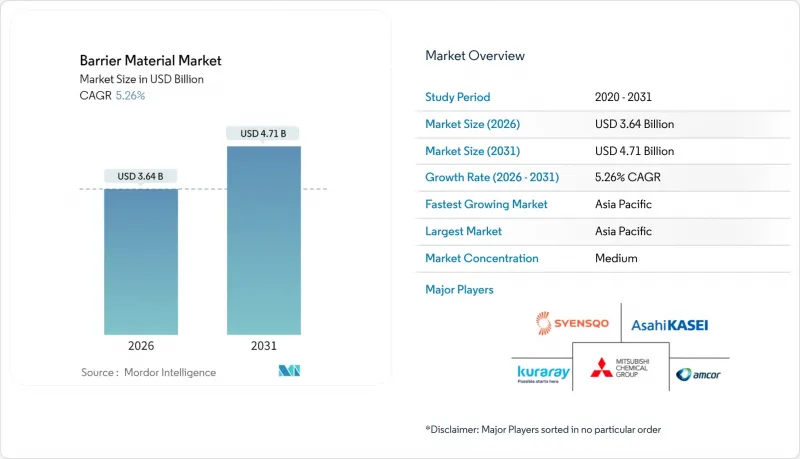

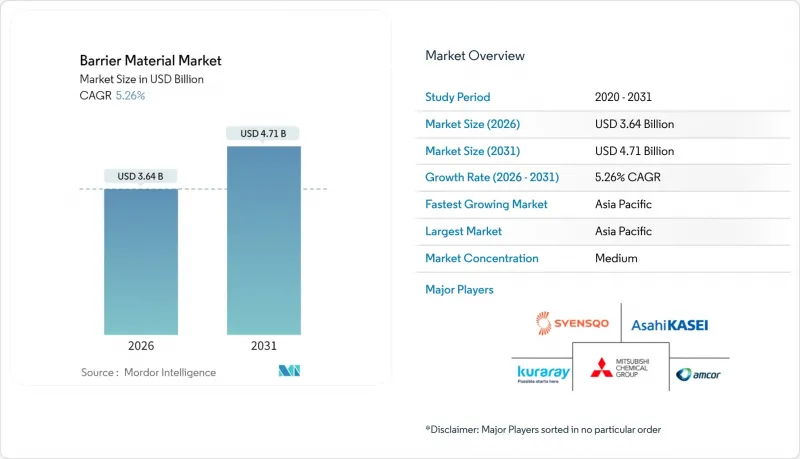

배리어재 시장은 2025년 34억 6,000만 달러에서 2026년에는 36억 4,000만 달러로 성장하고, 2026-2031년 CAGR 5.26%로 성장을 지속하여, 2031년까지 47억 1,000만 달러에 이를 것으로 예측됩니다.

식품의 유통기한을 연장하는 다층 필름에 대한 수요 증가, 아시아태평양의 제약 생산 능력의 급속한 확대, PFAS 화학물질에 대한 규제 전환 가속화 등이 성장을 견인하는 주요 요인으로 꼽힙니다. 브랜드 소유자의 순환 경제 목표에 대한 노력은 재활용 가능한 폴리올레핀 구조에 대한 투자를 촉진하고 있으며, 전자상거래의 급격한 성장으로 인해 컨버터는 더 긴 공급망을 통해 장벽 성능을 유지할 수 있는 더 견고하고 펑크에 강한 포장 형태를 개발하도록 유도하고 있습니다. 동시에 알루미늄, 에틸렌, 프로파일렌의 원료 수급이 타이트해짐에 따라 공급 계약의 비용 전가 조항이 강화되어 주요 수지 업체 간의 수직계열화를 촉진하는 요인으로 작용하고 있습니다. 경쟁적 차별화는 절대적인 장벽 성능에서 낮은 환경 영향과 여러 관할권에서 검증된 컴플라이언스 문서로 동등한 보호 기능을 제공하는 능력으로 옮겨가고 있습니다.

수분 함량이 높은 베이커리 제품, 유제품, 레토르트 식품 카테고리에서는 미생물의 증식과 지질 산화를 늦추도록 설계된 산소 및 수증기 차단 필름이 필수적입니다. 게라니올 등 식물 유래 활성 성분을 배합한 항균 배리어 플레이트는 빵과 페이스트리에서 5-10일의 유통기한 연장을 실현하고, 전 세계 식품 접촉 기준치 이하의 전이 수준을 유지하고 있습니다. 고투명 EVOH를 사용한 조정 분위기 포장 백은 산소 투과율을 0.1cc/m2/일 이하로 낮추어 냉장 육류 제품의 보존료 사용량 절감에 기여하고 있습니다. 국내 연구진이 개발한 식용 키토산-갈산 코팅은 외관의 손상 없이 자외선 차단과 항균 성능을 추가하여 범용 포장재보다 20-30% 높은 가격 책정이 가능한 프리미엄 시장을 개척하고 있습니다. 유통기한 연장은 전 세계 음식물 쓰레기 감축 목표와 직접적으로 일치하며, 장벽재 시장을 유엔 지속가능발전목표(SDGs) 12의 주요 촉진요인으로 자리매김하고 있습니다.

