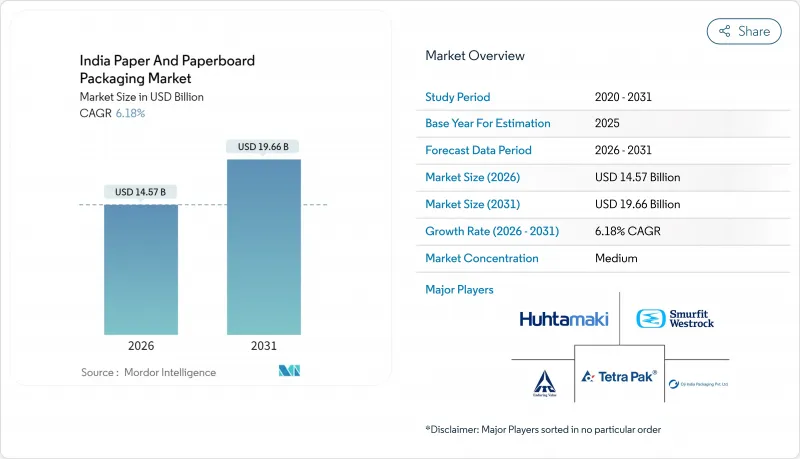

2026년 인도의 종이 및 판지 포장 시장 규모는 145억 7,000만 달러로 추정되며, 2025년 137억 2,000만 달러에서 성장할 것으로 예상됩니다.

2031년까지는 196억 6,000만 달러에 달하고,, 2026-2031년에 걸쳐 CAGR 6.18%로 확대될 전망입니다.

수요의 기세는 전국적인 일회용 플라스틱 폐지, 전자상거래 물류의 급속한 확대, 순환 경제 포장에 대한 브랜드 헌신을 반영합니다. 온라인 소매에서는 내충격성과 경량 수송 형태가 요구되기 때문에 판지 상자가 주류를 차지하고 있습니다. 한편, 액체용 카톤은 고급 음료의 성장과 무균 충전에 대한 투자의 혜택을 받고 있습니다. 식음료 브랜드는 재활용 가능한 단일 소재 포장의 도입을 가속화하고 있으며, 티어 1 도시와 티어 2 도시에서의 퀵커머스 거점의 확대에 의해 소형 2차 포장의 잠재 시장이 확대되고 있습니다. 공급면에서는 재생섬유의 생산 능력, 농업 잔류물 펄프라인, 고속 플렉소 인쇄기의 확충이 진행되고 있지만, 에너지 가격의 상승이나 수입 고지 가격의 변동에 의해 이익률 압력은 유지되고 있습니다.

주문량의 급증과 최대 35kg까지 허가된 퀵커머스 중량물 배송으로 컨버터는 라스트마일 효율화를 위해 강도와 평량을 양립한 판지 설계를 추구하고 있습니다. 플립 카트는 플라스틱 완충재 폐지 정책을 통해 이미 수백만 개의 소포를 종이 기반 포장으로 전환시켰습니다. Adani Wilmer와 같은 FMCG 공급업체는 온라인 채널을 위한 대형 SKU를 도입하여 판지 사용량 증가를 촉진하고 있습니다. 방갈로르와 델리 지역의 허브 네트워크는 보충을 가속화하지만 동시에 접촉점을 늘려 브랜드 가치를 유지하는 인쇄 그래픽에 대한 수요를 확대하고 있습니다. 결과적으로 판지 제조업체는 인라인 플렉소 폴더와 디지털 인쇄 모듈을 도입하여 준비 시간을 단축하고 폐기물을 줄이기 위해 노력하고 있습니다. 따라서 인도의 종이 및 판지 포장 시장은 전자상거래의 침투와 소재 중립의 지속가능성 요건이 교차하는 가운데 구조적인 상승효과를 얻고 있습니다.

