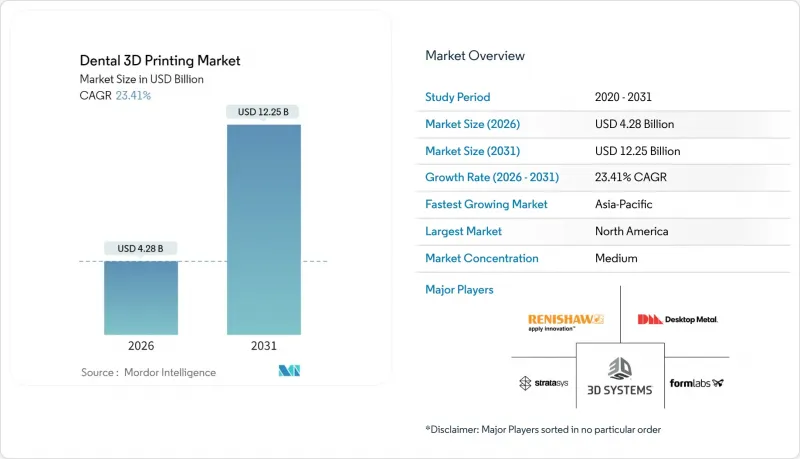

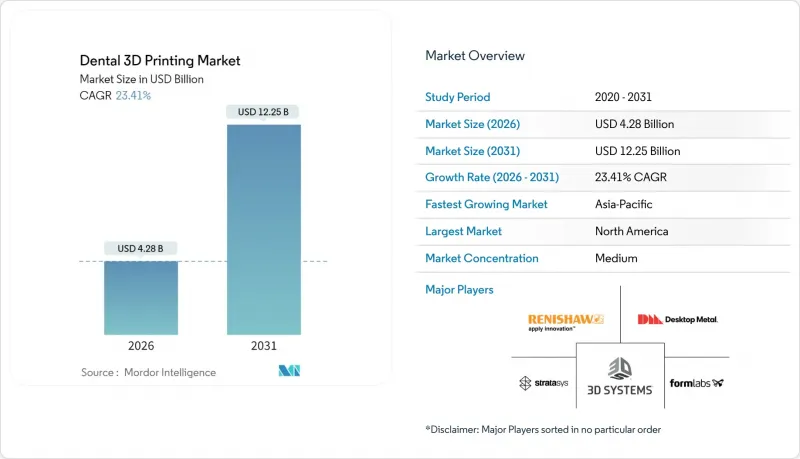

2026년 치과용 3D 프린팅 시장 규모는 42억 8,000만 달러로 추정되며, 2025년 34억 7,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측에서는 122억 5,000만 달러에 달하며, 2026-2031년에 CAGR 23.41%로 확대할 전망입니다.

직접 인쇄된 교정 장치의 신속한 규제 승인, AI 기반 설계 자동화, 아시아태평양의 디지털화 프로그램이 재료 폐기물을 최대 90%까지 줄이는 적층제조 공정으로의 전환을 가속화하고 있다(WILEY.COM). 주요 제조업체들은 대량 생산 실험실의 비용 절감을 위해 고속 프린터를 출시하고 있으며, 검증된 생체적합성 수지를 통해 임상의들은 체어사이드에서의 적용 범위를 확대할 수 있는 확신을 가질 수 있게 되었습니다. 일본과 중국의 의료보험사들은 이미 CAD/CAM 수복물에 대한 보험 적용을 시작했으며, 다른 지역도 이를 따라가는 정책적 추세를 보이고 있습니다. 동시에, 광개시제 화학물질에 대한 공급망 압력과 아크릴계 수지의 배출 제한이 강화됨에 따라 보다 친환경적인 화학 기술과 현지 조달 전략의 필요성이 부각되고 있습니다.

