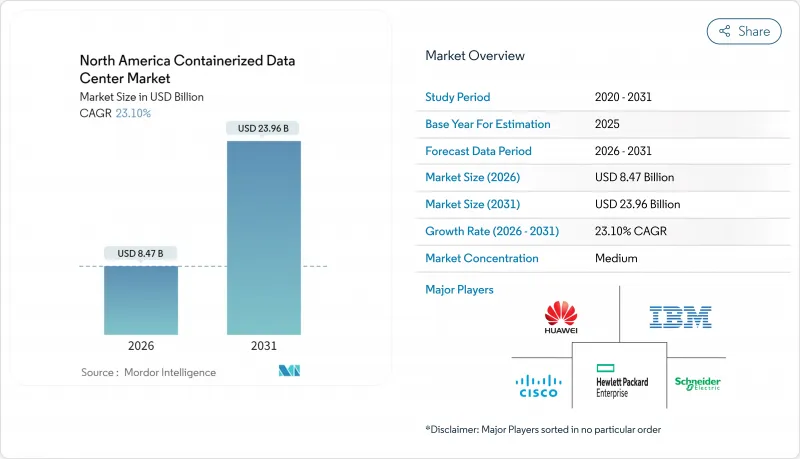

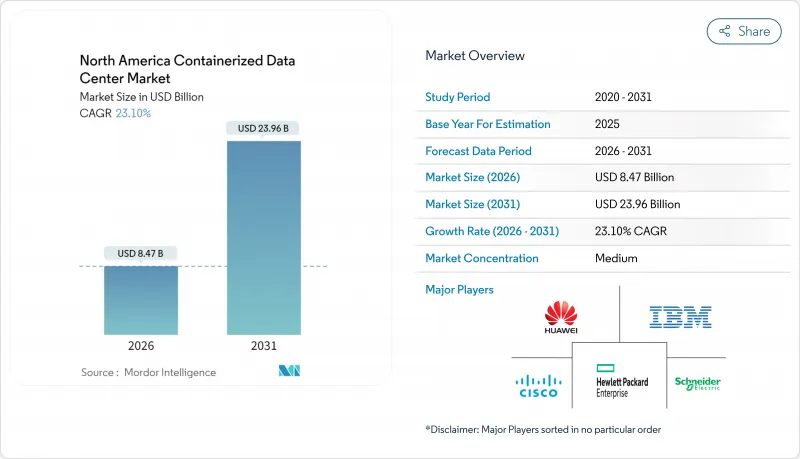

북미의 컨테이너형 데이터센터 시장은 2025년 68억 8,000만 달러로 평가되었으며, 2026년 84억 7,000만 달러에서 2031년까지 239억 6,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2026-2031년)에 있어서 CAGR은 23.10%를 나타낼 것으로 전망됩니다.

5G 배포와 인공지능 워크로드가 급증함에 따라 컴퓨팅 리소스를 사용자에게 가깝게 배치해야 하는 기업의 도입이 가속화되고 있습니다.

전력망의 제약에 직면하는 하이퍼스케일러 기업은 기존 건설의 18-24개월을 필요로 하는 대신 12-14주간 가동 가능한 모듈러 유닛을 실시에 추가 도입하고 있습니다. 관련 매크로 요인으로는 오프 그리드 내성을 실현하기 위해 소형 모듈로와 조립식 포드를 결합한 파일럿 프로그램과 전장의 AI 능력에 대한 방위 수요 증가가 있습니다. 랙 밀도가 40kW를 넘는 가운데 액체 냉각 기술과 조립식 전원 모듈을 습득한 공급업체는 다음의 성장파를 포착하는 태세가 갖추어져 있습니다.

디지털 혁신의 타임라인이 단축되는 가운데, 기업은 신규 시설 건설에 필요한 기간을 크게 하회하는 12-14주간의 도입이 가능한 솔루션을 우선하고 있습니다. IBM의 휴대용 모듈형 데이터센터는 건설 근로자와 허가 절차가 병목 현상이 되는 원격지 및 내륙 지역에서의 확장 시나리오에서 턴키형 격납장치가 요구를 충족시키는 방법을 보여줍니다. 통신 캐리어도 네트워크 에지에서 유사한 논리를 채택하고 표준화된 포드를 사용하여 지역 5G 허브를 구축함으로써 장기 임대에 의한 자본의 구속을 회피하고 있습니다. Eaton과 같은 공급업체는 통합 전원 공급 장치와 인-로우 냉각 기능을 갖춘 기성품 랙을 판매하여 중견 시장용 구매자의 설치 주기를 단축하고 있습니다. 이 속도의 이점은 예측할 수 없는 AI 추론 수요의 급증에 대응해야 하는 클라우드 제공업체에게도 중요합니다. 종합하면, 신속한 도입이라는 추진력은 선구자의 우위성을 증폭시켜, 보다 느리고, 기존의 건설 방식의 대안을 대체하고 있습니다.

