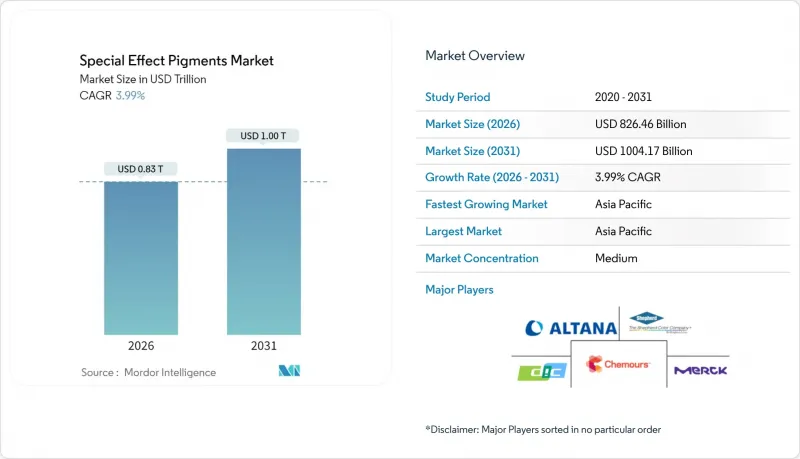

특수 효과 안료 시장 규모는 2026년에는 8,264억 6,000만 달러로 추정되며, 2025년 7,947억 8,000만 달러에서 성장하여 2031년에는 1조 41억 7,000만 달러에 이를 것으로 예측됩니다. 2026-2031년에는 CAGR 3.99%로 성장할 전망입니다.

시장을 특징짓는 것은 표면적인 성장률이 아닌 구조적 변화이며, 급속한 산업 재편, 소비재 및 산업용 제품의 고급화, 지속 가능한 제조로의 전환이 경쟁 구도를 결정하고 있습니다. 특히 합성 운모 기판을 기반으로 하는 경우, 진주광택 등급은 금속성 광택과 규제 적합성을 동시에 만족시키기 때문에 수요의 핵심이 되고 있습니다. 자동차 OEM 업체들은 전 세계적으로 컬러 매칭 기준을 강화하고 있으며, 레이더 투과성 및 수성 시스템에서 로트 간 일관성을 보장할 수 있는 공급업체에 대한 평가가 높아지고 있습니다. 화장품, 플라스틱, 첨단 디스플레이 분야에서의 동시 수요 증가로 고객층이 심화되는 한편, 아시아태평양의 생산기지는 원자재와 노동력의 효율성을 확보하여 전체 가치사슬의 비용 곡선을 압축하고 있습니다.

자동차 디자인 스튜디오는 차세대 차량의 차별화를 위해 더 깊은 색상 공간과 다층 광학 효과를 지정하고 있습니다. BASF의 2025년 컬러 트렌드 팔레트는 자율주행 센서에 방해가 되지 않는 적외선 투과성 안료와 바이오 수지를 통합했습니다. 레이더 투과성 요구 사항으로 인해 기존의 메탈릭 플레이크가 제거되고, 미적 감각과 센서 성능을 모두 만족시키는 진주 광택 및 크리스탈 유리 기술 개발이 시급한 상황입니다. 수성 탑코트가 유럽 OEM 라인의 주류로 자리 잡으면서 안료 제조업체는 낮은 VOC 수준에서 장기 분산 안정성을 입증해야 하는 과제를 안고 있습니다. 이러한 변화는 보수 도장 분야에도 파급되어, 차체 작업장에서는 분광광도계를 사용하여 OEM 색조를 재현하고 있습니다. 이를 통해 수리 패널을 공장 마감과 동일하게 재현할 수 있는 이펙트 안료에 대한 지속적인 수요가 보장됩니다. 이러한 요구사항은 종합적으로 공급업체의 통합을 촉진합니다. 전 세계 자동차 제조업체들은 여러 대륙에 걸친 프로그램을 동일한 품질 기준으로 대응할 수 있는 엄선된 벤더 리스트를 선호하기 때문입니다.