2025년 6월부터 시행되는 일본의 의약품 접촉 재료 포지티브 리스트는 흡습성 원약에 대해 수분 투과율 0.05g/m2/일 미만을 의무화하여 고품질 PVDC 및 EVOH 라미네이트의 채택을 가속화하고 있습니다. 중국의 GB 4806.7-2023 및 GB 43352-2023 표준은 낮은 전이 한계치를 규정하여 확실한 분석 데이터와 검증된 클린룸 필름을 보유한 공급업체에 유리합니다. 인도의 의약품 수출은 매년 15% 이상 증가하고 있으며, 블리스 터 포장 공급업체는 미국 FDA, 유럽의약품청(EMA), 의약품의료기기종합기구(PMDA)의 요구사항에 대한 동시 적합성 인증을 요구받고 있습니다. 이러한 추세에 따라 전 세계 컨버터들은 필름 생산을 아시아태평양으로 현지화하여 지역 공급 안정성을 강화하고 리드 타임을 단축하고 있습니다. 고도의 장벽 구조는 유통 중 단백질 안정성을 유지하기 위해 1ppm 미만의 산소 수준을 필요로 하는 바이오시밀러 제제를 지원하는 데에도 기여하고 있습니다.

EU에서는 폴리머 대체품 대비 높은 탄소강도를 반영하여 알루미늄 포장재에 0.80유로/kg의 포장세 도입을 검토 중입니다. 이 정책으로 인해 스낵 식품용 연포장에 얇은 호일 사용이 억제될 것으로 예측됩니다. 브랜드 소유자의 라이프사이클 평가 모델에 따르면, 알루미늄 층은 기능성 코팅이 적용된 단층 PE 구조와 비교하여 포장의 CO2 배출량을 최대 300% 증가시키기 때문에 기존에 성능 기준을 확립한 금속화 필름도 재설계가 필요합니다. 초고습도 의약품 포장에서는 여전히 호일을 대체할 수 없지만, 저탄소 제련 공정과 래치 원활한 재활용 경로에 대한 탐색이 가속화되고 있습니다. 불활성 양극을 이용한 시험용 전해전지에서 2025년까지 알루미늄 1톤당 7톤의 CO2 환산 절감 효과가 확인되었으나, 실용화까지는 아직 5년의 시간이 필요합니다. 당분간은 PET에 산화알루미늄 또는 실리카 코팅을 증착한 다층 구조가 높은 재료비에도 불구하고 점유율을 확대하고 있으며, 고급 과자 및 커피 제품의 포장재 선택 기준을 재구성하고 있습니다.

PVDC는 2025년, 습기에 민감한 의약품 및 고급 육류 가공품에 필수적인 탁월한 수증기 및 산소 투과 방지 성능으로 인해 배리어재 시장에서 44.60%의 압도적인 점유율을 유지했습니다. 환경 규제 당국의 염소 함유 폴리머에 대한 감시 강화라는 구조적 역풍에 따라 컨버터 업체들은 산소 차단 성능(0.1 cc/m2/일 미만)을 유지하면서 PVDC 프리 구조의 시험 도입을 추진하고 있습니다. EVOH는 결정질 에틸렌 블록 구조로 인해 높은 투명성과 우수한 건조 상태 산소 차단성을 발휘하면서 완벽한 호환성을 유지하기 때문에 5.62%의 연평균 복합 성장률(CAGR)로 괄목할 만한 성장세를 보이고 있습니다.

알루미늄 포일은 수증기 투과율이 0.001g/m2/일 이하이어야 하는 블리스 터 포장 뚜껑과 레토르트 파우치에서 여전히 중요한 역할을 하고 있습니다. 그러나 탄소세 시나리오와 알루미늄 포일 가격의 변동성으로 인해 브랜드 소유주들은 환경 친화적인 대안으로 PET에 실리카 증착 기술로 전환을 모색하고 있습니다. PEN(폴리에틸렌나프탈렌)은 고온 응용 분야 및 전자부품의 마이크로 캡슐화 응용 분야에 적용되며, 치수 안정성이 비용 민감도를 능가하는 틈새 수요를 확보하고 있습니다. 연구 파이프라인에는 나노 스케일 두께로 산소 투과율을 99% 감소시킬 수 있는 산화 그래핀 코팅이 포함되어 있으며, 롤투롤 코팅의 균일성이 개선되는 대로 2028년 이후 상업적 규모로 실현될 것으로 예측됩니다.

