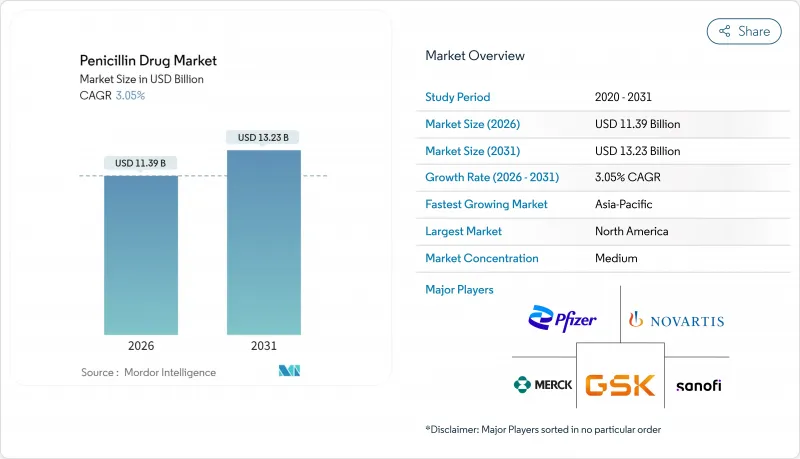

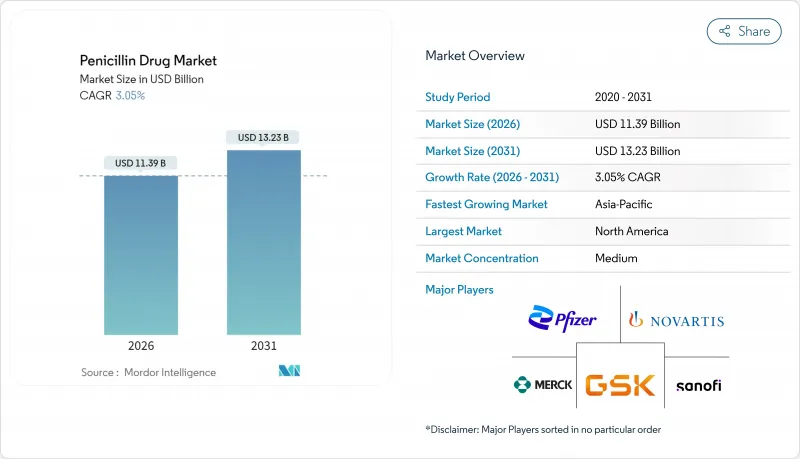

페니실린 의약품 시장은 2025년에 110억 5,000만 달러로 평가되었고, 2026년 113억 9,000만 달러에서 2031년까지 132억 3,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 3.05%를 나타낼 전망입니다.

이처럼 완만하지만 꾸준한 성장세는 페니실린이 기초 항생제로서 성숙기에 접어들었음을 반영하는 동시에, 베타-락타마제 억제제 혁신, 국내 원료의약품(API) 프로그램, 그리고 관리 중심의 좁은 스펙트럼 제제에 대한 수요 증가로 인해 창출된 새로운 기회를 시사합니다. 항생제 내성 그람양성균 감염 증가, 아시아태평양 지역의 발효 능력 부활, AI 기반 균주 공학은 경쟁 역학을 더욱 변화시키고 있습니다. 제조사들은 중국 API 집중도를 상쇄하기 위해 공급망을 현지화하고 있으며, 병원들은 1차 치료제 처방 목록 통제를 강화하고, 온라인 약국들은 점유율을 확대하고 있습니다. 이러한 요소들이 복합적으로 작용하여 광범위한 항생제 시장이 정체기에 접어들더라도 페니실린 시장이 탄력적인 성장 궤도를 유지할 것으로 예상됩니다.

전 세계 의료 시스템은 메티실린 내성 포도상구균(MRSA) 및 카르바페넴 내성 아시네토박터 균주의 급증에 직면하며, 표적 진단과 결합된 좁은 스펙트럼 페니실린에 대한 의존도가 재차 높아지고 있습니다. WHO는 여러 천연 페니실린을 “접근성” 제제로 분류하여, 내성 발달을 가속화하는 광범위 대체제보다 이를 우선 처방하도록 권장하고 있습니다. 감시 데이터에 따르면 분리균의 3분의 1에서 페니실린 내성을 보이는 Staphylococcus borealis가 확인되었으며, 이 결과는 병용 요법 연구를 촉진하고 적절히 관리될 경우 여전히 효과적인 기존 제제에 대한 수요를 강화하고 있습니다. 이에 병원들은 페니실린 감수성 검사 패널 사용을 확대하고 신속 분자 진단을 통합하여 처방을 정밀 조정하는 추세로, 이는 중기적으로 안정적인 처방량을 뒷받침할 것으로 예상됩니다.

