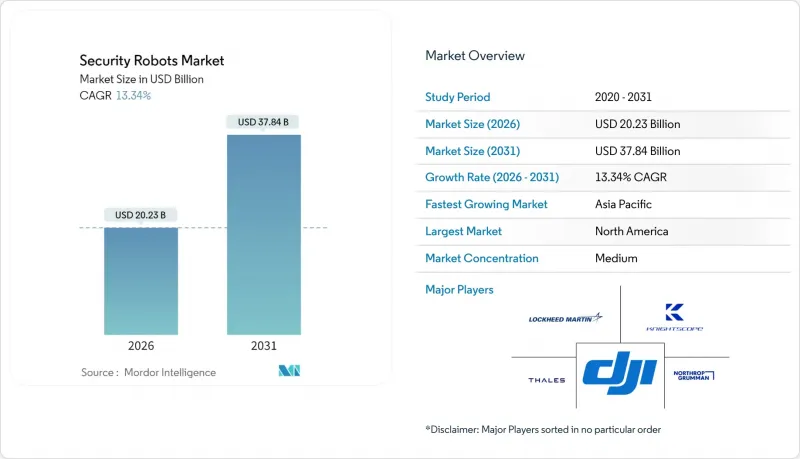

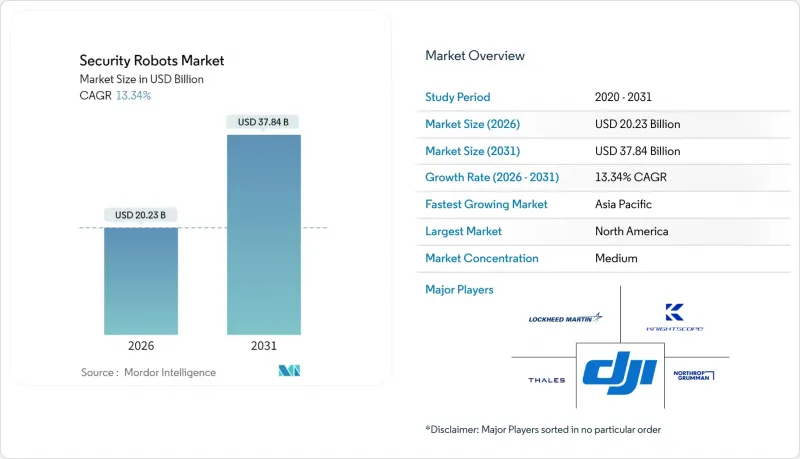

보안 로봇 시장은 2025년에 178억 5,000만 달러로 평가되었고, 2026년 202억 3,000만 달러에서 2031년까지 378억 4,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 13.34%로 예상됩니다.

자율 플랫폼이 AI 인식, 첨단 센서, 전 영역 탐색을 통합하여 위협이 나타나기 전에 예측하고 지속적으로 작동하는 시스템을 구현하면서 수요가 증가하고 있습니다. 국방시설, 공항, 발전소, 상업시설에서는 고정 카메라나 순찰 경비원을 대신해 24시간 감시, 오경보율 감소, 인건비 절감을 실현하는 로봇의 도입이 증가하고 있습니다. 초기 설비투자가 필요 없는 구독형 가격 책정, 중요 인프라의 경계침입 감지 국가 지침, 드론의 가시권 밖 비행(BVLOS) 경로를 개방하는 규제 발전으로 인해 성장이 더욱 가속화되고 있습니다. 한편, 사이버 방어의 취약성, 분절된 스펙트럼 정책, 얼굴인식 기술에 대한 대중의 불안감 등의 역풍도 존재하며, 벤더는 기술 설계와 투명한 거버넌스를 통해 이를 해결해야 합니다.

다중 스펙트럼 카메라와 컴퓨터 비전 모델을 융합한 열화상 기술은 오경보를 40% 감소시켜 공항과 원자력 발전소 운영자의 업무 부담을 줄였습니다. 엔비디아의 코스모스 플랫폼은 문맥을 해석하는 비전, 언어, 행동 모델에 정보를 제공하여 로봇이 정상적인 활동과 진정한 위협을 구분할 수 있도록 합니다. 이러한 스택을 통합한 에너지 기업은 운영자가 정확한 좌표와 위협 분류를 제공받음으로써 사고 대응 시간을 50% 단축할 수 있었습니다. 뛰어난 감지 정확도로 인해 로봇은 실험 단계에서 미션 크리티컬한 역할로 전환하고 있습니다.

