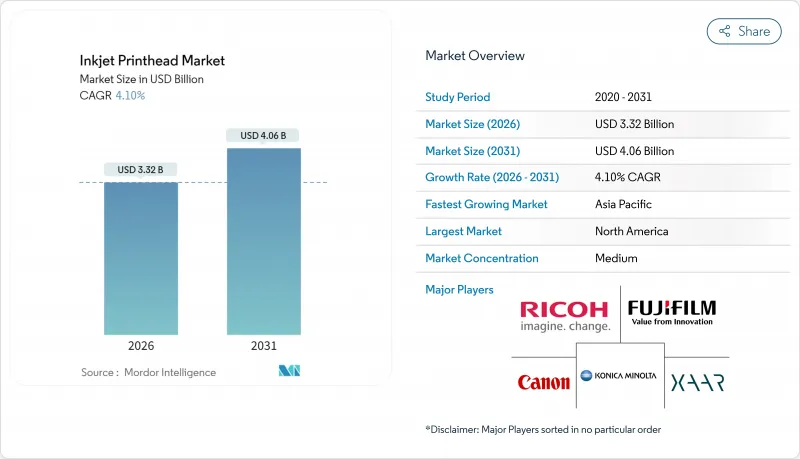

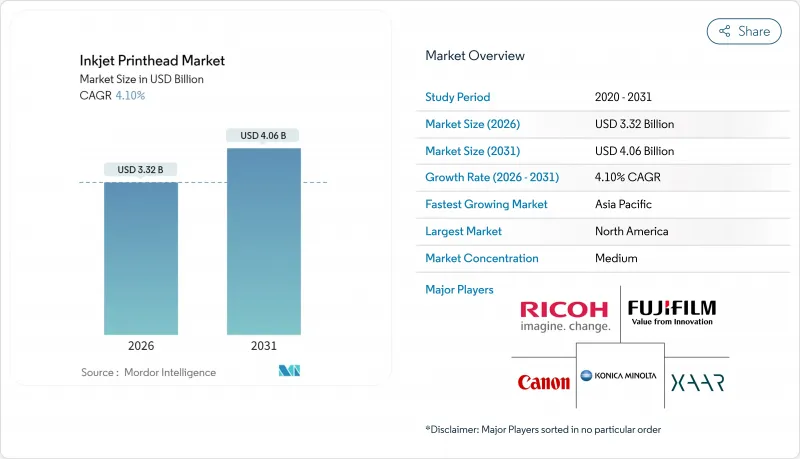

잉크젯 프린트헤드 시장은 2025년 31억 9,000만 달러로 평가되었고, 2026년에는 33억 2,000만 달러, 2031년에는 40억 6,000만 달러로 성장할 전망입니다. 2026년에서 2031년에 걸쳐 CAGR은 4.1%를 나타낼 것으로 예상됩니다.

오피스 인쇄에서 고정밀 산업용으로의 이행이 이 성장 궤도를 지원하고 있습니다. 제조업체 각 사는 마이크로 전기 기계 시스템(MEMS), 박막 압전 액추에이터, 싱글 패스 구조 등을 활용하고 있습니다. 견고한 전자상거래 활동, 브랜드 개인화 전략, 증가하는 지속가능성에 대한 요구가 수성 안료 잉크 수요를 뒷받침하는 반면, 적층 성형 기술은 새로운 고수익 기회를 창출하고 있습니다. 기존 벤더는 다년간 특허 포트폴리오와 이익률을 저하시키지 않고 고객 기반을 확대하는 플랫폼 판매 모델을 통해 지위를 지키고 있습니다. 세라믹과 반도체공급망 변동은 엄청난 이익을 압박하고 있지만, 예지 보전 분석은 가동 중단 위험을 줄이고 설비 종합 효율(OEE)을 향상시킵니다.

