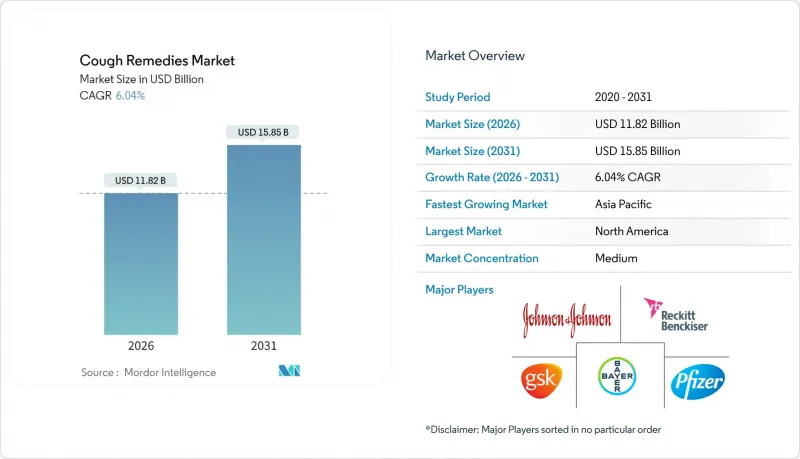

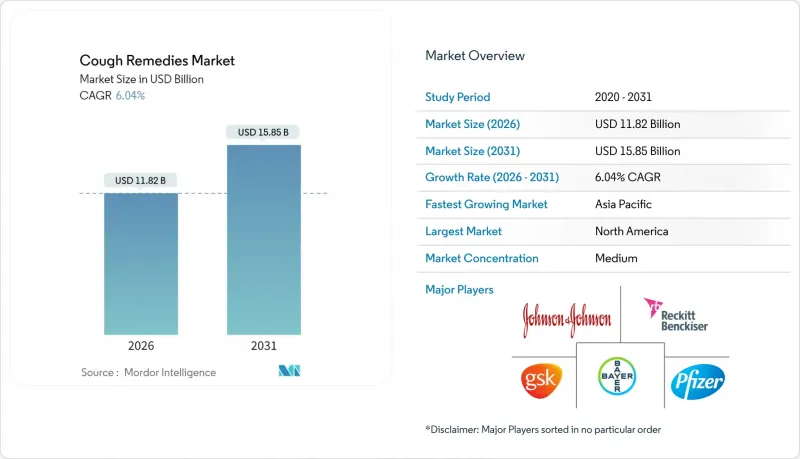

기침약시장은 2025년 111억 5,000만 달러에서 2026년에는 118억 2,000만 달러로 성장하고, 2026-2031년 CAGR 6.04%로 성장을 지속하여, 2031년까지 158억 5,000만 달러에 이를 것으로 예측됩니다.

안정적인 수요는 호흡기 질환의 높은 유병률, 소비자들이 처방전 없이도 치료를 받을 수 있는 규제 프레임워크, 성분 규제를 통한 제품 재설계가 활발하게 이루어지고 있기 때문입니다. 비오피오이드계 진해제 성분의 기술 혁신이 가속화되고 있으며, 제조업체들은 코데인 및 페닐에프린 규제 강화에 대한 대응책으로 이를 활용하고 있습니다. 한편, 디지털 소매의 확대와 셀프 케어 행동 증가로 인해 전자 약국에 대한 판매량이 증가하고 있으며, 전체 기침약 시장의 경쟁 우선순위를 재구성하고 있습니다. 정책 환경 변화에 대응할 수 있는 차별화된 호흡기 자산을 찾는 다국적 제약사 간 통합이 심화되고 있습니다.

