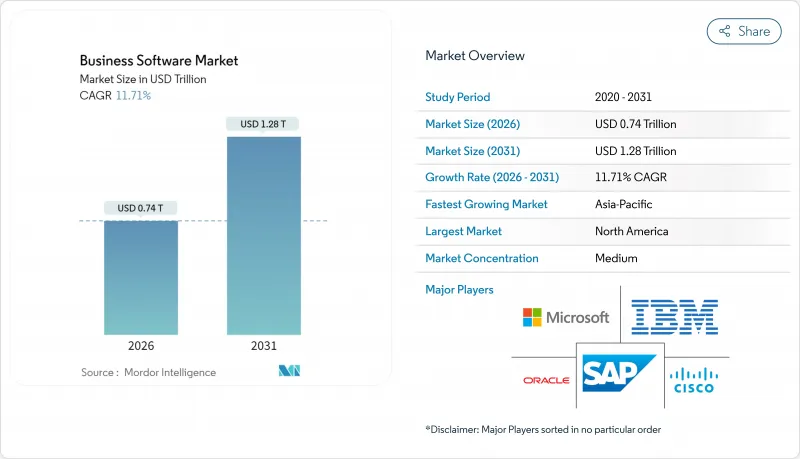

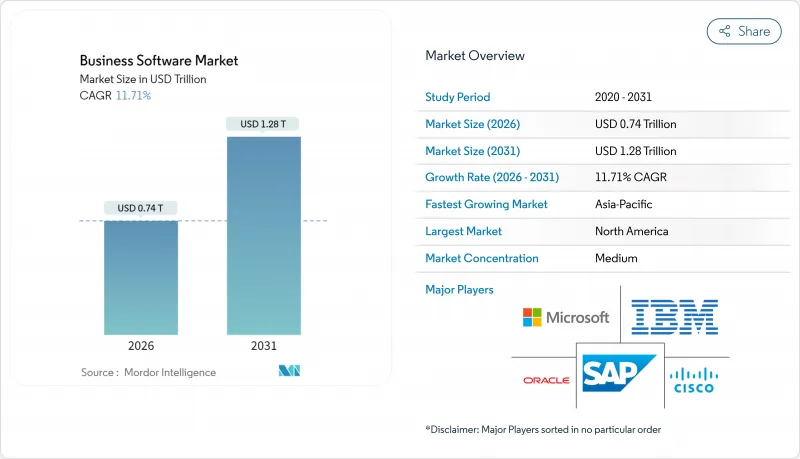

비즈니스 소프트웨어 시장 규모는 2026년 7,373억 달러로 추정되고, 2025년 6,600억 달러에서 성장했으며, 2031년에는 1조 2,817억 달러에 이를 것으로 예측됩니다. 2026-2031년 연평균 복합 성장률(CAGR)은 11.71%로 성장할 전망입니다.

이 급속한 확대는 기업이 AI를 활용한 워크플로우 자동화, 클라우드 네이티브 도입, 분석 기능을 업무 프로세스에 직접 통합하는 데이터 중심 아키텍처로 전환하고 있음을 반영합니다. 감사가능한 ESG 보고에 대한 기업 수요, 강인한 지역 공급망 재구축의 필요성, 로우코드 개발 플랫폼의 주류화가 각각 새로운 지출 흐름을 촉진하고 있습니다. 기존 플랫폼 공급업체가 AI 네이티브 신흥 기업 및 총소유비용(TCO)이 낮은 오픈소스 제품군과 경쟁하면서 경쟁압력이 커지고 있습니다. 구독 가격 모델은 지속적인 수익을 확대하는 반면, 고객 획득 비용을 증가시키고 있으며, 공급업체는 가치 기반 패키징 및 클라우드 비용 최적화 서비스의 정교화를 강요하고 있습니다. 지역별 성장 궤적은 분기하고 있습니다. 북미의 구매 담당자는 AI 통합에 주력하고, 아시아태평양의 조직은 클라우드 퍼스트 도입을 추구하며, 유럽 기업은 GDPR(EU 개인정보보호규정) 및 새로운 데이터 현지화 의무에 대응하기 위해 주권 준수 솔루션을 요구하고 있습니다.

