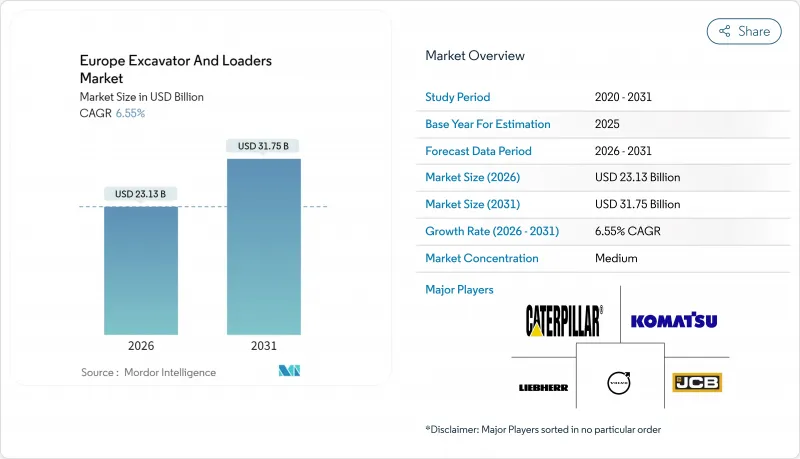

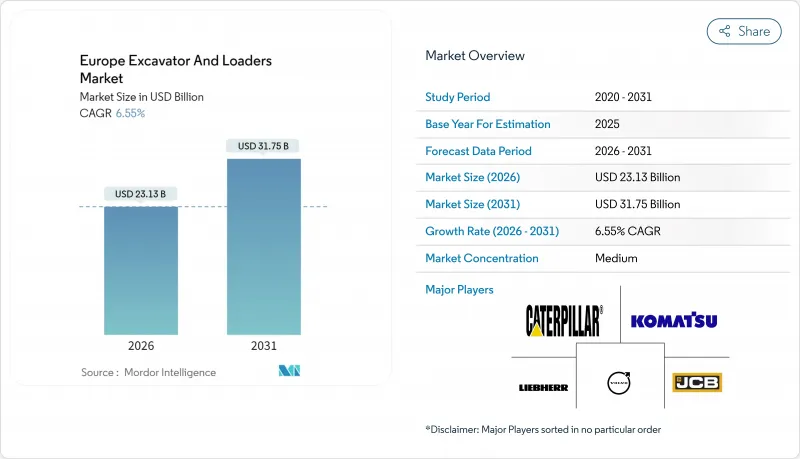

유럽의 굴착기 및 로더 시장 규모는 2026년 231억 3,000만 달러로 추정됩니다. 이는 2025년 217억 1,000만 달러에서 성장한 수치이며, 2031년에는 317억 5,000만 달러에 이를 것으로 예측되고 있습니다. 2026년부터 2031년까지는 CAGR 6.55%를 나타낼 것으로 전망되고 있습니다.

유럽 그린딜에 의한 자금공급, 유행후 프로젝트 지연의 해소, 그리고 엄격한 스테이지 V 배출규제가 함께 단기적인 경제변동을 견디는 설비투자 증가 경향이 지속되고 있습니다. 전기식 및 하이브리드식 기계의 투입은 현재, 연차 제품 사이클에서 실시되고 있어, 디젤 구동 시스템으로부터의 이행을 가속화함과 동시에, 유럽을 제로 에미션 작업 현장의 조기 도입 실험장으로서 확립하고 있습니다. 설비의 서비스화 모델이 주목을 받고 있습니다. 높은 이자율과 복잡한 컴플라이언스 비용은 사용량 기반 액세스가 완전 소유보다 매력적이기 때문입니다. 경쟁의 역학은 디지털 트윈에 의한 현장 자동화, 플리트 텔레매틱스, 무선 소프트웨어 갱신을 중심으로 전개해, 중기를 물리적인 생산성에 더해, 평생에 걸친 데이터 가치를 제공하는 접속 자산으로 변혁하고 있습니다.

