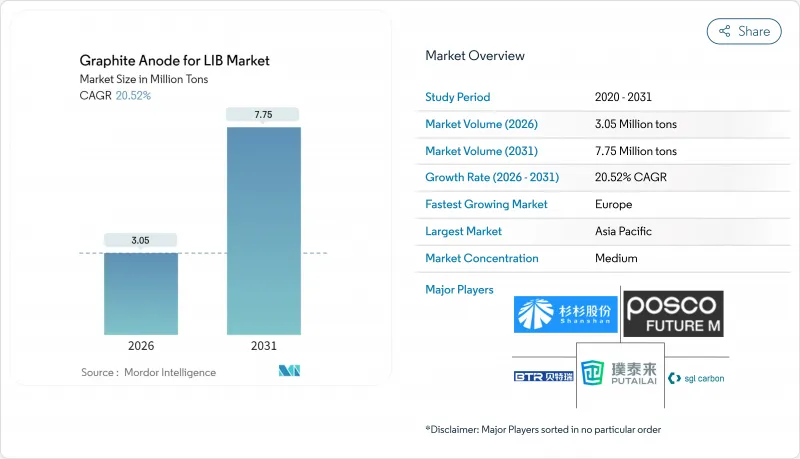

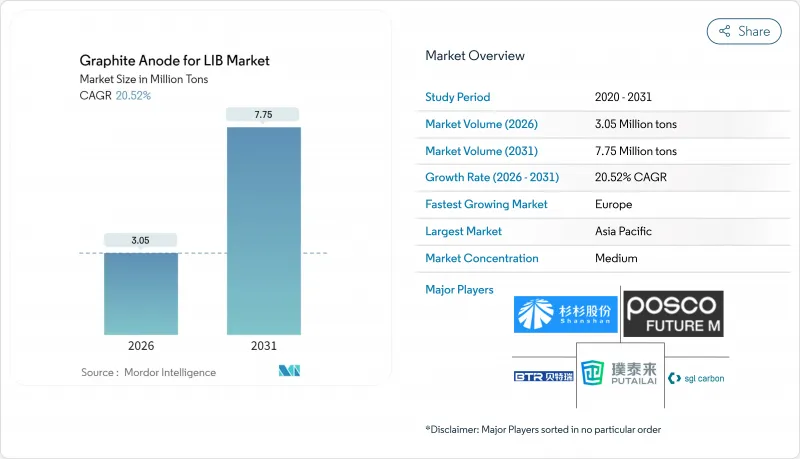

LIB용 흑연 음극 시장 규모는 2025년 253만 톤으로 평가되었고, 2026년 305만 톤에서 2031년까지 775만 톤에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) CAGR은 20.52%로 성장이 전망되고 있습니다.

전기자동차(EV)용 배터리 용량 증가, 거치형 축전 프로젝트의 확대, 국내 조달을 장려하는 현지 조달 의무화가 함께, 채용이 가속하고 있습니다. 합성 흑연은 그 설계된 미세구조가 급속 충전의 요구를 견디기 때문에 여전히 수량 기준으로 주도적 지위를 유지하고 있습니다. 그러나 비용에 중점을 둔 천연 흑연은 자동차 등급 순도에 저비용으로 도달하는 정제 기술로 성능 차이를 줄이고 있습니다. 미국 인플레이션 억제법에서 인도 생산 연동형 인센티브 제도에 이르는 지역별 우대책으로 공급망은 기가팩토리 근교의 지역 클러스터로 분산화가 진행되고 있습니다. 이 변화는 물류 비용을 압축하는 동시에 원산지 규칙에 대한 적합성을 높이고 있습니다. 경쟁의 치열함은 여전히 높아 중국의 기존 기업이 전구체 코크스에 수직 통합을 확대하는 한편, 한일의 전문 기업은 독자적인 코팅 화학 기술로 차별화를 도모하고, 구미의 신규 참가 기업은 정부 대출을 활용해 저탄소 시설을 건설하고 있습니다. 동시에 수출 관리 리스크, 배출 규제, 실리콘 리치 음극 등장이 다가오는 가운데, 배터리 제조업체는 합성 원료 및 천연 원료의 이중 조달을 진행하고 있으며, LIB용 흑연 음극 조달 전략을 더욱 재구축하고 있습니다.

