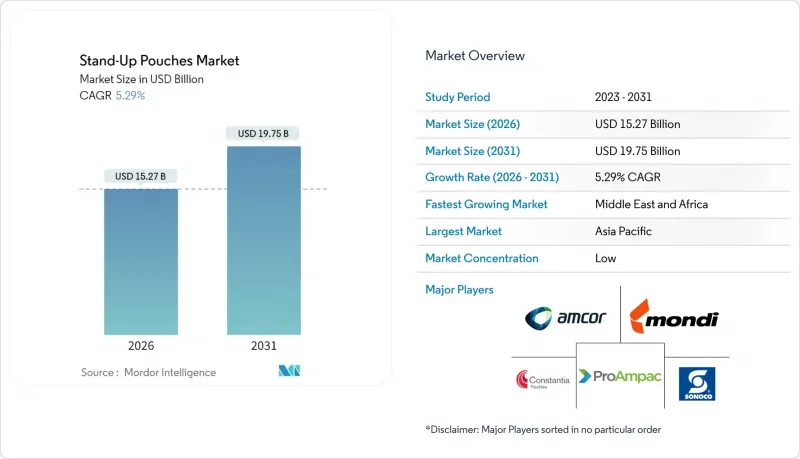

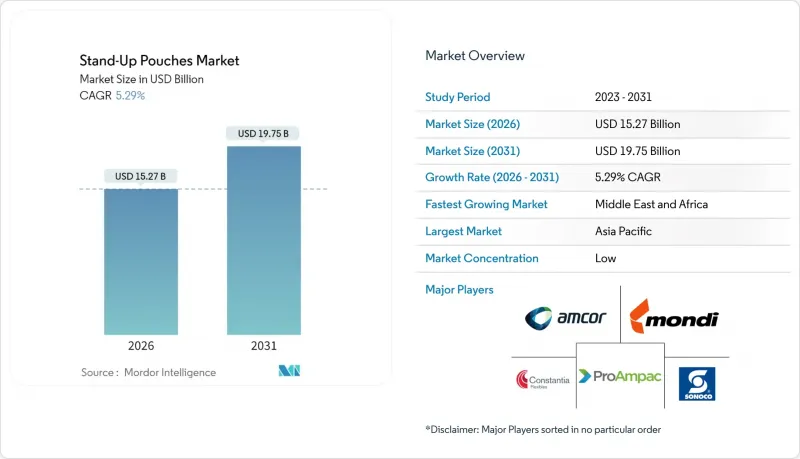

스탠드 업 파우치 시장 규모는 2026년에는 152억 7,000만 달러로 추정되고 있어 2025년 145억 달러에서 성장이 전망됩니다.2031년까지 예측에서는 197억 5,000만 달러에 이르고, 2026-2031년 CAGR 5.29%로 성장할 전망입니다.

가볍고 재밀봉이 가능하며 시각적으로 매력적인 포장에 대한 수요 증가가 이러한 성장세를 뒷받침하고 있습니다. 유럽의 규제 개혁, 동아시아의 기능성 음료 혁신, 북미 반려동물사료 브랜드의 경질 포장에서 연질 포장으로의 전환이 채택량 증가를 가속화하고 있습니다. 단일 소재의 재활용 가능한 포맷으로 조기에 전환하면 제조업체는 비용과 평판 측면에서 우위를 점할 수 있습니다. 한편, 핫필 및 레토르트 성능의 향상으로 식품, 음료 및 가정용품 카테고리 전반에 걸쳐 최종 용도의 가능성이 확대되고 있습니다. 아시아태평양의 생산 규모 확대, 라틴아메리카의 기술 업그레이드, 그리고 Amcor, Mondi, Sonoco가 주도하는 활발한 M&:A 파이프라인은 기업들이 효율성과 순환성을 추구하면서 경쟁의 경계를 재정의하고 있습니다.

