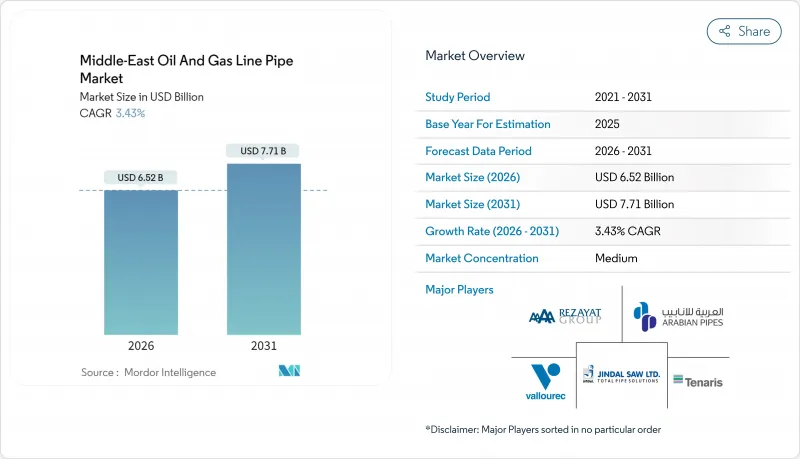

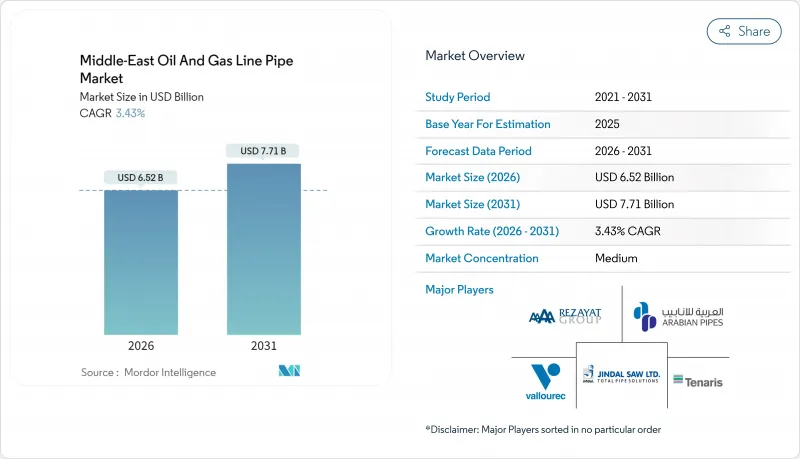

중동의 석유 및 가스 라인 파이프 시장은 2025년 63억 달러로 평가되었으며, 2026년 65억 2,000만 달러에서 2031년까지 77억 1,000만 달러에 이를 것으로 예상됩니다.

예측 기간(2026-2031년)에 있어서 CAGR은 3.43%를 나타낼 것으로 전망되고 있습니다.

견조한 업스트림 가스 사업, 국경을 넘는 간선 파이프라인, 수소 대응 파일럿 사업이 주요한 성장 엔진인 한편, 현지 조달 의무에 의해 국내 제조업체에의 조달 경향이 강해지고 있습니다. 대구경 나선 용접관 수요 증가, 사워 가스·수소 환경에 있어서 2상강의 용도 확대, 정부 지출에 의한 지원책이, 지역 제조업체의 경쟁력을 강화하고 있습니다. 한편, EU 탄소 국경 조정 메커니즘(CBAM)에 의한 비용 압력과 돌발적인 원유 가격 충격은 수출업체의 단기적인 확대를 억제하고 있습니다. 이란의 프로젝트 연기 및 이라크의 선택적 자금 조달 지연은 지정학적 위험이 지출 동향에 지속적으로 영향을 미치는 실태를 보여줍니다.