2024년 1월부터 2025년 10월까지 발표된 기가팩토리 계획은 표준 흑연 부하에서 음극 수요를 증가시켰습니다. 2027년까지 CATL의 데브레첸 공장과 BYD의 라용 공장이 추가 생산 능력을 공급할 전망입니다. 한편 테슬라의 텍사스 공장은 시라 리소시즈사의 루이지애나주 생산량의 대부분을 10년간의 오프테이크 계약으로 확보했습니다. 미국 인플레이션 억제법 및 EU 배터리 규제에서 정한 함량 기준을 충족하기 위해 셀 제조업체는 현재 최종 조립 기지에서 200km 이내에 음극 라인을 설치해야 합니다. 이 전략은 규제 준수를 보장할 뿐만 아니라 현지 공급업체로부터 업스트림 공급량을 확보하는 것입니다. 수요가 늘어나면서 설비 가동 속도가 쫓지 않는 상황에서 이 광범위한 확장으로 LIB용 흑연 음극 시장에서는 2027년까지 구조적인 공급 부족이 발생할 것으로 전망됩니다.

2024년 중국산 합성 흑연의 단가는 상당한 하락을 기록했습니다. 이 변화는 내몽골과 사천성에 있어서의 신규로의 가동이 요인으로 되어 있습니다. 통합 생산 기업은 중국 석유화공(시노펙)과의 계약을 활용하여 석유침상코크스를 할인 가격으로 조달하고 있습니다. 아체손로를 고가동률로 운전함으로써 만들어진 비용 절감분을 전지 제조업체 고객에게 환원하고 있습니다. 이 가격 하락은 엔트리 레벨 EV 및 오토바이 시장에서 일본과 한국의 경쟁업체에 우위를 가져왔습니다. 그러나 유럽 연합의 잠정적인 안티 댐핑 관세로 인해 유럽 시장에서의 이점은 현재 완화되고 있습니다. 결과적으로, 이 비용 중심의 대체 현상은 수량의 성장을 가속할 뿐만 아니라 LIB용 흑연 음극 시장에서 지정학적 긴장을 증가시킵니다.

2024년 중국은 세계의 천연 흑연 채굴 생산량 및 구상화 처리 능력을 지배했습니다. 2023년 12월의 수출 허가 확대에 따라 베이징 당국은 현재 배터리용 플레이크의 수출을 모두 관리하고 있으며, 중국 국외로의 출하 지연을 일으키고 있습니다. 2024년 초, LG 에너지 솔루션은 허가 지연으로 브로츠와프 공장의 운영 중단에 직면했으며, 삼성 SDI는 더 비싼 합성 원료를 선택했습니다. 모잠비크의 바라마광산과 마다가스카르의 모로 광산에서 조업을 확대하고 있음에도 불구하고, 중국 이외 공급원으로부터의 총 공급량은 2026년까지 부족할 것으로 예상되어 LIB용 흑연 음극 시장의 변동성이 높아지고 있습니다.

합성 흑연은 NMC 및 NCA 화학 조성에서 비교할 수 없는 사이클 수명과 초급속 충전 프로토콜과의 호환성으로 2025년 공급량의 56.78%를 차지했습니다. 한편 천연 흑연은 엔트리 레벨 LFP 배터리에서 틈새 시장을 발견했습니다. 이 배터리는 초기 사이클 효율이 낮고 비용면에서 우수성을 가지고 있습니다. 이 비용 효율성은 견조한 성장을 이끌어내고 있으며, 2031년까지 24.10%의 연평균 복합 성장률(CAGR)이 예상됩니다. 결과적으로 LIB용 흑연 음극에 사용되는 천연 흑연 제품 시장은 크게 확대될 전망입니다. 이에 반해 합성 흑연의 생산량은 보다 완만한 성장이 예상됩니다. 금속 불순물을 10ppm 미만, 탄소 순도를 99.95%로 높이는 선진적인 정제 기술에 의해 성능 격차는 해소되었습니다. 이 새로운 신뢰성은 BYD의 Blade Battery가 2만 5,000달러 미만의 EV 라인에서 천연 원료를 고비율로 채용하고 있다는 사실에서도 분명합니다.