2025년 2월부터 시행되는 유럽연합 포장 및 포장 폐기물 규제에 따라 2030년까지 모든 소비자용 포장재의 재활용과 플라스틱 포장재의 재활용 플라스틱 함량 30% 이상 의무화가 시행됩니다. 각 제조업체들은 다층 알루미늄 구조에서 단일 소재 폴리에틸렌 필름으로 빠르게 전환하고 있으며, 일반 가정용 재활용 시스템과의 호환성을 유지하고 있습니다. 암코의 리키플렉스 앰플리마 파우치는 이러한 기준을 충족하며, 기존 라미네이트 대비 이산화탄소 배출량을 79%, 물 사용량을 84% 줄인 것으로 보고되고 있습니다. 일찍 도입하는 브랜드 소유자는 확대 생산자 책임(EPR) 비용 절감과 진열 효과 향상을 통한 소구력 강화를 기대할 수 있지만, 늦게 대응하는 기업은 R&D 비용 상승과 진열 공간 손실의 위험에 직면할 수 있습니다. 이 전환은 컨버터가 새로운 씰링 기술을 라이선싱하고 장벽 성능을 손상시키지 않으면서 필름의 두께를 얇게 만들어 스파우츠 파우치 시장을 강화할 수 있도록 합니다.

동아시아 소비자들은 휴대용 단백질 쉐이크, 비타민 젤, 식사 대용 음료 등을 적극적으로 받아들이고 있습니다. 85℃ 이상의 내열성으로 가공업체는 방부제를 생략하고 상온 보관 기간을 연장하여 영양가 높은 배합을 실현할 수 있습니다. 일본 방재용품 코너에서는 모리나가제과의 5년 보관이 가능한 '인제리 에너지 롱라이프' 파우치가 주목받고 있으며, 극한의 차단성과 레토르트 성능에 대한 기대감을 뒷받침하고 있습니다. 한국의 한 스타트업 기업은 밀레니얼 세대 여성을 타겟으로 한 단백질 믹스용 1인분 용기를 판매하며 전년 대비 3배의 매출을 올리고 있습니다. 이러한 혁신적인 제품은 동남아시아의 편의점과 고급 체육관에서 채택을 촉진하고, 스탠드업 파우치 시장에 새로운 수요 창출의 길을 열어주고 있습니다.

미국에서는 2030년까지 플라스틱 재활용률을 61%까지 끌어올리기 위해 360억-430억 달러의 인프라 구축이 필요합니다. 재료 회수 시설이 유연한 라미네이트 재료를 식별하고 분류 할 수있을 때까지 브랜드 소유자는 다층 파우치를 확장하는 데 신중합니다. 따라서 제조업체들은 단일 소재의 개발을 가속화하고 있지만, 전환 비용과 기존 설비의 위험으로 인해 스탠드업 파우치 시장의 성장이 일시적으로 둔화되고 있습니다.

2025년 기준, 플라스틱 구조가 스탠드업 파우치 시장의 71.17%를 차지했습니다. 이는 가공업체가 폴리에틸렌의 밀봉성, 폴리프로필렌의 내열성, PET의 투명성을 중시했기 때문입니다. 생분해성 옵션은 규제와 소비자 수요에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 6.78%를 나타낼 것으로 예측됩니다. 다만, 소량 SKU에 대한 대응은 여전히 과제입니다. 아크레드 패키징의 사탕수수 유래 수지 파우치는 단위당 43g의 CO2를 상쇄하면서 기존 설비에서 가공성을 실현하고 있습니다.

한편, 암코의 AmFiber 종이 기반 배리어 라미네이트는 알루미늄이 함유되지 않은 유통기한을 원하는 스낵 제조업체를 타겟으로 하고 있습니다. 특수 EVOH 배리어와 나일론 타이 층은 산소에 민감한 충전재를 계속 보호하고 있지만, 비용 상승으로 인해 고부가가치 뉴트리슈티컬 제품 라인으로 재배치되고 있습니다. 생분해성 스탠드업 파우치 시장 규모는 2029년까지 10억 8,000만 달러 이상에 달할 것으로 예상되지만, 플라스틱은 여전히 식음료 분야의 주력 소재로서의 지위를 유지할 것으로 예측됩니다. 재활용 설계 가이드라인의 진화는 빠른 실험을 촉진하고, 스탠드업 파우치 시장에서 플라스틱은 기존 기술과 혁신의 기반이 되고 있습니다.