2억 1,300만 명 이상이 만성 호흡기 질환을 앓고 있으며, 하기도 감염은 여전히 사망원인 5위를 차지하고 있어 예방적 기침 관리는 임상현장에서 중요한 과제입니다. COPD 관련 사망의 약 90%는 중저소득 국가에서 발생하며, 처방전 없이 구입할 수 있는 저렴한 치료제에 대한 지속적인 수요가 발생하고 있습니다. 역학 연구에 따르면, 만성 기침은 수면의 질 저하와 직장 내 생산성 저하와 관련이 있다는 사실이 밝혀지면서 환자들은 기존의 대증요법보다 더 효과적인 대안을 찾고 있습니다. GARD와 같은 세계 협력은 조기 개입과 지역 차원의 인식 제고 활동을 강화하여 기침약 시장의 잠재적 고객 기반을 확대하고 있습니다. 아시아태평양(APAC)과 중동 및 아프리카(MEA)에서 발병률과 인지도가 높아짐에 따라 다국적 제조업체들은 공급망 강화와 지역 기반 마케팅을 통해 증가하는 수요를 충족시키기 위해 노력하고 있습니다.

규제 당국은 특정 처방약 성분이 특정 조건 하에서 OTC 시장으로 전환할 수 있는 길을 열어 놓았습니다. 미국에서는 2024년 '비처방 사용 추가 조건(ACNU)'을 제정하여 금기 사항을 선별하는 전자 문진표에 응답한 후 더 강력한 기침약을 사용할 수 있도록 했습니다. 베트남은 2025년 약국법을 개정하여 승인된 의약품의 전자상거래 판매를 승인했습니다. 이를 통해 신청 서류 처리 기간이 단축되고, 혁신 기업 시장 진입 비용이 절감되었습니다. 간소화된 유통 경로를 통해 기업은 현재 성분 금지의 위협을 받고 있는 기존 제품의 재처방 및 재포지셔닝을 촉진하고, 기침약 시장 전체공급 다양성을 유지할 수 있습니다. 또한, 일반의약품의 접근성 확대는 단순 기침에 대한 일상적인 의사 방문을 줄여 의료시스템의 효율화 목표를 지원합니다.

성분 심사 강화로 인해 제품 포트폴리오가 축소되고, 컴플라이언스 비용이 증가하고 있습니다. 영국에서는 2024년 코데인 액제가 OTC에서 처방약으로 전환되었는데, 이는 상담 응답자의 59%가 오남용 위험성을 지적한 이후 규제 강화 추세를 상징하는 사례입니다. 미국 FDA 심사관은 경구용 페닐에프린이 측정 가능한 효과가 없습니다는 결론을 내렸고, 연간 약 18억 달러의 소매 수익이 위험에 처해있습니다. 유럽 가이드라인은 복합 허브 활성 성분에 대해 10년 이상의 문헌적 증거를 요구하고 있어 빠른 제품 라인 확장을 방해하고 있습니다. 향후 덱스트로메토르판이 처방약으로 전환될 경우, 이해관계자들은 의사들의 진료 횟수와 생산성 손실이 210억-310억 달러 증가할 것으로 예상하고 있어 그 경제적 파급효과가 얼마나 큰지 알 수 있습니다. 소규모 제조업체는 전 세계 각국의 서로 다른 기준을 충족하기 위해 필요한 임상시험 자금 조달에 있어 특히 큰 부담에 직면해 있습니다.

복합제는 2025년 기준 기침약 시장의 34.29%를 차지하며, 기침, 코막힘, 발열을 한 번에 완화하는 제품에 대한 소비자 수요를 반영하고 있습니다. 이 부문의 강점은 감기/독감 유행 시기에 다른 카테고리와의 교차 프로모션, 쓴맛이 나는 유효성분을 가리는 코팅정 등 부가가치가 높은 제형에 있습니다. 허브/천연 성분 제품군은 원재료에 대한 회의적인 시각이 높아지면서 보다 순한 제품을 찾는 소비자들로 인해 CAGR 8.54%로 신규 가구를 확보했습니다. 임상 문헌에서 백리향과 프리메라 혼합물 등 식물성 성분의 효능이 합성 비교약과 동등한 효과를 나타내는 것이 지속적으로 입증되어 약사들 사이에서 신뢰도를 높이고 있습니다. 진해제의 혁신은 코데인을 대체할 P2X3 또는 TRP 채널 차단제에 초점을 맞추었습니다. 한편, 구아이페네신을 주성분으로 하는 거담제는 가래성 기침에 대한 의사들의 지지로 판매량을 유지하고 있습니다. 점액 용해제는 폐색성 폐질환에 대한 적용 범위가 확대되어 만성질환자 기침약 시장 규모에 추가적인 판매량을 가져오고 있습니다.

