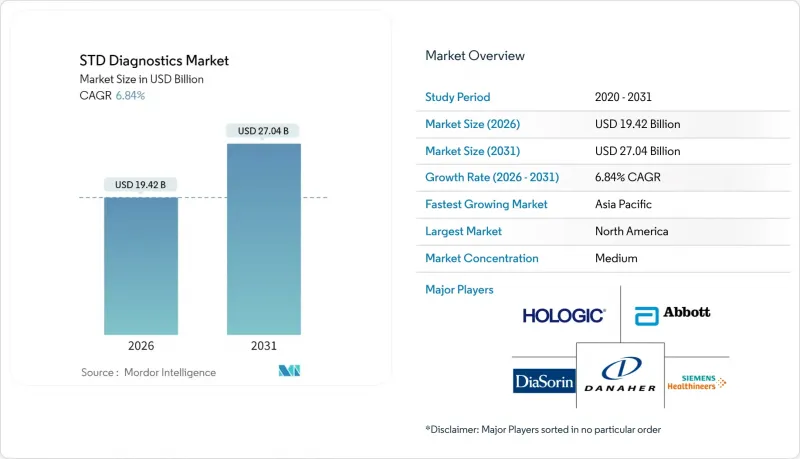

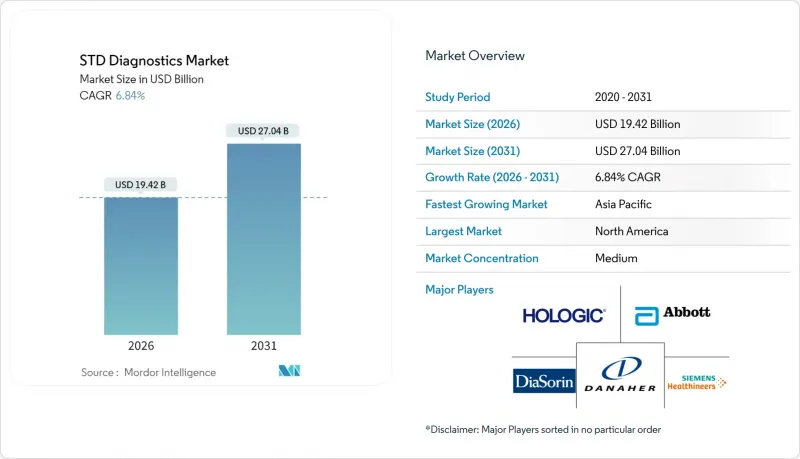

성병(STD) 진단 시장은 2025년에 181억 8,000만 달러로 평가되었고, 2026년 194억 2,000만 달러에서 2031년까지 270억 4,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.84%로 예상됩니다.

이러한 성장은 미국 내 매독 확진자가 80% 급증(2022년 확진자 수가 207,000명을 넘어섰음)하고, 이러한 추세를 억제하기 위한 연방정부 태스크포스가 설치되면서 가속화되고 있습니다. 세계보건기구(WHO)는 현재 2022년 전 세계 매독 감염 건수를 800만 건으로 추산하고 있으며, 이는 성인 감염을 90% 감소시키겠다는 2030년 목표와의 격차를 더욱 부각시키고 있습니다. 성병(STI)의 총 발생률은 1990년 이후 58.38% 증가했으며, 특히 저소득 지역에서 심각한 부담이 발생하고 있습니다. 규제 측면에서는 2025년 5월 FDA가 핵산 STI 검사를 Class II로 재분류하고, 혁신 플랫폼의 승인 주기를 단축하는 등 규제 강화 움직임이 계속되고 있습니다. 보험사는 2024년 5월에 예방 서비스표를 업데이트하여 성병 검진을 무료로 보장하고, 정기 검진 횟수를 확대했습니다. 그러나 여전히 68%의 개인은 수치심을 이유로, 85%는 의료진의 판단을 두려워하고 있으며, 재택 검사 및 디지털 연결형 진단에 대한 수요가 증가하고 있습니다.