둥근 바닥(도이엔) 파우치는 성숙한 성형 장비와 광범위한 응용 분야로 인해 2025년 38.11%의 매출 점유율을 차지할 것으로 예측됩니다. 한편, 사각 바닥 디자인은 바닥의 안정성 향상으로 인해 5.52%의 연평균 복합 성장률(CAGR)로 성장을 보이고 있으며, 2차 포장 없이도 더 큰 충전 용량을 지원합니다. K-Seal 및 Delta Seal 사양은 변조 방지 기능을 원하는 의약품 충전업체에서 선호하고 있습니다. 외식업계 바이어들은 소스 및 조미료용 2L 및 5L 코너 하단 파우치를 찾고 있으며, 팔레트 효율성과 HDPE 병 대비 79%의 배출량 감소를 이유로 꼽고 있습니다.

그러나 1리터 이상 SKU의 레토르트 처리 시 헤드스페이스 관리, 유럽 수프 라인의 보급 지연 등 기술적 과제는 여전히 남아있습니다. 거싯 모양과 캡 벤트에 대한 지속적인 연구개발을 통해 압력차를 최소화하여 스탠드업 파우치 시장에서의 새로운 점유율 확대가 기대됩니다.

2025년 스탠드업 파우치 시장에서 아시아태평양은 38.21%의 점유율로 1위를 차지했습니다. 이는 중국의 대규모 가공시설, 일본의 핫필 기술 개발, 한국의 프리미엄화 전략에 힘입은 것입니다. 2025년까지 500만 톤의 신규 생산능력이 추가될 것으로 예상되는 폴리에틸렌 공급과잉은 필름 가격을 압박하고 있으며, 가공업체에게는 원재료 조달 측면에서의 우위를 가져다주지만, 수익률에 압박을 가하고 있습니다. 암콜이 구자라트주의 피닉스 플렉서블즈를 인수하면서 인도의 2,000만 달러 규모의 의료용 포장 틈새 시장 진출이 확대되고 현지 생산이 가속화되고 있습니다.

북미는 잘 구축된 식품 가공 인프라와 반려동물 우선주의 문화를 배경으로 안정적인 수요가 유지되고 있습니다. 인프라 격차는 심각하며, 2030년까지 자재 회수 시설을 현대화하기 위해서는 400억 달러의 자금이 필요합니다. 임박한 25%의 수지 관세는 비용 압박을 증폭시키지만, 한편으로는 지역의 수지 투자 및 재생수지의 시범 도입을 촉진하고 있습니다. 캘리포니아주의 2026년 재활용 소재 함유 의무화 정책과 함께 이러한 정책은 스탠드업 파우치 시장을 단일 소재 PE 레토르트 형태로 이끌고 있습니다.

유럽은 규제의 선구자로서 스탠드업 파우치 시장 전체에 재활용을 고려한 설계를 의무화하고 있습니다. Amkor, Mondi, Bischoff + Klein 등의 선도기업들은 이미 30% PCR 기준을 충족하고 PET/알루미늄/OPE 3중 구조 대비 79%의 CO2를 저감하는 PP 및 PE 단층 파우치 상용화에 성공했습니다. 북유럽의 리필 프로그램은 저탄소 포장이 온라인 편의성과 결합될 때 소비자의 수용이 빠르게 진행될 수 있다는 것을 입증하고 있습니다.