싱글 패스 인쇄기는 여러 번 사이클을 제거하고 생산 시간을 최대 70% 단축하므로 단납기 생산의 경제성을 실현합니다. EFI사의 Nozomi C18000은 유럽의 컨버터 기업에 도입되어 1,200dpi로 매분 400피트의 선속도를 달성하여 처리량 경제성을 실증하고 있습니다. 섬유 제조업체도 같은 성과를 올리고 있어, Kornit사의 Atlas MAX는 계절마다의 소 로트 생산에 대응하면서, 색정도를 손상시키지 않습니다. 신속한 납기 대응에 대한 수요가 지속적인 프린트 헤드 수주를 견인하고 있으며, 특히 다양한 점도와 고속 운전에 대응한 모델이 요구되고 있습니다. 포장 분야에서 개인화가 확대됨에 따라 단일 패스 시스템은 기존에 정적이었던 생산 라인을 유연한 데이터 중심 자산으로 전환합니다. 각 유닛이 여러 개의 압전 헤드 컬럼을 채택하기 때문에 이 기술은 부품 공급업체에게 안정적인 수요 창출원이 되었습니다.

MEMS 노즐 어레이와 박막 액추에이터의 조합에 의해 300m/min의 라인 속도로 2피코리터 미만의 미세 액적을 실현. 의약품 코팅이나 미세 회로 형성 등 정밀 가공을 가능하게 합니다. 자아사의 2024년 특허 시리즈에서는 각 노즐에 독립 구동 전자회로를 탑재하고, 비상 중에 액적량을 가변 제어하는 기술을 상세하게 설명하고 있습니다. 교세라의 KJ4 플랫폼은 600노즐/인치와 1.5-42피코리터의 가변 액적을 실현하여 그래픽 인쇄와 기능성 도포를 모두 가능하게 함으로써 이 개념을 상품화했습니다. 이 진보는 잉크 낭비를 줄이고 운영 비용을 줄입니다. 왜냐하면 작은 방울은 제곱미터당 안료 사용량을 줄이기 때문입니다. 장기적으로 이러한 헤드는 속도보다 정밀도가 우선하는 바이오프린팅과 스마트 패키징의 노력을 지원하는 기반이 됩니다.

고급 잉크젯 라인은 동등한 처리 능력을 가진 레이저 코더나 플렉소 인쇄기에 비해 40-60% 비쌉니다. 가격에 민감한 지역의 소규모 제조업체는 장기적으로 보면 설치 및 판대가 낮게 유지되지만 업데이트를 늦추고 있습니다. OEM이 제공하는 금융 프로그램은 초기 장벽을 완화하지만, 단색 마킹과 초대량 SKU에서는 여전히 기존 키트의 ROI 계산이 유리합니다. 신흥 경제국의 통화 변동성은 이 주저를 강화하고 잉크젯 프린트헤드 시장의 성장 속도를 약간 둔화시키고 있습니다.

2025년 시점의 잉크젯 프린트헤드 시장 점유율에서 드롭 온 디맨드 방식이 67.98%를 차지하고 연속 흐름 방식을 크게 웃돌았습니다. 압전식은 열 스트레스 없이 2피코리터 미만의 정확도를 요구하는 산업 현장에 공급되며, 열식 카트리지는 비용에 중점을 둔 사무 기기에서 지위를 유지하고 있습니다. 이 부문은 5.17%의 연평균 복합 성장률(CAGR)이 예상되며, 이는 단위 성장의 급증이 아니라 재료 과학의 지속적인 개선을 반영합니다. 연속 기술은 끊임없는 흐름이 최고 속도를 가능하게 하는 코딩 틈새 시장을 유지하고 있지만, 정확성 부족이 보다 광범위한 보급을 방해하고 있습니다.

박막 액추에이터는 소비 전력 절감과 1,200dpi의 네이티브 해상도 향상을 실현해, 고밀도 그래픽이나 기능성 인쇄에 있어서 드롭 온 디맨드 방식의 우위성을 높이고 있습니다. 리코의 MH5421F는 멀티 드롭 파형을 탑재해, 4-42피코리터의 잉크량을 온 디맨드로 토출, 간판용 기재와 PCB 기판 모두에 대응합니다. 단일 패스 라인이 골판지 공장 및 섬유 공장에 보급됨에 따라 각 장치에는 수백 개의 노즐이 통합되어 잉크젯 프린트헤드 시장 규모에 상당한 교체 예비 부품의 지속적인 수익을 제공합니다.

