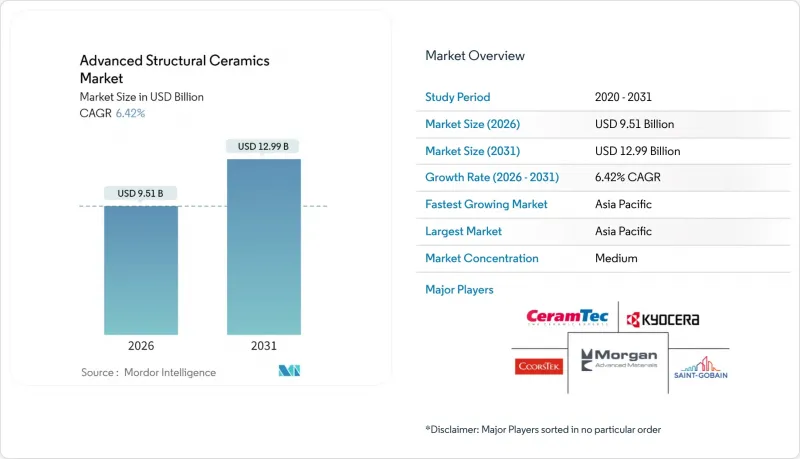

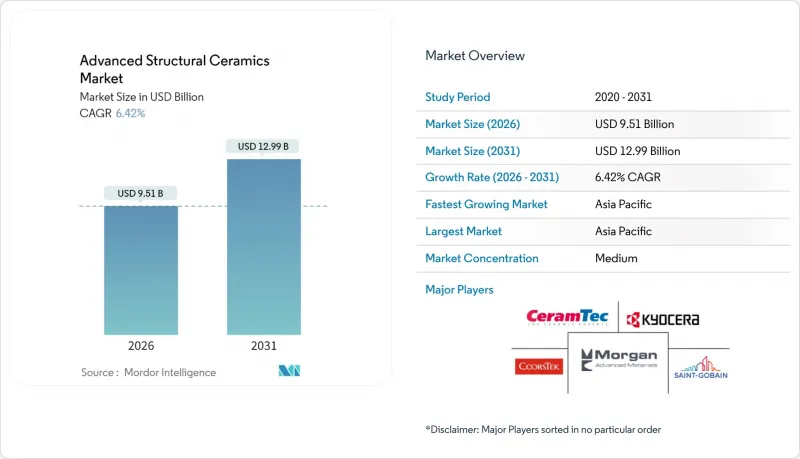

첨단 구조용 세라믹 시장은 2025년에 89억 4,000만 달러로 평가되었고, 2026년 95억 1,000만 달러에서 2031년까지 129억 9,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.42%로 예상됩니다.

상업적 이익은 특히 전기 파워트레인, 5G 인프라, 수소 터빈 등 금속이나 폴리머로는 부족한 영역에서 이 소재의 기능성에 기인합니다. 항공우주 제조업체가 연료 절약형 엔진을 추구하고, 반도체 팹이 저손실 기판을 채택하고, 에너지 기업이 더 높은 온도와 고효율의 터빈을 설계함에 따라 수요가 가속화되고 있습니다. 업계 재편도 성장을 견인한다: 쿠어스텍의 2억 4,500만 달러 규모의 산고반 첨단 세라믹 인수는 규모 확대와 공급 리스크 감소를 가져옵니다. 아시아태평양은 반도체 산업 클러스터의 집적과 강력한 자동차 전동화 정책으로 생산 우위를 유지. 한편, 적층가공 기술은 폐기물 감소와 맞춤형 신속화를 실현하고, 특수 등급의 새로운 수익원을 개척할 수 있습니다.

제트 엔진 제조업체들은 현재 1,600℃ 이상의 흡기 온도를 목표로 하고 있으며, 이 온도 범위에서 실리콘 카바이드와 질화규소는 완전한 기계적 강도를 유지합니다. 이 세라믹은 새로운 터빈 플랫폼에서 연료 효율을 15-20% 향상시키며, 미 국방부는 마하 5 비행을 실현하는 초고온 복합재료에 의존하는 극초음속 항공기 프로그램에 자금을 지원하고 있습니다. 우주 비행의 요구는 이러한 필요성을 더욱 높이고 있으며, 재사용 가능한 발사체에는 질량 증가 없이 수백 번의 사이클을 견딜 수 있는 열 보호 시스템이 요구되고 있습니다.

질화알루미늄 및 탄화규소 기판은 폴리머 충전재에 비해 5-10배 빠른 속도로 배터리와 인버터의 열을 발산합니다. 테슬라는 모델 3의 인버터에 실리콘 카바이드를 채택하여 효율을 약 9% 향상시키고 전체 시스템 질량을 줄였습니다. 고급 전기자동차는 현재 800V 아키텍처로 전환하고 있으며, 세라믹 계면 소재는 급속 충전 시 셀을 안전한 온도 범위 내에서 유지하여 팩 수명을 연장하고 피트 스톱 시간을 단축할 수 있습니다.

