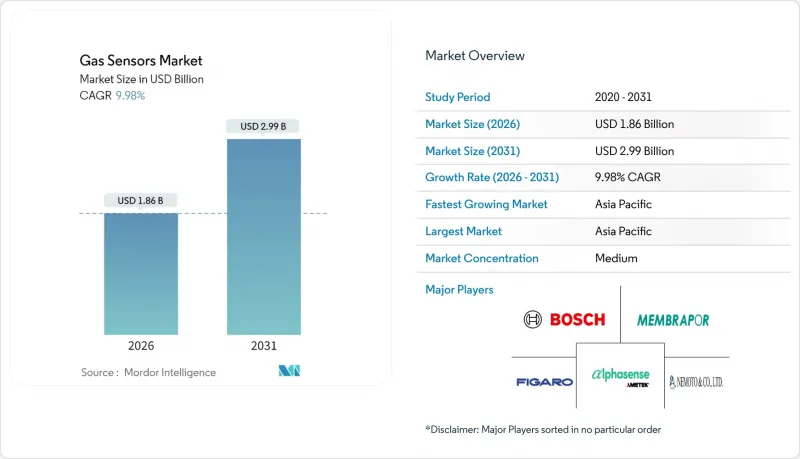

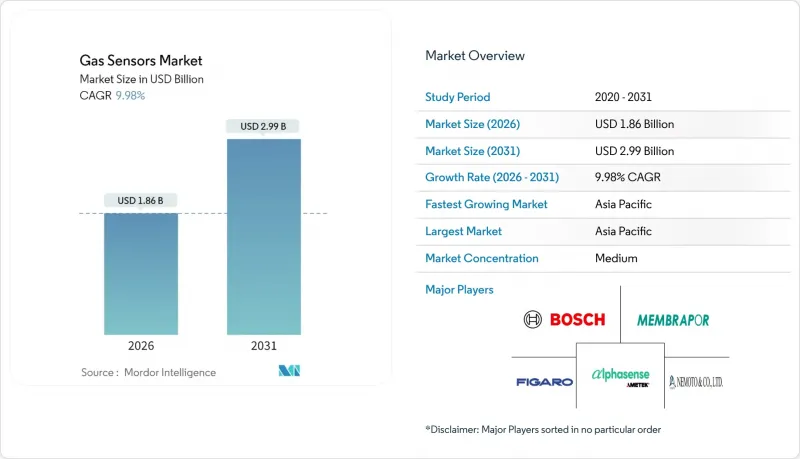

가스 센서 시장은 2025년에 16억 9,000만 달러로 평가되었고, 2026년 18억 6,000만 달러에서 2031년까지 29억 9,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 9.98%로 예상됩니다.

유로 7 차량 진단 시스템의 빠른 도입, 작업장 안전 규제 강화, 스마트시티 대기질 개선 정책으로 인해 센서 출하가 가속화되고 있습니다. 전기화학식에서 소형화 MEMS 반도체 광학 플랫폼으로의 전환은 평균 판매 가격의 향상과 인공지능 기반의 선택성을 실현할 수 있는 모멘텀을 제공합니다. 아시아태평양은 자동차 및 전자기기 제조 거점으로서 가장 규모가 큰 지역 점유율을 차지하고 있습니다. 한편, 메탄 누출 규제를 배경으로 탄화수소 및 휘발성유기화합물(VOC) 감지 장치가 가장 빠르게 성장하는 가스 감지 유형이 되고 있습니다. 기존 업체 간 통합으로 경쟁 구도가 재편되는 한편, 10ppm 미만의 교차 민감도 및 웨이퍼 가격 변동성과 같은 기술적 과제는 비용 중심의 틈새 시장에서의 보급을 억제할 수 있습니다.

유로 7 및 EPA Tier 3 규제에 따라 자동차 제조업체는 차량의 전체 수명주기 동안 질소산화물, 미립자 물질 및 탄화수소를 지속적으로 추적해야 하며, -40°C-70°C에서 작동하는 견고한 멀티 가스 어레이에 대한 수요가 증가하고 있습니다. 보쉬의 레이더 지원 감지 모듈과 하니웰의 배터리 안전 전해질 감지기는 규제 요건이 내연기관과 전기 플랫폼 모두를 포괄하게 되었음을 보여줍니다. 15 년의 장기 내구성 요구 사항으로 인해 고체 상태 및 NDIR 솔루션이 추진되고 있으며, 수명이 짧은 전기 화학 전지는 제쳐두고 있습니다.