2차적인 영향도 나타나고 있습니다. 페닐에프린이 함유된 충혈 제거제는 재처방이 필요하고, 소매점에서는 플라노그램을 조정해야 하며, 허브 및 식염수 기반 스프레이에 새로운 선반 공간을 제공해야 합니다. FDA의 구미 제형 승인은 새로운 경구용 제형에 대한 규제 당국의 관용을 보여주며, 아연 강화 츄어블과 허니 라벤더 맛의 용해성 정제 등 다양한 브랜드의 실험적 개발을 촉진하고 있습니다. 항균제 관리의 추진으로 바이러스 감염에 대한 항생제 사용이 억제되고, 항생제 보조제는 감소하는 추세입니다. 이를 통해 연구 개발 자금은 면역 지원 식물 성분과 기침 반사 조절제 등에 재분배되고 있습니다.

2025년 기준 기침약 시장의 58.10%를 시럽-린투스가 차지하고 있으며, 부드러운 입맛과 빠른 점막 흡수로 성인부터 어린이까지 선호하고 있습니다. 그러나 구미젤리, 젤리, 박막제의 선호도 향상으로 8.63%의 연평균 복합 성장률(CAGR)을 기록함. 바쁜 부모들이 이동 중에도 복용할 수 있는 얼룩이 잘 묻지 않는 개별 포장을 선호하는 경향이 있습니다. 각 제조업체들은 펙틴이나 젤라틴 기질을 활용하여 표준 USP 유효성분을 함유하고 있습니다. 재방문 고객을 확보하기 위해 맛의 유형을 확대하는 중입니다. 정제-캡슐은 낮에 몰래 복용하고 싶은 성인 전문직 종사자들의 필수품으로, 서방형 비드는 효과 지속 시간을 연장하여 근무 교대 근무를 커버할 수 있습니다. 트로치는 목구멍에 집중적인 윤활을 제공하고, 새로 개발된 무설탕 포뮬러는 당뇨병 환자나 칼로리를 걱정하는 소비자를 위한 제품입니다. 진화하는 건강 트렌드 속에서 존재감을 유지하고 있습니다.

2025년 발표된 규제 개정으로 단일제제 보유자는 신약 신청서 제출 없이 고형 경구용 제형 간 전환이 가능해져 라이프사이클 관리의 가속화와 신속한 기술 전환이 가능해졌습니다. 비강 스프레이는 상기도 충혈에 대한 국소 작용을 활용하여 알레르기 시즌에 맞추어 수요가 급증하는 경향이 있으며, 기침 증상이 감소하는 시기에 대한 헤지 기능을 제공합니다. 증기흡입제나 증기흡입제는 특히 경구용 다제 병용이 우려되는 노인시설에서 촉각적 편안함을 원하는 간병인을 위한 치료법으로 계속 활용되고 있습니다.

