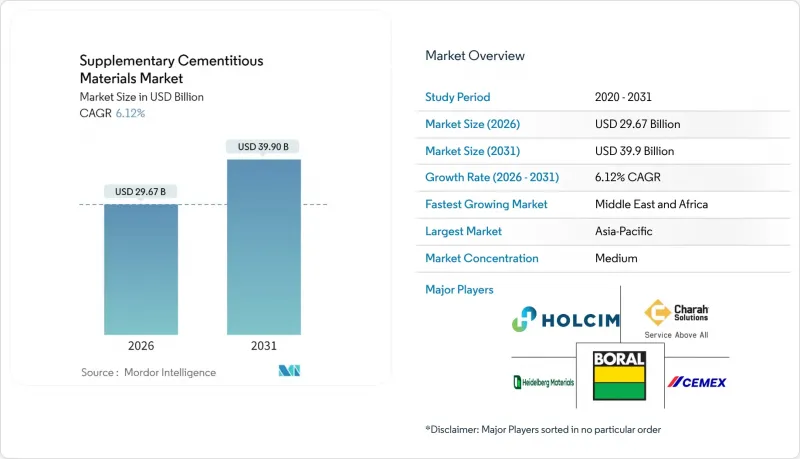

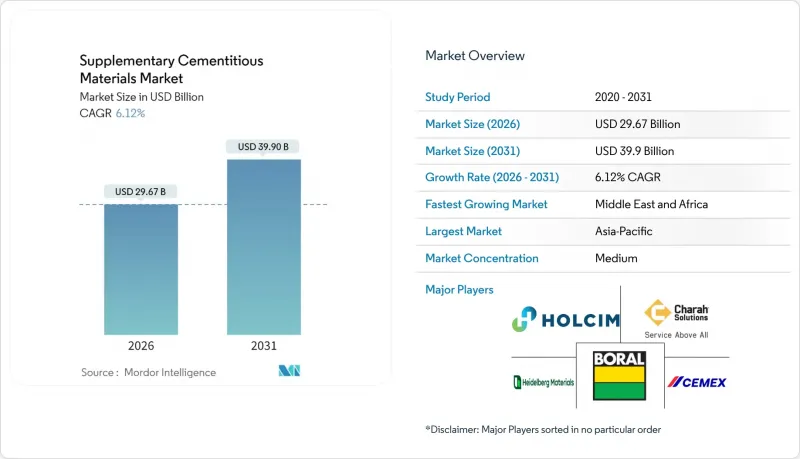

SCM(Supplementary Cementitious Material) 시장은 2025년 279억 6,000만 달러에서 2026년에는 296억 7,000만 달러로 성장하며, 2026-2031년에 CAGR 6.12%로 추이하며, 2031년까지 399억 달러에 달할 것으로 예측되고 있습니다.

이러한 확대는 정부의 탄소가격제 시행과 유틸리티 저탄소 콘크리트 의무화 도입에 따라 건설 업계가 지속가능한 건축 방식으로 빠르게 전환하고 있음을 반영합니다. 사우디의 1조 1,000억 달러 규모의 '비전 2030' 계획과 같은 인프라 투자 프로그램의 가속화는 석탄 연소 제품별 감소에 따라 클링커 함량을 줄여야 하는 시멘트 업계의 과제와 맞물려 보충 시멘트 재료에 대한 지속적인 수요를 창출하고 있습니다. 소성 점토, 화산 포졸란, 석회석 혼합 시멘트와 같은 공급 측면의 기술 혁신은 플라이 애시와 슬래그 공급 감소를 완화하는 동시에 플래시 소성 기술은 가공 에너지 요구 사항을 최대 40%까지 줄여 가용 원료 기반을 확대합니다.

대규모 유틸리티 자금이 보충 시멘트질 재료 시장을 지원하고, 인도의 인프라 자본 지출은 2023-24년 5.7배 증가한 361억 달러, 사우디아라비아의 비전 2030은 1조 1,000억 달러 이상, 아프리카의 인프라 지출은 연평균 930억 달러에 달할 전망입니다. 에 달할 전망입니다. 이 계획은 콘크리트의 시멘트계 보조재(SCM) 대체율 향상을 규정하고 있으며, 시드니 메트로에서는 38-52%의 대체율을 달성하여 프로젝트 전체에서 12만 톤의 CO2 환산 배출량 감축을 달성했습니다. 따라서 건설 수요의 급증은 SCM 수요를 두 배로 늘리고, 공급업체가 플래시칼시너 장비에 대한 투자 및 물류 최적화를 정당화하는 장기 계약을 확보할 수 있게 해줍니다.

