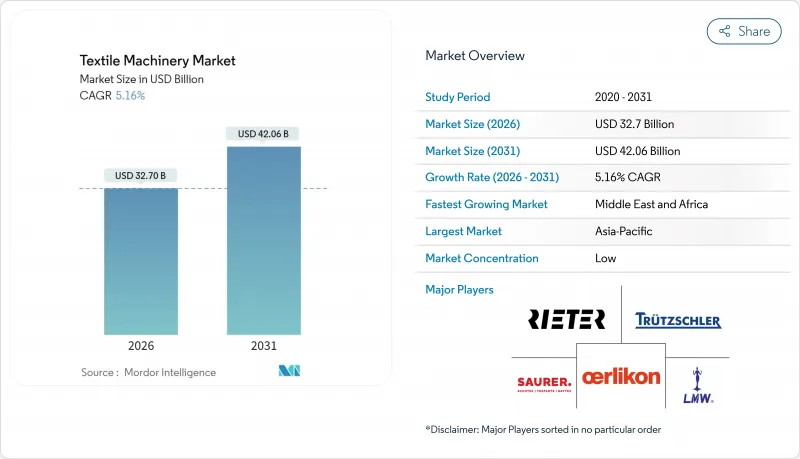

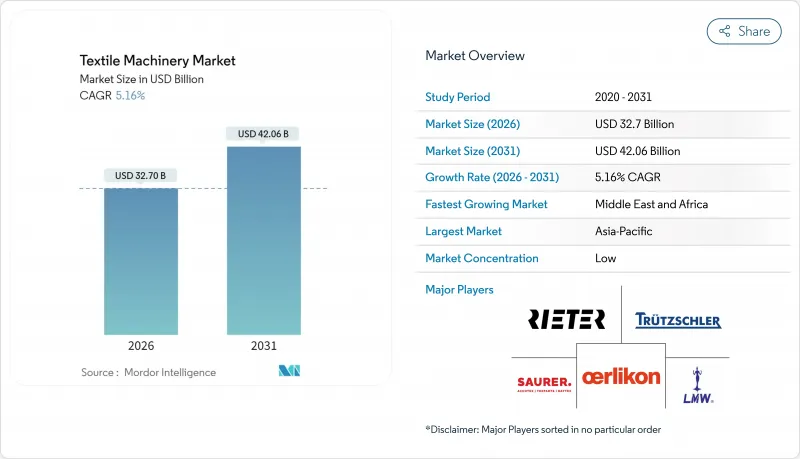

세계의 섬유 기계 시장은 2025년에 311억 달러로 평가되었고, 2026년 327억 달러에서 2031년까지 420억 6,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 5.16%를 나타낼 전망입니다.

공장 투자는 숙련 노동력 부족을 해소하고 가동률을 높이는 인더스트리 4.0 도구를 중심으로 점점 더 집중되고 있습니다. 스마트 센서, 클라우드 분석, AI 기반 결함 감지 기술이 기계 업그레이드를 촉진하는 한편, 재활용 의무화로 자동 분류 및 섬유-섬유 시스템 주문이 증가하고 있습니다. 의료용, 보호용, 스포츠 용품 부문의 기술 섬유 수요는 기존 의류 시장을 계속해서 앞지르며 새로운 수익원을 창출하고 있습니다. 비용 효율적인 합성 섬유와 바이오 기반 대체재 모두 기계 판매를 끌어올리며, 미주 지역의 관세 유발 근거리 생산(nearshoring)은 유연하고 소량 생산이 가능한 생산 라인 주문 증가를 가속화하고 있습니다.

제조업 구매관리자지수(PMI)는 2025년 4월 섬유 공장의 확장세를 보여주었으며, 운영자들은 만성적인 노동력 부족을 상쇄하기 위해 로봇 공학과 AI를 활용하고 있습니다. 미국 생산자들은 패턴 복잡성을 최적화하고 폐기물을 줄이는 지능형 편직 소프트웨어를 도입했습니다. IoT 플랫폼을 통해 관리자는 파키스탄 공장 시험에서 입증된 바와 같이 습도와 에너지를 실시간으로 추적할 수 있습니다. 컨볼루션 모델 기반 AI 비전 시스템은 결함 감지 정확도를 90% 후반대로 끌어올려 재작업량을 감소시킵니다. 처리량 증가와 폐기물 감소의 누적 효과로 자동화 라인은 선택적 투자가 아닌 전략적 투자가 되었습니다.