스마트폰이 주도하는 뷰티 문화는 광학적인 기이함을 주류의 기대치로 전환시켜 피부와 손톱에 컬러 여행과 광채를 만들어내는 홀로그램 및 진주광택 마이크로플레이트에 대한 수요를 증가시키고 있습니다. FDA의 천연 운모의 안구용 영구 목록 등록은 소비자들이 성분의 안전성에 대한 감시를 강화하는 시기에 규제적 확실성을 제공합니다. 주요 브랜드는 현재 중금속을 포함하지 않는 제품 라인을 규정하고 있으며, 더 높은 입자 균일성과 낮은 미량 금속 함량을 제공하는 합성 운모 및 붕규산 유리베이스로의 전환을 촉진하고 있습니다. 아시아의 K-뷰티 혁신 기업들은 제품 수명주기을 단축하고, 안료 공급업체들이 몇 주 안에 고객의 요청에 따라 색조를 제공할 수 있는 민첩한 소량 생산에 박차를 가하고 있습니다. 수익률의 가능성은 높아지는 반면, 새로운 색상마다 세계 컴플라이언스 문서 인증이 필요하기 때문에 유지 비용도 상승하고 있습니다.

REACH 규정에 따른 서류 업데이트는 알루미늄 및 구리 플레이크에 대한 철저한 독성 데이터를 요구하고 있으며, 중소 안료 제조업체는 불균형적인 규정 준수 예산을 할당하거나 해당 지역에서 철수해야 하는 상황에 처해 있습니다. 동시에, 용제계에서 수성 바인더로의 전환으로 인해 기존의 리핑제가 알칼리성 매체에 용해되거나 가스화되기 때문에 재배합이 요구되고 있습니다. 독자적인 봉입 및 패시베이션 기술을 보유한 공급업체는 규제 마찰을 고객 충성도 구축 서비스로 전환할 수 있지만, 후발업체는 승인 주기가 길어지고 수익이 침식되고 있습니다.

2025년 기준 특수효과 안료 시장의 51.02%를 차지한 펄 안료는 2031년까지 연평균 복합 성장률(CAGR) 4.07%로 가장 빠른 성장세를 유지할 것으로 예상되며, 대량 생산과 성장 양면에서 선도적인 위치를 확고히할 것으로 예측됩니다. 유리 플레이크 및 합성 운모 배합물은 레이더 투과성과 초저 중금속 함량을 제공하여 적용 범위를 확대하여 전기자동차 외장재 및 고급 화장품용 파우더에서 높은 평가를 받고 있습니다. 특수 효과 안료 시장은 OEM의 투명 코팅층이 가변 두께 라멜라를 통합하여 혜택을 받고 있습니다. 이를 통해 도료의 변색을 최소화하면서 컬러 트래블 효과를 만들어 도장 공정의 패스 수를 줄이고 사이클 타임을 단축할 수 있습니다.

메탈릭 등급은 보호용 탑코트 분야에서 핵심적인 지위를 유지하고 있지만, 광도보다 레이더 적합성이 우선시되는 특수효과 안료 시장에서는 점유율이 감소하는 추세입니다. 첨단 실리카 캡슐화 공정을 보유한 벤더는 지역별로 위탁 가공업체에 기술 라이선싱을 통해 수익률을 보호하고, 지적재산권 희석을 피하면서 규모를 확보할 수 있습니다. 광학 가변 안료 및 홀로그램 안료는 보안 잉크 및 브랜드 보호 라벨에 활용되고 있습니다. 시장 규모는 전반적으로 작지만, 평균 이상의 가격 책정을 실현하고 포트폴리오의 수익성을 강화하여 단순한 상품 부가물이 아닌 전략적 확장 분야로서의 지위를 유지하고 있습니다.

특수 효과 안료 보고서는 안료 유형(금속, 진주 광택, 기타), 최종 사용자 산업(페인트 및 코팅, 화장품, 플라스틱, 인쇄 잉크, 기타 용도), 지역(아시아태평양, 북미, 유럽, 유럽, 남미, 중동 및 아프리카) 별로 분류됩니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

아시아태평양은 2025년 특수효과 안료 시장 규모의 45.12%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 4.55%로 2031년까지 세계 제조 거점으로서의 입지를 확고히 하고 있습니다. 중국의 자동차 도료 분야에서의 우위가 지역 수요를 뒷받침하는 한편, 인도의 장식용 도료 분야에서 7% 이상의 성장이 진주광택 분산액 수요 증가를 주도하고 있습니다. 전기자동차의 현지 생산을 촉진하는 정부의 특혜 조치로 인해 대륙 간 동일한 컬러 라이브러리를 요구하는 외국 제조업체들이 모여들었습니다. 이에 따라 안료 제조업체들이 지역 내에 기술 서비스 연구소를 설립하려는 움직임이 가속화되고 있습니다. 베트남과 말레이시아의 동남아시아 전자기기 클러스터는 다운스트림 채널을 더욱 다양화하여 스마트폰 케이스와 웨어러블 기기 하우징용 고순도 특수효과 등급을 흡수하고 있습니다.

