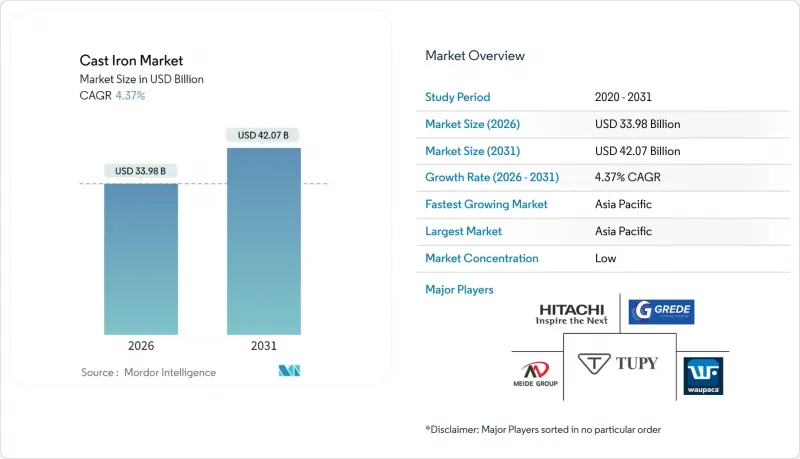

주철 시장은 2025년에 325억 6,000만 달러로 평가되며, 2026년 339억 8,000만 달러에서 2031년까지 420억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 4.37%로 예상됩니다.

이러한 꾸준한 성장은 신뢰성, 가공성, 비용 우위가 경량화 및 신규 합금의 매력을 능가하는 성숙된 산업에서 이 소재의 확고한 입지를 반영합니다. 수요는 진동 감쇠와 열 안정성이 필요한 자동차 브레이크 시스템, 연성 철관 설치, 공작기계 베이스에 의해 지원되고 있습니다. 아시아태평양의 생산능력 투자, 특히 중국의 신규 고로 건설과 인도의 지속적인 증설은 공급을 보장하고 다운스트림 제조업체에 대한 납품 비용을 절감할 수 있습니다. 주조업체들은 풍력 터빈 허브에는 구상흑연주철을, 고압 수소 파이프라인에는 연성주철을 활용하는 등 재생에너지 분야에서도 기회를 포착하고 있습니다. 동시에, 적층제조 기술과 전기로로의 개조는 생산자들이 에너지 소비를 줄이고 지속가능성 지표에서 차별화를 꾀할 수 있도록 돕고 있습니다.

회주철은 열전도율과 감쇠 특성이 반복적인 제동 사이클에서 안전 기준을 충족하므로 로터 재료의 기본값으로 계속 채택되고 있습니다. 컴팩트 흑연 주철(CGI)은 재활용성을 유지하면서 질량을 줄이고, 자동차 제조업체가 배출가스 규제를 충족시키면서 주조 효율을 유지할 수 있도록 도와줍니다. 하이브리드 및 레인지 익스텐더 파워트레인은 소형화되고 고온에 견딜 수 있는 엔진이 더 높은 강도 대 중량비를 요구하는 성장 분야를 추가하고 있습니다. 동시에 전동화의 발전으로 모터 하우징, 배터리 팩 구조 프레임 등 주철의 새로운 용도가 생겨나면서 기존 엔진 수요가 줄어든 이후에도 금속 주문이 지속될 것으로 예측됩니다.

정부의 인프라 계획에 따라 상하수도 시설 개보수를 위한 연성철관 채택이 가속화되고 있습니다. 100년의 수명과 완벽한 재활용성을 갖춘 이 소재의 특성을 높이 평가하고 있기 때문입니다. 미국 주철관 회사가 2억 8,500만 달러를 투자한 용광로 현대화를 통해 용해 능력을 25% 향상시키는 동시에 CO2 배출량을 62% 감소시킴. 이를 통해, 유틸리티 사업자가 탈탄소화 목표를 훼손하지 않고 주철을 지정할 수 있다는 것을 보여주었습니다. 신흥 국가에서는 초기 비용보다 수명주기 비용 절감을 중시하는 경향이 강해져, 주철의 내구성이 초기 투자비용을 상쇄하는 배수설비, 교량 지대, 건축 파사드 분야에서 수요가 견고합니다. 이러한 모멘텀은 중동 및 라틴아메리카의 상수도 유틸리티에도 영향을 미쳐 북미의 주택 착공률 둔화를 상쇄하고 있습니다.