코팅 기술은 진화를 계속하고 있으며, 현재는 두 소재 모두 피치 유래 탄소 또는 탄소 나노 튜브층을 활용하여 초기 쿨롱 효율의 향상을 도모하고 있습니다. 이러한 수렴 경향에도 불구하고, 합성 흑연은 달력 수명 유지에서 우위를 유지하고 있습니다. 이 장점은 150,000마일 보증을 제공하는 자동차 제조업체에게 매우 중요합니다. EU의 탄소 규제에 의해 표준 항속 거리 모델은 천연 흑연으로 이행하는 한편, 미국 국내 조달 크레딧 제도는 고급차용으로 합성 흑연 회귀를 촉구하고 있습니다. 이 동향에 의해 LIB용 흑연 음극의 재료 치환은 세계가 아닌 지역적인 패턴을 형성합니다. 결과적으로 업계는 양극화가 진행되어 고볼륨 및 가격 중시의 천연 흑연 부문과 고급 및 엔지니어링 특화의 합성 흑연 틈새 시장이 명확하게 나뉘어져 있습니다.

LIB용 흑연 음극 시장 보고서는 음극 재료 유형별(합성 흑연 및 천연 흑연), 최종 용도별(전기자동차, 에너지 저장 시스템, 소비자용 전자 장비 등), 지역별(아시아태평양, 북미, 유럽 및 세계 기타 지역)로 분석됩니다. 시장 예측은 수량(톤)과 금액(달러)으로 제시됩니다.

아시아태평양은 2025년 출하량의 73.85%를 차지했으며, 주로 중국의 방대한 제조 능력에 견인되었습니다. 이 나라에서는 정제 코크스 소성, 흑연화, 구상화, 셀 조립 등의 공정이 단일성 클러스터 내에서 원활하게 통합되어 있습니다. 중국의 우위성은 저비용 전력, 성에 의한 토지 할인, 신속한 허가 절차에 있으며, 비용 리더십을 확고하게 하고 있습니다. 한편, 일본과 한국은 독자 개발의 코팅 기술로 강화된 고이익률의 합성 흑연으로 축족을 옮기고 있습니다. 특히 미쓰비시 화학의 MAGE-M 시리즈는 3nm 미만의 코팅 기술로 고사이클 수명을 실현하고, LIB용 흑연 음극 시장에서 성능 중시의 틈새 시장을 확립하고 있습니다.

유럽은 2031년까지 연평균 복합 성장률(CAGR) 28.05%라는 가장 급격한 성장이 전망되고 있습니다. 이것은 자동차 제조업체가 EU 전지 규제(2027년까지 역내 조달율의 기준치를 의무화)에 대한 대응을 진행하는 움직임에 견인되는 것입니다. 스웨덴의 노스볼트사는 이미 앞서 수용액 야금 공정에 의한 흑연 사이클을 대규모로 실시하여 생산량 확대를 계획하고 있습니다. 한편 BASF의 슈발츠하이데 공장에서는 재생에너지를 활용하여 제조 공정(크래들 투 게이트)의 탄소 강도를 저감하면서 합성 흑연을 연간 생산하고 있습니다. 게다가 프랑스의 베르콜과 이탈리아의 이탈 볼트가 합작 사업을 개시해, 연간 생산량의 확대를 목표로 하고 있어 유럽의 강화를 도모하고 있습니다. 그러나 유럽의 현금 비용은 여전히 아시아태평양보다 상당히 높기 때문에 LIB용 흑연 음극 시장에서 경쟁력을 유지하기 위해서는 탄소 국경 조정이 매우 중요합니다.