유럽은 전 세계 배합 기준을 형성하는 규제적 영향력을 가지고 있습니다. REACH 규제와 2023년 마이크로 플라스틱 규제는 바이오 계면활성제 및 캡슐화 금속 플레이크로의 전환을 가속화하고 있으며, 이러한 정책적 환경은 선행 기업에게 방어 가능한 프리미엄 가격 책정을 가져옵니다. 독일과 이탈리아의 자동차 제조업체들은 미크론당 광학적인 부풀어 오름을 강화하는 저막 두께의 클리어 코트를 추진하고 있으며, 안료 공급업체들에게 높은 종횡비의 플레이트 렛과 보다 엄격한 입자 크기 관리를 요구하고 있습니다. 건축용 도료 분야에서는 북유럽 국가들이 거의 제로 VOC 기준을 지정하고 있고, 이것이 유럽 전역으로 빠르게 확산되면서 수성페인트 인증이 없는 수입 배합제의 기술적 장벽이 높아지고 있습니다.

북미에서는 자동차 보수 도장 생태계가 유지되고 있으며, 메탈릭 펄 터치업 제품에 대한 수요가 안정적으로 유지되고 있습니다. 미국 식품의약국(FDA)의 운모(운모)의 영구 착색 첨가제 면제 지정은 화장품 효과 안료의 원료 선택을 안정화시키고, 새로운 색상 출시 시 인증 프로세스를 효율화합니다. 멕시코의 자동차 조립 거점 확대는 안료의 국경 간 물류를 활성화하고, 미국 공급업체는 니어쇼어링을 활용하여 리드타임을 단축하고 있습니다. 중동 및 아프리카에서는 인프라 사업이 장식용 도료의 사용을 가속화함에 따라 장기적인 성장 여력이 있을 것으로 예측됩니다. 그러나 현지 생산능력이 제한적이기 때문에 수입에 의존하고 있으며, 통합된 화물 네트워크를 가진 다국적 기업이 우위를 점하고 있습니다. 남미의 안료 수요는 브라질의 자동차 벨트 지역에 집중되어 있으며, 환율 변동성으로 인해 수익 송금 관리를 위한 헤지 전략이 필수적입니다.

Special Effect Pigments market size in 2026 is estimated at USD 826.46 billion, growing from 2025 value of USD 794.78 billion with 2031 projections showing USD 1004.17 billion, growing at 3.99% CAGR over 2026-2031.

Structural change rather than headline growth defines the landscape, with rapid consolidation, premium-finish adoption across consumer and industrial goods, and a pivot toward sustainable manufacturing dictating competitive outcomes. Pearlescent grades remain the fulcrum of demand because they deliver both metallic brilliance and regulatory compliance, especially when based on synthetic mica substrates. Automotive OEMs have tightened global color-matching standards, elevating suppliers that can guarantee batch-to-batch consistency in radar-transparent and water-borne systems. Parallel momentum in cosmetics, plastics, and advanced displays is deepening the customer mix, while the Asia-Pacific production base secures raw-material and labor efficiencies that compress cost curves for the entire value chain.

Automotive design studios are specifying deeper color spaces and multilayer optical effects to differentiate next-generation vehicles. BASF's 2025 color trend palette integrates bio-based resins with infrared-transparent pigments that do not interfere with autonomous driving sensors. Radar transparency disqualifies conventional metallic flakes, adding urgency to pearlescent and crystal-glass innovations that marry aesthetics with sensor performance. Water-borne topcoats now dominate European OEM lines, compelling pigment makers to demonstrate long-term dispersion stability at low VOC levels. The shift extends to refinish operations, where body shops deploy spectrophotometers to replicate OEM shades, guaranteeing ongoing demand for effect pigments able to match factory finishes on repaired panels. These requirements collectively reinforce supplier consolidation because global automakers favor a tightly curated vendor list that can service multi-continent programs with identical quality metrics.

