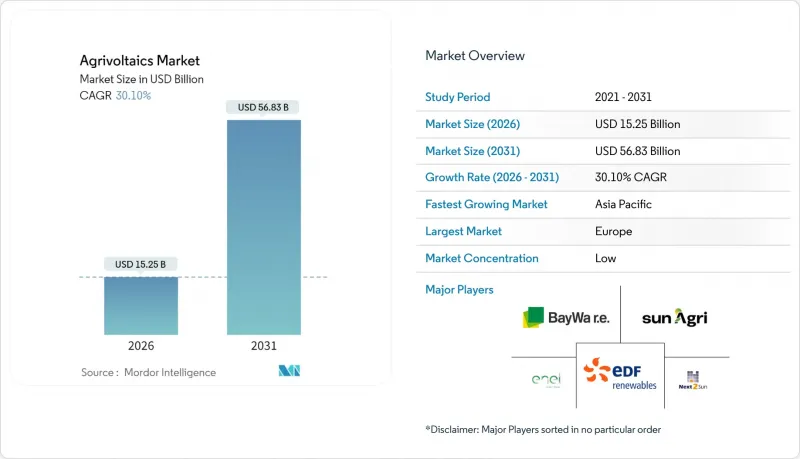

Agrivoltaics 시장 규모는 2026년에는 152억 5,000만 달러로 추정되고 있으며, 2025년 117억 2,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측에서는 568억 3,000만 달러에 달하며, 2026-2031년에 CAGR 30.1%로 확대할 전망입니다.

이러한 성장 궤적은 토지 이용 경제의 근본적인 변화에 기인합니다. 작물과 전력이라는 이중 수입원으로 인해 기존 태양광발전 대비 15-25%의 자본 프리미엄을 정당화할 수 있게 되었기 때문입니다. 아시아태평양은 2024년 매출의 69.19%를 차지하며, 중국에서는 양식, 밭작물, 축산을 상업적 규모로 통합하는 500개 이상의 프로젝트가 도입되었습니다. 유럽에서는 생산 농지에 대규모 태양광발전소 설치를 금지하는 한편, 고가형 복합이용시스템은 예외로 인정하는 규제를 통해 가속화되고 있습니다. 한편, 북미에서는 농업경영을 유지하는 멀티기가와트 규모의 사업이 빠르게 진행되고 있습니다. 양면 모듈, 고정 경사형 모듈, 지상 설치 레이아웃이 현재 도입을 주도하고 있지만, 정밀농업 데이터가 기존 태양광발전으로 달성할 수 없는 수확량 증가와 물 절약 효과를 정량화할 수 있으므로 동적 추적기, 온실 지붕, 반투명 라미네이트가 빠르게 성장하고 있습니다.

전용 고정가격 임베디드제도는 지상 설치형 어레이에 비해 15-20% 높은 자본비용을 상쇄할 수 있는 현금 흐름을 보장합니다. 이탈리아의 2026년까지 1.04GW에 달하는 인센티브는 순수 전력회사 조달이 아닌 농가 주도의 사업화를 촉진하고 있습니다. 프랑스에서는 이에 이어 35개 생산자가 주도하는 450MW 규모의 협동조합 프로젝트가 진행되었습니다. 일본의 2040년 재생에너지 로드맵은 옥상 및 태양광 용량을 우선순위에 두고 장기적인 정책의 가시성을 강화하고 있습니다. 초기 프로젝트에서 생성된 실적 데이터는 후속 리스크 프리미엄을 낮춰 유럽 및 아시아태평양 전체에 선순환적인 보급 사이클을 형성하고 있습니다.

2024년 이후 양면 모듈의 세계 비용은 25-30% 하락하여 토지 비용을 증가시키지 않고도 에너지 밀도를 높일 수 있습니다. 단면 패널 대비 15-25%의 수율 향상은 추운 지역에서의 눈의 알베도 효과에 의해 더욱 강화되어 프로젝트의 경제성을 높입니다. 2024년 중국의 양면 모듈 200GW의 설치 용량은 추가적인 가격 하락을 지원할 것이며, 영국의 수직 양면 어레이는 경사형 시스템 대비 25.38%의 출력 증가를 보일 것입니다. 비용 추이를 볼 때, 고부가가치 농지에서도 3-5년 이내에 그리드 패리티를 달성할 수 있을 것으로 예측됩니다.