규제 압력은 점점 더 강해지고 있습니다. 프랑스의 RE2020은 신축 건물의 탄소 매장량을 640-740kg CO2-e/m2로 제한하고, EU의 탄소국경조정 메커니즘은 수입품에 탄소기준 가격을 부과합니다. 미국에서는 연방정부 자금으로 콘크리트 조달시 환경제품선언(EPD)을 의무화하는 '청정구매법'이 시행되고, 캘리포니아 주에서는 건설자재에 탄소 가격을 적용하고 있으며, 고SCM 배합 콘크리트에 대한 프리미엄 시장이 형성되고 있습니다. 이러한 규제는 탈탄소화 콘크리트를 경제적으로 매력적인 대안으로 만들고, 규제 대응 수단으로서 SCM에 대한 구조적 수요를 고정화시키고 있습니다.

미국의 석탄 화력 발전량은 2010년 이후 60% 감소했으며, 고품질 플라이 애시 공급량이 급감하고 있습니다. 한편, 제철업체들이 전기로로 전환함에 따라 고로 슬래그 공급량도 감소하는 추세입니다. 잔재재 더미에는 40-60%의 가격 프리미엄이 붙고, 운송 거리도 길어지기 때문에 비용 우위가 훼손되고 있습니다. 따라서 콘크리트 제조업체는 대체 SCM을 중심으로 배합 설계를 재검토하거나 더 높은 원료 비용을 지불해야 하며, 새로운 공급원이 성숙할 때까지 단기적인 성장은 제한적일 것입니다.

플라이 애시는 석탄 화력 발전의 감소에도 불구하고 잘 구축된 물류 네트워크와 예측 가능한 포졸란 특성에 힘입어 2025년 시멘트계 혼화제 시장에서 41.72%의 점유율을 차지할 것으로 예측됩니다. 슬래그 시멘트(GGBFS)는 고로 생산량 축소가 지속되는 가운데 고성능 콘크리트 분야에 공급되며, 이를 이어갑니다. 한편, 소성 점토는 플래시 칼시너 장비의 보급으로 CAGR 6.88%로 확대되고 있습니다. 이를 통해 에너지 비용을 절감하고, 카올린 광석 함량이 15-25%인 점토도 경제적으로 처리할 수 있게 되었습니다. 이러한 성장 궤도에 따라 소성 점토는 감소하는 석탄 유래 원료의 주요 대체품으로 자리매김하여 지역 공급 포트폴리오를 재구성하고 풍부한 광상을 배경으로 신규 시장 진출기업을 유치하고 있습니다.

각 제조업체들은 초정밀 입자 크기 제어가 가능한 전용 소성 및 분쇄 공장에 자본을 집중 투입하고 있으며, 포졸란 반응지수를 800mg Ca(OH)2/g 이상으로 높여 프리미엄 가격을 실현하고 있습니다. 실리카퓸과 고반응성 메타카올린은 초고성능 콘크리트 분야에서 틈새 역할을 유지하는 한편, 석회석 필러는 포틀랜드 석회석 시멘트의 세계 보급을 지원하여 단계적 탈경화 경로를 강화하고 있습니다. 이러한 추세는 산업 폐기물의 기회적 활용에서 계획적이고 확장 가능한 시멘트계 보조 재료 시장 생산 전략으로의 전환을 보여줍니다.