기존 고로에서는 용선 1톤당 약 0.6톤의 코크스를 소비하므로 주조공장은 변동하는 석탄 수입가격과 탄소세의 영향을 받기 쉽습니다. 유럽 사업은 전력 요금과 지정학적 불확실성으로 인해 비용 기반이 상승하여 가장 큰 부담을 안고 있습니다. 이로 인해 일부 소규모 파운드리 업체들은 조업을 중단하거나 문을 닫아야 하는 상황에 처해 있습니다. 코크스 건식 담금질 시스템이나 바이오차 대체는 열 손실과 탄소 강도를 감소시키지만, 대규모 생산자만이 상각할 수 있는 막대한 자본 지출이 필요합니다. 재생에너지 가격이 하락하고 고로 개조가 보급되기 전까지는 에너지가 이익률의 발목을 잡아 저비용 지역으로 생산 이전을 유도할 수 있습니다.

2025년 기준 회주철은 주철 시장 점유율의 47.12%를 차지할 것으로 예상되며, 열전도율과 진동 흡수 특성에 의존하는 브레이크 로터, 엔진 하우징, 공작기계 베드 응용 분야가 그 기반이 되고 있습니다. 하드 레이저 표면처리를 통한 내마모성 향상으로 연삭설비 및 농업용 경운공구 분야에서 수요 증가가 예상됩니다.

전기 피팅 및 수공구용 가단주철 수요 증가로 CAGR 4.84%를 유지하는 한편, 높은 인장강도와 연신율이 요구되는 수도 인프라 및 풍력발전용 주물 분야에서는 연성주철의 점유율이 확대되고 있습니다. 내마모성 광산 라이너용 백주철은 틈새 시장을 유지하고 있으며, CGI(용융주철)는 OEM(Original Equipment Manufacturer)의 피로 특성 검증이 진행됨에 따라 점진적으로 확대되는 추세입니다.

아시아태평양은 2025년 전 세계 생산량의 38.45%를 공급하며 5.12%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 이 지역의 주철 시장은 광석 채굴, 코크스로 및 다운스트림 가공을 통합한 고밀도 밸류체인 클러스터에 의해 지원되고 있습니다. 허베이성과 산둥성에 신설된 고로는 고상압력-산소가 풍부한 설계를 채택하여 기존 설비보다 10-12% 적은 코크스 소비량을 실현했습니다. 유럽 제조업체와의 에너지 효율 격차를 줄이고 있습니다. 필리핀을 필두로 동남아시아에서는 연간 철강 소비량을 1,000만 톤 규모로 끌어올리기 위한 인프라 계획이 속속 발표되고 있습니다.

북미에서는 자동화 기술 리더십과 연방정부의 우대정책이 맞물려 핵심 부품의 국내 회귀가 진행되고 있습니다. 미국주조협회 회원사가 1,050개사를 돌파한 것은 생산능력 갱신과 숙련공 확보의 순풍이 불고 있음을 보여줍니다. 공정의 디지털화와 3D 샌드 프린팅 기술로 인해 지역 제조업체들은 방위 및 항공우주 분야, 고부가가치 및 단납기 EV 부품 등 고매출을 창출할 수 있는 분야에서 민첩성을 발휘하고 있습니다. 그러나 스미스 주조소 등 엄격한 배출 규제로 인해 폐쇄된 사례는 컴플라이언스 비용과 경쟁력 확보의 균형을 맞출 필요성을 강조하고 있습니다.

유럽에서는 에너지 공급 쇼크에 따라 코크스 부족을 보완하기 위해 전기로화 및 바이오차르 시험이 진행되고 있습니다. 2024년 겉보기 철강 소비량은 2.3% 감소할 것으로 예상되며, 건설업은 7분기 연속 감소세를 보이고 있습니다.

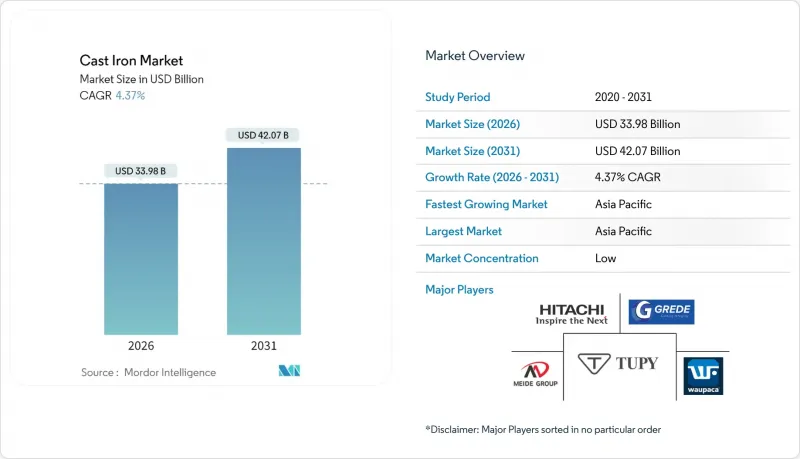

The Cast Iron Market was valued at USD 32.56 billion in 2025 and estimated to grow from USD 33.98 billion in 2026 to reach USD 42.07 billion by 2031, at a CAGR of 4.37% during the forecast period (2026-2031).