Smartphone-driven beauty culture has converted optical novelty into mainstream expectation, lifting demand for holographic and pearlescent microplates that create color-travel and sparkle on skin and nails. The permanent FDA listing of natural mica for eye-area use provides regulatory certainty just as consumers intensify scrutiny of ingredient safety. Major brands now stipulate heavy-metal-free portfolios, encouraging the migration toward synthetic mica and borosilicate glass bases that offer higher platelet uniformity and lower trace metals. Asia's K-beauty innovators accelerate trend cycles, shortening product lifetimes and forcing pigment suppliers to operate agile, small-batch manufacturing that can deliver bespoke shades within weeks. While margin potential rises, sustainment costs climb as firms must certify worldwide compliance dossiers for each new hue.

REACH dossier updates demand exhaustive toxicological data for aluminum and copper flakes, obliging smaller pigment companies to allocate disproportionate compliance budgets or exit the region. Simultaneously, the move from solvent to water-borne binders forces reformulation because traditional leafing agents dissolve or gas in alkaline media. Suppliers equipped with proprietary encapsulation and passivation know-how can transform regulatory friction into loyalty-building service, but late adopters are confronting prolonged approval cycles that erode revenue.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pearlescents held 51.02% of the special-effect pigments market share in 2025 and are forecast to maintain the fastest 4.07% CAGR to 2031, confirming their dual status as volume and growth leader. Glass-flake and synthetic mica formulations widen the application canvas by providing radar transparency and ultralow heavy-metal content, attributes prized in electric-vehicle exteriors and luxury-cosmetic powders. The special-effect pigments market benefits as OEM clear-coat layers integrate variable-thickness lamellae that produce color-travel with minimal flop, cutting paint-shop passes and lowering cycle times.

Metallic grades retain core positions in protective topcoats, yet their share of the special-effect pigments market is slipping where radar compliance outranks sparkle intensity. Vendors with advanced silica encapsulation processes defend margins by licensing technology to regional tollers, securing scale without dilution of intellectual property. Optically variable and holographic pigments serve security inks and brand-protection labels; although collectively smaller, they achieve above-average pricing and bolster portfolio profitability, ensuring they remain a strategic extension rather than a commodity add-on.

The Special-Effect Pigments Report is Segmented by Pigment Type (Metallic, Pearlescent, and Other Pigment Types), End-User Industry (Paints and Coatings, Cosmetics, Plastics, Printing Inks, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 45.12% of the special-effect pigments market size in 2025 and is tracking a 4.55% CAGR through 2031, consolidating its role as the global manufacturing hub. China's dominance in automotive coatings underpins regional demand, while India's 7%-plus growth in decorative paints generates incremental volume for pearlescent dispersions. Government incentives for electric-vehicle localization attract foreign assemblers that mandate identical color libraries across continents, encouraging pigment makers to establish in-region technical-service labs. Southeast Asian electronics clusters in Vietnam and Malaysia further diversify downstream channels, absorbing high-purity effect grades for smartphone casings and wearable housings.

Europe wields regulatory influence that shapes worldwide formulation standards. REACH and the 2023 microplastics restriction accelerate the pivot to bio-based surfactants and encapsulated metal flakes, a policy environment that rewards early movers with defensible premium pricing. German and Italian automotive OEMs commit to low-film-thickness clearcoats that intensify optical flop per micron, pushing pigment suppliers toward higher aspect-ratio platelets and tighter particle-size control. In architectural coatings, Nordic countries specify near-zero VOC benchmarks that quickly propagate across the continent, ratcheting technical barriers for imported formulations lacking water-borne credentials.

North America maintains a sizable automotive refinish ecosystem, ensuring predictable pull for metallic and pearlescent touch-up products. The U.S. Food and Drug Administration's permanent listing of mica as an exempt color additive stabilizes raw-material selection for cosmetics effect pigments, streamlining certification for new color launches. Mexico's ascendant vehicle assembly footprint heightens cross-border pigment logistics, with U.S. suppliers leveraging near-shoring to cut lead times. The Middle East and Africa offer long-run upside as infrastructure programs accelerate decorative-coatings use; however, limited local production capacity means import dependence persists, advantaging multinationals with integrated freight networks. South America's pigment demand centers on Brazil's automotive belt, though currency volatility necessitates hedging strategies to manage revenue repatriation.