라틴아메리카는 생산 능력의 핫스팟으로 부상하고 있습니다. 브라질에서는 식품 산업이 7.2%의 성장률을 기록했으며, 펩시콜라의 2억 4,000만 달러 규모의 공장 확장으로 인해 2025년에는 8레인 파우치 충전 기계 3대가 가동될 예정입니다. 멕시코와 콜롬비아는 순환형 포장 투자에 대한 세액공제를 연장하여 다국적 컨버터 기업을 유치하고, USMCA(미국-멕시코-캐나다 협정)의 규정에 따라 미국으로의 수출 루트를 개척하고 있습니다.

중동 및 아프리카은 8.39%의 가장 빠른 CAGR을 기록했으며, 무균 우유, 향이 있는 물, 알루미늄이 없는 파우치형 과일즙이 견인차 역할을 했습니다. SIG의 케냐에서의 Prime 55 도입과 테트라팩의 나이지리아 프로모션 캠페인은 진입장벽을 낮추고 있습니다. 에너지 절약형 살균 기술과 저렴한 가격의 피팅 부품은 스탠드업 파우치 시장의 지역 성장을 가속하는 주요 성공 요인으로 자리매김하고 있습니다.

Stand-up pouches market size in 2026 is estimated at USD 15.27 billion, growing from 2025 value of USD 14.5 billion with 2031 projections showing USD 19.75 billion, growing at 5.29% CAGR over 2026-2031.

Rising demand for lightweight, resealable, and visually engaging packaging underpins this growth momentum. Regulatory reforms in Europe, functional-beverage innovation in East Asia, and a shift from rigid to flexible packaging among North American pet food brands are accelerating volume adoption. Early moves toward mono-material, recyclable formats provide manufacturers with cost and reputation advantages, while improvements in hot-fill and retort performance broaden end-use possibilities across the food, beverage, and household categories. Production scale in Asia-Pacific, technology upgrades in Latin America, and a vibrant M&A pipeline led by Amcor, Mondi, and Sonoco are redefining competitive boundaries as companies chase efficiency and circularity.

The European Union Packaging and Packaging Waste Regulation, effective as of February 2025, requires all consumer packs to be recyclable by 2030 and to contain at least 30% post-consumer recycled content for plastics. Producers are rapidly transitioning from multi-layer aluminum structures to mono-material polyethylene films, which remain compatible with curbside recycling streams. Amcor's Liquiflex AmPrima pouch meets these criteria and reports a 79% reduction in carbon emissions, alongside an 84% decrease in water use compared to legacy laminates. Brand owners who adopt early see lower extended producer responsibility fees and improved shelf-appeal messaging, while late movers face R&D cost spikes and possible loss of shelf space. The pivot strengthens the spouted pouches market as converters license new sealing technologies and downgauge films without compromising barrier integrity.

East-Asian consumers are embracing protein shakes, vitamin gels, and meal-replacement drinks in portable portions. Hot-fill tolerance beyond 85 °C allows processors to skip preservatives, extend ambient shelf life, and deliver nutrient-dense formulas. Japan's disaster-preparedness aisle now features Morinaga Seika's five-year "in Jelly Energy Long Life" pouch, validating extreme barrier and retort performance expectations. Start-ups in South Korea triple their year-over-year sales by marketing single-serve spouts for protein mixes targeting female millennials. These breakthroughs inspire adoption in Southeast-Asian convenience stores and premium gyms, giving the stand-up pouches market fresh volume pipelines.

The U.S. requires USD 36-43 billion in infrastructure upgrades to lift plastics recycling rates to 61% by 2030. Until material recovery facilities can recognize and separate flexible laminates, brand owners hesitate to scale multilayer pouches. Producers are therefore accelerating the development of mono-materials, but transition costs and legacy equipment risks temporarily slow the growth of the stand-up pouches market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic structures controlled 71.17% of the stand-up pouches market in 2025 as processors valued polyethylene's sealability, polypropylene's heat stability, and PET's clarity. Biodegradable options are projected to record a 6.78% CAGR through 2031, driven by regulatory and consumer demand, while still addressing small-run SKUs. Accredo Packaging's sugarcane-derived resin pouch offsets 43 grams of CO2 per unit while offering drop-in machinability.

