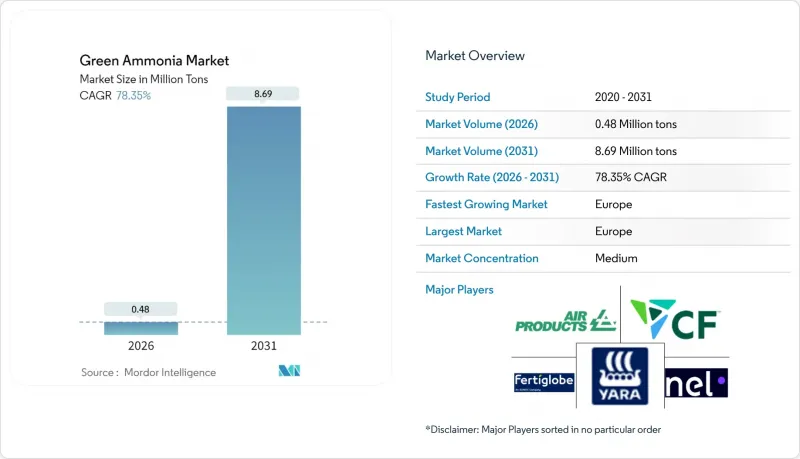

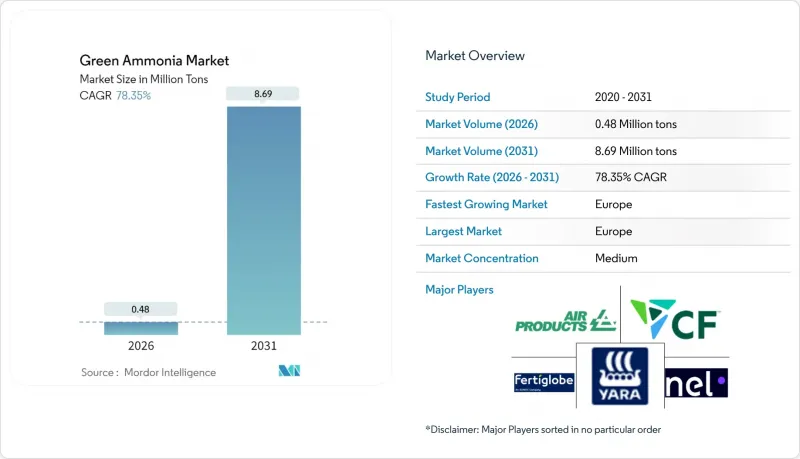

2026년 그린 암모니아 시장 규모는 48만 톤으로 추정되며, 2025년 27만 톤으로부터 성장이 전망됩니다.

2031년에는 869만 톤에 달할 것으로 예측되고 있으며, 2026-2031년에 CAGR 78.35%로 확대할 전망입니다.

유럽, 일본, 인도의 정책적 지원 강화, 자원이 풍부한 지역의 재생 전력 비용이 1kWh당 0.02달러대로 떨어지고, 비료와 무탄소 연료라는 그린 암모니아의 이중적 유용성이 결합되어 보급이 가속화되고 있습니다. 해운 분야의 탈탄소화 의무, 특히 유럽연합(EU)이 2024년부터 해운 부문을 배출권거래제(ETS)에 포함시키겠다는 방침에 따라 암모니아 추진 선박에 대한 조기 수요가 창출되고 있습니다. 한편, 독일, 일본, 한국의 수소 전략에서는 그린 암모니아가 주요 수소 운반체로 자리매김하고 있습니다. 프로젝트 차원에서는 재생에너지 발전, 대규모 전기분해, 암모니아 합성을 통합한 플랜트가 규모의 경제를 실현하고 있습니다. 한편, 블루 암모니아와의 경쟁은 계속되고 있지만, 그린 암모니아 시장은 천연가스 가격 변동으로부터의 독립성과 향후 탄소 가격 프리미엄을 기대할 수 있다는 장점이 있습니다.