고가 설치 구조와 넓은 열 간격으로 인해 지상 설치형 태양광발전과 비교하여 프로젝트 자본 지출이 15-25% 증가합니다. 금융기관이 작물과 전력의 복합매출을 평가하므로 자금조달의 장벽은 여전하지만, 독일 분석에 따르면 농장 규모에 따라 연간 매출이 15,000-23만 5,000유로까지 다양합니다. 양면수광형과 추적 시스템 도입에 따른 학습곡선 효과로 인한 비용 절감은 2027년까지 그리드 패리티에 도달할 것으로 예측됩니다.

2025년 기준, 고정형 경사형 어레이가 농업용 태양광발전 시장의 69.62%를 차지할 것으로 예측됩니다. 그 이유는 구조의 단순함과 내구성에 있습니다. 다이내믹 트래커는 하드웨어 가격 차이가 8-12%로 축소되는 가운데 CAGR 31.25%로 성장하고 있습니다. 이들은 일사각도를 최적화하고, 서리 피해 위험이 높은 과수원을 위한 가변형 차광 기능을 제공합니다. Fraunhofer ISE의 경량 작물 탑재 모듈은 정밀농업 장비와 연동되는 차세대 설계의 선구자입니다. 동적 설치 시스템은 이미 베리류, 양상추 등 고부가가치 분야에서 활용되고 있으며, 시장 모델에서는 2030년까지 35-40%의 점유율을 차지할 것으로 예측했습니다.

고정식 구성은 여전히 목초지 방목을 지배하고 있으며, 균일한 차광을 통해 계절 조정 없이도 사료 품질을 향상시킬 수 있습니다. 추적기의 O&M 비용이 감소하고 실시간 농학 제어가 확대됨에 따라 생산자는 특정 작물 및 가축의 요구 사항에 맞게 패널의 이동성을 조정하는 균형 잡힌 설계 믹스를 기대하고 있으며, 이는 농업용 로봇 시장의 자본 격차를 더욱 좁힐 수 있습니다.

양면 모듈은 2025년 출하량의 74.52%를 차지하며 CAGR 31.02%로 성장하고 있습니다. 중국에서의 양산화와 수직형 거치대의 급속한 보급으로 양면 어레이는 작물 관상층, 토양, 적설 등 후면에서 빛을 채광할 수 있으며, 추가 부지 없이도 헥타르당 발전량(kWh)을 증가시킬 수 있습니다. 영국 실지시험에서 수직단면 설치방식 대비 일량 7.87%, 경사단면 기준치 대비 25.38% 높은 발전량을 기록해 성능적 우위를 입증했습니다.

단면적 패널은 저알베도 지역에서는 여전히 사용되지만, 2028년까지 가격 경쟁력이 역전되어 신규 태양광발전 설비는 모두 양면형으로 전환될 가능성이 있습니다. 빛 이용 효율 5-5.5%를 실현하는 반투명 라미네이트는 온실용으로 보급이 진행되고 있으며, PAR광(식물생장광)의 필요성과 전력 자급자족의 균형을 실현하고 있습니다. 기술 로드맵에서는 페로브스카이트와 실리콘을 결합한 양면 셀을 구현하여 모듈 효율 30% 이상의 모듈 효율을 달성함으로써, 아그리바익스 시장의 면적당 규모 우위를 더욱 확대할 것으로 예상하고 있습니다.

본 농업용 태양광 시장 보고서는 시스템 설계(이동식 패널/고정식 패널), 기술(단면/양면/반투명), 작물(과일/채소/기타), 설치 장소(온실/지상 설치/차광망), 용도(목초지 농업, 원예/경작 농업, 실내 농업 등), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카) 별로 분류하여 조사했습니다. 중동, 아프리카) 별로 분류되어 있습니다.

아시아태평양은 2025년 전 세계 매출의 68.70%를 차지할 것으로 예상되며, 중국의 양식장, 논, 염소 목장 등 500개 이상의 가동 사이트가 이를 주도했습니다. 산동성의 양어장 시스템은 유휴 수면을 발전소로 전환하면서 새우 수확량을 50% 증가시켰습니다. 일본은 2040년까지 재생에너지 비율 40-50% 달성을 위해 옥상 및 농지 설치형 어레이에 대한 자금 지원을 포함한 복합 이용 모델을 의무화하고 있습니다. 인도에서는 저비용 강철 캐노피가 소규모 농지에 적용되고 있으며, 한국에서는 농업과 태양광발전의 통합을 통해 바이오연료 잠재력을 정량화하고 있습니다.