제약 파이프라인에는 내성 균주에 대한 페니실린 효과를 회복시키는 베타-락타마제 억제제 복합제가 점차 증가하고 있습니다. 미국 FDA는 2023년 아시네토박터 감염 치료용 설박탐-듀르로박탐을 승인했으며, 이는 콜리스틴 대비 현저히 낮은 신독성을 입증했습니다. 메로페넴, 아비박탐, 차세대 금속-베타락타마제 차단제를 결합한 삼중 요법은 2상 임상에서 긍정적 결과를 보고하며 다제내성 사례에 대한 치료 옵션을 확대하고 있습니다. 기기 혁신도 눈에 띈다 : 2025년 4월 승인된 파이페라실린-타조박탐용 DUPLEX 용기는 병상 준비 시간을 단축하고 오염 사건을 억제합니다. 이러한 임상적 및 기술적 진전은 고급 반합성 페니실린의 프리미엄 가격 책정력을 유지시켜 페니실린 의약품 시장 성장에 실질적으로 기여할 전망입니다.

클레브시엘라 폐렴균 ST307과 같은 고위험 클론은 3세대 세팔로스포린에 대해 85% 이상, 카르바페넴에 대해 60% 이상의 내성을 보이며 베타락탐계 항생제의 효능을 직접 위협합니다. 카르바페넴 내성 아시네토박터는 WHO 목록에서 최우선 등급에 도달했으며, 페니실린과 고급 세팔로스포린 모두를 무력화시키는 교차 내성을 지닙니다. 치료 복잡성 증가는 병원 비용을 증가시키고 치료 옵션을 제한하며, 페니실린을 우회하는 예비 항생제 사용 증가를 부추겨 급성 치료 시장의 성장 동력을 전반적으로 약화시킵니다.

2025년 천연 페니실린은 페니실린 계열 항생제 시장 점유율의 53.10%를 차지하며 연쇄상구균 및 매독 감염에 대한 경험적 치료에서 지속적인 우위를 입증했습니다. 성숙한 발효 기술, 낮은 원가, 필수 의약품 목록 등재로 인해 견고한 기본 판매량이 유지되고 있습니다. 반합성 계열인 아미노페니실린, 가성그람음성균 치료제, 베타-락타마제 억제제 복합제는 증가하는 내성 패턴과 광범위한 치료 범위에 대한 병원 수요에 힘입어 연평균 6.35%의 성장률을 보이고 있습니다. 반합성 계열의 페니실린 시장 규모 확대는 설박탐-듀르로박탐과 같은 신규 승인 약물과 DUPLEX 즉시 사용 시스템 같은 제형 개선으로 더욱 가속화되고 있습니다.

경쟁 측면에서 반합성 파이프라인은 기존 천연물보다 높은 보험 적용 가격을 요구하는 추가적 스펙트럼 확장으로 인해 불균형적인 R&D 자금을 유치하고 있습니다. 인도의 생산연계인센티브(PLI) 프로그램은 발효 공정 대비 화학합성 경로에 10% 인센티브를 제공하여, 제조사들이 합성 원료의약품(API)으로만 전환하기보다 생물 기반 생산 능력 현대화를 유도하고 있습니다. 페니실리움 유전체 편집 기술의 돌파구는 천연 페니실린 생산량을 높일 수 있는 수율 개선을 약속하며, 저소득 국가 입찰 시장에서 핵심적인 경제적 매력도 유지할 수 있습니다.

경구 제제는 2025년 페니실린 의약품 시장 규모의 41.05%를 차지했으며, 외래 진료 모델, 소아 투여 편의성, 높은 환자 순응도에 힘입어 가장 빠른 5.85% CAGR로 성장하고 있습니다. 아목시실린-클라불란산 복합제는 광범위 항생제 옵션으로 흔한 호흡기 병원체를 표적화하며 여전히 세계의 최상위 처방약으로 자리매김하고 있습니다. 경구제 형태의 페니실린 의약품 시장 점유율 증가는 입원 비용 억제를 위한 조기 퇴원 및 가정 기반 치료를 장려하는 지불자 전략을 반영합니다.

중증 감염 및 수술 예방을 위한 비경구제 제제는 여전히 중요하지만, 투여 복잡성으로 인해 성장 속도가 더디게 나타납니다. 병원들은 페니실린 알레르기 표기 환자에서 세파졸린 및 천연 페니실린의 안전한 대체를 가능하게 하는 약사 주도 관리 프로토콜을 도입하고 있으며, 이는 본질적으로 비경구 수요를 확대하는 동시에 고가의 카르바페넴 의존도를 낮추고 있습니다. DUPLEX로 대표되는 기기 혁신은 조제 오류를 최소화하고 적시 조제를 지원하여 경구 제품과의 성장 격차를 다소 상쇄하고 있습니다.