개발도상국에서는 비료 수입 의존도를 낮추고 식량안보 강화를 위해 그린암모니아의 국내 생산을 우선시하고 있습니다. 러시아·우크라이나 분쟁으로 인해 기존 비료 무역의 취약성이 드러나자 케냐, 나이지리아 등 국가들은 공급망 안정화를 위해 기가 와트 규모의 재생에너지에서 암모니아로 전환하는 프로젝트를 발표했습니다. 아프리카 연합의 2063년 탄소중립 목표는 풍력-태양광 자원과 소규모 농민 협동조합을 연결하는 민관 협력 사업을 촉진하고 있습니다. 다자간 금융기관은 지속가능한 비료 프로그램에 23억 달러를 배정하고, 전기분해 시설에 대한 우대 대출을 촉진하고 있습니다. 태양광-풍력 잠재력이 높은 국가에서는 수입 회색 암모니아보다 낮은 납품비용을 실현할 수 있으며, 경쟁 구도가 변화하고 있습니다. 식량 수입 비용이 증가함에 따라 농업부는 비료 정책과 에너지 자립 목표를 통합하려는 움직임을 가속화하고 있으며, 신규 플랜트 자금 조달을 지원하는 오프 테이크 계약 체결을 촉진하고 있습니다. 이러한 모멘텀은 아프리카 및 남아시아 전역의 그린 암모니아 시장 확대에 크게 기여하고 있습니다.

국제해사기구(IMO)의 2050년 배출량 반감 목표와 EU 탄소가격제 확대가 암모니아 연료 도입을 촉진하고 있습니다. 머스크, NYK를 비롯한 해운사들은 암모니아 대응 선박을 발주하여 2030년 이전에 상업운항을 계획하고 있습니다. 일본 경제산업성은 암모니아 엔진에 대한 공동 자금 지원을 통해 발전소의 20% 암모니아 혼소를 의무화함으로써 연료 수요의 중복을 만들어내고 있습니다. 2025년에 발표될 임시 IMO 가이드라인은 안전 프로토콜을 명확히 하고, 로테르담과 싱가포르의 연료 보급 기지에 대한 투자를 촉진할 것입니다. 항만 당국은 연료 보급 인프라와 재생 수소의 백홀 운송을 통합하여 선구자적 우위를 확보하고 지역 클러스터를 강화할 수 있습니다.

전해장치 패키지는 총 설치 비용의 최대 절반을 차지하며, 알칼리식 유닛의 경우 1kW당 800-1,200달러입니다. 연간 100만톤 규모의 그린 암모니아 복합단지에는 500-1,000MW 규모의 전해설비가 필요하며, 하버보쉬 합성설비와 재생에너지 발전설비를 추가하기 전에 4억-12억 달러의 투자가 필요합니다. 지속적인 암모니아 생산을 위해서는 안정적인 재생 전력 또는 축전지 완충 시스템이 필요하며, 이는 자본 지출을 10-15% 증가시킵니다. 프로젝트 파이낸싱은 15-25년 전력 구매 계약 및 제품 판매 계약에 의존하지만, 이러한 계약 형태는 신흥 시장에서는 아직 일반적이지 않습니다. 미국 인플레이션 억제법, 유럽 혁신기금 등의 혜택이 있음에도 불구하고 기술 리스크 프리미엄의 상승으로 균등화 비용이 크게 증가하고 있습니다. 이러한 비용 상승으로 인해 최종 투자 결정이 지연되고 있으며, 이는 그린 암모니아 시장에 심각한 도전이 되고 있습니다.

2025년 기준 농업 부문이 그린 암모니아 시장의 87.25%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 84.1%로 확대될 것으로 예측됩니다. 이 통계는 새로운 에너지 응용 분야가 등장하고 있는 가운데 비료 수요가 여전히 주도적인 위치를 차지하고 있음을 보여줍니다. 식량 불안정 지역에서는 에너지에 의존하지 않는 영양소 솔루션이 요구되고 있으며, 보조금 제도의 조합으로 현지 생산 설비의 회수 기간이 단축되고 있습니다.

선박 연료는 현재 낮은 수준에 머물러 있지만, 확정된 조선 수주와 연료 보급 터미널의 발표는 2028년까지 전환점을 맞이할 것임을 시사하고 있습니다. 일본에서는 화력발전소에서 암모니아 혼소 시험(최대 20%)이 실시되고 있으며, 플랜트 가동률 향상과 단위 비용 절감으로 이어지는 크로스오버 수요를 입증하고 있습니다. 독일과 한국의 수입 전략에 힘입은 수소운반선 분야는 재생에너지 공급기지와 산업 소비지를 연결하는 장거리 운송수단을 제공합니다. 화학원료 및 철강 탈탄화는 틈새 시장이지만 고부가가치 판로를 창출하여 매출구조를 다변화하고, 그린암모니아 산업을 상품 사이클의 변동으로부터 보호합니다.