수성 잉크는 규제 우대책과 강화된 안료 봉입 화학 기술에 지지되어 2025년에는 매출의 31.76%를 차지했습니다. UV경화형 잉크는 후진을 숭배하고 있습니다만, 고온 노출 없이 플라스틱이나 금속에 순간에 접착하는 LED 경화 기술의 보급에 의해 2031년까지 연평균 복합 성장률(CAGR)5.72%를 기록할 전망입니다. 내후성이 환경면에서의 트레이드 오프를 웃도는 옥외 배너 용도에서는 용제계 잉크가 계속 사용되고, 신축성을 필요로 하는 고신장성 텍스타일에는 라텍스계 블렌드 잉크가 채택되고 있습니다.

브랜드 소유자가 순환형 경제 지표를 중시하는 가운데, 바이오의 배합 기술이 성장 분야로서 대두하고 있습니다. INX사의 식물 유래 제품군은 지속 가능한 원료가 색역이나 내구성을 손상시키지 않는다는 것을 실증하고 있습니다. 한편, UV 헤드는 접이식 카톤 라인에 도입이 진행되고 있어 순간 경화에 의한 라미네이트 공정의 단축으로 총 생산 리드 타임을 삭감합니다.

북미는 확립된 R&D 생태계와 예측 보전 플랫폼의 신속한 도입으로 2025년 수익의 39.70%를 유지했습니다. 용제 배출을 제한하는 연방 환경 규제는 수성 잉크로의 업그레이드 투자를 촉진하고, 성숙한 전자상거래 기반이 직렬화 및 스캔 가능한 포장에 대한 수요를 확고하게 하고 있습니다.

아시아태평양은 중국의 스마트 팩토리 계획과 일본의 액추에이터 기술에 견인되어 6.43%의 연평균 복합 성장률(CAGR)이 전망됩니다. 엡손의 중국 신조립 거점은 리드 타임 단축과 환율 변동 리스크 헤지를 실현했고, 미마키의 TS200은 고신장성 섬유 대응 승화 헤드를 탑재해 동남아시아의 폴리에스테르 공장을 타겟으로 하고 있습니다. 지역적 비용 우위성은 OEM 아웃소싱을 유치하고 잉크젯 분사 기구에 필수적인 세라믹 MEMS 칩의 현지 부품 클러스터가 강화되고 있습니다.

유럽은 기술력이 풍부한 것, 신규 설비 도입을 웃도는 갱신 수요에 의해 성장은 성숙 단계에 있습니다. REACH 규정에 따라 낮은 VOC 잉크로의 전환이 가속화되고, 케니히 앤드 바우어 듀스트는 고부가가치 소량 로트 안건으로 고액 설비 투자를 정당화하는 카톤 인쇄기를 전개하고 있습니다. 순환형 포장에 대한 정부 지원책이 식품 및 의약품 컨버터에 있어서의 헤드 갱신의 안정 수요를 지지하고 있습니다.

The inkjet printhead market is expected to grow from USD 3.19 billion in 2025 to USD 3.32 billion in 2026 and is forecast to reach USD 4.06 billion by 2031 at 4.1% CAGR over 2026-2031.

A migration from office printing toward high-precision industrial use underpins this trajectory as manufacturers exploit micro-electromechanical systems, thin-film piezo actuators, and single-pass architectures. Robust e-commerce activity, brand personalization strategies, and rising sustainability mandates are reinforcing demand for water-based pigmented inks, while additive manufacturing creates fresh, high-margin opportunities. Established vendors defend their positions through multi-year patent portfolios and platform sales models that expand the accessible customer base without diluting margins. Supply chain volatility in ceramics and semiconductors continues to pressure gross profits, yet predictive-maintenance analytics soften downtime risks and lift overall equipment effectiveness.

Single-pass presses eliminate multi-pass cycles and cut production time by up to 70%, making short runs financially viable. EFI's Nozomi C18000 installs across European converters and delivers 400 linear ft/min at 1,200 dpi, validating throughput economics. Textile producers observe similar gains; Kornit's Atlas MAX handles seasonal micro-batches without sacrificing color accuracy. Demand for agile turnaround fuels sustained printhead orders, especially those rated for diverse viscosities and high-speed operation. As personalization expands within packaging, single-pass systems transform once-static production lines into flexible, data-driven assets. Because each unit uses multiple rows of piezo heads, the technology generates a steady pull-through for component suppliers.