유럽연합(EU)은 2030년까지 기후 변화 대책에 합치한 지출로 1조 유로를 계상해 철도전화, 에너지 절약형 공공건축물, 신재생에너지 대응 그리드에 수십억 유로를 투입하고 있습니다. 공공 조달에서는 스테이지 V 대응 또는 완전 전동 기기의 지정이 증가하고 있어, 렌탈 플릿은 노후화된 디젤 기기의 쇄신을 강요받고 있습니다. 전기 함대 확장을 위해 대형 렌탈 그룹에 제공된 1억 유로의 대출은 우대 금융이 민간 부문의 현대화 주기를 촉진하는 방법을 보여주는 좋은 예입니다. 초기 비용이 아닌 라이프사이클 배출량으로 입찰을 평가하는 조달 정책이 도입을 가속화시키고, 북유럽 전역에서 배터리 구동식 굴착기, 텔레핸들러, 현장용 발전기 수요가 상승 스파이럴을 형성하고 있습니다.

락다운에 의해 수백 개의 지자체·상업 프로젝트가 연기되었고, 2025년에 들어 계약자의 수주잔고는 과거 최고를 기록했습니다. 규제완화에 따라 연기된 안건과 신규 그린딜 안건이 동시 진행됨에 따라 가동률은 과거 최고 수준을 돌파했습니다. 중형 굴착기의 임대일당은 건설업체가 비용억제보다 공사완료를 우선했기 때문에 두 자리 프리미엄 가격으로 상승했습니다. 이 수주 잔량의 집중에 의해 OEM 제조업체는 2026년까지의 생산 계획을 가시화할 수 있어 부품 조달을 현지화하는 것과 동시에, 납기 단축으로 이어지는 지역별 배터리 팩 조립 라인의 설치를 정당화할 수 있게 되었습니다.

유럽 렌탈 매출은 2024년 2% 이상 성장해 건설 GDP를 웃도는 성장을 유지했습니다. 고소 작업차의 일부 카테고리에서는 렌탈 보급률이 80%를 넘고 있습니다. 통합업체는 지역 거점을 인수하고, 조달을 일원화, 수량 할인을 협상함으로써 OEM의 품목별 이익률을 압박. 계약업체가 변동비 지향으로 이행하는 가운데, 제조업체는 보수 계약이나 잔존 가치 보증에 축족을 옮기고 있지만, 플릿이 자산을 장기 사이클로 활용하기 때문에 판매 대수는 여전히 억제되고 있습니다.

굴착기는 2025년 유럽 건설기계 시장 수익의 58.10%를 차지했고 11.3%의 연평균 복합 성장률(CAGR)이 전망되고 있습니다. 이것은 붐과 버킷을 갖춘 범용 플랫폼이 전통적으로 전용 기계에 할당 된 많은 작업을 흡수하고 있음을 보여줍니다. 민첩한 소형 모델은 배출 가스 규제 대상의 좁은 도시 현장을 기동적으로 이동하고, 45톤급 유닛은 철도 성토의 굴착이나 해상 풍력 발전 기초 공사에 대응합니다. 통합 틸트 로테이터와 퀵 커플러 시스템은 어태치먼트 교환 시간을 몇 초로 단축시켜 가동 시간의 효율화를 도모하고 있습니다. OEM 제조업체가 기계 제어 소프트웨어와 무선 교정 기능을 통합함으로써 굴착기는 3D 현장 데이터를 기반으로 센티미터 단위의 정지가 가능한 자율 작업 스테이션으로 진화하고 있습니다. 현장 밖에 설치된 원격 조작 캐빈은 안전성을 향상시키고 노동력 확보 범위를 넓힙니다. 이것은 유럽의 노동력 고령화가 진행되는 가운데 매우 중요한 이점입니다.