ISO 45001의 세계 채택, OSHA의 밀폐 작업 기준, REACH 물질 규정의 상한선으로 인해 공장에서는 연속 고정식 감지기, 개인용 배지, 휴대용 스니퍼의 도입이 요구되고 있습니다. 화학 처리 시설, 배터리 제조 라인, 반도체 클린룸에서는 자가 교정 기능과 클라우드 대시보드에 데이터 기록 기능을 갖춘 MEMS 어레이로 업데이트가 진행되고 있습니다. 플랜트 전체 디지털 트윈 플랫폼과의 통합을 통해 예지보전을 실현하여 다운타임과 보험료를 절감하고 있습니다.

실험실 테스트에서 저가의 포름알데히드 감지 셀이 오존과 이산화질소에 의한 오감지를 보여 야외 스테이션에서 사용하기에 부적합한 것으로 나타났습니다. 농업용 암모니아 모니터도 비슷한 간섭에 직면하고 있으며, 선택적 주석 첨가 인듐 산화물 막은 좁은 분석 대상 범위 내에서만 작동합니다. 금속유기구조(MOF) 필터와 머신러닝 분류기는 식별 정확도를 향상시키지만, 부품 비용이 증가하여 대중용 웨어러블 기기로의 보급을 가로막고 있습니다.

2025년 가스 센서 시장에서는 일산화탄소 감지기가 가정용 경보, 보일러 모니터링, 차량 내 안전 용도로 26.05%의 점유율을 차지하며 수량 기준으로 선두를 유지했습니다. 그러나 OGMP 2.0 메탄 규제에 따라 에너지 기업이 누출 배출량 추적이 의무화됨에 따라 탄화수소 및 VOC 감지기는 11.95%의 연평균 복합 성장률(CAGR)로 모든 부문을 능가하는 성장세를 보일 것으로 예측됩니다. 이러한 변화는 가스 센서 시장을 메탄, 에탄, 벤젠을 동시에 측정하는 다성분 센서 어레이로 재조정하여 석유 및 가스 사업자의 총소유비용을 절감할 수 있습니다. 300나노와트 소비전력으로 1-1,000ppm의 수소를 측정하는 새로운 나노 트랜지스터식 검출기는 배터리 모듈, 드론, 주거용 연료전지 시스템까지 모니터링 범위를 확대할 수 있습니다.

탄화수소 붐으로 인해 도시 전체 누출 매핑 프로그램을 구축하는 환경 모니터링 계약업체를 위한 가스 센서 시장 규모가 확대되고 있습니다. 메탄 전용 칩에 대한 OEM 수요도 평균 단가를 끌어올려 성숙한 일산화탄소 및 산소 카테고리의 가격 하락을 일부 상쇄하고 있습니다. 한편, 산소결핍 감지 제품은 야금업과 펄프공장에서 안정적인 수요를 유지하고 있으며, 이산화탄소용 비분산형 적외선(NDIR) 셀은 실내 공기질 규제에 따라 성장세를 보이고 있습니다. 특수 이산화황 및 황화수소 감지기는 정유소 굴뚝이나 광산 갱도에 한정되어 있지만, 고사양 공급업체에게는 틈새 수익원이 되고 있습니다.

전기화학식 감지 소자는 검증된 현장 신뢰성과 낮은 초기 비용으로 2025년 기준 31.65%의 점유율을 유지하며 산업 안전 계측 시스템 생태계의 핵심을 담당하고 있습니다. MEMS 반도체 광학 스택은 고유한 선택성, 드리프트 저항, 머신러닝 기반 패턴 라이브러리와의 호환성을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 15.60%로 확대될 것으로 예상되며, 시장 상황은 빠르게 변화하고 있습니다. 이러한 급격한 성장은 캘리브레이션이 필요 없는 라이프사이클을 요구하는 자동차, HVAC, 민수용 IoT 단말 관련 가스 센서 시장 규모를 확대할 것입니다.

하이브리드 디바이스는 광학식, 전기화학식, 금속산화막식을 단일 패키지에 통합하여 여러 개의 개별 기판을 대체하고 조달을 효율화합니다. 보쉬 센서텍의 BME688 '전자코'는 AI 기반 시그니처를 통해 식품 부패 및 산불의 전조를 감지하는 것이 특징입니다. 펄스 구동 MEMS 히터와 심층 신경망의 조합으로 수소, 일산화탄소, 암모니아의 식별 정확도가 100%에 도달했습니다. 소프트웨어의 중요성이 커지는 가운데, 무선으로 펌웨어 업데이트가 결정적인 차별화 요소로 떠오르면서 하드웨어 중심의 경쟁사들은 분석 벤더와의 제휴를 모색하고 있습니다.