아부다비 국영 석유회사(ADNOC)의 170억 달러 규모의 힐 & 가샤 계획은 하루에 15억 입방 피트의 초산성 가스를 운송할 수 있는 내식성 라이닝(CRA)을 실시한 파이프라인을 요구하며, 모든 입찰에 높은 수준의 내식성 요건이 포함되어 있습니다. 카타르의 노스필드 웨스트(예산 약 170-180억 달러)에서는 EPCI 계약자가 고압 정격의 24인치 이상의 스풀을 통합하기 때문에 해저 파이프 수요가 크게 증가하고 있습니다. 사우디아라비아의 홍해 앞바다 평가 프로젝트는 2030년까지 가스 생산량을 60% 증가시키는 목표 달성과 관련되어 있으며, 얕은 해역에서의 유연한 플로우 라인이 선호되고 있습니다. 이것은 복합재료 대체품에 틈새 기회입니다. 걸프 전역에서 수심이 증가함에 따라 24인치 이상의 파이프 직경이 필수적이며 용접식 SAW 파이프공급량이 증가하고 있습니다. 인증 요건도 엄격해지고 있으며, UAE 및 사우디아라비아 광구에서 운영하는 해양 계약업체는 ISO 14001 준수를 의무화하고 사실상 자격 증명의 장애물을 인상하고 있습니다.

2024년 3월에 이라크 내각의 승인을 얻은 바스라-아카바간 파이프라인(전장 1,200km, 총 사업비 50억 달러)은 일량 225만 배럴의 수출 능력을 목표로 하고 있습니다. 그러나 은행 제재로 인해 자금 조달이 복잡해지고 실시 기간이 장기화 될 전망입니다. 사우디아라비아와 쿠웨이트의 파트너 회사는 Dollargas 논을 위한 공동 파이프라인을 설계 중이며 해양 단위화가 파이프라인 패키지의 규모 확대에 기여하고 있음을 보여줍니다. 인도·중동·유럽 경제 회랑(IMEC)에서 구상되는 수소 회랑에서는 파단 인성 지표를 통합함으로써 API 5L X70을 넘는 수소 대응 강재에 대한 재료 사양 강화가 진행되고 있습니다. 정치적으로 민감한 장거리 루트에서는 두꺼운 두께와 확대된 음극방식이 요구되어 톤수와 가치가 증가하고 있습니다.

과거 데이터에 따르면 원유 가격 하락과 중동에서 EPC 계약 수여에는 12개월의 시간 지연이 발생했으며, 2014년부터 2015년까지의 사례에서는 18개월 동안 계약 수가 60% 감소했습니다. 현재의 파이프라인 EPC 계약에 있어서 헤지 조항에는 브렌트 원유 가격이 90일 연속으로 배럴당 50 USD를 하회했을 경우, 15-20%의 코스트 상승폭이 설정되어 있습니다. 이라크에서는 석유부와 관련된 여러 파이프라인 프로젝트가 세입 부족으로 2026년 예산 사이클에 통합되었습니다. 사우디아라비아와 UAE의 소블린 펀드는 부분적으로 역순환적이지만, GCC의 소규모 국가들은 유사한 완충재가 없으며 프로젝트의 타이밍 위험을 증폭시키고 있습니다.

2025년 중동의 석유 및 가스 라인 파이프 시장에서 용접 파이프가 62.25%의 점유율을 차지하고 SAW의 비용 우위성을 중시하는 장거리 원유·가스 프로젝트를 지원했습니다. G5PS사가 사우디 아람코사로부터 1억 8,600만 사우디아라비아 리얄(5,000만 달러)의 나선형 용접 파이프 수주를 획득한 것으로, 중요한 수송 파이프라인에 있어서 SAW의 채용이 더욱 강화되었습니다. 무봉강관공급은 재료의 무결성이 비용을 초과하는 고압 수소 파일럿 플랜트에서 여전히 필수적이지만, 대량 수송 분야의 점유율은 점차 감소하고 있습니다. 운송비 절감과 현지 조달 크레딧이 수입 무봉강관의 장점을 상회하기 때문에 현지 생산화로 용접강관 플랜트의 경쟁력이 높아지고 있습니다. 간선 파이프라인이 연장됨에 따라 중동의 석유 및 가스 라인 파이프 시장에서 용접 강관 카테고리의 규모는 2031년까지 연평균 복합 성장률(CAGR) 3.44%로 확대될 것으로 예측됩니다.