유럽은 CAGR 31.60%로 가장 빠르게 성장하는 지역입니다. 이탈리아는 비옥한 토양에 지상 설치형 태양전지판을 금지하고, 17억 유로의 인센티브 기금을 결합하여 개발업체들의 애그리볼트 시스템 진입을 촉진하고 있습니다. 프랑스의 'Terr'Arbouts'(35개 농가 파트너와 7㎢)와 독일의 'SUNfarming-SPIE' 753MW 파크는 대규모 도입 준비가 되어 있음을 보여주고 있습니다. 강설량이 많은 북유럽 국가에서는 일조시간이 짧은 겨울철에 양면 집광패널의 후면 발전 효과를 활용하여 대륙 전체에 활력을 불어넣고 있습니다.

북미에서는 복합용도 메가사이트에 의한 규모 확대가 진행되고 있습니다. 오하이오주의 태양광 800MW + 축전 300MW 복합단지는 부지의 3분의 2를 농경지로 확보하여 규제 당국의 수용성을 보여주고 있습니다. 버몬트주의 수직 설계는 농지 이용률 90%를 유지합니다. 연방 LASSO 어워드 자금은 가축 방목과 태양광발전을 결합하고, 미국 농무부와 에너지부의 연구 협력을 통해 농업학 데이터세트를 생성하여 위험 감소와 자본 유입 촉진에 기여하고 있습니다. 멕시코의 원주민 시범 시설은 농업용 태양광발전이 오지 지역의 디젤 펌프 비용 절감과 옥수수 수확량 향상에 기여할 수 있다는 것을 입증하고 있습니다.

남미와 중동 및 아프리카은 여전히 개발 중입니다. 콜롬비아의 초기 단계 사이트와 카타르의 반투명 양상추 온실은 탐색 단계이긴 하지만 유망한 발판을 보여주고 있습니다. 이들 지역에서는 2027년 이후 지붕 설치형 태양광발전의 보급 곡선을 반영하여 비용 하락이 발생할 수 있습니다.

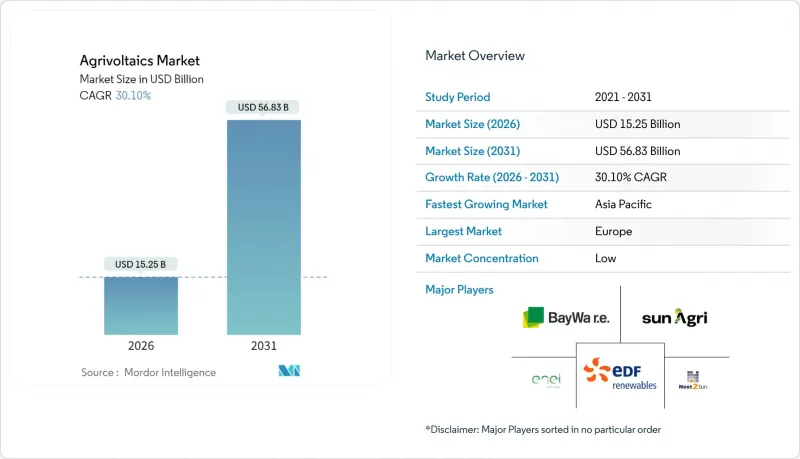

Agrivoltaics market size in 2026 is estimated at USD 15.25 billion, growing from 2025 value of USD 11.72 billion with 2031 projections showing USD 56.83 billion, growing at 30.1% CAGR over 2026-2031.

This trajectory stems from a fundamental shift in land-use economics: dual revenue streams from crops and electricity now warrant a 15-25% capital premium over conventional solar. Asia-Pacific holds 69.19% of 2024 revenue after China deployed more than 500 projects that integrate aquaculture, field crops, and livestock at a commercial scale. Europe accelerates under mandates that prohibit utility-scale arrays on productive farmland yet exempt elevated dual-use systems, while North America fast-tracks multi-gigawatt ventures that preserve farming operations. Bifacial modules, fixed-tilt racking, and ground-mounted layouts dominate current rollouts, but dynamic trackers, greenhouse roofs, and semi-transparent laminates are growing rapidly as precision agriculture data quantifies yield gains and water savings that conventional photovoltaics cannot deliver.

Dedicated feed-in tariffs guarantee cash flows that offset the 15-20% capital premium over ground-mount arrays. Italy's incentive covering 1.04 GW by 2026 catalyzes farmer-led ventures rather than pure-utility procurement. France followed with a 450 MW cooperative project driven by 35 growers. Japan's 2040 renewables road map prioritizes rooftop and agrivoltaic capacity, reinforcing long-run policy visibility. Early projects create performance data that lowers subsequent risk premiums, creating a virtuous adoption cycle across Europe and Asia-Pacific.

