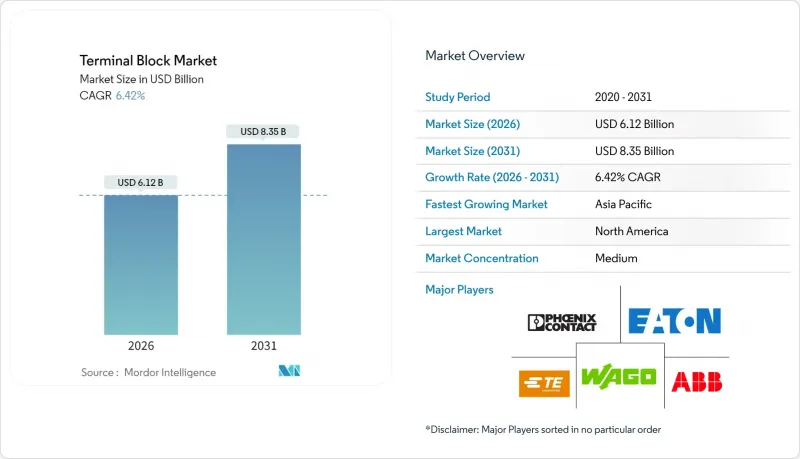

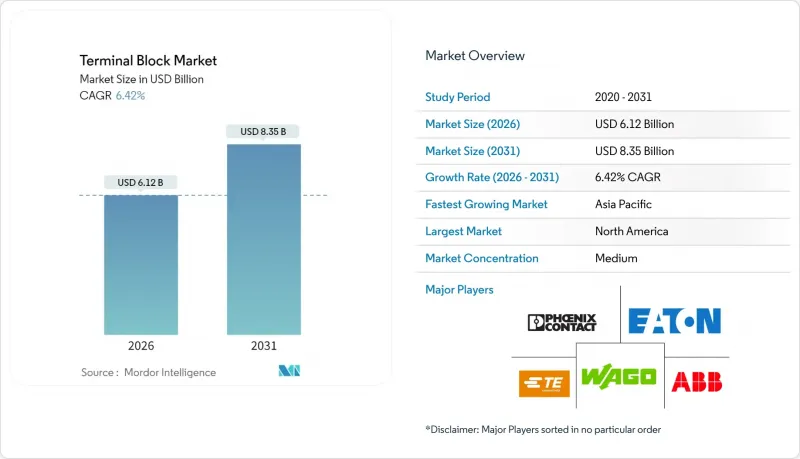

단자대 시장은 2025년에 57억 5,000만 달러로 평가되었으며, 2026년 61억 2,000만 달러에서 2031년까지 83억 5,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 6.42%로 예상됩니다.

산업 자동화의 급속한 확산, 재생에너지 인프라의 확대, 가속화되는 건물 전기화 프로그램이 이러한 성장을 뒷받침하고 있으며, 터미널 블록 시장은 세계 전기화 추세의 주요 수혜자로 자리매김하고 있습니다. 모듈식 배선 아키텍처와 센서가 풍부한 생산 환경의 결합으로 고밀도 피드스루 블록 및 센서/액추에이터 블록에 대한 수요가 증가하고 있습니다. 재생에너지 분야에서는 1,500V 정격의 고전압 직류 블록의 채택이 촉진되고 있으며, 북미와 유럽의 빌딩 자동화 개보수 분야에서는 설치 시간을 단축하고 유지보수를 용이하게 하는 컴팩트한 DIN 레일 솔루션이 선호되고 있습니다. 한편, 구리-알루미늄 가격 변동과 위조부품 리스크는 기존 공급업체들의 이익 확대를 억제하고 있습니다. 그러나 기존 브랜드들은 배선 작업을 줄이고 스마트 팩토리의 재구성을 지원하는 푸시-인-플러그인(Push-in, Plug-in) 설계를 통한 혁신을 지속하며 단자대 시장에서의 경쟁력을 유지하고 있습니다.

제조업체들은 유연성이 높고 센서가 풍부하게 탑재된 운영을 실현하기 위해 생산라인을 재설계하고 있으며, 신속한 배선 변경이 요구되고 있습니다. 피닉스 컨택트사는 이러한 스마트 팩토리 도입을 지원하기 위해 자동화 물류에 1억 유로를 투자했습니다. 바이드뮬러가 도입한 모듈식 사이드 엔트리 푸시인 블록은 연결 시간을 50% 단축하고, 다운타임 없이 라인 재구성을 가능하게 합니다. 제어반 제조업체는 조립 주기 단축과 숙련된 노동력 절감의 이점을 누리고 있으며, 단자대 시장은 인더스트리 4.0 아키텍처의 핵심 동력으로 강화되고 있습니다. IO-Link 및 기타 장치 레벨 네트워크는 제어반 당 I/O 포인트 수를 더욱 증가시켜 센서/액추에이터 블록의 수주를 촉진하고 있습니다. 아시아태평양과 유럽에서 자동화 플랜트가 확산됨에 따라 모듈식 배선 연결 밀도에 대한 수요는 계속해서 주요 촉진요인이 될 것입니다.