자동 초음파 검사와 로봇 용접의 보급 확대로 품질 수준이 향상되고, 현장에서의 불량품률이 저하, 라이프 사이클 비용이 절감되고 있습니다. 테나리스 사우디 스틸 파이프스는 향후 대규모 가스 프로젝트에 대응하기 위해 2024년 7월 주바이르 공장의 LSAW(긴 용접 강관) 생산 능력을 두배로 늘렸습니다. 코팅 라인과 나사 절단 라인을 자체 내부에 통합하는 제조업체는 부가가치를 높이고 가속화되는 납기 요구에 더 잘 대응하고 있습니다.

탄소강은 기존의 석유 및 가스 운송에서 비용 성능의 적합성으로 2025년에 64.40%의 점유율을 획득했습니다. 그러나 수소, 블루 암모니아 및 초산성 가스 수송에는 우수한 내식성 및 내취화성이 요구되기 때문에 2상강 및 초2상강 부문은 6.00%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. SABIC사가 다루는 연간 120만 톤의 블루 암모니아 프로젝트의 FEED에서는 극저온 대응 듀플렉스 강관 라인이 요구되고, 조달 대상이 탄소강 등급에서 이행하고 있습니다. 또한 사우디아라비아의 마스터 가스 시스템에 있어서 고압 가스용 합금 선정도 API 5L X80로 이행하고 있어 고강도화의 동향이 정착하고 있습니다.

에미레이트 스틸 알칸에 의한 슈퍼 듀플렉스 용해 경로의 투자는 지역 제강소가 특수강의 이익률을 추구하고 있음을 보여줍니다. 중동의 석유 및 가스 라인 파이프 시장에서의 특수 합금 점유율은 여전히 겸손하지만, 이익에 대한 기여도는 매우 크며 제품 가격 변동으로부터 제강소를 보호하고 있습니다.

중동의 석유 및 가스 라인 파이프 시장 보고서는 유형별(심리스관·용접관), 재질별(탄소강, 합금강, 스테인리스/내식 합금강, 2상/슈퍼 2상강), 직경별(12인치 미만, 12-24인치, 24인치 이상과), 용도(수송, 갱내 케이싱·튜빙, 석유 및 가스 집약, 물·가스 주입), 지역(사우디아라비아, 아랍에미리트(UAE), 카타르, 쿠웨이트, 바레인, 이라크 등)별로 분류되고 있습니다.

The Middle-East Oil And Gas Line Pipe Market was valued at USD 6.30 billion in 2025 and estimated to grow from USD 6.52 billion in 2026 to reach USD 7.71 billion by 2031, at a CAGR of 3.43% during the forecast period (2026-2031).

Robust upstream gas programs, cross-border trunk lines, and hydrogen-ready pilots are the principal growth engines, while localization mandates tilt procurement in favor of domestic mills. Rising demand for large-diameter spiral-welded pipes, widening use of duplex alloys in sour-gas and hydrogen service, and supportive sovereign spending buffers are strengthening the competitive positions of regional manufacturers. At the same time, cost pressures from the EU Carbon Border Adjustment Mechanism (CBAM) and episodic oil-price shocks temper near-term expansion for exporters. Project deferrals in Iran and selective funding delays in Iraq demonstrate how geopolitical risk continues to impact spending trajectories.

ADNOC's USD 17 billion Hail & Ghasha program requires CRA-lined lines that can carry 1.5 billion cubic feet per day of ultra-sour gas, inserting premium corrosion-resistant requirements into every bid. Qatar's North Field West, budgeted at about USD 17-18 billion, adds substantial subsea pipe demand as EPCI contractors integrate 24-in-plus spools with elevated pressure ratings. Saudi Arabia's offshore Red Sea appraisals, linked to meeting a 60% gas production growth target by 2030, favor flexible flowlines in shallow waters-a niche opportunity for composite alternatives. Deeper water profiles across the Gulf now mandate diameters of>= 24 inches, shifting volumes toward welded SAW supply. Certification requirements are tightening, with ISO 14001 compliance compulsory for offshore contractors operating in the UAE and Saudi blocks, effectively lifting qualification thresholds.