지능형 자동화 도구의 도입은 규칙 기반 봇을 훨씬 뛰어넘고 AI 에이전트가 ERP, CRM, 협업 제품군을 가로질러 작업을 조정하는 단계로 전환하고 있습니다. Microsoft는 Office와 Dynamics에 Copilot 에이전트를 통합하고 엔드 투 엔드 워크플로를 재구성하는 자연어 프롬프트를 구현했습니다. 시티즌스 은행은 AI 코드 생성 어시스턴트 도입 후 소프트웨어 엔지니어링 부문에서 20%의 생산성 향상을 달성했습니다. 더욱 광범위한 업계 횡단 조사에서는 기능적인 생산성이 30-55% 향상된 것으로 보고되었습니다. 공급업체 각 회사는 통합 패브릭의 컨텍스트 데이터를 통합하므로 자동화는 순수한 작업 속도가 아닌 의사 결정의 품질을 향상시킵니다. 선행 도입 기업은 방어 가능한 우위성을 확보하는 한편, 후발 기업은 적응형 지능이 부족한 레거시 스크립팅 툴에 고전하고 있습니다.

2025년까지 미국 기업의 절반 이상이 기간 소프트웨어를 SaaS를 통해 운영하고 1,000억 달러를 넘는 새로운 B2B 기회를 창출했습니다. 이 전환은 공급업체의 수익을 고객 가치와 연동시키지만 고객 이반 관리 및 사용량 기반 계약의 중요성을 높입니다. 베트남의 조사에 따르면, 종량 과금제가 현금 흐름 제약을 완화하기 때문에 중소기업의 대기업을 웃도는 도입률을 나타냈습니다. 벤더는 과금 엔진에 AI를 짜넣어 계층의 개별화 및 소비 동향의 가시화를 진행하고 있지만, 기업측에서는 동시에 FinOps 수법을 채용해, 과잉 라이선스를 삭감하고 있습니다. 비용 시각화가 진행되는 동안 공급자의 차별화는 측정 가능한 ROI에 따라 달라지며, 보다 정교한 제품 로드맵과 판매 후 성공 프로그램이 요구되고 있습니다.

경제적 불확실성으로 클라우드 인보이스의 조사가 가속화되고 기업은 인스턴스의 적정 규모화 및 할당 해제 자동화를 실현하는 AI 탑재 비용 거버넌스 툴의 도입을 진행하고 있습니다. 인텔은 지속적인 최적화 프레임워크 도입 이후 전 세계 고객이 34%의 비용 절감을 달성했다고 보고했습니다. FinOps 팀은 이러한 인사이트를 조달 주기에 통합하여 공급업체 라이선스의 확장을 억제하고 업데이트 협상을 장기화하고 있습니다. 소프트웨어 제공업체는 지갑 공유를 유지하기 때문에 기능적 이점 외에도 효율성 향상을 정량화해야 합니다.

ERP 솔루션은 2025년 수익의 25.74%를 차지했으며, 비즈니스 소프트웨어 시장에서 핵심 업무의 핵심 역할을 강조했습니다. 대규모 제조업, 소매업, 공공기관은 통합된 재무, 조달 및 생산 모듈에 의존하고 프로세스 규율을 유지하고 있습니다. 그러나 기업이 데이터 중심의 의사 결정 주기를 선호하는 동안 애널리틱스 플랫폼은 2031년까지 12.05%의 연평균 복합 성장률(CAGR)을 기록했습니다. 베이커리 체인의 St-Donat사는 35만 달러의 예산으로 로트 추적 기능과 모바일 주문 접수를 실현하는 식품 특화형 클라우드 ERP를 도입하여 기존의 회계 도구를 대체했습니다. 병행하여 셀프서비스 BI 스위트는 고급 시각화와 예측 모델링을 민주화하고 성숙한 ERP 제품군에서 성장세를 빼앗고 있습니다.

이 분석 기술의 파도는 경영진이 요구하는 예측 포커스팅, 자동화된 데이터 스토리텔링, 임베디드 AI 추천의 추진과 시기를 동일하게 하고 있습니다. 각 공급업체는 ERP 워크벤치에 실시간 대시보드를 통합하면서도 전문 제공업체는 임상시험 성능 및 옴니채널 마케팅 기여와 같은 수직 KPI에 초점을 맞추어 보다 신속한 규모 확장을 실현하고 있습니다. 컴플라이언스 요구 사항이 확대되면서 감사 범위가 넓어짐에 따라 재무, 인사 및 프로젝트 포트폴리오 모듈은 안정적인 수요를 유지하고 ESG 보고 도구는 '기타' 범주 내에서 상승하고 있습니다. UL Solutions와 Worker는 각각 공급망 전체의 배출 데이터를 포착하는 탄소 회계 엔진을 번들로 제공하며, 이는 보다 광범위한 지속가능성으로의 전환을 반영합니다.