Global bifacial module costs have fallen 25-30% since 2024, raising energy density without raising land costs. Yield gains of 15-25% over monofacial panels, enhanced by snow albedo in cold climates, strengthen project economics. China's 200 GW of 2024 bifacial capacity underpins further price compression, and vertical bifacial arrays in the United Kingdom show 25.38% output gains over tilted systems. The cost trajectory suggests grid-parity agrivoltaics within three to five years, even in high-value farmland.

Elevated mounting structures and wider row spacing raise project capex by 15-25% versus ground-mount solar. Financing hurdles persist as lenders gauge combined crop and power revenues, although German analyses show diversified annual profits of EUR 15,000-235,000 by farm scale. Learning-curve savings from bifacial and tracking adoption are expected to reach parity by 2027.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fixed-tilt arrays held 69.62% of the agrivoltaics market share in 2025, due to their simplicity and durability. Dynamic trackers are growing at a 31.25% CAGR as hardware premiums narrow to 8-12%; they optimize sun angles and offer variable shading for frost-prone orchards. Fraunhofer ISE's lightweight, crop-mounted modules signal next-generation designs that align with precision-farming equipment. Dynamic installations are already serving high-value segments, such as berries and lettuce, and market models suggest they can reach a 35-40% share by 2030.

Fixed configurations still dominate grassland grazing, where uniform shade enhances forage quality without seasonal adjustments. As tracker O&M costs decrease and real-time agronomic control expands, producers expect a balanced design mix that tailors panel mobility to specific crop or livestock requirements, further reducing the capital gap for the agrivoltaics market.

Bifacial modules commanded 74.52% of 2025 shipments and are advancing at 31.02% CAGR. Mass production in China and the rapid diffusion of vertical racking enable bifacial arrays to harvest light from the rear side, such as from crop canopies, soil, or snow, thereby increasing kWh per hectare without requiring additional land. UK field tests record 7.87% higher daily output than vertical monofacial setups and 25.38% better than tilted monofacial baselines, validating the performance edge.

Monofacial panels remain in low-albedo areas, but parity pricing may flip all new agrivoltaic capacity to bifacial by 2028. Semi-transparent laminates, which deliver 5-5.5% light utilization efficiency, are gaining traction for greenhouses, balancing PAR light needs with electrical autonomy. Technology roadmaps foresee tandem perovskite-silicon bifacial cells, enabling module efficiencies of over 30%, thereby amplifying the agrivoltaics market size advantage per acre.

The Agrivoltaics Market Report is Segmented by System Design (Dynamic Panel and Fixed Panel), Technology (Monofacial, Bifacial, and Translucent), Crop (Fruits, Vegetables, and Others), Placement (Greenhouses, Ground Mounted, and Shading Nets), Application (Grassland Farming, Horticulture and Arable Farming, Indoor Farming, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Asia-Pacific retained 68.70% of global revenue during 2025, propelled by China's 500-plus operational sites spanning aquaculture, rice paddies, and goat pastures. Shandong's fish-pond systems increased shrimp yields by 50% while converting idle water surfaces into power plants. Japan mandates dual-use models to achieve its 40-50% renewable electricity goal by 2040, financing sheltered rooftop and farmland arrays. India's low-cost steel canopies suit smallholder plots, while South Korea quantifies biofuel potential from agri-PV integration.

Europe is the fastest-growing region at a 31.60% CAGR. Italy's ban on ground-mount solar panels over fertile soil, coupled with a EUR 1.7 billion incentive fund, is funneling developers into agrivoltaics. France's Terr'Arbouts, covering 7 km2 with 35 farmer partners, and Germany's SUNfarming-SPIE 753 MW park illustrate scale readiness. Snow-rich Nordic nations exploit bifacial rear-side gains during low-sun winters, reinforcing continental momentum.

North America scales via mixed-use mega-sites. Ohio's 800 MW solar-plus-300 MW storage complex reserves two-thirds of the acreage for crops, signaling regulatory acceptance. Vermont's vertical design retains 90% farmland utility. The Federal LASSO Prize funding combines cattle grazing with solar energy, and the USDA-DOE research alliance generates agronomic datasets that mitigate risk and increase capital inflows. Mexico's indigenous pilot arrays demonstrate that agrivoltaics can reduce diesel pump costs and enhance maize yields in marginalized communities.

South America and the Middle East & Africa remain nascent. Colombia's early-stage sites and Qatar's semi-transparent lettuce greenhouses highlight exploratory but promising footholds. These regions may experience cost declines post-2027, mirroring the diffusion curves of rooftop solar.