전 세계적으로 태양광 및 풍력발전 설비가 증가함에 따라 자외선, 진동, 광범위한 온도 변화에 견딜 수 있는 등급의 단자대가 요구되고 있습니다. TE Connectivity는 Harger 인수를 통해 에너지 관련 제품군을 확장하고, 이들 설비에 대한 낙뢰 보호 및 접지 솔루션을 제공하고 있습니다. 배터리 에너지 저장 시스템에는 극성 반전을 방지하는 고전압 직류 블록이 필요합니다. Phoenix Contact의 극성 커넥터는 1,500V 어레이의 이러한 요구 사항을 충족합니다. 송전망 사업자도 간헐적 발전으로 인한 송전을 최적화하기 위해 전류 감지 기능을 통합한 스마트 단자대를 지정하고 있습니다. 이러한 인프라 구축의 추진은 견고하고 모니터링 기능이 있는 연결 하드웨어의 설치 기반을 확대하고, 단자대 시장의 수익 전망을 강화할 수 있습니다.

2025년 초, 구리 가격은 톤당 1만 달러를 넘어 전도성 금속을 많이 소비하는 블록 제조업체의 이윤을 압박했습니다. 알루미늄 비용의 급등은 대면적 전력 블록에도 추가적인 부담을 주고 있습니다. 계약상 금속 가격 조항에 따라 일부 비용은 구매자에게 전가되지만, 경쟁 입찰로 인해 완전한 회수가 제한되어 단자대 시장 전체의 순이익률이 억제되고 있습니다. 공급업체들은 위험을 줄이기 위해 구리 피복 알루미늄이나 도체 질량 감소 설계를 모색하고 있지만, 인증 주기의 지연으로 인해 급속한 보급을 방해하고 있습니다.

2025년 기준, 피드스루 블록은 단자대 시장 규모의 35.92%를 차지하며, 공장 및 기계설비에서 전력 분배의 기반이 되는 커넥터 역할을 하고 있습니다. 견고한 스크류 클램프 설계로 다양한 도체 크기에 대응할 수 있어 OEM용 표준 카탈로그 제품으로 자리매김하고 있습니다. 한편, 센서/액추에이터 블록은 상태 모니터링 및 예지보전을 위한 분산형 I/O 도입에 따라 8.28%의 가장 빠른 CAGR을 기록했습니다. 단위 길이당 높은 접점 밀도는 캐비닛의 소형화 목표에 부합합니다. 배리어 블록 및 패널 블록은 에너지 및 철도 애플리케이션의 고전압 및 안전 요구 사항을 충족하는 반면, 퓨즈 차단 유형은 회로 보호 기능을 통합하고 보호 기능 내에 연결성을 추가적으로 통합합니다. 열전대 블록과 LED 상태 블록은 신호 처리와 배선을 통합한 애플리케이션 특화 설계로의 전환을 보여줍니다.

피드스루의 우위는 지속될 것이며, IIoT 도입으로 인한 센서 포인트의 증가에 따라 그 우위는 약간 감소할 것으로 예상됩니다. 이에 각 제조사들은 공간 절약성과 빠른 교체성을 겸비한 다단식 및 탈착식 센서 블록으로 제품 라인을 확장하고 있습니다. 이러한 추세는 제품 구성의 변화를 촉진하고, 단자대 시장 전체의 평균 판매 가격 상승과 수익 성장을 뒷받침하고 있습니다.

DIN 레일 블록은 세계 표준화와 현장 서비스 편의성으로 인해 2025년 단자대 시장 점유율 54.78%를 차지할 것으로 예상됩니다. 스냅온 설계로 개조 및 확장을 간소화하여 패널 제작자 간 재고의 공통성을 유지합니다. PCB 실장 솔루션은 현재 소형화, 드라이브, 전원장치, IoT 엣지 노드에서 소형화된 어셈블리에 대응하기 위해 7.16%의 CAGR로 성장하고 있습니다. 픽앤플레이스 호환성을 통해 고속 SMT 라인이 가능하여 단가를 높이면서 총 제품 비용을 절감할 수 있습니다. 진동 차단 및 고전류 지연이 필요한 중장비 인클로저의 경우, 패널 장착형 및 직접 부품 실장형 변형이 계속 채택되고 있습니다.