클라우드 도입은 2025년 비즈니스 소프트웨어 시장 규모의 59.12%를 차지했으며, 13.45%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 기업의 95%가 최소한 하나의 미션 크리티컬 워크로드를 퍼블릭 또는 하이브리드 클라우드로 마이그레이션하여 탄력적인 확장성 및 빠른 기능 제공 사이클을 추구하고 있습니다. Microsoft와 Oracle은 멀티클라우드 인터커넥트를 새로운 세계 지역으로 확장하여 고객이 재설계 없이 데이터베이스를 분석 엔진 근처에 배치할 수 있도록 했습니다. 아시아태평양에서는 5G 전개와 정부 지원 데이터센터 계획을 통해 마이그레이션 일정이 더욱 단축되었습니다.

주권과 지연이 우려되는 금융, 방위, 의료 분야에서는 온프레미스 도입이 여전히 계속되고 있습니다. 공급업체 각 회사는 현재 자체 스택의 컨테이너화된 버전을 제공하고 있으며 고객은 라이선스 및 지원 권한을 유지하면서 프라이빗 클러스터와 퍼블릭 클라우드 간에 워크로드를 이동할 수 있습니다. 소블린 클라우드 서비스를 통해 유럽 은행은 규제 대상 데이터를 국내에 호스팅할 수 있어 컴플라이언스 및 클라우드의 경제성을 양립하고 있습니다. 물류 및 제조업 고객을 위해 공장 현장에서 밀리초 미만의 응답성과 분석을 위한 중앙 통제를 양립시키는 엣지 컴퓨팅 설계도가 등장하고 있습니다.

비즈니스 소프트웨어 시장은 소프트웨어 유형별(ERP, CRM, 비즈니스 인텔리전스 및 애널리틱스 등), 전개 모드별(클라우드, 온프레미스), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 의료, 생명 과학, 정부 및 공공 부문 등), 조직 규모별(대기업, 중소기업) 및 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 성숙한 클라우드 인프라와 엄격한 업계 규제에 힘입어 2025년 비즈니스 소프트웨어 시장 수익의 25.05%를 차지했습니다. Microsoft는 2025년 167억 5,000만 달러의 설비 투자를 실시하여 미국의 AI 교육 용량에 대한 수요 증가에 대응했습니다. 캐나다 은행은 주권 준수 SaaS를 도입하고 멕시코 제조업체는 니어 쇼어링 업무 흐름 최적화를 위해 공장 현장의 디지털화를 추진하고 있습니다. 이 지역의 초점은 기본적인 클라우드 마이그레이션에서 AI를 활용한 생산성 향상으로 이행해 기존의 라이선스 갱신 비용을 넘은 잠재적인 지출 확대가 전망됩니다.

아시아태평양은 가장 성장이 빠른 지역으로 2031년까지 연평균 복합 성장률(CAGR) 12.52%로 확대될 전망입니다. 중국에서는 정부 주도의 디지털 경제 구상에 기업용 소프트웨어가 통합되어 현지 벤더는 국내 클라우드 정책에 적합합니다. 일본은 인구구조 변화에 따른 압력을 상쇄하기 위해 노동력 생산성 플랫폼을 추구하고 있습니다. 한편 인도에서는 급성장하는 중소기업 부문이 로우코드 스위트를 활용해 업무의 형식화를 진행하고 있습니다. 싱가포르와 홍콩은 지역 클라우드 허브 역할을 하며 동남아시아의 전자상거래 사업자에게 지연에 민감한 서비스를 제공합니다.

Business software market size in 2026 is estimated at USD 737.3 billion, growing from 2025 value of USD 660 billion with 2031 projections showing USD 1,281.7 billion, growing at 11.71% CAGR over 2026-2031.

This rapid expansion reflects enterprises' pivot toward AI-enabled workflow automation, cloud-native deployment, and data-centric architectures that embed analytics directly into operational processes. Corporate demands for auditable ESG reporting, the need to rebuild resilient regional supply chains, and the mainstreaming of low-code development platforms each fuel fresh spending streams. Competitive pressure intensifies as incumbent platform vendors contend with AI-native challengers and open-source suites that offer lower total cost of ownership. Subscription pricing models deepen recurring revenue yet elevate customer acquisition costs, prompting vendors to refine value-based packaging and cloud cost-optimization services. Regional growth trajectories diverge: North American buyers focus on AI integration, Asia-Pacific organizations pursue cloud-first adoption, and European firms seek sovereignty-compliant offerings to meet GDPR and emerging data-localization mandates.