세계보건기구(WHO)의 기록에 따르면, 2024년에는 매일 100만 건 이상의 새로운 성병이 발생했습니다. 클라미디아 및 임질 감염의 약 70%는 무증상이기 때문에 감염 사슬을 끊기 위해서는 정기적인 검사가 필수적입니다. 15-24세 Z세대와 젊은 밀레니얼 세대가 신규 확진자의 거의 절반을 차지함에 따라, 의료 시스템은 신속한 결과 제공과 재감염 연쇄 감염을 억제할 수 있는 신속한 PoC 검사를 도입해야 하는 상황입니다. 2024년 성병 병원체로 발견된 마우팍스는 기존 성병과 새로운 위협을 구분할 수 있는 다중 검사 패널이 임상의에게 필요하기 때문에 더 많은 진단 수요를 창출했습니다. 병원체와 내성 프로파일의 동시 검출을 통해 핵산 플랫폼은 확대되는 성병(STD) 진단 시장의 중심에 자리 잡고 있습니다.

미국 예방의학전문위원회(USPSTF)는 2024년 25세 미만의 성생활을 하는 모든 개인에게 클라미디아 및 임질에 대한 연례 검사를 권장하는 검진 가이드라인을 확대했습니다. 캐나다에서도 비슷한 움직임이 있었는데, 원주민 및 오지 지역 사회에서의 검사 확대에 7,400만 캐나다 달러(5,480만 달러)의 예산을 책정했습니다. 유럽연합 회원국들은 FDA 승인 또는 CE 마크를 획득한 분자 검사를 권장하는 가이드라인을 통일했습니다. 이러한 프로그램은 예측 가능한 조달 경로를 제공하고, 품질 기준을 강화하며, 1차의료, 공중보건, 지역사회에서 성병(STD) 진단 시장 규모를 확장하고 있습니다.

조사 데이터에 따르면, 성인의 43%가 타인의 평가나 사생활 침해에 대한 두려움 때문에 성병 검사를 미루거나 거부하는 것으로 나타났습니다. 특정 지역에서는 문화적 금기로 인해 검사가 성적으로 문란한 것과 동의어로 여겨져 여성의 생식 의료에 대한 접근이 불균형적으로 제한되고 있습니다. 2024년에 시작된 공중보건 캠페인은 검사를 일상적인 건강 지표로 재정의했지만, 보급률은 여전히 고르지 않습니다. 익명의 재택 검사 키트와 앱 예약제 진료 예약은 일부 사용자들의 낙인감을 줄이는 데 기여하고 있지만, 여러 관할권에서 원격의료에 대한 법적 제한이 보급 확대를 늦추고 있습니다. 학교 기반 성교육 시범사업은 실시지역에서 검사율을 25% 향상시켰으며, 커리큘럼이 전국적으로 확대되면 장기적인 효과가 기대됩니다.

HIV 검사 부문은 2025년 매출의 28.45%를 차지할 것으로 예상되며, 이는 혈액 서비스, 임산부 검진, 고위험군 정기 검사 의무화 정책이 정착된 것을 반영합니다. 매독 검사는 선천성 감염 억제를 위한 임산부 건강검진 의무화로 2위를 유지했습니다. 클라미디아 및 임질 검사는 성적으로 활동적인 젊은 층에 대한 연례 검사 권고에 힘입어 총 수익의 약 3분의 1을 창출했습니다.

마이코플라즈마 제니탈륨은 지속성 요도염에서의 역할에 대한 인식이 높아지면서 2031년까지 연평균 성장률(CAGR) 7.77%로 가장 높은 성장 전망을 보였습니다. HPV 및 HSV 분야는 다중 NAAT 검사를 통한 감별진단의 효율화로 꾸준한 성장세를 보이고 있습니다. 트리코모나스는 환자가 병원을 떠나기 전에 치료 가능한 감염을 감지하는 당일 검사 가능한 PoC 플랫폼의 혜택을 누리고 있습니다. 연성하수는 틈새 시장이지만, 분자 검출 정확도가 향상되면서 기존의 진단 누락이 줄어들고 있습니다.

분자진단 플랫폼은 2025년 50.78%의 점유율을 유지하며 가이드라인에 기반한 진료를 지원하는 신속하고 민감한 결과를 제공합니다. 면역 측정법은 자원이 한정된 환경에서 여전히 중요하지만, 정확도 문제가 시장 점유율 확대에 걸림돌이 되고 있습니다.

