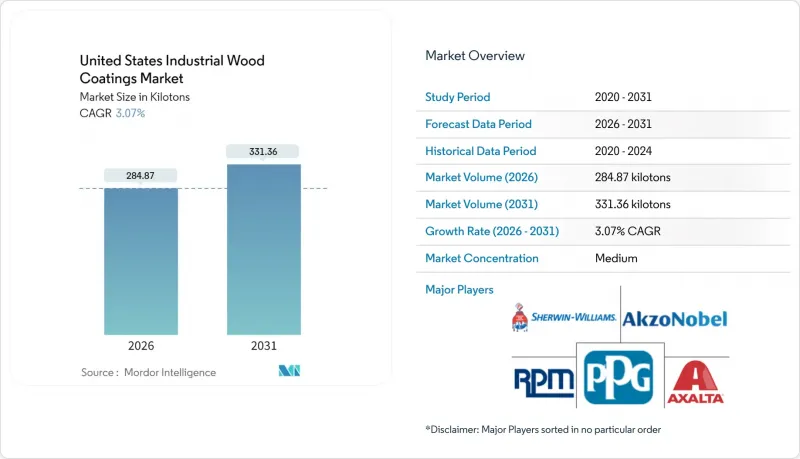

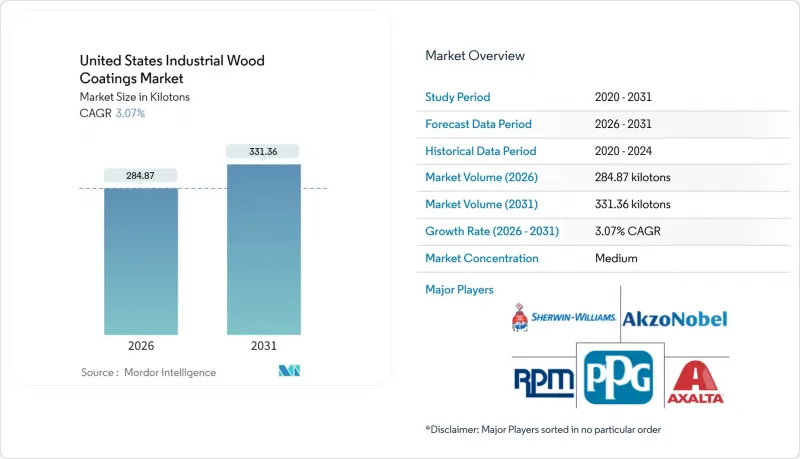

미국의 산업용 목재 코팅 시장은 2025년 276.39 킬로톤에서 2026년에는 284.87 킬로톤으로 성장하여 2026년부터 2031년까지 CAGR 3.07%를 기록하며 2031년까지 331.36 킬로톤에 달할 것으로 예측됩니다.

이러한 꾸준한 확대는 주택 건설의 회복, 가속화되는 임대용 건설 붐, 현장 노동력을 줄이기 위한 공장 도장 마감으로 제조 전환에 기인합니다. 폴리우레탄계 도료는 우수한 내화학성으로 인해 주류를 차지하고 있지만, 수계 대체품에 대한 규제 압력에도 불구하고 용제계 화학제품은 여전히 생산량에서 선두를 유지하고 있습니다. 목공 부품 공급업체는 숙련공 부족을 억제하고 마감의 일관성을 유지하기 위해 로봇 도장 라인과의 원활한 통합을 실현하는 배합을 우선시하고 있습니다. 수지 혁신과 엔드 투 엔드 자동화 지침을 결합한 제조업체는 고객이 성능과 환경 기준을 모두 충족할 수 있도록 보장함으로써 시장 점유율을 확대하고 있습니다. 폴리에스테르 폴리올, 이산화티타늄 등 원자재 관련 이슈는 조달 전략을 시험하는 상황이 지속되고 있으며, 전략적 비축 및 장기 공급 계약 협상을 촉구하고 있습니다.

가구 및 캐비닛 판매 증가가 탑코트, 실러, UV 필러의 견조한 수요를 뒷받침하고 있습니다. 국내 제조업체는 팬데믹으로 인한 운송 혼란 이후 점유율을 확대했습니다. 대형 캐비닛 인클로저 및 임베디드 가전제품 수납으로의 전환으로 인해 내스크래치성 폴리우레탄 층에 대한 수요가 증가하고 있습니다. 주방 리모델링에서는 깊이 있는 색감과 낮은 VOC 적합성을 겸비한 얼룩이 요구되며, 어둡고 저광택의 마감재가 선호되고 있습니다. 수성 폴리우레탄 하이브리드 제품으로 대응하는 공급업체는 2026년 도입 예정인 신규 라인에 대한 입찰을 따냈습니다.

주택 개보수 지출은 2024년에 정점을 찍고, 주택 소유주들은 주방 개조, 맞춤형 목공품, 나무 바닥 재시공에 저축한 돈을 사용했습니다. 캐비닛 교체 주기가 빨라짐에 따라 마감재 수명이 단축되어 공장 도장 코팅 주문이 꾸준히 증가하고 있습니다. 거주 중인 주택에서 작업하는 계약자들은 저취 및 빠른 경화 시스템을 지정하고, 환기 시간을 연장하지 않고도 촉박한 프로젝트 일정에 대응할 수 있는 아크릴계 및 UV 경화형 옵션에 대한 수요가 더욱 확대되고 있습니다.