북미는 2025년 전 세계 매출의 38.10%를 차지하며 가장 큰 비중을 차지할 것으로 예측됩니다. 높은 보험 적용률, 광범위한 소매 약국 네트워크, 기술을 활용한 셀프케어의 조기 도입이 그 기반이 되고 있습니다. 각 제조업체들은 감기-독감 유행 시기에 맞추어 전국적인 TV 광고와 소셜 미디어 캠페인에 막대한 홍보 예산을 투입해 브랜드 선호도를 강화하고 있습니다. 유효 성분에 대한 FDA의 지속적인 심사는 예측에 불확실성을 야기하지만, 성숙한 제품 라인에 활력을 불어넣는 재처방 파이프라인의 촉매제가 될 수 있습니다. 미국이 차세대 P2X3 길항제 임상시험의 중심지로 자리 잡으면서 미국이 혁신의 출발점으로서의 역할을 강화하고 있습니다. 캐나다의 적극적인 코데인 규제는 마케터들이 비오피오이드 제품군을 더욱 두드러지게 포지셔닝하도록 강요하고 있으며, 기침약 시장 상황을 미묘하게 재구성하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 시장으로 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.46%를 나타낼 것으로 예측됩니다. 이는 급성장하는 중산층의 소비, 도시화, 제품 승인 속도를 높이는 규제 현대화에 힘입은 것입니다. 중국과 인도는 큰 시장 기회를 가지고 있지만, 가격 통제와 언어의 다양성으로 인해 세밀한 세분화 전략이 요구됩니다. 일본에서는 고령화에 따라 만성질환용 거담제, 점액용해제에 대한 안정적인 수요가 지속되고 있습니다. 한편 베트남에서는 전자상거래의 합법화로 인해 지역 거점으로부터의 국경 간 배송이 확대되고 있습니다. 호주 당국은 증거에 기반한 자연요법을 권장하는 지역 약국 실무 표준에 기침약을 포함시켜 SKU의 다양화를 촉진하고 있습니다. 이러한 추세와 맞물려 아시아태평양의 기침약 시장 규모는 확대되는 반면, 국내 제네릭 의약품과의 경쟁은 더욱 치열해지고 있습니다.

유럽은 성숙한 수요와 엄격해지는 규제의 균형을 맞추고 있습니다. 영국 내 코데인 제제의 재분류와 역내 페닐에프린의 효능에 대한 이슈로 인해 기업들은 주력 SKU를 재설계해야 하는 상황에 처해 있으며, 일시적으로 매장 내 공급이 부족합니다. 한편, 유럽의약품청(EMA)의 새로운 호흡기 백신 승인은 항기침제 연구에도 영향을 미칠 수 있는 과학적 리더십의 지속을 강조하고 있습니다. 독일은 유럽에서 가장 큰 수익원이며, 취약 계층을 위한 특정 OTC 기침약에 대한 보험 적용을 위한 탄탄한 제도가 뒷받침되고 있습니다. 남유럽 시장에서는 전통적 식물요법에 따른 허브 시럽의 채택이 증가하고 있으며, 지역별로 제품 구성의 차이가 심화되고 있습니다.

남미와 중동 및 아프리카에서는 소규모 기반에서 두 자릿수 가치 성장을 보이고 있습니다. 브라질과 멕시코의 도시 약국에서는 복합 기침약의 진열대 배치가 현대화되어 구매에 대한 거부감이 줄어들고 구매량이 증가하고 있습니다. GCC 국가에서는 만성 호흡기 질환 치료의 보험 적용 범위가 확대되면서 고수익률의 비오피오이드계 흡입제가 수혜를 받고 있습니다. 사하라 이남 아프리카에서는 소아 폐렴 진단 키트를 배포하는 기증자 지원 프로그램이 기침 증상 관리에 대한 부모들의 인식 개선에 간접적으로 기여하고 있지만, 여전히 저렴한 가격이 문제점으로 지적되고 있습니다.

The cough remedies market is expected to grow from USD 11.15 billion in 2025 to USD 11.82 billion in 2026 and is forecast to reach USD 15.85 billion by 2031 at 6.04% CAGR over 2026-2031.