그린 암모니아 시장 보고서는 용도별(농업, 선박 연료, 발전, 수소 운반체, 기타 용도) 및 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

유럽은 2025년 그린 암모니아 시장 점유율 35.35%, CAGR 84.9%로 선두를 달리고 있으며, 탄소 가격을 내재화하고 재생에너지 함량을 우대하는 종합적인 정책 정합성이 그 기반이 되고 있습니다. 노르웨이의 SkiGA 해상풍력발전에서 암모니아 생산 프로젝트는 연간 10만 톤을 공급하여 통합 밸류체인의 지역 표준을 확립할 것입니다. 독일은 로테르담에 전용 수입 터미널을 설치하여 국내 전해설비 확충을 보완함으로써 산업 사용자를 위한 공급 이중화를 확보하고 있습니다.

아시아태평양은 지역 기여자로서 중요한 역할을 담당하고 있습니다. 일본은 해운과 발전소용 수요를 합쳐 2050년까지 3,000만 톤의 암모니아 수요를 목표로 하고 있습니다. 한편, 중국은 성(省)급 경기부양책으로 다(多)기가와트급(級)의 재생에너지 유래 암모니아 플랜트를 시범적으로 도입하고 있습니다. 한국의 민관연합은 13개 기업과 5개 기관이 생산-수입 물류에서 협력하고 있으며, 인도의 연간 55만 톤 규모의 보조금 제도는 AM Green사의 안드라프라데시주 100만 톤 복합단지 등 메가 프로젝트를 촉진하고 있습니다. 이러한 노력은 지역 전체의 견고한 성장을 지원하고 있으며, 아시아태평양의 시설들은 내수와 수출 모두에 대비하고 있습니다. 북미에서는 인플레이션 억제법에 따른 생산 세액공제의 혜택을 받고 있으며, CF Industries의 루이지애나주 합작법인이 연간 140만 톤의 생산능력을 목표로 하고 있는 것이 그 증거입니다. 중동 및 아프리카은 수출 지향적 허브로 부상하고 있으며, UAE는 독일로 향하는 첫 H2Global 파일럿 선적을 확보하여 장거리 무역의 경제성을 입증했습니다. 브라질 세아라 주에서는 육상 풍력발전과 항구의 근접성을 활용한 여러 프로젝트가 진행 중이며, 남미가 세계 그린 암모니아 시장에서 차지하는 점유율을 확대하고 있습니다. 이들 대륙 전체에서 비교우위는 재생 자원의 부존량, 정책적 인센티브, 수요지까지의 운송 거리 등의 요소에 따라 달라지며, 이는 향후 투자 배분을 결정하는 요인이 될 것입니다.

Green Ammonia market size in 2026 is estimated at 0.48 million tons, growing from 2025 value of 0.27 million tons with 2031 projections showing 8.69 million tons, growing at 78.35% CAGR over 2026-2031.

Intensifying policy support in Europe, Japan and India, falling renewable electricity costs toward USD 0.02 per kWh in resource-rich regions, and the dual utility of green ammonia as fertilizer and carbon-free fuel collectively accelerate adoption. Maritime decarbonization mandates, particularly the European Union's inclusion of shipping in its Emissions Trading System from 2024, create early demand for ammonia-powered vessels, while hydrogen strategies in Germany, Japan and South Korea position green ammonia as a key hydrogen carrier. At the project level, integrated plants that combine renewable generation, large-scale electrolysis and ammonia synthesis are unlocking economies of scale. Meanwhile, competition from blue ammonia continues, yet the green ammonia market benefits from independence from natural-gas volatility and the prospect of future carbon-pricing premiums.

Developing economies are prioritizing domestic production of green ammonia to reduce fertilizer import dependence and strengthen food security. The Russia-Ukraine conflict exposed vulnerabilities in conventional fertilizer trade, prompting Kenya, Nigeria, and similar nations to announce gigawatt-scale renewable-to-ammonia projects to stabilize supply chains. The African Union's 2063 neutrality goals foster public-private ventures that link wind and solar resources to smallholder cooperatives. Multilateral lenders have allocated USD 2.3 billion to sustainable fertilizer programs, channeling concessional finance into electrolysis capacity. Countries with high solar and wind potential can achieve delivered costs that undercut imported gray ammonia, shifting the competitive balance. As food-import bills rise, agricultural ministries increasingly bundle fertilizer policy with energy-independence targets, accelerating offtake agreements that underpin financial close for new plants. This momentum contributes strongly to green ammonia market expansion across Africa and South Asia.