인도의 면사 생산자들은 중국 수요 회복과 현지 소매 시장 확대로 2025 회계연도에 7-9% 매출 성장을 전망합니다. 유리한 원사 스프레드와 개선된 면화 공급이 공장 업그레이드를 뒷받침합니다. 아세안과 아프리카 전역의 인구 구조적 호재는 방적 및 편직 라인에 대한 신규 설비 수요를 창출합니다. 관세가 기존 공급망을 불안정하게 하지만, 개발도상국 브랜드들은 여전히 규모를 필요로 하여 비용 효율적이면서도 현대적인 기계에 대한 균형 잡힌 투자를 촉진합니다. 공급업체에게는 유연한 금융 지원과 모듈식 업그레이드가 여전히 핵심 판매 포인트입니다.

완전한 방적 또는 직조 라인은 1천만 달러를 초과할 수 있어 중형 방적공장에는 장벽입니다. 대형 공급업체조차 기술 주기 단축으로 인해 신중하게 투자수익률(ROI)을 모델링합니다. 오늘날 최첨단 링방적기는 상각 전에 노후화될 위험이 있습니다. 이탈리아 OEM 업체들은 거시경제 불확실성으로 예산이 동결된 2023년 주문량이 16% 감소했습니다. 환율 변동은 남아시아와 아프리카에서 수입 기계 가격을 더욱 부풀립니다. 공급업체들은 비용 분산과 기술적 종속 제한을 위한 트레이드인 프로그램, 금융 패키지, 모듈형 추가 기계를 통해 대응하고 있습니다.

2025년 방적 기계는 섬유 기계 시장 점유율의 44.02%를 차지하며, 원사 변환에서 핵심적인 역할을 강조했습니다. 전 세계 단섬유 스핀들 설치 용량은 2억 3,200만 대에 달했으며, 방적공장들이 고속화 및 파손률 감소를 추구함에 따라 교체 수요는 안정적으로 유지되고 있습니다. 리터(Rieter)의 드로프레임 특허 획득과 트루츠슐러(Trutzschler)의 생산량 50% 증대형 12헤드 코머는 OEM 업체들이 혁신을 통해 마진을 방어하는 방식을 보여줍니다. 직기 및 편직기는 핵심 기둥으로 뒤를 잇지만, 재활용 분쇄기, 디지털 프린터, 바이오 섬유 압출기에 비해 성장 속도가 더딘 편입니다.

기타 기계 카테고리는 규모는 작지만 2031년까지 연평균 6.66% 성장률을 기록할 전망입니다. 투자자들은 면과 폴리에스터를 분리하거나 혼방 직물을 화학적으로 분해하는 재활용 라인을 선호합니다. 자동차 복합재용 현무암 또는 아라미드 섬유를 직조하는 특수 직기도 주목받고 있습니다. 의류 생산 주기가 단축되면서, 단일 디자인을 제공하는 직물 직접 인쇄기(DTOG)는 섬유와 디지털 영역을 아우르는 기계 공급업체에게 새로운 수익원을 창출합니다. 기계 포트폴리오 확대는 공급업체가 일반 원사 시스템에만 의존하지 않고 다양한 현금 흐름을 추구할 수 있는 기반을 마련합니다.

2025년 기준 반자동 플랫폼이 섬유 기계 시장 규모의 43.05%를 차지하며 선두를 달렸는데, 이는 인건비와 자동화 가격 사이의 균형을 반영합니다. 이 라인은 여전히 도핑(도핑 : 직물에서 실을 제거하는 작업)과 품질 검사를 위한 작업자가 필요하지만, 장력 및 속도 제어를 위한 센서가 통합되어 있습니다. 완전 자동화 운영으로 가는 길은 명확합니다. 데이터 연결성과 AI 비전은 추가 하드웨어만 필요로 하지만 가동 시간을 기하급수적으로 향상시킵니다.