Steady demand stems from the high prevalence of respiratory diseases, regulatory frameworks that preserve consumer access to non-prescription care, and a brisk pace of product reformulation prompted by ingredient rulings. Innovation is accelerating in non-opioid antitussive compounds, helping manufacturers counterbalance tighter codeine and phenylephrine restrictions. Meanwhile, digital retail expansion and rising self-care behaviors are channeling more volume toward e-pharmacies, reshaping competitive priorities across the cough remedies market. Consolidation among multinational drug makers is intensifying as firms seek differentiated respiratory assets that can weather shifting policy landscapes.

Over 213 million individuals are living with chronic respiratory disease, while lower respiratory infections remain the fifth-leading cause of death, keeping preventive cough management high on clinical agendas. About 90% of COPD-related deaths occur in low- and middle-income countries, creating sustained demand for accessible therapies that can be purchased without a prescription. Epidemiological studies also link chronic cough to poor sleep quality and reduced workplace productivity, prompting patients to seek more effective options than traditional symptomatic relief. Global alliances such as GARD reinforce early intervention and community-level education that enlarge the addressable base for the cough remedies market. As incidence and awareness rise in APAC and MEA, multinational manufacturers are ramping up supply chains and localized marketing to capture incremental volume.

Regulators are opening pathways that allow certain prescription molecules to migrate into OTC settings under structured conditions. The United States enacted Additional Conditions for Nonprescription Use (ACNU) in 2024, enabling consumers to secure stronger cough remedies after completing an electronic questionnaire that screens for contraindications. Vietnam revised its pharmacy law in 2025 to authorize e-commerce sales of approved medicines, shortening dossier processing and lowering market-entry costs for innovators. Simplified routes to shelf encourage firms to reformulate or reposition legacy products now threatened by ingredient bans, thereby maintaining supply diversity across the cough remedies market. Wider OTC availability also reduces routine physician visits for uncomplicated cough, supporting health-system efficiency goals.

Ingredient reviews are shrinking product portfolios and inflating compliance costs. The United Kingdom's 2024 switch of codeine linctus from OTC to prescription-only status typifies the tightening trend after 59% of consultation respondents cited misuse risks. In the United States, FDA reviewers concluded that oral phenylephrine lacks measurable benefit, jeopardizing nearly USD 1.8 billion in annual retail revenue. European guidelines mandate 10-plus years of bibliographic evidence for combination herbal actives, hampering rapid line extensions. If future deliberations convert dextromethorphan to prescription status, stakeholders project a USD 21-31 billion surge in clinician visits and productivity losses, highlighting the financial stakes. Smaller manufacturers face particular strain financing the clinical work needed to satisfy diverging global standards.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Combination formulations commanded 34.29% cough remedies market share in 2025, a reflection of consumer appetite for single-dose relief covering cough, congestion, and fever. The segment draws strength from cross-category promotions during cold-and-flu spikes and from value-added delivery formats like coated tablets that mask bitter actives. Herbal / natural lines are winning new households at an 8.54% CAGR as shoppers seek gentler profiles amid rising ingredient skepticism. Clinical literature continues to validate botanicals such as thyme-primula blends that show non-inferior results to synthetic comparators, reinforcing their credibility among pharmacists. Antitussive innovation focuses on P2X3 or TRP channel blockers poised to replace codeine, while expectorants anchored by guaifenesin maintain volume through physician endorsement for productive cough. Mucolytics are also finding broader application in obstructive lung disease, adding incremental tonnage to the cough remedies market size for chronic-care patients.

Second-order impacts are emerging: decongestants containing phenylephrine will require reformulation, pushing retailers to adjust planograms and granting herbal or saline-based sprays new shelf space. FDA clearance of gummy formulations demonstrates regulator openness to novel oral vehicles, encouraging brands to experiment with zinc-enhanced chewables or honey-lavender melts. Antibiotic adjuncts are receding as antimicrobial stewardship discourages use in viral infections, reallocating R&D dollars toward immune-supportive botanicals and cough reflex modulators.