2024년 생산량 점유율이 낮았던 북미는 보조금을 제공하는 섹션 45X 세제 우대책을 배경으로 2030년까지 점유율이 2배 이상으로 확대될 전망입니다. 실러사의 비달리아 공장은 2025년에 현저한 생산 페이스를 달성해 국내산 프리미엄을 활용해 테슬라의 텍사스 기가팩토리에 직접 공급하고 있습니다. 테네시주에서는 에너지부 대출 보증을 받은 노보닉스사가 2026년까지 합성 흑연의 생산 능력을 시작하여 인근 포드사 및 GM사용 공급을 시작할 예정입니다. 한편 캐나다의 퀘벡 광산에서는 천연 플레이크 공급량을 늘리고 있지만 연방 정부의 허가 취득에 시간이 걸리고 있으며, 그 큰 영향은 2027년 이후에 어긋날 전망입니다. 멕시코는 전극 코팅 및 팩 조립에서 비용 경쟁력으로 두드러지지만, 주요 흑연 자산이 부족하기 때문에 단기적으로 북미 공급은 제한된 상태가 지속될 전망입니다.

The Graphite Anode for LIB Market was valued at 2.53 million tons in 2025 and estimated to grow from 3.05 million tons in 2026 to reach 7.75 million tons by 2031, at a CAGR of 20.52% during the forecast period (2026-2031).

Rising electric-vehicle (EV) cell capacity, expanding stationary storage projects, and localization mandates that reward domestic content are collectively accelerating adoption. Synthetic graphite retains its volume leadership because its engineered microstructure tolerates fast-charge demands; however, cost-sensitive natural graphite is closing the performance gap as purification routes reach automotive-grade purity at a lower cost. Regional incentive packages-from the U.S. Inflation Reduction Act to India's Production-Linked Incentive scheme-are fragmenting supply chains into local clusters located near gigafactories, a shift that compresses logistics costs while improving compliance with origin rules. Competitive intensity remains high as Chinese incumbents extend vertical integration into precursor coke, Japanese and Korean specialists differentiate through proprietary coating chemistries, and Western newcomers attract government loans to build low-carbon facilities. Simultaneously, export-control risks, emissions regulations, and the impending arrival of silicon-rich anodes are prompting cell makers to dual-source synthetic and natural feedstocks, further reshaping procurement strategies for the graphite anode in the LIB market.

Between January 2024 and October 2025, announced gigafactory projects led to an incremental anode requirement at standard graphite loadings. By 2027, CATL's Debrecen and BYD's Rayong projects are expected to contribute additional capacity. Meanwhile, Tesla's Texas facility has secured a significant portion of Syrah Resources' Louisiana output through a decade-long offtake agreement. To meet the content thresholds set by the U.S. Inflation Reduction Act and EU Battery Regulation, cell manufacturers are now required to position anode lines within 200 km of their final assembly points. This strategy not only ensures compliance but also secures upstream volumes from local suppliers. As commissioning struggles to keep pace with demand, this widespread expansion is set to create a structural deficit in the graphite anode market for lithium-ion batteries (LIB) until 2027.

In 2024, unit prices for Chinese synthetic graphite experienced a significant decline, a shift attributed to the activation of new furnaces in Inner Mongolia and Sichuan. Integrated producers, leveraging Sinopec contracts, procure petroleum needle-coke at discounted rates. They operate Acheson furnaces at a high utilization rate, subsequently passing these savings on to their cell customers. While this price drop gives an edge over Japanese and Korean competitors in the entry-level EV and two-wheeler markets, provisional EU anti-dumping duties now moderate this advantage within the European market. As a result, this cost-driven substitution not only propels volume growth but also heightens geopolitical tensions in the graphite anode market for lithium-ion batteries.

In 2024, China dominated the world's mined natural graphite production and global spheroidization capacity. Following an expansion of export licenses in December 2023, Beijing now oversees all battery-grade flake exports, causing delays for shipments outside China. In early 2024, LG Energy Solution faced a shutdown at its Wroclaw plant due to permit delays, while Samsung SDI opted for a pricier synthetic feedstock. Despite scaling operations at Mozambique's Balama and Madagascar's Molo mines, the total supply from non-Chinese sources is projected to fall short until 2026, leading to heightened volatility in the graphite anode market for lithium-ion batteries (LIBs).