도시 지역의 소비자가 포장 라벨의 폐기 실적을 조사하는 가운데 재활용 가능성이 구매 결정 요인이 되었습니다. 주요 식품 가공업자는 다층 플라스틱을 사용하지 않고 유지 및 습기 차단 기능을 실현하는 수성 또는 바이오폴리머 코팅 단일 소재 판지에 대한 라미네이트 재설계를 진행하고 있습니다. 후타마키와 인도 산업연맹의 제휴를 통해 단일 소재 형태가 기계적 재활용 프로세스를 용이하게 하는 방법을 명시한 오픈소스 설계 가이드가 작성되었습니다. 브랜드 소유자가 2026년에 강화되는 생산자 책임 재활용(EPR) 달성을 목표로 하는 가운데 섬유의 순도와 추적성을 보장할 수 있는 벤더가 높게 평가됩니다. 코팅 화학은 인라인에서 대규모로 적용될 수 있기 때문에 컨버터는 이익률과 속도의 양면에서 우위를 확보하고 인도의 종이 및 판지 포장 시장에서 장기적인 성장 원동력을 강화하고 있습니다.

인도에서는 재생 판지 원료의 약 30%를 해상 수송에 의한 재생 섬유에 의존하고 있으며, 운송 장애나 입찰 경쟁이 스팟 가격을 높여 제지 공장의 이익률을 압박하고 있습니다. 인도 제지공업회는 중국 및 칠레로부터의 다층 판지 수입에 대해 가격파괴를 이유로 관세부과를 요청했습니다. JK 페이퍼의 2024년도 이익 58% 감소는 비용 급등이 수익과 직결된 실사례입니다. 2025년 중반에는 북미의 새로운 펄프라인이 세계 가격을 억제했지만, 환율 변동과 홍해 항로 리스크에 의해 변동성은 높아지고, 인도의 종이 및 판지 포장 시장의 단기 성장세를 둔화시키고 있습니다.

판지 원지는 2025년 매출의 48.23%를 차지하였고 완충성과 팔레트 효율을 중시하는 EC 풀필먼트 센터에 의해 뒷받침되고 있습니다. 액체용 카톤은 규모가 작지만 고급 유제품 주스 및 무균 조리 식품 솔루션을 배경으로 CAGR 7.28%가 전망되고 있습니다. 판지용 등급은 인도의 종이 및 판지 포장 시장에서 전환 비용을 줄이는 인라인 인쇄 및 다이컷 기술에 대한 투자를 원동력으로 2026-2031년에 걸쳐 22억 9,000만 달러까지 증가할 것으로 예측되고 있습니다. 테트라팩의 획기적인 5% ISCC PLUS 인증 재생 폴리머층 도입을 계기로 UFlex 등 액체용 카톤의 대기업은 연간 생산량을 120억 팩으로 확대할 계획입니다. 한편, 접이식 카톤은 단일 소재 가이드라인에 맞는 수성 배리어 코트를 통한 개선으로 소비재 부문에서 안정적인 기반을 유지하고 있습니다. 특수 판지와 성형 섬유는 틈새 보호 요건과 환경친화적인 브랜딩을 배경으로 원료 가격 변동을 완화하는 프리미엄 가격 차이를 확보하고 있습니다.

경쟁의 관점에서 ITC와 같은 주요 그룹은 농림업에서 완성된 판지에 이르기까지 모든 프로세스를 관리하여 원료 헤징 및 제품 개발 사이클의 단축을 실현합니다. 이에 비해 판지 제조업체는 디지털 시장에 가까운 장소에 인쇄 프로세스를 배치하여 당일 상자 보충을 실현함으로써 대응하고 있습니다. 인도의 종이 및 판지 포장 시장이 슈퍼 로컬 배송으로 전환하는 가운데 이는 운영상의 이점이 되었습니다.