배리어재료 보고서는 유형별(알루미늄, 에틸렌비닐알코올(EVOH), 폴리에틸렌나프탈레이트(PEN), 폴리염화비닐리덴(PVDC), 기타), 최종사용자 산업별(식음료, 제약, 농업, 화장품, 자동차, 기타), 지역별(아시아태평양, 북미, 유럽, 유럽, 남미, 중동 및 아프리카), 지역별(아시아태평양, 북미, 유럽, 남미, 중동. 남미, 중동/아프리카) 별로 분석했습니다. 시장 예측은 금액 기준(USD)으로 제시됩니다.

아시아태평양은 2025년 매출의 41.10%를 차지할 것으로 예상되며, 이는 타의 추종을 불허하는 제조 규모와 현재 엄격한 미국 및 EU 표준을 준수하는 규제 조화가 반영된 결과입니다. 중국에서는 2024년 GB 4806.7이 시행되어 총 이동량 제한이 10mg/dm2 이하로 강화됨에 따라 약사법 III류 기준에 부합하는 고순도 EVOH 수지 및 PVDC-PVDC 복합 필름의 신속한 인증 취득이 촉진되었습니다. 2025년 6월부터 시행되는 일본의 포지티브 리스트에 따라 국내 컨버터는 30nm 두께의 실리카 층을 도포할 수 있는 플라즈마 코팅 장비의 도입을 추진하고 있습니다. 완벽한 투명성을 유지하면서 알루미늄 포일 수준의 차단성을 실현했습니다. 인도에서는 제네릭 의약품의 승인 가속화에 따라 블리스 터 포장 수출이 두 자릿수 성장세를 지속하고 있습니다. 운송 지연 및 환위험을 피하기 위해 국내 공동 압출 능력에 대한 투자가 진행되고 있습니다.

북미에서는 전자상거래에 따른 펑크 방지 파우치 수요와 캘리포니아주의 PFAS 사용 금지 등 유해물질 저감법 등 규제 강화가 시장을 주도하고 있습니다. 생산자책임재활용(EPR) 비용 확대에 대한 브랜드 대응으로 단일 소재 PE 파우치로의 재설계가 이미 진행 중입니다.

유럽은 순환경제 의무화가 가장 빠르게 진행되고 있으며, PPWR 초안은 2030년까지 시장 진입을 위한 전제조건으로 재활용 설계를 규정하고 있습니다. 독일과 프랑스에서는 연질필름 보증금 반환제도를 시범적으로 도입하고 있습니다. 남미와 중동 및 아프리카은 규모는 작지만, 특히 영양강화식품과 시판 의약품에서 소득 성장에 대한 높은 탄력성을 보이고 있습니다. 열대 기후와 유통 중단을 견딜 수 있는 장벽성 포장이 필요합니다.

The Barrier Material market is expected to grow from USD 3.46 billion in 2025 to USD 3.64 billion in 2026 and is forecast to reach USD 4.71 billion by 2031 at 5.26% CAGR over 2026-2031.

Rising demand for multilayer films that extend food shelf life, rapid pharmaceutical capacity additions in Asia-Pacific, and accelerated regulatory moves away from PFAS chemicals are the principal forces shaping growth. Brand-owner commitments to circular-economy goals are steering investments toward recyclable polyolefin structures, while the e-commerce boom pushes converters to engineer tougher, puncture-resistant formats that preserve barrier integrity through longer supply chains. Concurrently, tightening raw-material supply balances for aluminum, ethylene and propylene are elevating cost-pass-through clauses in supply contracts, creating incentives for vertical integration among large resin producers. Competitive differentiation is shifting from absolute barrier performance to the ability to achieve comparable protection with lower environmental footprints and validated compliance dossiers across multiple jurisdictions.

High-moisture bakery, dairy, and ready-meal categories rely on oxygen- and water-vapor-tight films engineered to slow microbial growth and lipid oxidation. Antimicrobial barrier plates infused with plant-based actives such as geraniol have demonstrated 5-10-day shelf-life extensions for breads and pastries, while maintaining migration levels below global food-contact thresholds. Modified-atmosphere pouches incorporating high-clarity EVOH achieve oxygen-transmission rates below 0.1 cc/m2/day, reducing the need for preservatives in chilled meats. Edible chitosan-gallic acid coatings developed by Korean researchers add UV protection and antimicrobial performance without altering appearance, opening premium niches that command 20-30% price uplifts over commodity packaging. Shelf-life extension aligns directly with global food-waste-reduction targets and positions the barrier material market as a central enabler of United Nations Sustainable Development Goal 12.