가스 센서 시장 세분화는 가스 유형(산소, 일산화탄소 등), 기술(전기화학식, 광이온화식 등), 폼팩터(고정형/현장 설치 모듈, 휴대용/휴대용 장치 등), 연결 방식(유선, 무선), 최종 사용자 산업별(산업 안전, 공정, 자동차 파워트레인, HVAC 등), 지역별로 분류됩니다. 자동차 파워트레인, HVAC 등), 지역별로 분류됩니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

아시아태평양은 2025년 42.90%의 매출 점유율을 차지하며 가스 센서 시장을 주도하고 있으며, 2031년까지 연평균 복합 성장률(CAGR) 13.72%를 나타낼 것으로 예측됩니다. 중국의 스마트시티 구상은 블록 단위의 오염 감시망 구축을 의무화하고 있으며, 수만 개의 저비용 노드를 요구하고 있습니다. 한편, 인도에서는 ISO 45001의 준수 추진으로 자동차, 시멘트, 특수화학 분야의 공장 바닥 개보수가 가속화되고 있습니다. 일본의 수소사회 구상은 서브ppm 수준의 안전감시장치 수주를 촉진하고, 한국의 반도체 산업 확대는 국내 MEMS 공급망의 기반을 구축하고 있습니다. 윈센일렉트로닉스와 피가로 엔지니어링과 같은 현지 유력 기업들은 부품 집적화와 노동력 차익거래를 활용하여 수출시장과 내수시장 모두에 서비스를 제공함으로써 가스 센서 시장에서 지속적인 리더십을 유지하고 있습니다.

북미는 성숙하면서도 혁신이 주도하는 시장입니다. EPA Tier 3 배출 규제, 슈퍼 에미터 프로그램, 캐나다의 메탄 75% 감축 목표가 고정밀 누출 감지 네트워크에 대한 수요를 촉진하고 있습니다. 텍사스와 앨버타주의 석유 채굴 사업자는 위성 통신망에 연결된 광학식 메탄 감지 카메라를 도입했습니다. 한편, 미국 중서부 지역의 배터리 기가팩토리 확장에서는 작업자 보호를 위해 다가스 대응 전기화학식 감지 랙을 채택하고 있습니다. 센서 OEM과 소프트웨어 기업의 합작 투자로 데이터량을 압축하고 지적 재산을 보호하는 엣지 분석 모듈이 개발되어 서비스 분야로의 가치 전환이 가속화되고 있습니다.

유럽은 규제 중심의 자세를 유지하고 있습니다. 유로 7 규제로 인해 경/중형 차량용 NOx 후처리 프로브가 추진되고, 2024년 채택된 EU 전역의 메탄 규제에 따라 업스트림 에너지 기업들은 플레어와 컴프레서를 지속적으로 모니터링해야 합니다. 독일 그린 스틸 파일럿 라인에서는 산소 및 수소 감지기를 폐쇄 루프 버너에 통합했습니다. 한편, 스칸디나비아 도시에서는 5G로 연결된 자전거 도로 대기질 표시판에 이산화질소(NO2) 및 오존(O3) 센서를 추가하고 있습니다. 데이터 주권법은 On-Premise 서버와 암호화 무선 프로토콜을 촉진하고, 다국적 센서 군의 조달 사양을 형성하고 있습니다.

The gas sensors market was valued at USD 1.69 billion in 2025 and estimated to grow from USD 1.86 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 9.98% during the forecast period (2026-2031).

Rapid adoption of Euro 7 on-board diagnostics, stricter workplace safety rules, and smart-city air-quality initiatives are accelerating sensor shipments. Momentum is reinforced by the transition from electrochemical to miniaturized MEMS-semiconductor optical platforms, which boost average selling prices and enable artificial-intelligence-based selectivity. Asia-Pacific commands the largest regional position thanks to its automotive and electronics manufacturing base, while hydrocarbon and volatile-organic-compound devices are the fastest expanding gas type on the back of methane leak regulations. Consolidation among incumbents is reshaping competitive dynamics, yet technical hurdles such as sub-10 ppm cross-sensitivity and wafer-price volatility may curb adoption in cost-sensitive niches.

Euro 7 and EPA Tier 3 rules oblige automakers to continuously track nitrogen oxides, particulate matter, and hydrocarbons across the full vehicle life cycle, raising demand for robust, multi-gas arrays rated for -40 °C to 70 °C operation. Bosch's radar-enabled sensing modules and Honeywell's battery-safety electrolyte detectors illustrate how compliance requirements now encompass internal combustion and electric platforms alike. Long-term durability mandates of 15 years are pushing solid-state and NDIR solutions, sidelining short-lived electrochemical cells.

Global adoption of ISO 45001, OSHA's confined-space norms, and REACH substance caps compels factories to deploy continuous fixed detectors, personal badges, and portable sniffers. Chemical processors, battery-manufacturing lines, and semiconductor cleanrooms are upgrading to MEMS arrays that self-calibrate and log data to cloud dashboards. Integration with plant-wide digital-twin platforms supports predictive interventions that cut downtime and insurance premiums.