시멘트질 재료 보고서는 SCM 유형(플라이 애시, 슬래그 시멘트, 실리카퓸 등), 최종사용자(주택건설, 상업 및 공공시설, 산업시설 등), 재료 형태(분말, 슬러리/현탁액 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동/아프리카) 별로 세분화되어 있습니다. 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

아시아태평양은 SCM(보조 시멘트계 재료) 시장의 중심지로서 2025년 시장 규모의 47.88%를 차지할 것으로 예측됩니다. 이는 중국의 지속적인 건설 활동 둔화 추세와 2023-24년 361억 달러에 달하는 인도의 인프라 지출 급증에 힘입은 것입니다. 석탄재와 고로 슬래그를 쉽게 구할 수 있다는 점이 저비용 공급을 지원했으나, 환경정책에 따른 석탄화력발전소 폐지가 가속화되면서 지역 시멘트 대기업은 카올린 광상에 가까운 소성점토 허브를 우선순위에 두고 있습니다. 아세안 국가들은 '일대일로' 자금을 활용하여 고SCM 콘크리트를 대량으로 필요로 하는 교통 회랑을 건설 중이며, 일본과 한국은 내진 및 해양 인프라를 위해 고품질 메타카올린 혼화제를 도입하고 있습니다.

중동 및 아프리카은 사우디아라비아의 NEOM, 홍해 프로젝트, 저탄소 소재에 대한 지역적 의무를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 6.42%로 가장 빠른 성장세를 보일 것으로 예측됩니다. 아랍에미리트의 '에스티다마'와 이집트의 녹색건축 기준은 SCM 사용 기준을 명시하고 있으며, 동아프리카의 화산재 처리 및 사헬 지역 전역의 소성 점토 프로젝트에 대한 투자를 촉진하고 있습니다. 물류 문제와 품질 보증의 부족이 당장의 규모 확대에 걸림돌이 되고 있지만, 광물 자원이 풍부하므로 처리 인프라가 성숙해지면 지역 자급자족이 가능할 것으로 보입니다. 북미에서는 석탄화력발전이 60% 감소하면서 플라이 애시 공급이 타이트해지고, 네바다주와 유타주에서 천연 포졸란 자원의 탐사가 진행되는 한편, 유럽으로부터의 슬래그 수입이 증가하고 있습니다. 연방정부의 청정구매 규정과 주정부 차원의 세액공제 혜택으로 고SCM 배합 조기 도입 기업이 우대받고 있으며, 공급 마찰에도 불구하고 수요는 견고하게 유지되고 있습니다. 유럽은 성숙한 탄소가격제도와 RE2020 건축기준을 통해 석회석, 소성점토 및 재생미세 분말을 산업적 규모로 통합하는 기술적 한계에 도전하고 탈탄소화의 시험장으로서의 역할을 확고히 하고 있습니다. 남미는 규모는 작지만, 브라질의 해안 내진보강 프로젝트와 칠레의 광산 인프라가 내구성과 저탄소 콘크리트를 요구하면서 탄력을 받고 있으며, 지역내 포졸란-왕겨재 사업이 점차 세계 공급망로 연결되고 있습니다.

The Supplementary Cementitious Materials market is expected to grow from USD 27.96 billion in 2025 to USD 29.67 billion in 2026 and is forecast to reach USD 39.9 billion by 2031 at 6.12% CAGR over 2026-2031.

This expansion reflects the construction sector's rapid shift toward sustainable building practices as governments enforce carbon-pricing schemes and public-sector projects embed low-carbon concrete mandates. Accelerating infrastructure investment programs-such as Saudi Arabia's USD 1.1 trillion Vision 2030 pipeline-collide with the cement industry's need to reduce clinker content amid dwindling coal-fired by-products, creating durable demand for SCMs. Supply-side innovation in calcined clay, volcanic pozzolans, and limestone-blended cements mitigates the shrinking availability of fly ash and slag, while flash-calcination technology lowers processing energy requirements by up to 40% and broadens the viable feedstock base.

Massive public-works funding underpins the supplementary cementitious materials market, with India's infrastructure capital expenditure swelling 5.7 times to USD 36.1 billion in 2023-24, Saudi Arabia's Vision 2030 exceeding USD 1.1 trillion, and African infrastructure outlays averaging USD 93 billion each year. These programs specify higher SCM substitution in concrete-Sydney Metro achieved 38-52% replacement, resulting in a 120,000-tonne CO2-e reduction across projects . The construction surge, therefore, multiplies SCM demand, enabling suppliers to secure long-term contracts that justify investments in flash-calciner capacity and logistics optimization.