Meanwhile, Amcor's AmFiber paper-based barrier laminate targets snack producers searching for aluminum-free shelf life. Specialty EVOH barriers and nylon tie layers continue to protect oxygen-sensitive fillings, but cost spikes reposition them toward high-value nutraceutical lines. The stand-up pouches market size for biodegradable grades is projected to cross USD 1.08 billion by 2029, yet plastics will still anchor core food and beverage volumes. Evolving design-for-recycle guidelines stimulate rapid experimentation, positioning plastics as both incumbent and innovation canvas in the stand-up pouches market.

Round-bottom (Doyen) pouches accounted for a 38.11% revenue share in 2025, thanks to their mature forming equipment and broad application adoption. Corner-bottom designs, however, exhibit a 5.52% CAGR growth due to improved base stability, which supports larger fill volumes without requiring secondary cartons. K-Seal and Delta-Seal variants appeal to pharmaceutical fillers requiring tamper-evident integrity. Foodservice buyers are pursuing 2-L and 5-L corner-bottom pouches for sauces and condiments, citing pallet efficiency and 79% emission savings compared to HDPE bottles.

Nonetheless, technical challenges, chiefly headspace management during retort for SKUs exceeding 1 L, and slow migration in European soup lines, persist. Continuous R&D in gusset geometry and cap venting aims to minimize pressure differentials, promising to unlock new market share gains in the stand-up pouches market.

The Stand-Up Pouches Market Report is Segmented by Material Type (Plastic, Paper, and More), Product Type (Doyen/Round Bottom, K-Seal, and More), Application (Food, Beverage, Personal Care and Cosmetics, Healthcare and Pharmaceuticals, Pet Care, and Other Application), Distribution Channel (Direct Sales, and Indirect Sales), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific dominated with 38.21% share of the stand-up pouches market in 2025, underpinned by China's large-scale converting facilities, Japan's hot-fill R&D, and South Korea's premiumization playbook. Expected polyethylene oversupply, with 5 million tons of new capacity in 2025, is pressuring film pricing, offering converters raw-material leverage but compressing their margins. Amcor's acquisition of Phoenix Flexibles in Gujarat expands its reach into India's USD 20 million medical packaging niche and accelerates localized production.

North America leverages entrenched food-processing infrastructure and a pets-first culture to anchor steady demand. Infrastructure gaps loom large, with a USD 40 billion funding requirement to modernize material recovery facilities before 2030. Imminent 25% resin tariffs amplify cost pressures, yet they are also stimulating regional resin investment and trials using recycled resin. Coupled with California's 2026 recyclable-content mandate, such policies push the stand-up pouches market toward mono-material PE retort formats.

Europe stands at the regulatory vanguard, compelling design-for-recycling across the stand-up pouches market. Early adopters, including Amcor, Mondi, and Bischof + Klein, have already commercialized PP and PE single-web pouches that meet the 30% PCR threshold and deliver 79% CO2 cuts compared to PET/Alu/OPE triplex structures. Nordic refill programmes prove that consumer uptake can be rapid when lower-carbon packaging meets online convenience.

Latin America emerges as a capacity hotspot. Brazil registers 7.2% growth in the food industry, and PepsiCo's USD 240 million plant upgrade will commission three eight-lane pouch fillers in 2025. Mexico and Colombia extend tax credits for circular-packaging investments, attracting multinational converters and opening export corridors into the United States under USMCA provisions.

The Middle East and Africa experience the fastest CAGR at 8.39%, led by aseptic milk, flavored water, and fruit nectar packed in aluminum-free pouches. SIG's Prime 55 installation in Kenya and Tetra Pak's promotional campaigns in Nigeria lower entry barriers. Energy-efficient sterilization and affordable fitment remain key success factors poised to drive regional growth within the stand-up pouches market.