연구에 따르면 디지털 워크플로는 직접 치료 비용을 18% 절감하고, 실험실 작업 비용을 49% 절감하는 것으로 나타났습니다. 당일 배송으로 재방문이 불필요하며, 8점 이상의 수복물을 동시에 인쇄할 수 있으며, 대량 진료소에서 규모의 경제를 실현할 수 있습니다. 디지털 의치 제작의 단가는 현재 1 개당 5.95달러(절삭 의치 43.18달러 대비)로, 환자 1인당 154분의 진료 시간을 절약할 수 있습니다. 이러한 경제성은 신속한 대응과 환자 만족도를 높이고자 하는 비용에 민감한 진료소에서 선호하고 있습니다. 수지의 수율 향상과 프린터 가격의 하락으로 치과용 3D 프린팅 시장의 초기 도입자 외의 접근성이 확대되면서 그 매력은 더욱 커지고 있습니다.

세계에서 고령화가 진행되면서 크라운, 브릿지, 틀니에 대한 수요가 지속적으로 증가하고 있습니다. 65세 이상 성인의 무치악 비율은 계속 증가하고 있으며, 의료 시스템은 부가적인 제조 기술로 실현 가능한 효율적인 수복 치료를 우선시할 수밖에 없습니다. 일본이 그 과제를 여실히 보여주고 있습니다. 2024년에는 인력 부족으로 인해 역대 가장 많은 치과가 문을 닫을 것으로 예상되며, 남아있는 치과들은 생산성 향상을 위해 디지털화를 추진해야 합니다. 중국과 서방 국가에서도 비슷한 인구통계학적 압력이 나타나고 있습니다. 3D 프린팅 기술은 맞춤 보철물을 제공함으로써 적합성을 향상시키면서 재수술을 줄이는 맞춤형 보철물을 제공함으로써 이러한 급증하는 수요에 대응할 수 있는 확장 가능한 길을 제시합니다.

전문가용 프린터의 가격은 엔트리 모델 4,499달러부터 생산시스템의 경우 5자릿수 가격대까지 폭넓게 책정되어 있습니다. 레진이나 금속 분말의 비용은 시술량이 예측하기 어려운 진료소에서 지속적인 지출 요인이 됩니다. 독일 진료소를 대상으로 한 횡단면 조사에서 특히 싱글체어 진료에서 투자비용이 도입장벽의 1위로 꼽혔습니다. 리스 프로그램이나 부품별 과금 서비스가 부담 경감에 기여하고 있지만, 라틴아메리카와 동남아시아 일부 지역에서는 여전히 높은 가격이 장벽으로 작용하고 있습니다.

2025년 치과용 3D 프린팅 시장 매출의 45.18%는 인탱크 광중합 방식이 차지할 것으로 예상되며, 그 정확성과 다양한 수지 팔레트가 시장에서 높은 평가를 받고 있는 것으로 나타났습니다. 선택적 레이저 소결 방식의 CAGR 24.68%는 금속 프레임워크 및 임플란트 부품에 대한 수요 증가를 반영하고 있으며, 이러한 추세에 따라 프린터 제조업체들은 코발트 크롬 및 티타늄을 위한 분말 베드 온도 조절을 추진하고 있습니다.

가시광선 광개시제의 연구개발로 경화속도가 향상되고 독성 배출물이 감소함에 따라 탱크식 시스템은 다가오는 ISO 표준에 부합하는 방향으로 나아가고 있습니다. 한편, PolyJet 및 디지털 광처리 플랫폼은 다재료 가이드 및 풀 컬러 모델을 위한 틈새 시장을 개발하고 있습니다. 검증된 재료 라이브러리가 확대됨에 따라 구매자들은 오픈 아키텍처 프린터로 미래를 내다보고 치과용 3D 프린팅 시장에서 교차 기술의 유연성을 활용하고 있습니다.