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Synthetic graphite captured 56.78% of 2025 volume, thanks to its unmatched cycle life in NMC and NCA chemistries, as well as its compatibility with ultra-fast charging protocols. Meanwhile, natural graphite found its niche in entry-level LFP batteries. These batteries, although they accept a lower first-cycle efficiency, offer a cost advantage. This cost efficiency is driving robust growth, forecasted to propel a 24.10% CAGR forecast to 2031. As a result, the market for natural graphite products used in graphite anodes for LIBs is set to surge significantly. In contrast, synthetic volumes are anticipated to grow at a more modest rate. Advanced purification techniques, which achieve metallic impurities below 10 ppm and carbon purity of 99.95%, have bridged the performance gap. This newfound confidence is evident as BYD's Blade Battery opts for a high percentage of natural feedstock in its sub-USD 25,000 EV line.

Coating technologies are evolving, with both materials now utilizing pitch-derived carbon or carbon-nanotube layers to boost initial coulombic efficiency. Despite this convergence, synthetic graphite maintains an edge in calendar-life retention. This advantage is pivotal for automakers providing 150,000-mile warranties. While EU carbon regulations may steer standard-range models towards natural graphite, U.S. domestic-content credits are incentivizing premium vehicles to lean back towards synthetic graphite. This dynamic is creating a regional, rather than a global, pattern of material substitution in the graphite anode for the LIB market. Consequently, the industry is splitting into two distinct segments: a high-volume, price-sensitive natural-graphite sector and a premium, engineered synthetic niche.

The Graphite Anode for LIB Market Report is Segmented by Anode Material Type (Synthetic Graphite and Natural Graphite), End-Use Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, and Others), and Geography (Asia-Pacific, North America, Europe, and Rest of the World). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Asia-Pacific supplied 73.85% of 2025 shipments, largely driven by China's significant manufacturing capacity. This capacity seamlessly integrates processes like refinery coke calcination, graphitization, spheroidization, and cell assembly within single provincial clusters. China's edge comes from low-cost electricity, provincial land discounts, and expedited permitting, solidifying its cost leadership. Meanwhile, Japan and South Korea are pivoting towards high-margin synthetics, enhanced with proprietary coatings. Notably, Mitsubishi Chemical's MAGE-M series commands a premium for its sub-3 nm coatings, boasting high full-depth cycles, highlighting a performance-centric niche in the graphite anode market for lithium-ion batteries (LIB).

Europe is expected to exhibit the steepest regional growth, at a 28.05% CAGR, to 2031, driven by automakers' efforts to align with the EU Battery Regulation, which mandates a regional content threshold by 2027. Northvolt's site in Sweden is already ahead of the curve, recycling graphite through a hydrometallurgical loop with significant output and plans for expansion. Concurrently, BASF's Schwarzheide facility produces synthetic graphite annually, harnessing renewable energy to reduce its cradle-to-gate carbon intensity. Further bolstering the region, France's Verkor and Italy's Italvolt have initiated joint ventures aimed at increasing annual production. However, challenges loom as European cash costs are still significantly higher than those in the Asia-Pacific region, making carbon-border adjustments crucial for competitiveness in the graphite anode market for LIBs.

North America, which accounted for a smaller share of the 2024 volume, is poised to more than double its share by 2030, driven by Section 45X credits that offer subsidies. Syrah's Vidalia plant achieved a notable run-rate in 2025, directly supplying Tesla's Texas gigafactory, capitalizing on a premium for domestic origin. In Tennessee, Novonix, with backing from a Department of Energy loan guarantee, is set to launch synthetic capacity by 2026, catering to Ford and GM within a close radius. While Canada's Quebec mines are ramping up natural-flake supply, they're grappling with extended federal permitting, pushing their significant impact to post-2027. Mexico stands out for its cost-effective electrode coating and pack assembly, yet the absence of major graphitization assets keeps the North American supply constrained in the short term.