호주와 일본은 현재 조종사의 시야 밖 비행을 허용하는 위험 기반 규제 프레임워크를 도입하고 있습니다. 감지 및 회피 시스템을 통한 안전성을 확보하면서 기존에는 수십 명의 경비원이 필요했던 수 킬로미터의 경계선을 단일 기기로 경비할 수 있어 커버리지 확대와 헥타르당 비용 절감을 실현하고 있습니다. 인도 태평양 지역의 각국 정부는 광활한 해안선과 외딴 지역의 시설에서 자율 순찰이 필수적이라는 것을 인식하고 지역적 수요를 촉진하고 있습니다.

EU 회원국마다 주파수 대역의 할당량이 다르기 때문에 업체들은 각 국가별로 무전기를 커스터마이징할 수 밖에 없어 규모의 경제가 훼손되고 있습니다. 2024년 시행 예정인 EU AI법에서는 보안 로봇도 고위험 시스템으로 분류되어 컴플라이언스 관련 서류가 증가하고 비용이 증가하게 됩니다. 이러한 장벽은 소규모 사업자의 진입을 가로막고, 특히 국경을 넘나드는 시설의 다국적 진출을 지연시키고 있습니다.

UAV(무인항공기)는 신속한 전개와 광범위한 커버리지로 경계침투 시 대응시간을 크게 단축할 수 있어 2025년 기준 보안로봇 시장의 53.40%를 차지하였습니다. 이 플랫폼은 전기 광학, 적외선, 음향 센서를 통합하여 밤낮으로 침입자를 추적할 수 있습니다. BVLOS 규제가 성숙함에 따라 UAV 순찰에 따른 보안 로봇 시장 규모는 2031년까지 꾸준히 확대될 것으로 예측됩니다. 인도 해군과 호주 해군도 분쟁 해역에 대한 감시 범위를 확대하는 초대형 자율 수중 차량(XLUUV) 수요를 주도하고 있습니다.

UGV(지상무인차량)는 14.85%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 부문입니다. 실내 쇼핑몰, 창고, 데이터센터 등에서는 항공기에 의한 감시가 어렵기 때문에 지속적인 지상 감시가 필요하기 때문입니다. 도난 방지에 어려움을 겪고 있는 소매업체는 실시간 영상을 관제실에 전달하고 음성으로 도난 방지 안내 방송을 송출하는 소형 UGV를 채택하고 있습니다. 5G를 통해 연결된 여러 대의 로봇이 순찰을 연계하여 사각지대를 줄이는 메시 네트워크를 형성합니다. 각 업체들은 LiDAR 기반 SLAM(자율 이동 매핑)과 클라우드 호스트형 AI를 통해 자율성을 강화하고, 감지, 분류, 대응 행동의 연계를 긴밀하게 하고 있습니다. 하이브리드 수륙양용 로봇과 AUV(Autonomous Underwater Vehicle)는 항만과 해양 플랫폼 주변이라는 특수한 틈새 시장을 개척하여 육해 경계를 넘나드는 위협에 대응하고 있습니다.

하드웨어는 2025년 매출의 67.10%를 차지했습니다. 이는 인식 센서, 연산 모듈, 견고한 섀시의 제조 비용이 여전히 높기 때문입니다. 부품 원가의 대부분은 LiDAR 유닛, 열화상 카메라, 엣지 GPU가 차지하며 단기 매출을 견인하고 있습니다. 그러나 최종 사용자가 운영 지출 모델로 전환함에 따라 서비스 분야는 18.15%의 연평균 복합 성장률(CAGR)로 급성장하고 있습니다. RaaS(Robot-as-a-Service) 번들은 다년 계약으로 로봇 본체, 소프트웨어, 현지 지원을 제공하여 고객의 감가상각 부담을 줄여줍니다. 2024년 나이트스코프는 K5 전 차량에 대해 추가 비용 없이 v5 구성으로 업그레이드할 수 있도록 함으로써 구독 서비스의 가치 제안을 입증했습니다.

