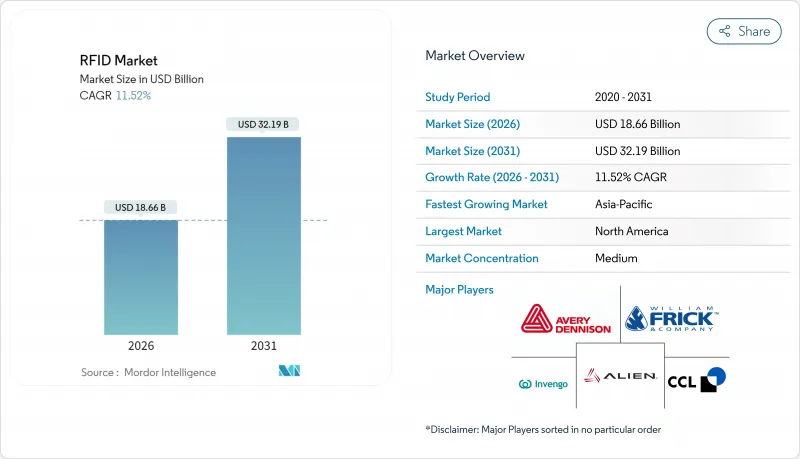

RFID 시장은 2025년에 167억 3,000만 달러로 평가되었으며, 2026년 186억 6,000만 달러에서 2031년까지 321억 9,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 11.52%로 예상됩니다.

현재의 성장 추세는 기술이 틈새 도구에서 옴니 채널 소매, 규제 의료, 정부 디지털 인프라 계획의 핵심 추진력으로 전환하고 있음을 반영합니다. UHF 인레이 가격이 0.04달러 미만인 수준에서 지속적으로 하락하면서 진입 장벽이 낮아졌으며, 개선된 Gen2v3 프로토콜은 혼잡한 환경에서 판독 신뢰성을 향상시키고 있습니다. FDA의 DSCSA와 인도의 FASTag 체계와 같은 정부 규정은 여전히 대규모 도입을 견인하고 있습니다. 동시에 클라우드 분석 플랫폼은 원시 태그 판독 데이터를 예측 유지보수 및 재고 계획 데이터로 변환하여 경영진의 신속한 의사결정에 활용하고 있습니다. 그 결과 RFID 시장은 고성장 부문으로의 침투를 추진하고 있으며, 태그 판독 소프트웨어 생태계에 대한 수년간의 투자 사이클을 강화하고 있습니다.

미국과 유럽연합(EU)의 의약품 관련 법규에 따라 유통업체는 엔드 투 엔드의 전자 추적 및 추적성 기능을 유지할 의무가 있습니다. RFID는 직렬화된 식별자, 만료 데이터 및 집계 코드를 단일 태그 내에 수용할 수 있는 능력으로 인해 높은 거래량 관리에서 2차원 바코드보다 우수함이 입증되었습니다. 프레제니우스사의 도입 사례는 임베디드 태그 데이터가 로트 수준의 회수를 자동화하고 환자 안전 점검을 강화하는 방법을 부각하고 있습니다. 컴플라이언스 기한이 다가오는 가운데 제약기업의 경영진은 RFID를 규제 대응 비용이 아닌 전략적 자산으로 간주하는 경향이 강해지고 있으며, 이는 RFID 시장의 장기적인 수요를 강화하고 있습니다.

선도적인 소매 기업은 의류에서 전자기기, 문구, 신선식품으로 RFID 요구사항을 확대하고 있습니다. Walmart의 최신 의무화와 Kroger의 베이커리 배포는 정확한 실시간 재고 시각화가 선반 재고율을 95% 이상으로 높여 품절을 최대 30% 절감하는 예를 보여줍니다. 셀프 계산의 가속화와 인건비 절감으로 매장 수익성이 향상됨에 따라 중견 소매업체에게도 RFID 도입의 매력이 높아지고 있습니다. 옴니채널 모델이 통일된 인벤토리 가시성을 추구하는 가운데 품목 수준의 태그는 RFID 시장의 단기 수익 기반이 될 전망입니다.