차세대 시퀀싱(NGS)은 병원체 및 내성 프로파일링을 동시에 수행할 수 있는 능력으로 인해 CAGR 9.13%를 나타낼 것으로 예측됩니다. 이 능력은 CDC와 같은 감시 기관으로부터 높은 평가를 받고 있으며, 2024년에는 4,500만 달러에 NGS 시스템 군을 구매했습니다. 바이오센서 및 마이크로플루이딕스 장치는 시료 전처리와 증폭을 칩에 통합하고 기술자의 기술을 최소화하는 휴대용 대체 장치에 대한 벤처 자금을 유치하고 있습니다. 비용 곡선은 하향 추세를 유지하고 있으며, 중규모 검사기관에도 차세대 시퀀싱 도입 기회가 확대되어 성병(STD) 진단 시장 경쟁 구도를 재정의하고 있습니다.

북미는 2025년 전 세계 매출의 41.62%를 차지했습니다. 예방적 성병 서비스가 보험 의무화에 따라 무상으로 제공되고, 매독 급증 대책에 대한 연방정부의 강력한 조정이 이를 뒷받침하고 있습니다. 높은 의료비 재량 지출과 신속한 규제 승인으로 이 지역은 혁신의 최첨단을 유지하고 있습니다. 그러나 지역 내 격차는 여전히 존재합니다. 남부 지역에서는 평균보다 높은 감염률이 보고되고 있으며, 이는 성숙한 시장 내에서도 의료서비스가 부족한 지역이 존재한다는 것을 시사합니다.

유럽은 보편적 의료보험제도와 지역 간 규제 조정을 기반으로 안정적인 기반을 가지고 있지만, 예산 압박으로 인해 비용 효율성이 높은 포인트 오브 케어(Point of Care) 모델이 강조되고 있는 상황입니다. 아시아태평양은 연평균 10.76%의 예상 CAGR로 가장 빠르게 성장하는 지역으로, 도시화, 공중보건 투자, 동남아시아 가임기 여성의 성병 유병률 11.6%가 성장을 주도하고 있습니다. 중국의 의료 분야 반부패 조치로 인해 2024년 외국산 진단기기 수입이 일시적으로 둔화되었지만, 아세안 국가와 인도의 인프라 투자로 검사 접근성 확대가 촉진되고 있습니다. 라틴아메리카와 중동 및 아프리카은 인식 증가와 모바일 헬스 보급이 인프라 부족을 보완하는 신흥 시장을 형성하고 있습니다. WHO가 지원하는 통합 진단 기술 및 저비용 다중 검사 패널에 대한 자금 지원은 이들 지역에 기부자 자본을 유도하고 있습니다. 남아공은 세계 최고 수준의 연령 조정 성병 발병률을 기록하고 있으며, 향후 확장 모델을 형성할 수 있는 기증자 지원 시범 프로젝트의 초점이 되고 있습니다. 전반적으로 지리적 다각화 전략이 세계 성병(STD) 진단 시장에서 경쟁하는 업체들의 수익 회복력을 결정지을 것입니다.

The STD diagnostics market was valued at USD 18.18 billion in 2025 and estimated to grow from USD 19.42 billion in 2026 to reach USD 27.04 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031).

Growth is propelled by an 80% surge in U.S. syphilis cases-exceeding 207,000 confirmed infections in 2022-and the creation of a federal task force to curb the trend. The World Health Organization now tracks 8 million global syphilis cases for 2022, underscoring the gap to its 2030 goal of a 90% reduction in adult infections. Overall STI incidence has climbed 58.38% since 1990, with the sharpest burdens in low socio-demographic regions. Regulatory momentum continues as the FDA reclassified nucleic-acid STI assays to Class II in May 2025, shortening approval cycles for innovative platforms. Insurers updated preventive-service tables in May 2024 to guarantee zero-cost STD screening, expanding routine testing volumes. Yet 68% of individuals still cite shame and 85% fear provider judgment, fueling demand for home-based and digitally connected diagnostics.

The World Health Organization recorded more than 1 million new sexually transmitted infection cases every day during 2024. Asymptomatic presentations account for roughly 70% of chlamydia and gonorrhea infections, so routine testing is vital to interrupt transmission. Gen Z and young millennials aged 15-24 represent nearly half of new cases, prompting health systems to integrate rapid PoC assays that deliver timely results and curb reinfection chains. The discovery of mpox as a sexually transmitted pathogen in 2024 created further diagnostic demand because clinicians need multiplex panels able to distinguish legacy STIs from emerging threats. Simultaneous detection of pathogens and resistance profiles places nucleic-acid platforms at the center of the expanding STD diagnostics market.