완전 고밀도 실리콘 카바이드 부품은 동급 니켈 합금 부품에 비해 3-5배의 비용이 소요됩니다. 이는 분말에 99.9%의 순도가 필요하고, 다이아몬드 연삭과 긴 소결 주기가 필요하기 때문입니다. 이트륨 안정화 지르코니아 원료 가격은 2024년 이후 공급 제약으로 인해 17% 상승했습니다. 비파괴 검사에 대한 추가 요구 사항과 엄격한 통계 관리로 인해 변환 비용이 10 - 15% 더 높아져 가격에 민감한 전자 제품 및 소형 엔진 부품에 사용할 수 없습니다.

알루미나는 2025년 첨단 구조용 세라믹 시장 규모의 28.55%를 차지할 것으로 예상되며, 마모 링, 기판, 임플란트 고정장치의 주요 소재가 될 것으로 예측됩니다. 광범위한 특성과 저렴한 비용으로 인해, 특히 화학적 불활성이 요구되는 산업용 밸브 및 의료기기에서 지속적인 수요가 보장됩니다. 실리콘 카바이드는 반도체 및 EV용 트랙션 인버터(높은 스위칭 속도에서 와이드 밴드갭 호환성을 필요로 하는) 수요에 힘입어 다음 큰 점유율을 형성하고 있습니다. 지르코니아의 CAGR 8.45%는 초고온로와 터빈 슈라우드로의 전환을 시사합니다. 이러한 응용 분야에서 지르코니아의 낮은 열팽창률은 응력 균열을 감소시킵니다. 이에 따라 주요 업체들은 분무건조탑과 등압프레스에 대한 투자를 확대하여 기공 크기 제어를 유지하면서 생산량 확대를 꾀하고 있습니다.

보다 광범위한 채택을 위해서는 배치 균질성 및 미량 원소 임계값을 인증하는 ISO 17025 시험의 보급이 핵심입니다. 시험소가 이러한 기준을 충족함에 따라 항공우주 제조업체들은 새로운 화학 성분을 고온 테스트에 통합하는 것에 대한 확신을 갖게 되었습니다. 한편, 적층가공 기술을 통해 단일 부품 내에서 알루미나와 지르코네이트를 결합한 기능적 경사 이중층 구조가 가능하여 비용과 응력분포의 최적화가 이루어지고 있습니다. 이러한 발전은 알루미나 양산 기반을 보호하면서 특수 등급의 고수익화를 실현하여 첨단 구조용 세라믹 시장을 균형 잡힌 성장 궤도로 이끌고 있습니다.

본 "첨단 구조용 세라믹 시장 보고서'는 재료 유형별(알루미나, 카바이드, 탄화물, 지르코네이트, 질화물, 기타), 최종 이용 산업별(자동차, 반도체, 의료, 에너지, 산업, 항공우주/방위산업, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동/아프리카), 지역별(아시아태평양, 북미, 유럽, 남미, 중동/아프리카)로 구분하여 조사 분석하였습니다. 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

아시아태평양은 원료 분말 정제, 부품 제조 및 최종 제품 조립의 긴밀한 협력으로 2025년 53.45%의 매출을 차지하며 6.98%의 연평균 복합 성장률(CAGR)로 우위를 확대할 것으로 예측됩니다. 중국에서는 2,200℃ 소결에 대응하는 새로운 가마가 가동되기 시작했고, 일본에서는 교세라, NGK, 덴카 간의 크로스 라이선싱을 통해 가공기술의 고도화가 진행되고 있습니다.

북미는 항공우주, 방위, 의료 기술 분야의 고성능 부문에 집중하고 있습니다. 쿠어스텍이 2024년 산고반 첨단 세라믹를 인수함에 따라 장갑 타일 및 반도체 지그용 미국 내 새로운 생산 능력이 추가되어 국내 공급의 안정성이 향상되었습니다. FDA Class III 임플란트 승인 및 AS9100 품질 감사를 포함한 엄격한 규제는 신규 진입을 제한하는 한편, 가격 안정화를 가져와 제조업체가 R&D 비용을 회수할 수 있도록 하고 있습니다.

유럽은 세라믹 매트릭스 복합재, 적층 성형, 수소 대응 터빈 분야에서 주도권을 유지하고 있습니다. 독일 자동차 부품 제조업체는 고속 전기 구동 장치에 질화규소 베어링을 내장하고, 영국은 재사용 가능한 우주 엔진용 세라믹 개발에 자금을 지원하고 있습니다. 유럽연합의 REACH 규정과 CE 마크 제도는 환경 적합성과 통일된 표시를 보장합니다. 신흥 동남아시아 거점 및 인도에서는 다국적 기업들이 차세대 전자기기 조립 거점 인근에 분말 제조 및 프레스 라인을 집중 배치하는 움직임으로 점유율 확대가 시작되었지만, 기술력 격차가 중기적 과제로 남아있습니다.