북미는 정교한 보험급여 제도, 광범위한 감수성 검사, 강력한 항생제 관리 의무화 정책을 바탕으로 2025년 페니실린 의약품 시장 점유율 37.20%를 차지하며 가장 높은 지역 매출을 기록했습니다. 미국 병원들은 수술 건수에 힘입어 높은 1인당 소비량을 유지하는 반면, 캐나다의 보편적 보험 제도는 제네릭 좁은 스펙트럼 제제를 선호합니다. 멕시코와의 국경 간 무역은 가격에 민감한 부문에 공급하고 아시아에서 API 수입 위험을 완화하는 니어쇼어링 전략을 지원합니다.

유럽은 확고한 처방 체계와 항생제 현대화를 위한 국가 재정 지원을 바탕으로 그 뒤를 잇습니다. 산도즈의 오스트리아 생산 거점 2억 유로 규모 업그레이드는 대륙 내 공급을 확보하고 유럽 연합을 완제제 신흥 수출국으로 자리매김합니다. 유럽의약품청(EMA)의 통합 라벨링 추진은 좁은 스펙트럼 선택을 장려하여, 2030년까지 전체 항생제 사용량을 30% 감축하는 목표 속에서도 사용량 안정성을 유지합니다.

아시아태평양 지역은 5.05%의 연평균 복합 성장률(CAGR)로 가장 빠른 지역 성장을 보이며, 인도의 생산연계인센티브(PLI) 지원 페니실린 G 생산 재개와 2023년 40개 혁신의약품 승인 속 중국의 확대되는 내수 수요에 힘입고 있습니다. 일본은 중국 의존도 탈피를 위한 다각화 차원에서 가동 중단된 원료의약품(API) 공장 재가동으로 세계의 시장 점유율 하락에 대응하고 있으며, 한국의 단계별 가격 모델은 광범위 항생제 접근성을 높이고 있습니다. 호주의 벤자틴 벤질페니실린 부족 사태는 수입 의존의 취약성을 드러내며 자립적 제조에 대한 입법 논의를 촉발했습니다.

라틴아메리카, 중동, 아프리카는 증가하는 감염병 부담과 건강보험 보급률의 점진적 개선이 맞물립니다. 입찰 중심 조달은 저비용 천연물 의약품을 선호하지만, 공급 변동성과 통화 변동성이 물량 성장을 제한합니다. 보건의료 인프라를 대상으로 한 다자개발은행 프로젝트가 추가 수요를 창출할 것으로 예상되나, 콜드체인 및 처방자 교육 제약 극복 여부가 흡수력에 좌우될 전망입니다.

The Penicillin Drug Market was valued at USD 11.05 billion in 2025 and estimated to grow from USD 11.39 billion in 2026 to reach USD 13.23 billion by 2031, at a CAGR of 3.05% during the forecast period (2026-2031).

This modest but steady trajectory reflects the maturity of penicillin as a foundational antibiotic while signaling fresh opportunities created by B-lactamase-inhibitor innovation, domestic active-pharmaceutical-ingredient (API) programs, and rising stewardship-focused demand for narrow-spectrum agents. Increasing drug-resistant gram-positive infections, a resurgence of fermentation capacity in Asia Pacific, and AI-enabled strain engineering are further shaping competitive dynamics. Manufacturers are localizing supply chains to offset Chinese API concentration, hospitals are tightening formulary controls around first-line agents, and online pharmacies are capturing incremental retail volumes. Together, these factors are expected to keep the penicillin drug market on a resilient growth path even as broader antibiotic volumes plateau.

Healthcare systems worldwide are confronting an upsurge in methicillin-resistant Staphylococcus and carbapenem-resistant Acinetobacter strains, prompting renewed reliance on narrow-spectrum penicillins coupled with targeted diagnostics. The WHO classifies several natural penicillins as "Access" agents, encouraging prescribers to prefer them over broader alternatives that accelerate resistance development. Surveillance data highlight Staphylococcus borealis showing penicillin resistance in one-third of isolates, a finding that is catalyzing combination-therapy research and reinforcing demand for established agents that remain effective when properly stewarded. Hospitals are therefore expanding use of penicillin susceptibility-testing panels and integrating rapid molecular diagnostics to fine-tune prescriptions, a trend expected to underpin steady volumes over the medium term.

Pharmaceutical pipelines are increasingly populated by B-lactamase-inhibitor pairings that rejuvenate penicillin effectiveness against resistant phenotypes. The U.S. FDA cleared sulbactam-durlobactam for Acinetobacter infections in 2023, demonstrating markedly lower nephrotoxicity than colistin. Triple regimens combining meropenem, avibactam, and next-generation metallo-B-lactamase blockers are reporting favorable Phase II outcomes, broadening options for multidrug-resistant cases. Device innovation is also visible: the DUPLEX container for piperacillin-tazobactam gained approval in April 2025, cutting bedside preparation time and curbing contamination events. Such clinical and technical advances are likely to sustain premium pricing power for advanced semisynthetic penicillins, contributing materially to penicillin drug market growth.