Adoption of intelligent automation tools has moved far beyond rule-based bots as AI agents orchestrate tasks across ERP, CRM, and collaboration suites. Microsoft embedded Copilot agents across Office and Dynamics, enabling natural-language prompts that restructure end-to-end workflows.Citizens Bank realized 20% productivity gains in software engineering after deploying AI code-generation assistants, while broader cross-industry studies cite functional productivity lifts of 30-55%. Vendors integrate contextual data from unified fabrics, so automation now drives decision quality rather than pure task speed. Early adopters secure defensible advantages as laggards struggle with legacy scripting tools lacking adaptive intelligence.

More than half of U.S. enterprises will run core software via SaaS by 2025, unlocking over USD 100 billion in fresh B2B opportunity. The move aligns vendor income with customer value, yet raises stakes for churn management and usage-based contracting. Vietnamese research shows SME adoption outpacing large enterprises because pay-as-you-go pricing eases cash-flow constraints. Vendors embed AI in billing engines to personalize tiers and surface consumption insights, but enterprises simultaneously adopt FinOps practices to trim redundant seats. As cost visibility grows, provider differentiation hinges on measurable ROI, forcing sharper product road-mapping and post-sale success programs.

Economic uncertainty accelerates scrutiny of cloud invoices, prompting enterprises to deploy AI-powered cost-governance tools that right-size instances and automate de-allocation. Intel documented 34% savings for a global client after implementing continuous optimization frameworks. FinOps teams integrate these insights into procurement cycles, dampening vendor-license expansion and stretching renewal negotiations. Software providers must now quantify efficiency gains alongside functional benefits to retain wallet share.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

ERP solutions accounted for 25.74% of 2025 revenue, underscoring their role as the transactional backbone of the business software market. Large manufacturers, retailers, and public agencies rely on integrated finance, procurement, and production modules to maintain process discipline. Still, analytics platforms record a 12.05% CAGR through 2031 as companies prioritize data-driven decision cycles. Bakery chain St-Donat replaced legacy accounting tools with a food-specific cloud ERP that delivered lot traceability and mobile order capture on a USD 350,000 budget. In parallel, self-service BI suites democratize advanced visualization and predictive modeling, siphoning growth momentum from mature ERP lines.

The analytics wave coincides with executives' push for predictive forecasting, automated data storytelling, and embedded AI recommendations. Vendors embed real-time dashboards into ERP workbenches, yet specialist providers scale faster by focusing on vertical KPIs such as clinical-trial performance or omnichannel marketing attribution. Finance, HR, and project-portfolio modules keep steady demand as compliance mandates expand audit scope, while ESG reporting tools emerge inside the "other" category. UL Solutions and Workiva each bundle carbon-accounting engines that capture emissions data across supply networks, reflecting the broader sustainability pivot.

Cloud deployments captured 59.12% of the business software market size in 2025 and are set to climb at a 13.45% CAGR. Ninety-five percent of enterprises have shifted at least one mission-critical workload to public or hybrid clouds, pursuing elastic scalability and faster feature cadence. Microsoft and Oracle extended their multi-cloud interconnect to new global regions, enabling customers to place databases near analytic engines without re-architecture. In APAC, 5G rollouts and state-backed datacenter programs compress migration timelines further.

On-premise installations persist in finance, defense, and healthcare where sovereignty or latency concerns prevail. Vendors now ship containerized versions of their stacks so clients can move workloads between private clusters and public clouds while preserving licensing and support entitlements. Sovereign-cloud services allow European banks to host regulated data inside national borders, blending compliance with cloud economics. Edge-computing blueprints emerge for logistics and manufacturing clients that require sub-millisecond response at plant sites yet central governance for analytics.

Business Software Market is Segmented by Software Type (ERP, CRM, Business Intelligence and Analytics, and More), Deployment (Cloud, On-Premises), End-User Industry (BFSI, Healthcare and Life Sciences, Government and Public Sector, and More), Organization Size (Large Enterprises, Smes), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 25.05% of 2025 revenue in the business software market, supported by mature cloud infrastructure and stringent sectoral regulations. Microsoft invested USD 16.75 billion in 2025 capital expenditures to keep pace with rising U.S. demand for AI training capacity. Canadian banks deploy sovereignty-compliant SaaS, while Mexican manufacturers digitize shop-floors to optimize near-shoring workflows. The region's focus shifts from basic cloud migration to AI-infused productivity, expanding addressable spending beyond traditional license uplift.

Asia-Pacific is the fastest-growing geography, advancing at a 12.52% CAGR through 2031. China embeds enterprise software into government-led digital-economy initiatives, and local vendors harmonize with domestic cloud policies. Japan pursues workforce-productivity platforms to offset demographic pressures, whereas India's booming SME segment harnesses low-code suites to formalize operations. Singapore and Hong Kong anchor regional cloud hubs, supplying latency-sensitive services to Southeast Asian e-commerce merchants.