GDPR(EU 개인정보보호규정)과 유사한 법령은 개인 정보를 수집하는 RFID 프로젝트를 복잡화하는 데이터 최소화 원칙을 의무화합니다. 소매업체는 프라이버시 바이 디자인(설계 단계부터 프라이버시 보호)의 제어 기능을 통합하여 민감한 데이터를 백엔드 데이터베이스로 마이그레이션하고 옵트아웃 옵션을 제공해야 하며, 이는 로드맵에 법적 심사 주기를 추가합니다. 그 결과 컴플라이언스 대응 부담이 도입 결정을 늦추고 RFID 시장에서 단기적인 성장 전망을 축소하고 있습니다.

RFID 태그는 2025년에 88억 3,000만 달러의 매출을 창출했으며, 낮은 단가 및 유지보수가 없는 설계로 RFID 시장 전체의 52.78%를 차지했습니다. 0.04달러 이하의 UHF 인레이는 대량 생산형 소비재의 라벨링을 가능하게 하고, 의약품 직렬화는 고부가가치 태그 수요를 창출하고 있습니다. 리더와 인터로게이터는 출하 대수가 적지만, 기업이 멀티 프로토콜에 대응하는 클라우드 연결 디바이스를 도입함에 따라 평균 판매 가격이 높아지고 있습니다. RFID 안테나와 미들웨어는 원시 판독 데이터를 생산 데이터로 변환하는 통합 기반을 형성하고 단순 식별을 엔드 투 엔드 시각화로 승화시킵니다.

능동형 RFID와 RTLS 인프라는 데이터센터 및 병원 내 실시간 위치정보와 환경 모니터링에 대한 경영진의 우선순위를 반영하여 12.52%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 능동형 플랫폼은 RFID 시장에서 센서 번들 판매 및 소프트웨어 구독의 혜택으로 2031년까지 64억 5,000만 달러 이상에 달할 것으로 예측됩니다. 배터리 보조 수동형 태그는 하이브리드 위치를 차지하며 완전한 배터리 비용 없이 장거리 판독이 필요한 창고 자동화 부문에서 실용성을 확대하고 있습니다. 인쇄형 및 칩리스 형태는 여전히 시험 단계이지만, 롤-투-롤 제조의 기술 혁신은 보다 광범위한 RFID 시장 내에서 향후 가격 파괴를 초래할 수 있습니다.

2025년 매출에서 UHF 대역은 40.72%를 차지하였고, 동대역은 RFID 시장에서 2031년까지 12.45%의 연평균 복합 성장률(CAGR)로 성장해 149억 달러를 돌파할 전망입니다. 소매 재고 관리 사이클에서는 고속 및 다품목 판독에 UHF가 적합하고, 직렬화 프로그램에서는 추가 데이터 용량이 높이 평가되고 있습니다. 최근의 Gen2v3 개선으로 태그 밀도가 높은 환경에서의 성능이 향상되어 혼합 재료 창고에서의 적용 범위가 넓어지고 있습니다.

고주파 및 NFC는 비접촉 결제나 가전기기의 페어링에 필수적이지만, 한 자릿수의 성장률은 많은 성숙 시장에서 이미 포화 상태에 도달했음을 나타내고 있습니다. 저주파 태그는 금속 투과성이 중요한 가축 관리 및 자동차 이모빌라이저에서 틈새 역할을 담당하고 있습니다. 마이크로파 대역의 도입은 고속도로 요금 징수와 산업 자동화의 요구를 충족하지만 비용면의 과제에 직면하고 있습니다. 각 공급업체는 현재 LF, HF, UHF 태그를 병렬로 읽을 수 있는 주파수 선택형 안테나에 대한 실험을 진행 중이며, 이 혁신 기술은 RFID 시장의 부문 경계를 모호하게 만들 수 있습니다.