소프트웨어 및 AI 스택은 고급 분석 기능, 자연어 인터페이스, 통합 API를 가능하게 하는 연간 라이선스를 통해 지속적인 수익을 창출합니다. 이러한 디지털 레이어는 시간이 지남에 따라 하드웨어보다 더 높은 수익률을 달성할 수 있습니다. 클라우드 대시보드를 통해 보안 책임자는 분산된 로봇군을 모니터링하고, 사고 영상에 대한 포렌식 분석, 무선으로 알고리즘 업데이트를 실시할 수 있으며, 사용자를 벤더의 생태계에 연결하여 보안 로봇의 총 잠재 시장을 확대하는 선순환이 이루어질 수 있습니다.

보안 로봇 시장 보고서는 로봇 유형(무인 항공기, 무인 지상 차량, 자율형 등), 구성 요소(소프트웨어, 서비스), 최종 사용자(국방/군사, 주거 등), 용도(정찰, 폭발물 감지, 순찰 등), 지역(북미, 유럽 등)으로 분류하여 분석합니다. 유럽 등). 시장 규모 및 예측은 금액(USD)으로 제공됩니다.

북미는 2025년 매출의 39.40%를 차지하며, 독보적인 국방 예산, 초기 BVLOS(가시권 밖 비행) 규제, 로봇 스타트업에 대한 벤처 자금이 이를 뒷받침하고 있습니다. 미국에서만도 쇼핑몰, 기업 캠퍼스, 시립 주차장 시설에 1,200대 이상의 자율 순찰 유닛이 배치되어 있습니다. 나이트스코프 도입으로 몇 달 만에 사건 발생률이 최대 50%까지 감소하여 중소도시가 전력 강화 방안으로 함대 시범 운영을 결정한 요인이 되었습니다. 캐나다와 멕시코도 국경 검문소 및 에너지 회랑을 위해 유사한 솔루션을 채택하여 지역 규모의 우위를 강화하고 있습니다.

아시아태평양은 장거리 드론 순찰을 허용하는 규제 완화와 급증하는 해군 예산으로 인해 15.05%의 가장 높은 CAGR을 기록했습니다. 호주의 1억 4,000만 달러 규모의 '고스트샤크 XLUUV' 계획은 수중 로봇 투자의 좋은 예이며, 중국은 심천 도심에서 시민과 대화하는 인간형 경찰 로봇을 전시하고 있습니다. 인도 해군은 대잠수함전용으로 12대의 국산 XLUUV를 계획하고 있으며, 이는 분쟁 해역에서의 해양 영역 인식에 대한 잠재적 수요를 뒷받침하고 있습니다.

유럽에서는 꾸준한 진전을 보이고 있지만, 복잡한 AI 규제와 전파 규제가 프로젝트 일정을 압박하고 있습니다. 탈레스(Tales)의 18억 파운드 규모의 해양 센서 계약과 키네틱(Kinetic)의 1억 6천만 파운드 규모의 지향성 에너지 프로그램 등 주목받는 방산 이니셔티브가 추진력을 유지하고 있습니다. 그러나 전파의 파편화로 인해 국경을 넘나드는 멀티 로봇의 원활한 연계를 방해하고 있으며, 통합 사업자는 국가별로 통신 시스템을 커스터마이징할 수밖에 없는 상황입니다.

The security robots market was valued at USD 17.85 billion in 2025 and estimated to grow from USD 20.23 billion in 2026 to reach USD 37.84 billion by 2031, at a CAGR of 13.34% during the forecast period (2026-2031).

Demand is rising because autonomous platforms now blend AI perception, advanced sensors, and all-domain navigation into systems that operate continuously and predict threats before they materialize. Defense installations, airports, power plants, and commercial campuses increasingly replace fixed cameras and roving guards with robots that deliver round-the-clock coverage, lower false-alarm rates, and cut personnel expenses. Growth is further reinforced by subscription pricing that removes upfront capex, by national mandates for perimeter intrusion detection at critical infrastructure, and by regulatory progress that opens Beyond Visual Line of Sight (BVLOS) air corridors for drones. Meanwhile, cyber-hardening gaps, fragmented spectrum policy, and public unease over facial recognition create headwinds that vendors must manage through technology design and transparent governance.

Thermal imaging fused with multi-spectral cameras and computer-vision models has cut nuisance alarms by 40%, easing operator workload at airports and nuclear plants. NVIDIA's Cosmos platform feeds Vision-Language-Action models that interpret context, letting robots distinguish normal activity from genuine threats. Energy companies that integrated these stacks trimmed incident response times by 50% because operators receive precise coordinates and threat classifications. Superior detection accuracy shifts robots from experimental trials to mission-critical roles.