The 1,200 km, USD 5 billion Basra-Aqaba pipeline, which won Iraqi cabinet clearance in March 2024, targets a 2.25 million bpd export capacity. However, banking sanctions complicate financing, lengthening the execution window. Saudi and Kuwaiti partners are designing shared pipelines for the Dorra gas field, underscoring how maritime unitization is enlarging pipe packages. Hydrogen corridors outlined in the India-Middle East-Europe Economic Corridor (IMEC) enhance material specifications toward hydrogen-compatible steels that exceed API 5L X70 by incorporating fracture-toughness metrics. Longer, politically sensitive routes are also specifying thicker walls and expanded cathodic protection, magnifying tonnage and value.

Historical data indicate a 12-month lag between crude-price dips and Middle East EPC awards, with the 2014-2015 episode resulting in a 60% reduction in contracts over 18 months. Current hedging clauses in pipeline EPCTs include cost-escalation bandwidths of 15-20% once Brent oil prices fall below USD 50 per barrel for 90 consecutive days. In Iraq, several pipeline projects linked to the Ministry of Oil have been included in the 2026 budget cycle amid revenue shortfalls. Saudi and UAE sovereign funds are partially counter-cyclical; however, smaller GCC states lack similar buffers, thereby amplifying project timing risk.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Welded pipe claimed a 62.25% share of the Middle East oil and gas line pipe market in 2025, underpinning long-distance crude and gas projects that favor SAW cost economics. G5PS secured a SAR 186 million (USD 50 million) Aramco spiral-welded order, reinforcing SAW acceptance in critical transmission. Seamless supply remains indispensable for high-pressure hydrogen pilots where material integrity trumps cost, but its share is inching down within bulk transmission. Localization makes welded plants more competitive because shipping savings and local-content credits outweigh the benefits of seamless imports. The Middle East oil and gas line pipe market size attributable to welded categories is projected to post a 3.44% CAGR through 2031 as trunk-line kilometers expand.

The growing adoption of automated ultrasonic inspection and robotic welding is enhancing quality levels, reducing field rejects, and lowering lifecycle cost profiles. Tenaris Saudi Steel Pipes doubled LSAW capacity in Jubail in July 2024 to address upcoming master-gas packages. Mills that integrate coating and threading lines in-house are capturing additional value and better meeting accelerated delivery timetables.

Carbon steel captured a 64.40% share in 2025 thanks to its cost-performance fit in conventional oil and gas flows. However, the duplex and super-duplex segment is growing at a 6.00% CAGR because hydrogen, blue ammonia, and ultra-sour gas service require superior corrosion and embrittlement resistance. SABIC's FEED for a 1.2 million tpa blue ammonia project calls for cryogenic-capable duplex lines, moving procurement beyond carbon grades. Alloy selections are also migrating toward API 5L X80 for high-pressure gas in Saudi Arabia's Master Gas System, cementing a trend toward higher strength.

Investment by Emirates Steel Arkan into super-duplex melt routes indicates regional mills are chasing specialty margins. The Middle East oil and gas line pipe market share for specialty alloys remains modest, but its contribution to profits is outsized, shielding mills from commodity price swings.

The Middle-East Oil and Gas Line Pipe Market Report is Segmented by Type (Seamless and Welded), Material (Carbon Steel, Alloy Steel, Stainless/CRA, and Duplex/Super-Duplex), Diameter (Below 12 Inch, 12 To 24 Inch, and Above 24 Inch), Application (Transmission, Down-Hole Casing and Tubing, Oil and Gas Gathering, and Water/Gas Injection), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Iraq, and More).