EPA의 유해 대기 오염 물질 규제에 따라 포름알데히드는 0.20ppm으로 제한되어 물티슈 얼룩에 염화메틸렌 사용을 억제하고 침투 깊이와 발색성 측면에서 타협을 강요하고 있습니다. 캘리포니아주의 추가 방향족 함량 규제는 철저한 제3자 테스트를 의무화하고 있으며, 이는 배합 비용을 증가시키고 있습니다. 컴플라이언스 체제에 한계가 있는 중소기업은 퇴출을 강요받고 있으며, 2027년 이후에는 공급업체 환경이 더욱 통합될 가능성이 높아지고 있습니다.

폴리우레탄계 도료는 2025년 미국 산업용 목재 코팅 시장 점유율의 59.42%를 차지하며 2031년까지 CAGR 3.60%로 확대될 것으로 예상됩니다. 폴리우레탄의 견뢰도는 가구 상판, 문, 계단 부품의 마모 및 화학제품 노출에 대한 요구 사항을 충족합니다. 수성 등급은 현재 투명성과 유동성에서 솔벤트 계열과 동등하게 되어, 엄격한 VOC 규제가 적용되는 주에서 채택이 가속화되고 있습니다.

아크릴계 화학제품은 마모가 적은 인테리어 부품에 대한 비용 효율적인 틈새시장을 유지하고 있습니다. 한편, 알키드 수지는 전통적인 목공 공장에서 여전히 주류이지만, 저취 제품에 시장 점유율을 빼앗기고 있습니다. 폴리에스테르 수지는 고생산성 캐비닛 및 바닥재 공장의 주류 UV 경화 라인의 핵심을 이루고 있습니다. 에폭시 수지는 강력한 내화학성을 필요로 하는 실험실 및 의료용 설비에 공급됩니다. 니트로셀룰로오스 래커는 악기 용도에 한정되어 있으며, 현악기 제작자가 중요시하는 빠른 수리 주기로 인해 그 가치를 유지하고 있습니다.

미국 산업용 목재 코팅 시장 보고서는 수지 유형(에폭시, 아크릴, 알키드, 폴리우레탄, 폴리우레탄, 폴리에스테르, 기타), 기술(수성, 솔벤트 기반, UV 경화형, 분말), 최종사용자 산업(목재 가구, 가구, 가구, 바닥재 및 데크, 기타)으로 분류됩니다. 시장 예측은 톤 단위로 제공됩니다.

The United States Industrial Wood Coatings Market is expected to grow from 276.39 kilotons in 2025 to 284.87 kilotons in 2026 and is forecast to reach 331.36 kilotons by 2031 at 3.07% CAGR over 2026-2031.

This steady expansion follows the recovery of residential construction, the accelerating build-to-rent boom, and a shift in manufacturing toward factory-applied finishes that reduce job-site labor requirements. Polyurethane systems dominate due to their superior chemical resistance, while solvent-borne chemistries still lead in volume, despite regulatory pressure favoring water-borne alternatives. Millwork suppliers are prioritizing formulations that integrate smoothly with robotic spray lines to curb skilled-labor shortfalls and maintain finish consistency. Manufacturers that pair resin innovations with end-to-end automation guidance are carving out share by ensuring customers meet both performance and environmental benchmarks. Challenges with raw materials, such as polyester polyols and titanium dioxide, continue to test procurement strategies, prompting strategic stockpiling and the negotiation of long-term supplier contracts.

Furniture and cabinetry increased sales, underpinning robust volume pull for topcoats, sealers, and UV fillers. Domestic makers gained ground after the pandemic's shipping snarls, and their shift toward larger cabinet carcasses and integrated appliance housing heightens the requirements for scratch-resistant polyurethane layers. Kitchen remodel projects now favor dark, low-gloss looks, demanding stains that balance deep color with low-VOC compliance. Suppliers responding with water-borne polyurethane hybrids are winning bids for new lines set to launch in 2026.

Home-improvement outlays peaked in 2024 as owners funneled savings into kitchen refits, custom millwork, and hardwood refinishing. Faster cabinet replacement cycles shorten finish lifespans, keeping orders for factory-applied coatings on a steady climb. Contractors working in occupied homes specify low-odor, rapid-cure systems, steering more volume to acrylic and UV-curable options that meet tight project schedules without extended ventilation times.

EPA caps on hazardous air pollutants restrict formaldehyde to 0.20 ppm and curb the use of methylene chloride in wipe stains, forcing compromises in penetration depth and color build. California's additional aromatic content rules require exhaustive third-party testing, which inflates formulation costs. Smaller regional companies with limited compliance teams face exit decisions, raising the likelihood of a more consolidated supplier landscape after 2027.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polyurethane systems accounted for 59.42% of the United States industrial wood coatings market share in 2025, expanding at a 3.60% CAGR toward 2031. The robustness of polyurethane meets the demands of abrasion and chemical exposure on furniture tops, doors, and stair parts. Waterborne grades now match solvent analogs in clarity and flow, accelerating adoption in states with stringent VOC caps.

Acrylic chemistries retain a cost-efficient niche for interior components with lighter wear, while alkyds continue to dominate traditional millwork shops but are losing market share to lower-odor options. Polyester resins form the backbone of UV-curable lines that dominate high-throughput cabinet and flooring plants. Epoxies supply laboratory and healthcare fixtures needing aggressive chemical resistance. Nitrocellulose lacquers, though relegated to musical instruments, preserve value through fast repair cycles valued by luthiers.

The United States Industrial Wood Coatings Market Report is Segmented by Resin Type (Epoxy, Acrylic, Alkyd, Polyurethane, Polyester, and Others), Technology (Water-Borne, Solvent-Borne, UV-Curable, and Powder), and End-User Industry (Wooden Furniture, Joinery, Flooring and Decking, and Others). The Market Forecasts are Provided in Terms of Volume (Tons).