The International Maritime Organization's target to halve emissions by 2050 and the EU carbon-pricing extension are catalyzing ammonia fuel adoption. Maersk, NYK Line, and other carriers have placed orders for ammonia-ready vessels, planning commercial operation before 2030. Japan's Ministry of Economy, Trade and Industry co-funds ammonia engines and mandates 20% ammonia co-firing in power plants, creating overlapping fuel demand. Interim IMO guidelines issued in 2025 clarify safety protocols, triggering investment in bunkering hubs at Rotterdam and Singapore. Port authorities that integrate bunkering infrastructure with renewable-hydrogen backhaul capture early-mover advantages, reinforcing regional clusters.

Electrolyzer packages account for up to half of the total installed cost, at USD 800-1,200 per kW for alkaline units. A 1 million-ton-per-year green ammonia complex demands 500-1,000 MW of electrolyzers, translating to USD 400-1,200 million before adding Haber-Bosch synthesis and renewable generation assets. Continuous ammonia output requires firm renewable power or battery buffer systems, adding 10-15% to capital expenditure. Project finance hinges on 15-25-year power-purchase and offtake contracts-structures still uncommon in emerging markets. Despite incentives like the US Inflation Reduction Act and Europe's Innovation Fund, higher technology risk premiums are significantly increasing the levelized costs. This rise is causing delays in final investment decisions, highlighting a significant challenge for the green ammonia market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Agriculture commanded 87.25% of the green ammonia market share in 2025, and the segment is expanding at an 84.1% CAGR through 2031. The statistic underscores the continued primacy of fertilizer demand even as new energy applications emerge. Food-insecure regions seek energy-independent nutrient solutions, and bundled subsidy schemes shorten payback periods on local production assets.

Marine fuel holds a modest baseline today, yet confirmed shipbuilding orders and bunkering terminal announcements indicate an inflection by 2028. Power generation trials in Japan, co-firing up to 20% ammonia in thermal plants, illustrate crossover demand that raises plant load factors and cuts per-unit costs. The hydrogen-carrier segment, backed by import strategies in Germany and South Korea, offers long-haul linkage between renewable hot-spots and industrial consumption centers. Chemical feedstock and steel decarbonization add niche but premium-valued outlets, broadening the revenue mix and cushioning the green ammonia industry against commodity-cycle volatility.

The Green Ammonia Market Report is Segmented by Application (Agriculture, Marine Fuel, Power Generation, Hydrogen Carrier, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Europe's leadership, with a 35.35% green ammonia market share in 2025 and an 84.9% CAGR, rests on comprehensive policy alignment that internalizes carbon prices and rewards renewable content. Norway's SkiGA offshore-wind-to-ammonia project will supply 100,000 tons per year, setting a regional benchmark for integrated value chains. Germany's dedicated import terminal at Rotterdam complements domestic electrolysis build-out, ensuring redundancy in supply for industrial users.

Asia-Pacific plays a significant role as a regional contributor. Japan targets 30 million tons of ammonia demand by 2050, combining maritime and power-station offtake, while China pilots multi-GW renewable ammonia plants under provincial stimulus packages. South Korea's public-private coalition aligns 13 firms and five institutes around production and import logistics, and India's 550,000-ton annual subsidy scheme catalyzes megaprojects such as AM Green's 1 million-ton complex in Andhra Pradesh. These initiatives collectively underpin strong regional growth, with Asia-Pacific facilities positioned both for domestic uptake and exports. North America benefits from the Inflation Reduction Act's production tax credits, evidenced by CF Industries' Louisiana joint venture targeting 1.4 million tons annual capacity. The Middle East and Africa are emerging as export-oriented hubs; the UAE secured the first H2Global pilot shipment to Germany, validating long-distance trade economics. Brazil's Ceara state aggregates several projects leveraging onshore wind and port proximity, broadening South America's stake in the global green ammonia market. Across these continents, comparative advantage hinges on renewable resource endowment, policy incentives and shipping distances to demand centers, factors that will shape future investment allocation.