RFID 시장은 기술별(RFID 태그, RFID 리더/인터로게이터, RFID 안테나, RFID 미들웨어와 소프트웨어, 능동형 RFID 및 RTLS 인프라), 주파수대별(저주파, 고주파 및 NFC, 초고주파, 마이크로파), 용도별(소매 및 의류, 의료, 기타), 최종 사용자 산업별(FMCG 및 CPG)로 나뉘며 시장 예측은 금액 기준(미국)으로 제공됩니다.

북미는 2025년 시점에서 37.15%의 점유율을 유지했으며, DSCSA(의약품 유통망 안전법)에 따른 소매 산업의 적극적인 도입 의무화, 대규모 데이터센터의 설치가 주요인입니다. 의료 제공업체는 자산의 과잉 보유 축소와 환자 처리 능력 향상을 위해 RTLS(실시간 위치 정보 시스템)의 도입을 가속화하고 있으며, 클라우드 사업자는 하이퍼스케일 캠퍼스 전체에서 태그를 활용한 모니터링을 확대하고 있습니다. 시책의 확실성과 성숙한 채널 파트너십은 RFID 도입에 대한 지속적인 자본 배분을 지원하며, 이 지역은 RFID 시장의 최전선에 위치하고 있습니다.

아시아태평양은 12.58%의 연평균 복합 성장률(CAGR)로 가장 강한 성장 궤도를 나타낼 전망입니다. 인도의 FASTag 프로그램에서만 지난 18개월간 6,000만 개 이상의 태그가 도입되어 국내 태그 조립 라인의 육성과 지역 BOM 비용의 감소를 촉진했습니다. 중국 OEM은 '중국 제조 2025' 구상하에 공장 현장의 MES 시스템에 RFID를 통합하고 있습니다. 동남아시아의 소매업체는 수작업 재고관리 기법을 비약적으로 개선하기 위해 이 기술을 도입하고 있습니다. 이러한 요인들이 함께 아시아태평양 전역에서 RFID 시장을 활성화하고 있습니다.

유럽에서는 EU의 위조 의약품 지침과 새로운 디지털 제품 여권 규제를 원동력으로 한 자릿수 후반의 높은 성장을 유지하고 있습니다. 프라이버시 규제로 소비자를 위한 도입은 둔화되고 있지만, 재활용 가능한 라벨과 안전한 클라우드 아키텍처에서 혁신을 촉진하고 있습니다. 중동 및 아프리카와 남미는 여전히 개발도상지역이지만 정부의 신분증 및 통행료 징수 프로젝트는 현지 RFID 시장 수요의 확대 전망을 시사하고 있습니다.

The RFID market was valued at USD 16.73 billion in 2025 and estimated to grow from USD 18.66 billion in 2026 to reach USD 32.19 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

The current upswing reflects the technology's shift from a niche tool into a core enabler of omnichannel retail, regulated healthcare, and government digital-infrastructure programs. Sustained reductions in UHF inlay pricing below USD 0.04 have lowered entry barriers, while improved Gen2v3 protocols enhance read reliability in crowded environments. Government mandates such as the FDA DSCSA and India's FASTag scheme continue to pull large-volume deployments. At the same time, cloud analytics platforms convert raw tag reads into predictive maintenance and inventory-planning data that executive teams use for faster decision making. As a result, the RFID market is on course to penetrate high-growth verticals, reinforcing a multi-year investment cycle in tags, readers, and software ecosystems.

Pharmaceutical legislation in the United States and European Union now obliges distributors to maintain end-to-end electronic track-and-trace capabilities. RFID's capacity to house serialized identifiers, expiration data, and aggregation codes inside a single tag has proved superior to 2D barcodes for managing high transaction volumes. Fresenius Kabi's deployment underscores how embedded tag data automates lot-level recalls and strengthens patient-safety checks. With compliance deadlines converging, pharmaceutical executives increasingly regard RFID as a strategic asset rather than a regulatory expense, reinforcing long-term demand in the RFID market.

Large retailers are widening RFID requirements from apparel into electronics, stationery, and perishables. Walmart's latest mandate and Kroger's bakery rollout illustrate how accurate, real-time stock visibility lifts on-shelf availability above 95% and reduces stockouts by up to 30%. Faster self-checkout and labor savings enhance store economics, making RFID adoption attractive even for mid-tier retailers. As omnichannel models demand unified inventory views, item-level tagging is set to anchor near-term revenue for the RFID market.