Australia and Japan now permit BVLOS patrols through risk-based regulatory frameworks that keep drones beyond pilot sight while maintaining safety via detect-and-avoid systems. Single aircraft can secure multi-kilometer perimeters that previously demanded dozens of guards, amplifying coverage and lowering cost per hectare. Governments across the Indo-Pacific see autonomous patrols as essential for vast coastlines and remote installations, spurring regional demand.

EU member states allocate spectrum differently, forcing vendors to customize radios for each country and undermining economies of scale. The 2024 EU AI Act also classifies security robots as high-risk systems, piling on compliance paperwork that inflates costs. These hurdles discourage small providers and delay multi-nation deployments, especially at cross-border facilities.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

UAVs retained 53.40% of the security robots market in 2025 thanks to rapid deployment and wide-area coverage that slash response times during perimeter breaches. Platforms integrate electro-optical, infrared, and acoustic sensors to track intruders day and night. The security robotsmarket size attributed to UAV patrols is projected to expand steadily through 2031 as BVLOS rules mature. Indian and Australian navies also push demand for extra-large autonomous underwater vehicles (XLUUVs) that extend surveillance into contested littorals.

UGVs represent the fastest-growing segment with a 14.85% CAGR because indoor malls, warehouses, and data centers need persistent ground-level monitoring where aerial flight is impractical. Retailers grappling with theft adopt compact UGVs that stream real-time video to control rooms and issue audible deterrence announcements. When linked via 5G, multiple robots coordinate patrols, creating a mesh that reduces blind spots. Vendors enhance autonomy with lidar-based SLAM and cloud-hosted AI, tightening loops between detection, classification, and response actions. Hybrid amphibious robots and AUVs carve a specialized niche around ports and offshore platforms, addressing threats that cross land-sea boundaries.

Hardware captured 67.10% of 2025 revenue because perception sensors, compute modules, and rugged chassis still carry high production costs. Lidar units, thermal cameras, and edge GPUs account for most of the bill of materials, anchoring near-term sales. Yet services are racing ahead at 18.15% CAGR as end users pivot to operating-expenditure models. RaaS bundles deliver robots, software, and field support under multi-year contracts, freeing customers from depreciation concerns. In 2024 Knightscope demonstrated that upgrading its entire K5 fleet to the v5 configuration incurred zero incremental cost to clients, underscoring the value proposition of subscription offerings.

Software and AI stacks generate sticky revenue through annual licenses that unlock advanced analytics, natural-language interfaces, and integration APIs. Over time, these digital layers command higher margins than hardware. Cloud dashboards let security directors monitor dispersed robot fleets, run forensics on incident video, and push over-the-air algorithm updates, creating a virtuous circle that ties users to a vendor's ecosystem and expands the total addressable security robots market.

Security Robots Market Report Segments the Industry Into Type of Robot (Unmanned Aerial Vehicles, Unmanned Ground Vehicles, Autonomous, and More), Component (Software, Service), End User (Defense and Military, Residential, and More), by Application (Spying, Explosive Detection, Patrolling, and More), and by Geography (North America, Europe, and More ). The Market Sizes and Forecasts are Provided in Terms of Value in (USD)

North America generated 39.40% of 2025 revenue, supported by unrivaled defense budgets, early BVLOS legislation, and venture funding for robotics start-ups. The United States alone fields 1,200-plus autonomous patrol units across malls, corporate campuses, and municipal parking structures. Knightscope deployments cut incidents by up to 50% within months, convincing mid-tier cities to pilot fleets as a force multiplier. Canada and Mexico adopt similar solutions for border crossings and energy corridors, reinforcing regional scale advantages.

Asia-Pacific posts the highest 15.05% CAGR thanks to regulatory overtures that permit long-range drone patrols and surging naval budgets. Australia's USD 140 million Ghost Shark XLUUV program exemplifies undersea robotics investment, while China showcases humanoid police robots that interact with citizens on the streets of Shenzhen. India's navy plans 12 indigenous XLUUVs for anti-submarine warfare, confirming pent-up demand for maritime domain awareness in contested waters.

Europe advances steadily but contends with complex AI and spectrum regulations that stretch project timelines. High-profile defense initiatives such as Thales's £1.8 billion maritime sensor contract and QinetiQ's £160 million directed-energy program sustain momentum. Still, spectrum fragmentation hampers seamless multi-robot coordination across borders, compelling integrators to tailor communications systems country by country.