2024년 기준에서 냉각에는 미국 데이터센터의 전력 소비량의 약 40%가 소비되어 운영 비용 증가와 지속가능성에 대한 엄격한 모니터링을 초래했습니다. 컨테이너형 아키텍처는 밀접하게 결합된 기류 경로와 칩 표면에 직접 도달하는 공장 설치형 액체 냉각을 통합하여 부하를 줄입니다. Microsoft는 모듈형 인클로저 내에서 칩 직결 냉각 루프의 테스트 운영을 수행하여 기존 시설보다 낮은 PUE 지표로 높은 랙 밀도를 달성했습니다. 분산형 설치를 통해 운영자는 재생에너지원 근처에 포드를 설치할 수 있어 탄소 강도 점수를 개선할 수 있습니다. GE 바노바의 RESTORE DC 블록 축전지 시스템은 동일한 ISO 표준으로 제공되어 재생에너지의 불안정성을 완화하는 하이브리드 축전을 실현합니다. 전기 요금 상승과 ESG 요건 강화로 설계 단계에서 효율성을 통합한 모듈형 플랫폼에 대한 수요가 증가하고 있습니다.

생성형 AI 트레이닝 클러스터는 랙당 40-60kW를 필요로 하는 경우에도 많은 컨테이너화 설계에서는 약 30kW가 상한이 되고 있습니다. 델 테크놀로지스는 2025년 1분기에 121억 달러의 AI 서버 수주를 획득했으며, 현재의 모듈러 사양을 넘는 계산 수요의 높이가 부각되고 있습니다. 연속적인 GPU 패브릭을 필요로 하는 고객은 냉각 플레넘과 버스웨이가 고밀도 부하에 대응하는 전용 설계 시설을 여전히 선택하는 경향이 있습니다. NVIDIA의 Blackwell 플랫폼은 기존의 ISO 표준 쉘에서는 재설계 없이는 대응할 수 없는 수준을 넘는 액체 냉각을 기본 사양으로 하고 있어 이 제약을 더욱 심각화시키고 있습니다. 따라서 기업은 에지추론을 위한 신속 도입 가능한 포드와 모델 트레이닝용 중앙시설에 자산을 분산시켜 향후 2년간 모듈형 도입의 전반적인 페이스를 조정할 전망입니다.

40피트 ISO 표준은 뛰어난 연산 밀도와 국제 운송 물류와의 호환성으로 2025년 수익의 51.45%를 유지했습니다. 그 이점은 하이퍼스케일러와 대기업에서 핵심 데이터센터의 전환 동향을 반영합니다. 한편, 20피트 ISO 규격의 대체품은 통신사업자가 마이크로 엣지 노드를 기지국 부지나 도시의 옥상 등 공간 제약이 있는 사이트에 도입하는 움직임에 따라 2031년까지 연평균 복합 성장률(CAGR) 19.12%를 나타낼 것으로 예측됩니다. 20피트 단위의 컨테이너형 데이터센터 시장 규모는 통신사업자가 5G 커버리지의 밀도 향상을 겨루는 가운데 급격히 확대될 것으로 전망됩니다. 설치 면적의 축소는 용지 정비 비용의 절감과 허가 수속의 간소화로 이어져, 통신 사업자가 서비스 차별화를 신속하게 실현하는 길을 엽니다. 한편, 40피트를 넘는 특주 케이스는 대형 전원 장치나 RF 실드가 필수가 되는 정부·에너지 프로젝트용입니다만, 수송상의 제약으로부터 주류화에는 이르지 않습니다.

수요의 양극화가 선명해지고 있습니다. 대형 ISO 표준은 클라우드 공급자의 핵심에서 에지로 수요 증가에 대응하고, 초소형 포드는 소매·제조·스마트 시티 전개에서 실시간 데이터 파이프라인을 지원합니다. 히타치 시스템즈는 2025년 5월, AI추론·서버룸 대체·통신 엣지 이용 사례를 커버하는 3표준 SKU로 제품 라인을 쇄신했습니다. 공급업체 각사가 「원 사이즈로 모두에 대응」의 시대가 종말한 것을 인식하고 있는 증좌입니다. CEATEC에 전시된 델타의 20피트 설계는 800G 이더넷과 1.5MW의 액체 냉각을 통합하여 보다 컴팩트한 공간에서도 고성능을 실현할 수 있음을 입증했습니다. 따라서 가격 성능 비율은 ISO 표준을 준수하면서 공급업체가 얼마나 능숙하게 고밀도 컴퓨팅을 패키징하는지에 달려 있습니다.