전자기기의 통합이 진행됨에 따라 PCB 설계는 양산성과 복잡성 측면에서 확대되고, 더 많은 혼합 신호 블록이 기판에 집적됩니다. 그러나 서비스 엔지니어들은 여전히 DIN 레일 레이아웃을 선호하는데, 이는 다운타임 위험과 배선 복잡성 때문에 모듈성이 정당화되기 때문입니다. 이러한 공존 관계는 단자대 시장 내 건전한 부문 다양성을 뒷받침하고 있습니다.

북미는 2025년 단자대 시장 매출의 41.38%를 차지할 것으로 예상되며, 항공우주, 자동차, 공정 산업에서 탄탄한 제조 기반이 이를 뒷받침하고 있습니다. 전력망 현대화와 멕시코에 대한 니어쇼어링으로 안정적인 캐비닛 수요를 확보했습니다. UL 1059 표준은 프리미엄 인증 블록에 대한 선호도를 강화하고 평균 가격을 유지합니다. 그러나 설치 기반이 성숙해짐에 따라 성장이 둔화되고 있기 때문에 공급업체들은 리노베이션 중심의 업그레이드와 스마트 캐비닛 솔루션에 초점을 맞추고 있습니다.

아시아태평양은 중국의 전자제품 생산과 지역 전기화 프로그램의 혜택을 받아 2031년까지 CAGR 7.05%로 성장할 것으로 예상됩니다. 중국 국내 업체들은 원가 경쟁력 있는 PCB 블록을 공급하고 있지만, 신뢰성이 요구되는 분야에서는 세계 OEM 업체들이 품질 면에서 우위를 점하고 있습니다. 인도와 아세안의 인프라 구축이 배전 및 공장 자동화 분야에서 DIN 레일 채택을 촉진하고 있습니다. 그러나 이 지역에서의 모조품 확산은 지적재산권 보호의 과제가 되고 있으며, 단자대 시장의 하위 계층의 가격 압축 요인으로 작용하고 있습니다.

유럽은 독일이 인더스트리 4.0을 주도하며 기술적으로 선도적인 위치를 유지하고 있습니다. EU 그린딜에 따른 풍력, 태양광, 에너지 저장에 대한 투자가 열악한 환경용 블록에 대한 수요를 불러일으키고 있습니다. 바이드뮬러의 11억 2천만 유로의 매출과 중국 내 생산능력 확대는 세계화된 유럽의 경쟁력을 입증하고 있습니다. 동유럽은 새로운 생산능력 구축의 잠재력을 가지고 있는 반면, 브렉시트는 영국의 물류를 복잡하게 만들고 있습니다. 중동 및 아프리카는 규모는 작지만, 스마트 그리드와 산업 다각화를 꾸준한 보급의 촉매제로 보고, 단자대 시장을 신흥 인프라 프로젝트로 확대시키고 있습니다.

The terminal block market was valued at USD 5.75 billion in 2025 and estimated to grow from USD 6.12 billion in 2026 to reach USD 8.35 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031).

Rapid adoption of industrial automation, expanding renewable-energy infrastructure, and accelerating building electrification programs underpin this advance, positioning the terminal block market as a core beneficiary of global electrification trends. Convergence of modular wiring architectures with sensor-rich production environments is lifting demand for high-density feed-through and sensor/actuator blocks. Renewable-energy applications are fuelling the uptake of high-voltage DC blocks rated to 1,500 V, while building-automation retrofits in North America and Europe favour compact DIN-rail solutions that shorten installation time and ease servicing. At the same time, copper and aluminium price swings and counterfeit component risks temper margin expansion for established suppliers. Nonetheless, established brands continue to innovate with push-in and pluggable designs that cut wiring labour and support smart-factory re-configurability, sustaining competitiveness within the terminal block market.

Manufacturers are re-engineering production lines for flexible, sensor-rich operations that demand fast-change wiring. Phoenix Contact invested EUR 100 million in automated logistics to support such smart-factory deployments. Modular side-entry push-in blocks introduced by Weidmuller cut connection time by 50%, allowing line re-configuration without downtime. Control-cabinet builders gain from shorter assembly cycles and reduced skilled-labour requirements, strengthening the terminal block market as a core enabler of Industry 4.0 architectures. IO-Link and other device-level networks further raise the number of I/O points per cabinet, boosting orders for sensor/actuator blocks. As automated plants proliferate across APAC and Europe, demand for modular wiring connection density will remain a primary catalyst.