MEMS nozzle arrays paired with thin-film actuators achieve sub-2 picoliter droplets at line speeds of 300 m/min, unlocking precision tasks such as pharmaceutical coatings and fine-line circuitry. Xaar's 2024 patent series details independent drive electronics for each nozzle that modulate volume on the fly. Kyocera's KJ4 platform commercialized the concept with 600 nozzles/inch and variable drops from 1.5 to 42 pL, enabling both graphics and functional deposition. The advance reduces ink waste and lowers operating costs because smaller drops translate into less pigment usage per square meter. Over the long term, these heads underpin bioprinting and smart-packaging initiatives where accuracy outranks raw speed.

Advanced inkjet lines cost 40-60% more than laser coders or flexo presses with similar throughput. Small manufacturers in price-sensitive regions delay upgrades despite lower setup and plate costs over the long haul. Financing programs offered by OEMs soften initial barriers, yet ROI calculations still favor legacy kit for mono-color marking or ultra-high-volume SKUs. Currency volatility in emerging economies reinforces the hesitation, slightly tempering the inkjet printhead market growth pace.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Drop-on-Demand accounted for 67.98% of the inkjet printhead market share in 2025, far outpacing continuous-flow systems. Piezo-based variants supply industrial sites that require sub-2 pL accuracy without thermal stress, while thermal cartridges hold ground in cost-sensitive office devices. The segment is forecast to post a 5.17% CAGR, reflecting continuous material science refinements rather than unit-growth spikes. Continuous technology retains coding niches where uninterrupted streams enable top speeds, but precision shortfalls curb its broader penetration.

Thin-film actuators cut power draw and raise native resolution to 1,200 dpi, giving Drop-on-Demand an advantage in high-density graphics and functional printing. Ricoh's MH5421F ships with multi-drop waveforms that lay down 4-42 pL volumes on demand, serving both signage and PCB substrates. As single-pass lines spread across corrugated and textile plants, each machine integrates hundreds of nozzles, embedding a substantial replacement-spares annuity into the inkjet printhead market size.

Aqueous inks commanded 31.76% revenue in 2025, buoyed by regulatory incentives and stronger pigment-encapsulation chemistries. UV-curables trail but are set to log a 5.72% CAGR to 2031, lifted by LED curing that bonds instantly to plastics and metals without high-heat exposure. Solvent fluids persist in outdoor banners where weathering resistance overrides environmental trade-offs, and latex blends serve high-stretch textiles that need elasticity.

Bio-based formulations occupy a rising niche as brand owners target circular-economy metrics. INX's plant-derived portfolio shows that sustainable inputs no longer compromise gamut or durability. UV heads, meanwhile, penetrate folding carton lines because instant cure accelerates lamination steps, trimming total turnaround.

The Inkjet Printhead Market Report is Segmented by Technology Type (Drop-On-Demand, and Continuous), Ink Type (Aqueous, Solvent-Based, UV-Curable, and More), Application (Packaging and Labeling, Textile Printing, and More), End-User (Office and Consumer-Based, Industrial Printing, Graphic Printing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America maintained 39.70% of 2025 revenue on the strength of entrenched R&D ecosystems and swift uptake of predictive-maintenance platforms. Federal environmental rules that restrict solvent discharge spur investment in water-based upgrades, and a mature e-commerce backbone secures demand for serialized, scannable packaging.

Asia-Pacific is expected to post a 6.43% CAGR, propelled by Chinese smart-factory programs and Japanese actuator know-how. Epson's new Chinese assembly hubs shorten lead times and hedge currency swings, whereas Mimaki's TS200 aims at Southeast Asian polyester mills with sublimation heads attuned to high-stretch fabrics. Regional cost advantages attract OEM outsourcing, intensifying local component clusters for ceramics and MEMS chips integral to inkjet jets.

Europe remains technology-rich but growth-mature as replacement buying overtakes greenfield installations. REACH regulations accelerate switchover to low-VOC fluids, and Koenig and Bauer Durst deploys carton presses that justify high cap-ex via premium short-run jobs. Government incentives for circular packaging underpin steady head retrofits across food and pharma converters.