

Global retailers are transitioning to 2D/QR codes in preparation for the GS1 Sunrise 2027 deadline, embedding expiry dates, lot numbers, and marketing links inside a single dense symbol. Early adopters report lower food waste and smoother omnichannel experiences because richer data supports automated markdowns and dynamic customer engagement. Investment returns manifest through fewer manual interventions, higher scan accuracy at point-of-sale, and emerging interactive marketing formats that leverage consumer smartphones. Hardware vendors gain incremental unit sales as retailers replace legacy 1D scanners with imagers capable of decoding stacked symbologies, while software providers capture upgrade fees tied to POS firmware refreshes.

Walmart's 2024 mandate for item-level RFID tags catalyzed broad retail adoption, pushing suppliers to embed inlays that retail chains read at dock, stockroom, and shelf. Cost per passive tag has fallen below USD 0.04, enabling mainstream categories such as apparel and home goods to justify real-time inventory visibility. Deployments deliver up to 25% accuracy improvement and materially reduce out-of-stock events . Continuous reads also power loss-prevention analytics, making RFID a dual lever for margin expansion and shrink mitigation.

Enterprises with 1990s-era ERP stacks struggle to ingest RFID and image data natively, often funding middleware layers that inflate project cost by up to 40%. The Automatic Identification And Data Capture (AIDC) market therefore faces elongated sales cycles because budgets must include integration, testing, and migration. In multi-site networks, disparate schema multiply complexity, generating data silos that erode promised ROI. Vendors mitigate risk by offering pre-built connectors and consulting engagements, yet the barrier remains meaningful for brown-field rollouts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware dominated 62.50% of 2025 turnover due to foundational equipment refresh across retail and healthcare. Yet pricing compression, standardization, and supply-chain contingencies squeeze margins, accelerating the pivot toward higher-margin consulting and support contracts. Vendors bundling hardware-as-a-service maintain volume while shifting mix. Consequently, Automatic Identification And Data Capture (AIDC) market competitive advantage tilts toward providers mastering hybrid revenue models that unite capital equipment with recurring service matrices.

The services layer contributed 11.64% CAGR, outpacing hardware because enterprises increasingly award outcome-based contracts covering integration, maintenance, and cloud analytics. Many tier-1 retailers migrate from capex procurement to managed services that ensure uptime for scanners, printers, and RFID portals. Services players differentiate through domain expertise in edge-to-cloud orchestration, cybersecurity hardening, and multi-site rollouts, while hardware OEMs acquire systems integrators to secure lifecycle revenue.

Barcodes retained 46.20% revenue share as ubiquitous checkout and compliance identifiers underpin omnichannel operations. The Automatic Identification And Data Capture (AIDC) market size tied to barcode printers, imagers, and labels continues to expand modestly alongside retail floor space growth. However, passive UHF-RFID expands at 12.05% CAGR, reflecting item-level mandates that unlock simultaneous multi-item scans and real-time inventory verification. ROI stems from shrink reduction and fulfillment accuracy, prompting fashion, sports equipment, and consumer electronics categories to convert.

Passive RFID's cost curve decline and middleware maturity support hybrid deployments where RFID bridges upstream supply-chain workflows while barcodes remain consumer-facing on the shelf. Active RFID preserves niche roles in high-value asset monitoring, particularly aerospace and healthcare equipment. OCR systems incorporating AI extract alphanumeric data in logistics and manufacturing, widening addressable scenarios where labels are absent or damaged.

The Automatic Identification and Data Capture (AIDC) Market Report is Segmented by Offering (Hardware, Software, Services), Product (Barcodes, RFID, Smart Cards, and More), Media Type (Labels, Tags, Cards), End-User Industry (Manufacturing, Retail and E-Commerce, and More), and by Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 34.00% of revenue in 2025 as early adopters institutionalized item-level RFID and digital patient safety. Walmart's mandate created a robust supplier ecosystem of inlay converters, printer-encoders, and middleware integrators. Meanwhile, the United States prioritizes biometric border control, reinforcing multi-technology adoption. Automatic Identification And Data Capture (AIDC) market participants capitalize on replacement cycles and advanced warehouse automation in Canada and Mexico that link cross-border supply chains.

Asia Pacific posts 11.44% CAGR, the fastest globally, fueled by manufacturing automation and national identity projects. China, the world's largest RFID tag producer, exports scale efficiencies that compress global tag pricing. South Korea, Japan, and India implement e-ID programs integrating biometrics, driving smart-card and sensor demand. E-commerce giants accelerate warehouse robotization, further expanding Automatic Identification And Data Capture (AIDC) market deployments.

Europe sustains steady growth through regulatory compliance. EU Medical Device Regulation mandates standardized UDI labeling, while the Digital Identity Framework Regulation sets a foundation for citizen wallets. France and Switzerland progress toward integrated identity-health solutions, reinforcing biometrics and smart-card volume. Automatic Identification And Data Capture (AIDC) market players align offerings with stringent data-protection norms, ensuring adoption remains compliant yet innovative.