Laboratory tests show low-cost formaldehyde cells registering false positives from ozone and nitrogen dioxide, disqualifying them for outdoor stations. Agricultural ammonia monitors face similar interference, while selective tin-doped indium oxide films work only within narrow analyte windows. Metal-organic-framework filters and machine-learning classifiers improve discrimination yet add bill-of-materials cost, restraining uptake in mass-market wearables.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Carbon monoxide devices dominated 2025 volume thanks to household alarms, furnace monitoring, and vehicle cabin safety, securing 26.05% of the gas sensors market share. Hydrocarbon and VOC detectors, however, are projected to outpace all peers with a 11.95% CAGR as OGMP 2.0 methane rules force energy firms to track fugitive emissions. This shift rebalances the gas sensors market toward multi-species arrays that quantify methane, ethane, and benzene simultaneously, decreasing total cost of ownership for oil and gas operators. Emerging nano transistor-based detectors measuring 1-1,000 ppm hydrogen at 300 nW consumption extend monitoring into battery modules, drones, and residential fuel-cell systems.

The hydrocarbon boom widens the addressable gas sensors market size for environmental-monitoring contractors building citywide leak-mapping programs. OEM demand for methane-specific chips also boosts average revenue per unit, partially offsetting price erosion in mature carbon monoxide and oxygen categories. Meanwhile, steady oxygen-deficiency products retain relevance in metallurgy and pulp mills, and carbon-dioxide NDIR cells ride the wave of indoor-air-quality legislation. Specialty sulphur-dioxide and hydrogen-sulphide instruments stay confined to refinery stacks and mining tunnels, yet they anchor niche profitability for high-spec suppliers.

Electrochemical elements retained 31.65% share in 2025 due to proven field reliability and low initial cost, keeping them central to the industrial safety-instrument-system ecosystem. The landscape is changing quickly as MEMS-semiconductor optical stacks are forecast to clock a 15.60% CAGR to 2031, driven by their inherent selectivity, drift immunity, and compatibility with machine-learning-based pattern libraries. This surge will lift the gas sensors market size linked to automotive, HVAC, and consumer IoT endpoints that demand calibration-free life cycles.

Hybrid devices blend optical, electrochemical, and metal-oxide principles inside one package, replacing multiple discrete boards and streamlining procurement. Bosch Sensortec's BME688 "electronic nose" showcases AI-enabled signatures that flag food spoilage and forest-fire precursors. Pulse-driven MEMS heaters coupled with deep neural networks now reach 100% identification accuracy across hydrogen, carbon monoxide, and ammonia. As software weight rises, firmware over-the-air updates become a decisive differentiator, nudging hardware-centric rivals to form alliances with analytics vendors.

Gas Sensors Market Segmented by Gas Type (Oxygen, Carbon Monoxide and More), Technology (Electro-Chemical, Photo-Ionization, and More), Form Factor (Fixed/In-situ Modules, Portable/Hand-held Devices and More), Connectivity (Wired, Wireless), End-Use Industry (Industrial Safety & Process, Automotive Powertrain & HVAC and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific anchors the gas sensors market with a 42.90% revenue share in 2025 and is poised for a 13.72% CAGR through 2031. China's smart-city blueprints mandate block-level pollution grids that demand tens of thousands of low-cost nodes, while India's drive to align with ISO 45001 fuels plant-floor retrofits across automotive, cement, and specialty-chemicals sectors. Japan's hydrogen-society ambitions accelerate orders for sub-ppm safety monitors, and South Korea's semiconductor expansions seed a domestic MEMS supply chain. Local champions such as Winsen Electronics and Figaro Engineering leverage component clustering and labour arbitrage to serve both export and internal markets, underpinning sustained leadership in the gas sensors market.

North America represents a mature yet innovation-led arena. EPA Tier 3 exhaust limits, the Super Emitter Program, and Canada's 75% methane-reduction target nurture demand for high-fidelity leak-detection networks. Oil-patch operators in Texas and Alberta deploy optical methane cameras networked to satellite feeds, while battery-gigafactory expansions in the United States Midwest specify multi-gas electro-chemical racks for worker protection. Joint ventures between sensor OEMs and software firms incubate edge-analytics modules that compress data volumes and protect IP, reinforcing value migration toward services.

Europe remains regulation centric. Euro 7 drives NOx after-treatment probes across light and heavy vehicles, and the EU-wide methane regulation adopted in 2024 compels upstream energy players to monitor flares and compressors continually. Germany's green-steel pilot lines integrate oxygen and hydrogen gauges into closed-loop burners, while Scandinavian cities add NO2 and O3 cells to bikeway air-quality signs connected over 5G. Data-sovereignty statutes encourage on-premises servers and encrypted wireless protocols, shaping procurement specifications for transnational sensor fleets.