완전 자동화로 인더스트리 4.0 대응 시스템은 2031년까지 연평균 6.78%의 성장률을 보일 것으로 예상됩니다. 방적 공장들은 기술자 채용 불가 문제를 대출 자금 조달보다 더 큰 제약으로 꼽으며, 무인 생산 현장으로의 전환을 가속화하고 있습니다. IoT 대시보드는 예측 유지보수를 가능케 하여 계획되지 않은 가동 중단 시간을 대폭 줄입니다. 수동 기계는 저임금 지역에서 여전히 사용되지만, 임금 인플레이션으로 인한 비용 격차 축소로 점유율이 지속적으로 하락하고 있습니다. 공급업체들은 로봇 도퍼와 같은 모듈형 업그레이드를 통해 전체 라인을 폐기하지 않고도 단계적으로 전환할 수 있도록 지원합니다.

아시아태평양 지역은 중국의 대규모 설치 기반과 인도 7개 공원 PM MITRA 계획(5억 3,500만 달러 규모)을 바탕으로 2025년 섬유 기계 시장 수요의 55.10%를 유지했습니다. 2차 중국 방적 공장들은 노동 의존도 감소를 위해 여전히 현대화를 추진 중이며, 인도 산업단지는 방적부터 후가공까지 아우르는 기계 패키지를 촉진하는 클러스터 시너지와 공유 유틸리티를 약속합니다. 중국 연안 지역의 임금 상승은 내륙 이전을 촉진하여 국내 업그레이드 주기를 단축하기보다 오히려 연장시키고 있습니다.

중동 및 아프리카는 무역 다각화로 이집트, 모로코, 에티오피아로의 주문이 증가함에 따라 2031년까지 가장 빠른 6.31% CAGR을 기록할 것으로 전망됩니다. 걸프 투자자들은 저비용 에너지 연계 통합 폴리에스터 공장에 자금을 지원하며, 이는 다운스트림 텍스처링 및 워프 니팅 라인을 필요로 합니다. 아프리카 방적공장은 AGOA(아프리카 성장기회법) 및 EU 무역 특혜를 활용해 관세 타격을 입은 아시아에서 이전된 의류 계약을 확보합니다. 기계 공급업체들은 현지 대학과 협력해 기술 프로그램을 운영하며, 도입을 저해할 수 있는 작업자 부족 문제를 완화합니다.

북미에서는 USMCA(미국 및 멕시코 및 캐나다 협정)의 규칙에 의해 멕시코 및 캐나다의 실 및 천이 보호되고, 미국 국경 부근에서 새로운 링 방적 및 에어 제트 직기 프로젝트가 추진되고 있습니다. 브랜드 기업은 관세 및 운송비 및 재고 리스크를 고려한 경우 10일간공급망 리드타임이 아시아와의 비용차이를 상쇄한다고 추정하고 있습니다. 유럽은 부가가치가 높은 부문, 즉 테크니컬 패브릭, 리사이클, 고급 울에 주력해 에너지 및 인건비를 상쇄하는 자동화 기술이 기반이 되고 있습니다. 튀르키예와 독일은 인근 지역에 고기능 직기를 수출함과 동시에 EU 에코 디자인 규제에 준거한 개조 공사에 의한 서비스 수익을 획득하고 있습니다.

The Global Textile Machinery Market was valued at USD 31.10 billion in 2025 and estimated to grow from USD 32.7 billion in 2026 to reach USD 42.06 billion by 2031, at a CAGR of 5.16% during the forecast period (2026-2031).

Factory investments increasingly revolve around Industry 4.0 tools that counter skilled-labor shortages and raise uptime. Smart sensors, cloud analytics, and AI-driven defect detection push equipment upgrades, while recycling mandates spur orders for automated sorting and fiber-to-fiber systems. Technical-textile demand in medical, protective, and sporting goods continues to outpace traditional apparel, opening fresh profit pools. Cost-efficient synthetic fibers and bio-based alternatives both lift machinery sales, and tariff-induced near-shoring in the Americas accelerates orders for flexible, low-lot production lines.

Manufacturing PMI readings showed textile mills expanding in April 2025, and operators now use robotics and AI to offset chronic labor gaps. U.S. producers adopted intelligent knitting software that optimizes pattern complexity and cuts scrap. IoT platforms let managers track humidity and energy in real time, as documented in Pakistan's mill trials. AI vision systems based on convolutional models push defect-detection accuracy into the high-90% range, reducing rework. The cumulative gains in throughput and waste reduction make automated lines a strategic rather than an optional investment.