High-risk clones such as Klebsiella pneumoniae ST307 exhibit resistance rates exceeding 85% to third-generation cephalosporins and 60% to carbapenems, directly threatening B-lactam efficacy. Carbapenem-resistant Acinetobacter has reached critical priority on the WHO list, with cross-class resistance that undermines both penicillins and advanced cephalosporins. Escalating treatment complexity inflates hospital costs, narrows therapeutic options, and fuels a tilt toward reserve antibiotics that bypass penicillin, collectively dampening market momentum in acute care.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Natural penicillins accounted for 53.10% of penicillin drug market share in 2025, certifying their continuing primacy in empirical therapy for streptococcal and syphilitic infections. Their mature fermentation know-how, low cost of goods, and inclusion on essential-medicine lists sustain robust baseline volumes. Semisynthetic classes aminopenicillins, antipseudomonal agents, and B-lactamase-inhibitor combinations are scaling at a 6.35% CAGR, propelled by rising resistance patterns and hospital demand for broader coverage. Penicillin drug market size gains in the semisynthetic cohort are further accelerated by fresh approvals such as sulbactam durlobactam and formulation enhancements like the DUPLEX ready-to-use system.

In competitive terms, semisynthetic pipelines attract disproportionate R&D funding because incremental spectrum extensions command higher reimbursed prices than legacy naturals. India's PLI program offers a 10% incentive for chemical-synthesis routes versus 20% for fermentation, nudging manufacturers to modernize bio-based capacity rather than pivot exclusively to synthetic APIs. Breakthroughs in Penicillium genomic editing promise yield improvements that could lift natural penicillin output while preserving the economic appeal pivotal for low-income-country tender markets.

Oral preparations represented 41.05% of the penicillin drug market size in 2025 and are advancing at the fastest 5.85% CAGR, buoyed by outpatient care models, pediatric dosing convenience, and higher patient adherence. Amoxicillin-clavulanate combinations remain among the top global prescriptions, with expanded-spectrum options targeting common respiratory pathogens. Penicillin drug market share gains in oral formats mirror payer strategies that incentivize early discharge and home-based therapy to contain hospitalization expenses.

Parenteral agents retain importance for severe infections and surgical prophylaxis but grow more slowly due to administration complexity. Hospitals are adopting pharmacist-led stewardship protocols that enable safe substitution of cefazolin and natural penicillins in penicillin-allergy-labelled patients, essentially widening parenteral demand while reducing reliance on costlier carbapenems. Device innovation exemplified by DUPLEX minimizes preparation errors and supports just-in-time compounding, modestly offsetting the growth differential with oral products.

The Penicillin Drug Market Report is Segmented by Source (Natural, Semisynthetic & Biosynthetic [Aminopenicillin, Antipseudomonal Penicillin, and More]), Route of Administration (Oral, Parenteral), End User (Human Health, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated the highest regional revenue, capturing 37.20% penicillin drug market share in 2025 on the back of sophisticated reimbursement systems, widespread susceptibility testing, and robust antimicrobial-stewardship mandates. Hospitals in the United States maintain high per-capita consumption driven by surgical volumes, while Canada's universal insurance favors generic narrow-spectrum agents. Cross-border trade with Mexico supplies cost-sensitive segments and supports nearshoring strategies that mitigate API import risks from Asia.

Europe follows with entrenched prescription frameworks and state financing for antibiotic modernization. Sandoz's EUR 200 million upgrade to its Austrian production hub secures continental supply and positions the bloc as an emerging exporter of finished formulations. The European Medicines Agency's harmonized labeling push encourages narrow-spectrum choices, sustaining volume stability even as total antimicrobial usage aims to decline by 30% by 2030.

Asia Pacific delivers the fastest regional growth at a 5.05% CAGR, propelled by India's PLI-funded penicillin G restart and China's expanding domestic demand amid 40 innovative drug approvals in 2023. Japan is countering lost global share by reopening mothballed API plants to diversify away from Chinese dependence, while South Korea's tiered pricing model lifts access to extended-spectrum agents. Australia's benzathine benzylpenicillin shortages illustrate the fragility of import reliance, spurring legislative debate over sovereign manufacturing.

Latin America, the Middle East, and Africa combine rising infectious-disease burdens with gradual improvements in health-insurance penetration. Tender-driven procurement favors low-cost naturals, though supply variability and currency volatility temper volume growth. Multilateral development-bank projects targeting healthcare infrastructure are expected to unlock incremental demand, yet absorption will hinge on overcoming cold-chain and prescriber-education constraints.