Regulatory pressure is intensifying. France's RE2020 caps embodied carbon in new buildings at 640-740 kg CO2-e/m2, while the EU's Carbon Border Adjustment Mechanism prices imports on a carbon basis. US Buy Clean rules require Environmental Product Declarations for federally funded concrete, and California applies carbon pricing to construction materials, creating premium markets for high-SCM mixes. These regulations make decarbonized concrete economically attractive, locking in structural demand for SCMs as a compliance pathway.

Coal-power output in the U.S. has fallen 60% since 2010, slashing high-grade fly ash volumes, while blast-furnace slag shrinks as steel producers pivot to electric arc furnaces. Remaining ash stockpiles command a 40-60% price premium, and transport distances lengthen, eroding cost advantages. Concrete producers must therefore re-engineer mix designs around alternative SCMs or pay higher inputs, constraining short-term growth until new supply sources mature.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fly ash held a 41.72% market share of the Supplementary Cementitious Materials market in 2025, supported by well-established logistics networks and predictable pozzolanic properties, despite declining coal generation. Slag cement (GGBFS) follows, supplying high-performance concrete segments even as blast-furnace output contracts. Calcined clay, however, is expanding at a 6.88% CAGR as flash-calciner units proliferate, lowering energy costs and enabling economic processing of clay with only 15-25% kaolinite. This trajectory positions calcined clay as the primary substitute for dwindling coal-derived sources, restructuring regional supply portfolios and inviting new entrants backed by mineral-rich deposits.

Manufacturers are funneling capital toward purpose-built calcination and grinding plants capable of ultraprecise particle-size control, raising pozzolanic reactivity indexes above 800 mg Ca(OH)2/g and drawing premium pricing. Silica fume and high-reactivity metakaolin maintain niche roles in ultra-high-performance concrete, while limestone filler underpins the global rollout of Portland Limestone Cement, reinforcing incremental de-clinkerization pathways. Collectively, these trends signal a pivot from opportunistic use of industrial waste toward deliberate, scalable supplementary cementitious materials market production strategies.

The Supplementary Cementitious Materials Report is Segmented by SCM Type (Fly Ash, Slag Cement, Silica Fume, and More), End User (Residential Construction, Commercial and Institutional, Industrial Facilities, and More), Material Form (Powder, Slurry/Suspension, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

The Asia-Pacific region remains the epicenter of the supplementary cementitious materials market, capturing 47.88% of the 2025 value, driven by China's continued but moderating construction activities and India's surge in infrastructure expenditure to USD 36.1 billion during 2023-24. Ready access to coal ash and blast-furnace slag once underpinned low-cost supplies; however, environmental policies are accelerating coal retirements, prompting regional cement majors to prioritize calcined-clay hubs near kaolinite-rich deposits. ASEAN economies are leveraging Belt and Road funding to build transport corridors that require high-SCM concrete volumes, while Japan and South Korea are deploying premium metakaolin blends in seismic-resistant and marine infrastructure.

The Middle East & Africa is projected to post the fastest 6.42% CAGR through 2031, underwritten by Saudi Arabia's NEOM, the Red Sea Project, and regional mandates for low-carbon materials. UAE's Estidama and Egypt's green-building codes codify SCM thresholds, attracting investment in volcanic-ash processing in East Africa and calcined-clay projects throughout the Sahel. Logistics hurdles and quality assurance gaps impede immediate scale-up; however, mineral abundance positions the region for self-sufficiency once the processing infrastructure matures. North America faces a tightening fly-ash pipeline after 60% coal-generation decline, driving exploration of natural pozzolan sources in Nevada and Utah, alongside increased slag imports from Europe. Federal Buy Clean rules and state-level tax credits reward early adopters of high-SCM mixes, keeping demand buoyant despite supply friction. Europe, with mature carbon-pricing and RE2020 building codes, pushes technical boundaries by integrating limestone-calcined clay and recycled fines at industrial scale, cementing its role as a decarbonization laboratory. South America, though smaller, gains momentum as Brazil's coastal resilience projects and Chile's mining infrastructure demand durable, low-carbon concrete, stimulating regional pozzolan and rice-husk ash ventures that gradually connect into global supply chains.