This steady growth reflects the material's entrenched role in mature industries where reliability, machinability, and cost advantages continue to outweigh the appeal of lighter or novel alloys. Demand is underpinned by automotive brake systems, ductile iron pipe installations, and machine-tool bases that require vibration damping and thermal stability. Capacity investments in Asia Pacific, particularly new blast furnaces in China and ongoing expansions in India, safeguard supply and lower delivered costs for downstream manufacturers. Foundries are also capturing opportunities in renewable energy, leveraging spheroidal graphite iron for wind-turbine hubs and ductile iron for high-pressure hydrogen pipelines. At the same time, additive manufacturing and electric furnace retrofits help producers trim energy intensity and differentiate on sustainability metrics.

Gray iron continues as the default rotor material because its thermal conductivity and damping characteristics match safety standards under repetitive braking cycles. Compact graphite iron (CGI) reduces mass without sacrificing recyclability, helping automakers meet emissions rules while retaining casting efficiencies. Hybrid and range-extender powertrains add growth avenues where downsized, high-temperature engines demand higher strength-to-weight ratios. Concurrently, electrification shifts spur novel cast iron applications in motor housings and battery-pack structural frames, sustaining metal orders long after traditional engine content recedes.

Government infrastructure programs accelerate ductile iron pipe uptake for water and wastewater upgrades, attracted by the material's 100-year service life and full recyclability. AMERICAN Cast Iron Pipe Company's USD 285 million furnace modernization raises melting capacity by 25% while cutting CO2 emissions 62%, signalling that utilities can specify cast iron without compromising decarbonization goals. Emerging economies prioritize lifecycle savings over initial cost, reinforcing demand in drainage, bridge bearings, and architectural facades where cast iron's durability offsets higher upfront spend. The momentum cascades into Middle East and Latin America water projects, balancing softer North American housing starts.

Traditional blast furnaces consume nearly 0.6 tons of coke per ton of hot metal, exposing foundries to volatile coal import prices and carbon taxes. European operations shoulder the heaviest burden as power tariffs and geopolitical uncertainty elevate cost bases, prompting some small foundries to idle or close. Coke dry quenching systems and biochar substitution cut thermal losses and carbon intensity but demand sizable capital outlays that only large producers can amortize. Until renewable electricity prices fall and furnace retrofits scale, energy remains a drag on margins and an incentive for production shifts toward lower-cost regions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Gray iron controlled 47.12% of the cast iron market share in 2025, anchored in brake rotors, engine housings, and machine-tool beds that depend on its thermal conductivity and vibration-damping attributes. Hard-laser surface treatments extend wear life, opening opportunities in crushing equipment and agricultural tillage tools.

Rising malleable iron demand for electrical fittings and hand tools underpins a 4.84% CAGR, while ductile iron gains share in water infrastructure and wind-energy castings that necessitate high tensile strength and elongation. White iron stays niche for abrasion-resistant mining liners, and CGI scales slowly as OEMs validate fatigue properties.

The Cast Iron Market Report is Segmented by Grade (Gray Iron, Ductile Iron, Malleable Iron, & White Iron), Casting Process (Sand Casting, Centrifugal Casting, and More), Application (Automotive and Transportation, Construction and Infrastructure, Industrial Machinery, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific supplied 38.45% of global output in 2025 and is growing at a 5.12% CAGR. Asia Pacific's cast iron market rests on dense value-chain clusters that integrate ore mining, coke ovens, and downstream machining. New furnaces built in Hebei and Shandong use high-top-pressure, oxygen-enrichment designs that consume 10-12% less coke than legacy units, narrowing the energy gap with European producers. Southeast Asia, led by the Philippines, unveils infrastructure pipelines that drive annual steel consumption toward 10 million tons.

North America combines automation leadership with federal incentives to reshore critical components. American Foundry Society membership crossing 1,050 companies indicates capacity renewal and skilled-worker recruitment tailwinds. Process digitization and 3D sand printing give regional producers agility for defense, aerospace, and short-run EV parts that carry premium margins. Yet stringent emission limits closed facilities such as Smith Foundry, underscoring the need to balance compliance costs with competitiveness.

Europe's energy supply shock drives furnace electrification and biochar trials to offset coke shortages. Apparent steel consumption slipped 2.3% in 2024, with the construction industry contracting for seven consecutive quarters.