The North America containerized data center market was valued at USD 6.88 billion in 2025 and estimated to grow from USD 8.47 billion in 2026 to reach USD 23.96 billion by 2031, at a CAGR of 23.10% during the forecast period (2026-2031).

Accelerated uptake comes from enterprises that must position computing resources closer to users as 5G rollouts and artificial intelligence workloads surge.

Hyperscalers facing power-grid constraints are supplementing their brick-and-mortar footprints with modular units that can be commissioned in 12-14 weeks instead of the 18-24 months typical of conventional builds. Allied macro factors include pilot programs that pair small modular reactors with prefabricated pods to achieve off-grid resilience, as well as rising defense demand for battlefield AI capability. Vendors that master liquid cooling and prefabricated power modules are positioned to capture the next wave of growth as rack densities push past 40 kW.

Enterprises confronted by compressed digital-transformation timelines are prioritizing solutions that can be deployed in 12-14 weeks, well inside the window required for green-field facilities. IBM's Portable Modular Data Center illustrates how turnkey enclosures satisfy remote or land-locked expansion scenarios where construction crews and permits create bottlenecks Telecommunications carriers employ similar logic at the network edge, using standardized pods to seed regional 5G hubs without tying up capital in long-term leases. Suppliers such as Eaton now sell off-the-shelf racks with integrated power and in-row cooling, shortening installation cycles for mid-market buyers. The speed advantage is equally important to cloud providers that need to address unpredictable spikes in AI inference demand. Taken together, the rapid-deployment driver amplifies first-mover advantages and displaces slower, stick-built alternatives.

Cooling consumed close to 40% of U.S. data center electricity in 2024, resulting in elevated operating expenses and sustainability scrutiny. Containerized architectures mitigate the load by integrating tightly coupled airflow channels and factory-installed liquid cooling that reaches chip surfaces directly. Microsoft has piloted direct-to-chip coolant loops inside modular enclosures, achieving higher rack densities at lower PUE metrics than legacy halls . Distributed footprints also allow operators to drop pods alongside renewable sources, improving carbon-intensity scores. GE Vernova's RESTORE DC Block battery system is delivered in the same ISO form factor, enabling hybrid energy storage that smooths renewable intermittency. Rising electricity tariffs and ESG mandates therefore push buyers toward modular platforms that embed efficiency by design.

Generative AI training clusters often demand 40-60 kW per rack, yet many containerized designs cap out at roughly 30 kW. Dell Technologies booked USD 12.1 billion in AI-server orders in Q1 2025, highlighting compute appetites that overshoot current modular envelopes Customers that need contiguous GPU fabrics still gravitate toward purpose-built halls where cooling plenums and busways handle dense loads. Nvidia's Blackwell platform compounds the constraint by specifying liquid-cooling baselines that exceed what most ISO shells can accommodate without redesign. Enterprises therefore split estates between quick-turn pods for edge inference and centralized facilities for model training, moderating overall modular uptake during the next two years.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The 40-foot ISO format retained 51.45% of 2025 revenue owing to superior compute density and compatibility with global shipping logistics. Its dominance reflects the core data center conversion trend among hyperscalers and large enterprises. The 20-foot ISO alternative, however, is forecast to register a 19.12% CAGR through 2031 as operators push micro-edge nodes into space-constrained sites such as cell-tower grounds and urban rooftops. The containerized data center market size for 20-foot units is projected to climb sharply as telecoms race to densify 5G coverage. Smaller footprints lower site-prep costs and simplify permitting, giving carriers a fast path to service differentiation. Conversely, custom enclosures exceeding 40 feet cater to government and energy projects where oversized power gear or RF shielding is mandatory, though transport limitations hinder mainstream adoption.

Demand bifurcation is becoming clearer: large ISO formats satisfy core-to-edge spillover for cloud providers, while ultra-compact pods serve real-time data pipelines in retail, manufacturing and smart-city rollouts. Hitachi Systems refreshed its range in May 2025 with three standard SKUs, each covering AI inference, server-room replacement and telco edge use cases, signaling vendor acknowledgment that one size no longer fits all. Delta's 20-foot design shown at CEATEC integrates 800 G Ethernet and 1.5 MW of liquid cooling, proving high performance is achievable even in tighter volumes. Price-performance ratios therefore hinge on how deftly suppliers package dense compute while adhering to ISO standards.

The North America Containerized Data Center Market Report is Segmented by Container Size (20-Foot ISO, 40-Foot ISO, Greater Than 40-Foot Custom), Component Module (IT Module, Power Module, Cooling Module, Monitoring and Management Module), End-User Industry (IT and Telecommunications, BFSI, Government and Defense, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).