Japan's Positive List for pharmaceutical contact materials, effective June 2025, mandates moisture-transmission rates below 0.05 g/m2/day for hygroscopic actives, accelerating adoption of premium PVDC and EVOH laminates. China's GB 4806.7-2023 and GB 43352-2023 standards embed low-migration limits that favor suppliers with robust analytical data and validated clean-room films. India's pharmaceutical exports are rising more than 15% annually, compelling blister suppliers to certify compliance with U.S. FDA, EMA and PMDA requirements simultaneously. These dynamics push global converters to localize film production in Asia-Pacific, strengthening regional supply security and shortening lead times. Advanced barrier structures also support biosimilar formulations, which require oxygen levels below 1 ppm to maintain protein stability during distribution.

The EU is evaluating an EUR 0.80/kg packaging tax on aluminum to reflect its high carbon intensity relative to polymer alternatives, a policy expected to curb thin-foil usage in snack-food flexibles. Brand-owner life-cycle assessment models show aluminum layers boosting package CO2 emissions by up to 300% versus mono-PE structures with functional coatings, prompting reformulation even where metallized films previously set performance benchmarks. Although foil remains irreplaceable in ultra-high-humidity pharmaceutical packs, the search for low-carbon smelting processes and latch-seamless recycling pathways has intensified. Pilot electrolysis cells using inert anodes demonstrated 7 tons CO2-equivalent savings per ton of aluminum in 2025, yet scale-up remains five years away. In the interim, multi-layer structures featuring evaporated aluminum oxide or silica coatings on PET are capturing share despite higher material costs, reshaping material selection criteria for premium confectionery and coffee formats.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

PVDC retained a commanding 44.60% barrier material market share in 2025, owing to unmatched water-vapor and oxygen impermeability critical for moisture-sensitive pharmaceuticals and premium processed meats. The segment is confronting structural headwinds as environmental agencies scrutinize chlorine-containing polymers, incentivizing converters to pilot PVDC-free structures that still match sub-0.1 cc/m2/day oxygen-barrier thresholds. EVOH stands out, posting a 5.62% CAGR, because its crystalline ethylene blocks yield high clarity and exceptional dry-state oxygen protection while remaining fully compatible.

Aluminum foil sustains relevance in blister lidding and retort pouches where water-vapor-transmission rates must reside below 0.001 g/m2/day; however, carbon-tax scenarios and foil price volatility are nudging brand owners toward silica-oriented deposition on PET as a lower-footprint substitute. PEN addresses high-temperature and electronics micro-encapsulation uses, capturing niche demand where dimensional stability outweighs cost sensitivity. Research and devlopment pipelines include graphene-oxide coatings capable of achieving 99% reduction in oxygen permeation at nanoscale thicknesses, projected to reach commercial scale post-2028 once roll-to-roll coating uniformity improves.

The Barrier Material Report is Segmented by Type (Aluminum, Ethylene Vinyl Alcohol (EVOH), Polyethylene Naphthalate (PEN), Polyvinylidene Chloride (PVDC), and Other Types), End-User Industry (Food and Beverage, Pharmaceutical, Agriculture, Cosmetics, Automotive, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific contributed 41.10%, to 2025 revenue, reflecting unmatched manufacturing scale and regulatory harmonization that now mirrors stringent U.S. and EU standards. China's 2024 rollout of GB 4806.7 tightened total-migration limits to less than or equal to 10 mg/dm2, catalyzing the rapid qualification of high-purity EVOH resins and PVDC-PVDC duplex films certified under Type III pharmacopoeia requirements. Japan's June 2025 Positive List has propelled domestic converters to install plasma-coating units capable of applying only 30 nm thick silica layers, achieving aluminum-foil-like barriers while remaining fully transparent. India's blister-pack exports continue double-digit expansion as generic drug approvals accelerate, prompting investments in in-country co-extrusion capacity to sidestep shipping delays and currency risk.

North America is buoyed by e-commerce-triggered demand for puncture-resistant pouches and legislative action, such as California's toxin-reduction acts that eliminate PFAS usage. Brand responsiveness to Extended Producer Responsibility (EPR) fees is already visible in reformulations toward mono-material PE pouches.

Europe is advancing fastest on circular-economy mandates, with PPWR draft language stipulating design-for-recycling as a prerequisite for market access by 2030; Germany and France are piloting deposit-return schemes for flexible films. South America and the Middle East and Africa, while smaller, exhibit high elasticity to income growth, particularly for fortified foods and over-the-counter medicines, which require barrier formats resistant to tropical climates and distribution gaps.