2025년 치과용 3D 프린팅 시장 매출의 39.94%를 장비가 차지할 것으로 예상되며, 이는 연구소의 프린터 및 스캐너 장비 증설에 대한 지속적인 설비투자를 반영합니다. 그러나 클리닉이 복잡한 장비의 설계 및 제조를 전문 업체에 아웃소싱하는 움직임에 따라 서비스 분야는 25.72%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다.

이 서비스 분야의 모멘텀은 중앙집중식 제조가 단가 인하로 이어지는 다른 의료 분야의 동향과 공통점이 있습니다. 수지 및 금속 분말 공급업체는 프린트팜과 협력하여 워크플로우를 검증하고 있으며, 현금 흐름을 안정화시키는 지속적인 수입원을 창출하고 있습니다. 그 결과, 향후 10년간 치과용 3D 프린팅 시장에서 서비스 사업자의 취급량이 장비 판매량을 넘어설 것으로 예측됩니다.

북미는 2025년 매출의 38.72%를 차지할 것으로 예상되며, FDA의 조기 승인 과정과 CAD/CAM 크라운의 보험 적용이 이를 지원하고 있습니다. 이 지역의 2031년까지 연평균 복합 성장률(CAGR) 22.45%는 견고하지만, 고소득층 대부분이 이미 디지털 치과를 이용할 수 있으므로 신흥 시장보다 느리게 성장하고 있습니다. 사모펀드 그룹은 여러 주에 걸친 사업 규모의 경제를 추구하는 롤업을 통해 랩 네트워크의 재편을 추진하고 있습니다.

아시아태평양은 25.11%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있으며, 중국의 첨단 제조 전략과 NMPA 승인을 앞당기는 보험 제도 개혁이 주도하고 있습니다. 일본에서는 고령화 인구와 체어사이드 수복 시술의 보험 적용이 안정적인 시술 건수를 지원하고 있으며, 인도에서는 디지털 헬스 정책과 치과 의료 관광이 수요를 증가시키고 있습니다. 이 지역의 구매력 다양성에 대응하기 위해 유연한 가격대 설정이 요구되고 있으며, 수입관세 회피 및 환율변동 리스크 감소를 위해 치과용 3D 프린터의 현지 조립이 촉진되고 있습니다.

유럽에서는 독일, 프랑스, 북유럽 국가의 공공 의료 기관이 비용 관리형 보철 치료에 3D 프린팅을 도입하면서 22.96%의 연평균 복합 성장률(CAGR)을 기록했습니다. 반면, 중동 및 아프리카과 남미 지역은 의료관광 회랑과 민간 의료투자를 원동력으로 각각 24.58%, 24.21%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 각국 정부는 국내 기술자들이 지역 수요에 대응할 수 있도록 육성 프로그램을 지원하고 있습니다.

Dental 3D Printing market size in 2026 is estimated at USD 4.28 billion, growing from 2025 value of USD 3.47 billion with 2031 projections showing USD 12.25 billion, growing at 23.41% CAGR over 2026-2031.

Rapid regulatory clearances for direct-printed orthodontic devices, AI-driven design automation, and Asia-Pacific digitization programs are accelerating the shift from subtractive techniques to additive processes that cut material waste by as much as 90% [WILEY.COM]. Leading manufacturers are rolling out high-speed printers that trim production costs for large-volume laboratories, while validated biocompatible resins give clinicians confidence to broaden chairside use. Healthcare payers in Japan and China are already reimbursing CAD/CAM restorations, signaling a policy tailwind that other regions are expected to follow. At the same time, supply-chain pressure on photoinitiator chemicals and looming emission limits for acrylate resins highlight the need for greener chemistries and local sourcing strategies.

Studies show that digital workflows cut direct treatment costs by 18% and slash laboratory labor expenses by 49%. Same-day delivery removes repeat visits, and simultaneous printing of eight or more restorations drives economies of scale for high-volume clinics. Digital denture fabrication now costs USD 5.95 per unit compared with USD 43.18 for milled alternatives, while saving 154 chairside minutes per patient. These economics resonate with cost-conscious practices seeking faster turnaround and higher patient satisfaction. The appeal grows as resin yields rise and printer prices fall, widening access beyond early adopters within the dental 3D printing market.