Rising global solar and wind installations require terminal blocks rated for UV, vibration, and wide temperature exposure. TE Connectivity broadened its energy portfolio via the Harger acquisition to address lightning protection and grounding for these assets. Battery-energy-storage systems need high-voltage DC blocks that prevent polarity reversal; Phoenix Contact's pole connectors meet that requirement for 1,500 V arrays. Grid operators also specify smart terminal blocks with integrated current sensing to optimise dispatch from intermittent generation. This infrastructure push multiplies install-base growth for rugged, monitored connection hardware, reinforcing revenue visibility for the terminal block market.

Copper prices exceeded USD 10,000 per ton in early 2025, squeezing margins for block makers who consume tonnes of conductive metal. Aluminium cost spikes add pressure on large cross-section power blocks. While metal clauses in contracts pass some costs to buyers, competitive bidding limits full recovery, curbing net profitability across the terminal block market. Suppliers explore copper-clad aluminium and reduced conductor mass designs to mitigate exposure, though qualification cycles slow rapid adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Feed-through blocks accounted for 35.92% of the terminal block market size in 2025, acting as foundational connectors for power distribution across factories and machinery. Sturdy screw-clamp designs allow versatile conductor sizes, preserving their status as baseline catalogue items for OEMs. Sensor/actuator blocks, however, record the fastest 8.28% CAGR as users add distributed I/O to achieve condition monitoring and predictive maintenance. Higher contact density per unit length aligns with cabinet downsizing goals. Barrier and panel blocks fulfill high-voltage and safety mandates in energy and rail applications, while fuse and disconnect variants integrate circuit protection, further embedding connectivity within protective functions. Thermocouple and LED status blocks illustrate the transition toward application-specific designs that merge signal processing with wiring.

Feed-through dominance will persist but marginally erode as IIoT deployments multiply sensor points. Producers therefore broaden lines with multi-level and pluggable sensor blocks that combine space savings with quick swap-out. These dynamics reinforce a product-mix shift that elevates average selling prices and supports revenue growth across the terminal block market.

DIN-rail blocks contributed 54.78% of the terminal block market share in 2025 thanks to global standardisation and field-service convenience. Their snap-on design simplifies retrofits and expansions, keeping inventory commonality across panel builders. PCB-mount solutions, though smaller at present, are climbing at a 7.16% CAGR to address miniaturised assemblies in drives, power supplies, and IoT edge nodes. Pick-and-place compatibility enables high-speed SMT lines, shrinking total product cost despite premium unit pricing. Panel-mounted and direct-component variants continue in heavy-duty enclosures where vibration isolation or high-current lugs are needed.

Continued electronics convergence means PCB designs will gain both volume and complexity, pulling more mixed-signal blocks onto boards. However, service engineers still favour DIN-rail layouts where downtime risk and wiring complexity justify modularity. This coexistence supports healthy segment diversity inside the terminal block market.

The Terminal Block Market Report is Segmented by Product Type (Feed-Through Terminal Blocks, Barrier/Panel Terminal Blocks, and More), Mounting Method (DIN-Rail Mounted, PCB-Mounted, and More), Connection Technology (Screw Clamp, Spring Clamp, and More), End-User Industry (Industrial Controls and Automation, Power and Energy, Telecom and Data-Com, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 41.38% of terminal block market revenue in 2025, anchored by established manufacturing in aerospace, automotive, and process industries. Grid-modernisation and near-shoring to Mexico secure stable cabinet demand. UL 1059 standards reinforce preference for premium certified blocks, sustaining average prices. Growth nonetheless moderates as the installed base matures, so vendors focus on retrofit-driven upgrades and smart-cabinet solutions.

Asia-Pacific is projected to grow at a 7.05% CAGR through 2031, benefiting from Chinese electronics production and regional electrification programs. Local makers in China supply cost-competitive PCB blocks, but global OEMs maintain quality leadership in segments demanding reliability. India and ASEAN infrastructure drives DIN-rail adoption in power distribution and factory automation. The region's counterfeit prevalence, however, challenges intellectual-property protection and compresses pricing in lower tiers of the terminal block market.

Europe remains technologically advanced, led by Germany's Industry 4.0 rollouts. EU Green Deal investments in wind, solar, and energy storage raise demand for harsh-environment blocks. Weidmuller's EUR 1.102 billion turnover and China capacity expansion underline globalised European competitiveness. Eastern Europe offers fresh capacity-build potential, while Brexit complicates UK logistics. The Middle East and Africa, though smaller, view smart-grid and industrial diversification as catalysts for steady adoption, extending the reach of the terminal block market into emerging infrastructure projects.