India's cotton-yarn producers expect 7-9% revenue growth in fiscal 2025 as Chinese demand rebounds and local retail expands. Favorable yarn spreads and improved cotton availability underpin mill upgrades. Demographic tailwinds across ASEAN and Africa add fresh capacity requirements for spinning and knitting lines. While tariffs unsettle traditional supply chains, developing-market brands still need scale, prompting balanced investments in cost-efficient yet modern machinery. For suppliers, flexible financing and modular upgrades remain critical selling points.

Complete spinning or weaving lines can exceed USD 10 million, a hurdle for mid-size mills. Even large suppliers carefully model ROI because technology cycles shorten; a state-of-the-art ring-spinning frame today risks obsolescence before amortization. Italian OEMs saw orders dip 16% in 2023 when macro uncertainty froze budgets. Currency swings further inflate imported equipment in South Asia and Africa. Vendors respond with trade-in programs, financing packages, and modular add-ons that spread costs and limit technological lock-in.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Spinning equipment accounted for 44.02% of the textile machinery market share in 2025, underscoring its central role in yarn conversion. Global installed short-staple spindle capacity hit 232 million units, and replacement demand remains steady as mills chase higher speed and lower breakage. Rieter's draw-frame patent win and Trutzschler's 12-head comber that lifts output 50% illustrate how OEMs defend margins through innovation. Weaving and knitting machines follow as core pillars but face slower growth relative to recycling shredders, digital printers, and bio-fiber extruders.

Other machine categories, while smaller, are set to post a 6.66% CAGR to 2031. Investors favor recycling lines that separate cotton and polyester streams or dissolve blended fabrics chemically. Specialty looms that weave basalt or aramid for automotive composites also gain traction. As apparel cycles compress, direct-to-garment printers that deliver one-off designs create new revenue for machinery vendors willing to straddle textile and digital domains. The broadening equipment menu positions suppliers to chase diverse cash flows rather than rely solely on commodity yarn systems.

Semi-automatic platforms led with 43.05% of the textile machinery market size in 2025, reflecting the balance between labor costs and automation pricing. These lines still need operators for doffing and quality checks, but integrate sensors for tension and speed control. The pathway to fully automatic operations is clear; data connectivity and AI vision add only incremental hardware but deliver exponential uptime gains.

Fully automatic, Industry 4.0-ready systems are forecast to grow at a 6.78% CAGR through 2031. Mills cite the inability to recruit technicians as a bigger constraint than loan financing, tipping decisions toward lights-out production floors. IoT dashboards allow predictive maintenance that slashes unplanned downtime. Manual machines persist in low-wage clusters yet continuously lose share as wage inflation erodes the cost gap. Vendors market modular upgrades such as robotic doffers that let owners transition stepwise without scrapping entire lines.

The Textile Machinery Market Report is Segmented by Machine Type (Spinning Machines, Weaving Machines, and More), by Automation Type (Manual, Semi-Automatic and Fully Automatic), by Application (Garments & Apparels, Household and Home Textiles, and More), by Raw Material (Cotton, Synthetic Fibers, and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific retained 55.10% of 2025 demand for the textile machinery market, anchored by China's large installed base and India's seven-park PM MITRA scheme worth USD 535 million. Tier-2 Chinese mills still modernize to cut labor dependence, while Indian parks promise cluster synergies and shared utilities that spur equipment packages covering spinning to finishing. Rising wages in coastal China drive inland relocation, lengthening the domestic upgrade cycle rather than shrinking it.

The Middle East and Africa are projected to log the fastest 6.31% CAGR through 2031 as trade diversification sends orders to Egypt, Morocco, and Ethiopia. Gulf investors bankroll integrated polyester plants tied to low-cost energy, requiring downstream texturizing and warp-knitting lines. African mills leverage AGOA and EU trade preferences to secure apparel contracts shifted from tariff-hit Asia. Equipment suppliers partner with local universities on skill programs, mitigating operator shortages that could blunt adoption.

North America benefits from USMCA rules that shield Mexican and Canadian yarn and fabric, fueling new ring-spinning and air-jet weaving projects near the U.S. border. Brands calculate that a 10-day supply-chain lead beats the cost delta with Asia once tariffs, freight, and inventory risks are considered. Europe focuses on value-added segments technical fabrics, recycling, and luxury wool, underpinned by automation that offsets energy and labor costs. Turkey and Germany export high-spec looms to neighboring regions and capture service revenue from retrofits complying with EU eco-design regulations.