An aging global population underpins sustained demand for crowns, bridges and dentures. Edentulism rates among adults over 65 continue to climb, prompting healthcare systems to prioritize efficient restorative care that additive technologies can deliver. Japan illustrates the challenge: a record number of dental clinics closed in 2024 due to workforce shortages, forcing remaining practices to digitize for productivity. Similar demographic pressure is emerging in China and Western Europe. 3D printing offers a scalable pathway to meet the surge, delivering custom prosthetics that improve fit while lowering rework rates.

Professional printers still range from USD 4,499 for entry models to much higher five-figure price tags for production systems. Resin and metal powder costs add recurring expense in clinics where procedure volume is unpredictable. A cross-sectional survey of German practices ranked investment cost as the top adoption barrier, especially for single-chair surgeries. Leasing programs and pay-per-part services are easing the burden, yet the sticker shock persists in Latin America and parts of Southeast Asia.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Vat photopolymerization accounted for 45.18% of the dental 3D printing market revenue in 2025, underscoring its precision and broad resin palette in the dental 3D printing market. Selective laser sintering's 24.68% CAGR reflects growing demand for metal frameworks and implant components, a trend that pushes printer makers to refine powder-bed temperatures for cobalt-chrome and titanium.

R&D into visible-light photoinitiators is raising cure speed while lowering toxic emissions, helping vat systems comply with looming ISO standards. Meanwhile, PolyJet and digital light processing platforms carve out niches for multi-material guides and full-color models. As validated material libraries expand, buyers are future-proofing with open-architecture printers to tap cross-technology flexibility in the dental 3D printing market.

Equipment generated 39.94% of the dental 3D printing market revenue in 2025, reflecting sustained capital expenditures by laboratories building fleets of printers and scanners. However, the services segment is climbing at a 25.72% CAGR as clinics outsource the design and production of complex appliances to specialized hubs.

This service momentum mirrors trends in other healthcare verticals where central fabrication can drive down unit cost. Resin and metal powder suppliers are partnering with print farms to validate workflows, adding a recurring revenue layer that stabilizes cash flow. As a result, service bureaus are forecast to eclipse equipment sales by volume in the dental 3D printing market during the next decade.

The Dental 3D Printing Market Report is Segmented by Technology (Vat Photopolymerization, Polyjet, and More), Product & Service (Materials, Equipment, Services), Application (Prosthodontics, Orthodontics, Implantology), End-User (Dental Laboratories, Hospitals & Clinics, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 38.72% of 2025 revenue, supported by early FDA pathways and insurance coverage for CAD/CAM crowns. The region's 22.45% CAGR to 2031 is healthy but slower than emerging markets because most high-income consumers already have access to digital dentistry. Private equity groups are reshaping laboratory networks through roll-ups that seek economies of scale across multistate operations.

Asia-Pacific is the fastest-growing region at 25.11% CAGR, propelled by China's advanced-manufacturing strategy and insurance reforms that speed NMPA approvals. Japan's elderly demographic and coverage for chairside restorations sustain steady procedure volume, while India's digital health mission and dental tourism add incremental demand. The region's diverse purchasing power calls for flexible price tiers, encouraging local printer assembly to avoid import duties and smooth currency volatility in the dental 3D printing market.

Europe posts a 22.96% CAGR as public-sector clinics in Germany, France and the Nordic countries adopt 3D printing for cost-controlled prosthodontics. Meanwhile, the Middle East & Africa and South America are expanding at 24.58% and 24.21% CAGR, respectively, driven by medical-tourism corridors and private healthcare investments. Governments are beginning to sponsor training programs that position domestic technicians to serve regional demand.