식음료 브랜드는 엄격한 위생 기준과 확대되는 콜드체인으로 2025년 매출의 39.35%를 차지했습니다. 한편, 퍼스널케어 및 화장품 부문은 7.72%의 연평균 복합 성장률(CAGR)이 예상되어 높은 성장률을 나타내고 있습니다. 푸드서비스 산업에서는 패스트푸드점이 재생 섬유와 PLA 분산체로 만들어진 내유성 클램쉘 용기를 도입하여 일회용 플라스틱 금지 지침에 대응하고 있습니다. 퍼스널케어 제품은 인도의 종이 및 판지 포장 시장에서 고급 브랜드가 플라스틱 용기에서 경질 종이 관 또는 오프셋 인쇄 슬리브로 이행하는 움직임으로 인해 2031년까지 5억 6,800만 달러로 성장할 전망입니다.

의료 부문에서는 국내 제약 생산량이 증가함에 따라 블리스터 포장용 안감과 의료용 카톤에 대한 수요가 안정되고 있습니다. 전자기기 제조업체는 정전기 방지 섬유 트레이를 요구하면서도, 발포재와의 기능적 동등성을 고려한 비용 비교에 의해 급격한 성장은 억제되고 있습니다. 산업용 및 자동차 부품 부문에서는 다층 판지 상자가 '메이크인 인디아' 시책에 의한 조달 확대와 함께 폭넓은 최종 용도 부문으로 균형 잡힌 수익 기반을 확보하고 있습니다.

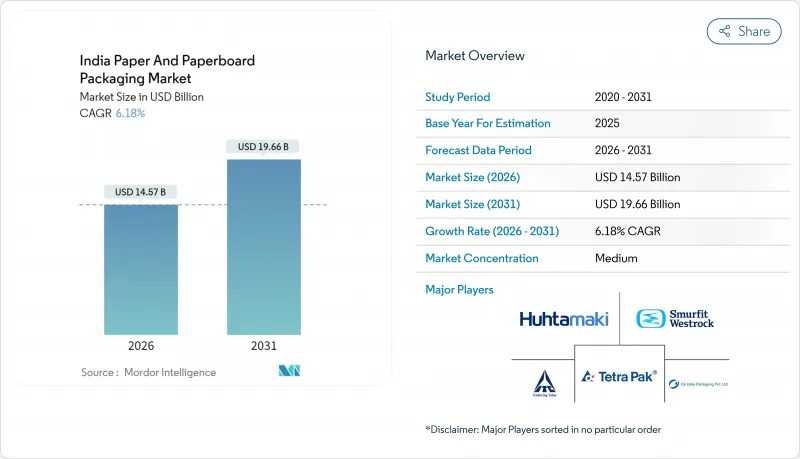

India paper and paperboard packaging market size in 2026 is estimated at USD 14.57 billion, growing from 2025 value of USD 13.72 billion with 2031 projections showing USD 19.66 billion, growing at 6.18% CAGR over 2026-2031.

Demand momentum reflects the nationwide shift away from single-use plastics, the rapid scale-up of e-commerce logistics, and brand commitments to circular-economy packaging.Corrugated boxes dominate because online retail requires impact-resistant yet lightweight transit formats, while liquid cartons are benefiting from premium beverage growth and aseptic filling investments. Food and beverage brands accelerate the adoption of recyclable mono-material packs, and quick-commerce hubs in Tier-1 and Tier-2 cities enlarge the addressable base for small-format secondary packs. On the supply side, recycled fiber capacity, agro-residue pulp lines, and high-speed flexo presses are expanding, yet margin pressure persists due to energy inflation and volatile imported waste-paper prices.

Order-volume surges and heavier quick-commerce shipments now permitted up to 35 kg are pushing converters to engineer corrugated designs that balance strength and grammage for last-mile efficiency. Flipkart's commitment to eliminating plastic cushioning has already converted millions of parcels to paper-based formats. FMCG suppliers such as Adani Wilmar have introduced larger stock-keeping units tailored for online channels, fueling incremental box tonnage. Regional hub networks in Bengaluru and Delhi enable faster replenishment but also multiply touch-points, widening demand for high-print graphics that preserve brand equity. As a result, corrugators are installing inline flexo folders and digital print modules to shorten make-ready times and cut waste. The India paper and paperboard packaging market, therefore, derives a structural uplift from the intersection of e-commerce penetration and material-neutral sustainability mandates.