The Advanced Structural Ceramics Market was valued at USD 8.94 billion in 2025 and estimated to grow from USD 9.51 billion in 2026 to reach USD 12.99 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031).

Commercial gains stem from the material's ability to operate where metals and polymers fall short, especially in electrified powertrains, 5G infrastructure, and hydrogen turbines. Demand accelerates as aerospace manufacturers seek fuel-saving engines, semiconductor fabs adopt low-loss substrates, and energy firms design hotter, leaner turbines. Consolidation also shapes growth: CoorsTek's USD 245 million purchase of Saint-Gobain Advanced Ceramics improves scale and cuts supply risk. Asia-Pacific retains a production edge thanks to deep semiconductor clusters and strong automotive electrification policies, while additive manufacturing reduces waste and speeds customization, opening fresh revenue pools for specialized grades.

Jet-engine makers now target inlet temperatures above 1,600 °C, a range where silicon carbide and silicon nitride retain full mechanical strength. These ceramics raise fuel efficiency by 15-20% in new turbine platforms, while the U.S. Department of Defense funds hypersonic vehicle programs that rely on ultra-high-temperature composites for Mach 5 flight. Spaceflight demands compound the need, as reusable launch vehicles require thermal-protection systems that survive hundreds of cycles without mass penalties.

Aluminum nitride and silicon carbide substrates dissipate battery and inverter heat at rates five to ten times higher than polymer fillers. Tesla uses silicon carbide in Model 3 inverters, improving efficiency by around 9% and trimming overall system mass. Premium electric cars now shift to 800 V architectures, and ceramic interface materials keep cells within safe temperature bands during fast charging, extending pack life and enabling shorter pit-stop times.

Fully dense silicon carbide parts cost three to five times more than equivalent nickel alloys because powders require 99.9% purity, diamond grinding, and long sintering cycles. Yttria-stabilized zirconia feedstock prices rose 17% after 2024 supply constraints. Added requirements for non-destructive testing and tight statistical controls lift conversion expenses another 10-15%, discouraging use in price-sensitive electronics and small-engine components.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Alumina generated 28.55% of the advanced structural ceramics market size in 2025 and remains the workhorse for wear rings, substrates, and implant fixtures. Its broad property set and accessible cost profile ensure sustained demand, particularly in industrial valves and medical tools that require chemical inertness. Silicon carbide forms the next largest slice, lifted by semiconductor and EV traction inverters that need wide-band-gap compatibility at high switching speeds. Zirconate's 8.45% CAGR signals a pivot toward ultrahigh-temperature furnaces and turbine shrouds, where its lower thermal expansion shrinks stress cracks. In response, top producers invest in larger spray-dry towers and isostatic presses to scale volumes while preserving pore-size control.

Broader adoption also hinges on ISO 17025 testing that certifies batch homogeneity and trace element thresholds. As labs meet these standards, aerospace primes feel more confident integrating newer chemistries into hot-section tests. Meanwhile, additive manufacturing enables functionally graded bilayers that marry alumina and zirconate within a single part, optimizing cost and stress distribution. These advances protect alumina's volume base while unlocking higher margins for specialty grades, keeping the advanced structural ceramics market on a balanced growth path.

The Advanced Structural Ceramics Report is Segmented by Material Type (Alumina, Carbides, Zirconate, Nitrides, and Others), End-Use Industry (Automotive, Semiconductors, Medical, Energy, Industrial, Aerospace and Defense, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific posted 53.45% revenue in 2025 and will extend its lead with a 6.98% CAGR thanks to tight coupling between raw-powder refining, component fabrication, and end-product assembly. China commissions fresh kilns capable of 2,200 °C sintering, while Japan advances processing know-how through cross-licensing among KYOCERA, NGK, and Denka.

North America concentrates on high-performance segments tied to aerospace, defense, and medtech. CoorsTek's 2024 purchase of Saint-Gobain Advanced Ceramics folds in new U.S. capacity for armor tiles and semiconductor fixtures, improving domestic supply security. Regulatory rigor, including FDA class-III implant approval and AS9100 quality audits, limits competitive entrants yet stabilizes pricing, allowing producers to recoup research and development outlays.

Europe maintains leadership in ceramic matrix composites, additive manufacturing, and hydrogen-ready turbines. German auto suppliers embed silicon nitride bearings in high-speed e-drives, while the United Kingdom funds ceramics for reusable space engines. The bloc's REACH and CE frameworks ensure environmental compliance and consistent labeling. Emerging Southeast Asian hubs and India start to gain share as multinationals co-locate powder-prep and pressing lines near next-generation electronics assembly, but technical skill gaps remain a medium-term hurdle.