Syrups and linctuses held 58.10% of cough remedies market share in 2025, favored for soothing mouthfeel and rapid mucosal absorption that appeals to both adults and children. Yet palatability improvements in gummies, jellies, and thin films are fueling an 8.63% CAGR as busy parents favor mess-free packets for on-the-go dosing. Manufacturers are leveraging pectin or gelatin matrices to embed standard USP actives, broadening flavor libraries to win repeat purchase. Tablet and capsule formats remain staples for adult professionals seeking discreet daytime relief, while sustained-release beads lengthen efficacy windows to cover work shifts. Lozenges deliver targeted throat lubrication, and new sugar-free recipes cater to diabetic or calorie-conscious shoppers, maintaining relevance amid evolving health trends.

Regulatory updates announced in 2025 permit monograph holders to switch between solid oral forms without filing a new drug application, accelerating life-cycle management and enabling rapid technology migration. Nasal sprays capitalize on localized action for upper-respiratory congestion, and demand typically spikes alongside allergy season, offering a hedge against cooldowns in cough incidents. Vapor rubs and steam inhalants continue to serve caregivers seeking tactile comfort remedies, especially in geriatric settings where oral polypharmacy is a concern.

The Cough Remedies Market Report is Segmented by Product Type (Antitussives, Expectorants, and More), Dosage Form (Syrup/Linctus, Tablets & Capsules, and More), Age Group (Pediatrics & Adolescents (Below 18 Years), and More), Distribution Channel (Retail Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed the largest slice of global revenue at 38.10% in 2025, anchored by high insurance coverage, expansive retail pharmacy networks, and early adoption of technology-enabled self-care. Manufacturers allocate sizable promotional budgets toward national television and social media campaigns timed with cold-and-flu peaks, reinforcing brand preference. Ongoing FDA reviews of active ingredients inject some forecast uncertainty, yet they also catalyze reformulation pipelines that can rejuvenate mature labels. The United States remains the focal point for clinical trials of next-generation P2X3 antagonists, reinforcing the region's role as launchpad for innovation. Canada's proactive codeine limitations pressure marketers to position non-opioid lines more prominently, subtly reshaping the cough remedies market landscape.

Asia-Pacific is the fastest-growing theatre, clocking a 7.46% CAGR between 2026-2031, propelled by burgeoning middle-class consumption, urbanization, and regulatory modernization that expedites product approvals. China and India represent high-volume opportunities, though their pricing controls and linguistic diversity necessitate granular segmentation strategies. Japan's aging population drives steady demand for expectorants and mucolytics tailored to chronic conditions, while Vietnam's e-commerce legalization ushers in cross-border shipments from regional hubs. Australian authorities integrate cough remedies into community-pharmacy practice standards that endorse evidence-based natural medicines, encouraging SKU diversity. Collectively, these dynamics enlarge the cough remedies market size in APAC while intensifying competition from domestic generics.

Europe balances mature demand with increasingly stringent oversight. The reclassification of codeine formulations in the United Kingdom and phenylephrine efficacy challenges across the bloc force companies to re-engineer top-selling SKUs, temporarily tightening shelf supply. On the upside, European Medicines Agency approvals of novel respiratory vaccines spotlight continued scientific leadership that may spill over into antitussive research. Germany remains Europe's largest revenue generator, sustained by a robust insurance system that reimburses certain OTC cough aids for vulnerable populations. Southern European markets see rising uptake of herbal syrups aligned with traditional phytotherapy practices, reinforcing regional product-mix nuance.

South America and the Middle East & Africa are displaying double-digit value growth from a small base. Urban pharmacies in Brazil and Mexico are modernizing layouts to stock combination cough remedies in frontline aisles, reducing stigma and increasing basket size. GCC countries expand insurance coverage for chronic respiratory treatments, benefiting high-margin non-opioid inhaled agents. In sub-Saharan Africa, donor-backed programs that distribute childhood pneumonia diagnostics are indirectly lifting parental awareness of cough symptom management, although affordability remains a constraint.