GDPR and analogous laws mandate data-minimization principles that complicate RFID projects capturing personal information. Retailers must embed privacy-by-design controls, shift sensitive data to back-end databases, and offer opt-out pathways, adding legal review cycles to implementation roadmaps. The resulting compliance overhead slows deployment decisions and trims near-term growth expectations within the RFID market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

RFID Tags delivered USD 8.83 billion in 2025 revenue, equating to a 52.78% slice of overall RFID market share thanks to their low unit cost and maintenance-free design. Sub-USD 0.04 UHF inlays unlock high-volume consumer-goods labeling, while pharmaceutical serialization adds defensible premium-tag demand. Readers and interrogators, though lower in shipment numbers, generate higher average-selling prices as enterprises adopt multi-protocol, cloud-connected devices. RFID Antennas and middleware form the integration fabric that converts raw reads into operational data, turning simple identification into end-to-end visibility.

Active RFID and RTLS infrastructure is projected to increase at a 12.52% CAGR, reflecting executive priority on real-time location and environmental monitoring inside data centers and hospitals. The RFID market size for active platforms is forecast to exceed USD 6.45 billion by 2031, benefiting from bundled sensor sales and software subscriptions. Battery-assisted passive tags occupy a hybrid position, expanding viability in warehouse automation where longer read ranges are required without full battery cost. Printed and chipless formats remain at pilot scale, yet breakthroughs in roll-to-roll manufacturing could unlock future price disruption inside the broader RFID market.

UHF captured 40.72% of 2025 revenue, with the RFID market size for this band on track to surpass USD 14.9 billion by 2031 amid a 12.45% CAGR. Retail inventory cycles favor UHF for fast, multi-item reads, while serialization programs value the added data capacity. Recent Gen2v3 improvements boost performance in tag-dense settings, expanding suitability for mixed-material warehouses.

High-Frequency/NFC remains indispensable for contactless payments and consumer-electronics pairing, though its single-digit growth reflects near-saturation in many mature markets. Low-Frequency tags hold niche roles in livestock management and automotive immobilizers where metal penetration is critical. Microwave deployments meet high-speed tolling and industrial automation needs but face cost hurdles. Vendors are now experimenting with frequency-selective antennas capable of reading LF, HF, and UHF tags in parallel, an innovation that could blur segment boundaries in the RFID market.

RFID Market is Segmented by Technology (RFID Tags, RFID Readers/Interrogators, RFID Antennas, RFID Middleware and Software, Active RFID/RTLS Infrastructure), Frequency Band (Low Frequency, High Frequency/NFC, Ultra-High Frequency, Microwave), Application (Retail and Apparel, Healthcare and Medical, and More), End-User Industry (FMCG and CPG, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 37.15% revenue share in 2025, anchored by DSCSA compliance, aggressive retail mandates, and large-scale data-center footprints. Healthcare providers accelerate RTLS rollouts to cut asset hoarding and enhance patient throughput, while cloud operators expand tag-enabled monitoring across hyperscale campuses. Policy certainty and mature channel partnerships support continued capital allocation toward RFID deployments, keeping the region at the forefront of the RFID market.

Asia Pacific delivers the strongest trajectory at a 12.58% CAGR. India's FASTag program alone introduced more than 60 million tags in the past 18 months, fostering domestic tag assembly lines and lowering regional BOM costs. Chinese OEMs integrate RFID into factory-floor MES systems under the Made-in-China 2025 framework, while Southeast Asian retailers adopt the technology to leapfrog manual inventory methods. These vectors combine to elevate the RFID market across Asia Pacific.

Europe sustains high-single-digit growth powered by the EU Falsified Medicines Directive and emerging Digital Product Passport legislation. Privacy regulation slows consumer-facing deployments but encourages innovation in recyclable labels and secure cloud architectures. Middle East & Africa and South America remain nascent, though government identity and toll projects signal future step-ups in local RFID market demand.