The U.S. Preventive Services Task Force broadened its screening guidance in 2024 to recommend annual chlamydia and gonorrhea tests for all sexually active individuals younger than 25. Similar moves in Canada earmarked CAD 74 million (USD 54.8 million) to extend testing in Indigenous and remote communities. European Union member states synchronized guidelines that favor FDA-cleared or CE-marked molecular assays. These programs provide predictable procurement streams, reinforce quality benchmarks, and enlarge the STD diagnostics market size across primary care, public health, and community settings.

Survey data show 43% of adults delay or reject STI screening for fear of judgment or privacy breaches. Cultural taboos in certain regions equate testing with promiscuity, disproportionately limiting women's access to reproductive care. Public-health campaigns launched in 2024 re-frame screening as a routine wellness metric, yet uptake remains uneven. Anonymous home kits and app-scheduled clinic slots alleviate stigma for some users, but legal restrictions on telemedicine in several jurisdictions slow wider adoption. Ongoing school-based sex-education pilots have lifted testing rates by 25% where implemented, suggesting long-run gains once curricula scale nationally.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The HIV segment collected 28.45% of 2025 revenue, underscoring entrenched policies that require routine screening in blood services, prenatal care, and high-risk populations. Syphilis anchors the number-two position thanks to prenatal mandates that aim to curb congenital infections. Chlamydia and gonorrhea testing together generated roughly one-third of total revenue, supported by annual testing advice for sexually active youth.

Mycoplasma genitalium reported the quickest 7.77% CAGR outlook through 2031, propelled by growing recognition of its role in persistent urethritis. HPV and HSV segments post steady gains as multiplex NAAT assays streamline differential diagnosis. Trichomonas benefits from same-visit PoC platforms that catch treatable infections before patients leave the clinic. Chancroid remains niche but experiences improved molecular detection accuracy, reducing historical under-diagnosis.

Molecular platforms retained 50.78% share in 2025, delivering rapid, highly sensitive results that support guideline-driven care. Immunoassays remain vital in lower-resource settings, yet accuracy gaps limit additional share gains.

Next-generation sequencing is set for a 9.13% CAGR thanks to simultaneous pathogen and resistance profiling, capabilities prized by surveillance bodies such as the CDC, which purchased fleet NGS systems for USD 45 million in 2024. Biosensor and microfluidic devices integrate sample prep and amplification on a chip, drawing venture funding into portable alternatives that require minimal technician skill. Cost curves remain on a downward slope, opening mid-tier labs to NGS adoption and redefining the competitive stakes within the STD diagnostics market.

The STD DisgnosticsMarket Report is Segmented by Test Type (Chlamydia, Gonorrhea, Syphilis, and More), Technology (Immunoassay-Based Methods, Molecular Diagnostics, Next-Generation Sequencing, and More), Location of Testing (Central & Hospital Laboratories, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 41.62% of global revenue in 2025, sustained by insurance mandates that make preventive STD services cost-free and by robust federal coordination to counter the syphilis surge. High discretionary healthcare spending and rapid regulatory approvals keep the region at the innovation vanguard. Nevertheless, intra-regional gaps prevail; Southern states report above-average infection rates, signaling under-served pockets even within a mature market.

Europe follows with a stable base built on universal health coverage and pan-regional regulatory harmonization, yet faces budgetary pressure that favors cost-effective point-of-care models. Asia-Pacific is the fastest-growing territory at a forecast 10.76% CAGR, driven by urbanization, public-health investments, and an 11.6% STI prevalence among reproductive-age women in Southeast Asia. China's anti-corruption clampdown in healthcare briefly slowed foreign diagnostic imports in 2024, but infrastructure spending across ASEAN and India is widening test access. Latin America and the Middle East & Africa together form an emerging corridor where rising awareness and mobile-health penetration offset infrastructure deficits. WHO-backed funding for integrated diagnostics and low-cost multiplex panels is steering donor capital into these regions. South Africa records the world's highest age-standardized STI rates, making it a focal point for donor-supported pilot projects that could shape future expansion models. Overall, geographic diversification strategies will define revenue resilience for vendors competing in the global STD Diagnostics market.