Recyclability is now a purchase driver as urban consumers scrutinize pack labels for end-of-life credentials. Large food processors are reformulating laminates toward single-substrate paperboard combined with aqueous or biopolymer coatings that deliver grease and moisture barriers without multi-layer plastics. Huhtamaki's partnership with the Confederation of Indian Industry created open-source design guides that clarify how mono-material formats ease mechanical recycling workflows. As brand owners chase Extended Producer Responsibility targets that ramp up in 2026, vendors able to guarantee fiber purity and traceability gain preference.Because coating chemistries can be applied in-line at scale, converters capture both margin and speed advantages, reinforcing the long-run tailwind on the India paper and paperboard packaging market.

India relies on seaborne recovered fiber for roughly 30% of recycled-board furnish; freight disruptions and bidding wars push spot prices, squeezing mill margins. The Indian Paper Manufacturers Association has petitioned for duties on multi-layer board imports from China and Chile, citing price undercutting. JK Paper's FY 2024 profit drop of 58% exemplifies how cost spikes flow through earnings. Although new North American pulp lines tempered global prices in mid-2025, currency swings and Red Sea routing risks keep volatility elevated, dampening the near-term growth tempo of the India paper and paperboard packaging market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Corrugated stock generated 48.23% of 2025 revenue, buoyed by e-commerce fulfillment centers that prize cushioning and pallet efficiency. Liquid cartons, though smaller, are slated for a 7.28% CAGR on the back of premium dairy, juice, and aseptic meal solutions. The India paper and paperboard packaging market size for corrugated grades is projected to increase by an additional USD 2.29 billion between 2026 and 2031, driven by investments in inline print-and-die-cut technology that lowers changeover costs. Liquid-carton leaders such as UFlex plan to lift output to 12 billion packs annually, helped by Tetra Pak's landmark rollout of 5% ISCC PLUS certified recycled-polymer layers. In parallel, folding cartons maintain a stable FMCG base, upgraded by water-based barrier coats that meet mono-material guidelines. Specialty paperboards and molded fiber trade on niche protection requirements and ecological branding, commanding premium spreads that cushion input volatility.

From a competitive stance, large groups like ITC control the full chain from agro-forestry to finished board, enabling raw-material hedging and shorter product-development cycles. Corrugators respond by co-locating print cells near digital marketplaces to deliver same-day box replenishment, an operational edge as the India paper and paperboard packaging market pivots toward hyperlocal delivery.

Food and beverage brands captured 39.35% revenue in 2025 due to stringent hygiene codes and an expanding cold chain, while personal care and cosmetics outperformed with an 7.72% CAGR forecast. Within food-service, quick-serve restaurants adopt grease-resistant clamshells built from recycled fiber plus PLA dispersion, aligning with the single-use-plastic ban. The India paper and paperboard packaging market size for personal-care items is slated to advance by USD 568 million through 2031 as premium labels trade plastic jars for rigid paperboard tubes and offset-printed sleeves.

On the healthcare front, blister backing and medical-grade cartons enjoy secure demand as domestic pharma output climbs. Electronics brands seek static-safe fiber trays but weigh cost against functional parity with foam, damping runaway growth. Industrial and automotive parts rely on multi-wall corrugated crates that dovetail with the Make in India sourcing expansion, ensuring a broad, balanced revenue footprint across end-use bands.

The India Paper and Paperboard Packaging Market Report is Segmented by Product Type (Folding Cartons, Corrugated Packaging, Liquid Cartons, and More), End-User Vertical (Food and Beverage, Healthcare and Pharma, Automotive, and More), Packaging Format (Primary Retail Packs, Secondary Transit Packs, and More), Material Grade (Virgin Fiber, Recycled Fiber, and More). The Market Forecasts are Provided in Terms of Value (USD).