스키드 스티어 로더, 휠 로더, 백호는 자재 적재와 다목적 유틸리티에서 여전히 중요성을 유지하지만, 그래플과 팔레트 포크 어태치먼트를 장착한 굴착기가 동등한 처리 능력을 발휘할 수 있기 때문에 그 성장은 둔화되고 있습니다. 전후 주택단지의 근대화가 진행되고 있는 가운데, 신축 붐을 갖춘 고소 해체용 굴착기 수요가 증가하고 있습니다. 텔레스코픽 핸들러는 텔레매틱스 기술에 의해 포크 각도를 실시간으로 계측하고, 오퍼레이터의 지원이나 보험사의 요건을 충족하는 것으로, 기종의 경계를 더욱 모호하게 하고 있습니다. 이 융합은 유럽 건설기계 시장 진출기업이 기존의 세로 분할 카테고리가 아닌 모듈형 플랫폼을 기반으로 제품 포트폴리오를 재설계하는 이유를 뒷받침합니다.

유럽 건설기계 시장 규모의 92.70%는 여전히 디젤/유압 시스템이 차지하고 있지만, 전동 모델의 19.1%라는 CAGR은 전환점이 추측의 영역에서 필연으로 이행한 것을 뒷받침하고 있습니다. 초기 도입은 가동 사이클이 현행의 배터리 밀도와 정합하는 3톤 미만의 소형기에 집중하고 있었지만, 현재는 OEM의 로드맵에 10-14톤의 굴착기나, 교환 가능한 배터리 팩을 탑재한 6m3 휠 로더가 기재되어 있습니다. 공공기관에서는 소음에 민감한 야간 작업용으로 전동 스키드 스티어 로더를 도입하여 작업자의 건강 증진과 이웃 주민의 수용성을 이유로 들고 있습니다. 채석장에서는 회생 브레이크를 현장의 분쇄기에 연결하여 에너지 효율을 향상시키는 송전망에 연결된 케이블식 기계가 재등장하고 있습니다.

충전 거점에서 멀리 떨어진 장기간 토목 공사 현장에서는 디젤 전기 하이브리드 기계가 잠정적인 틈새 시장을 채우고 있습니다. 스칸디나비아의 광산에서 실증시험 중인 연료전지 프로토타입은 성능 저하 없이 8시간의 가동을 실현하고 있지만, 수소 공급망은 아직 발전도상입니다. 구동 방식의 다양화는 유럽 건설기계 시장이 다양한 에너지 환경으로 전환하고 있음을 보여줍니다. 함대 관리자는 파워트레인을 지정하기 전에 지역 배출 규제, 가동 주기 및 총 에너지 비용을 종합적으로 고려해야 합니다.

Europe Excavator And Loaders market size in 2026 is estimated at USD 23.13 billion, growing from 2025 value of USD 21.71 billion with 2031 projections showing USD 31.75 billion, growing at 6.55% CAGR over 2026-2031.

A confluence of European Green Deal funding, pent-up post-pandemic project backlogs, and aggressive stage-V emission rules sustains a capital-expenditure upswing that is resilient to short-term economic volatility. Electric and hybrid machinery launches now occur on annual product-cycle cadences, accelerating the region's migration away from diesel powertrains and establishing Europe as an early-adopter laboratory for zero-emission job-sites. Equipment-as-a-Service models are gaining traction because high interest rates and complex compliance costs make usage-based access more attractive than outright ownership. Competitive dynamics increasingly revolve around digital-twin job-site automation, fleet telematics, and over-the-air software updates, turning heavy machines into connected assets that deliver lifetime data value in addition to physical productivity.

The European Union has earmarked EUR 1 trillion for climate-aligned spending through 2030, channeling billions into rail electrification, energy-efficient public buildings, and renewable-ready grids. Public tenders increasingly stipulate stage-V or fully electric equipment, prompting rental fleets to overhaul aging diesel inventories. A EUR 100 million loan extended to a leading rental group for electric fleet expansion exemplifies how concessional finance levers private modernization cycles. Procurement policies that score bids on life-cycle emissions rather than upfront cost accelerate adoption, creating an upward spiral in demand for battery-powered excavators, telehandlers, and site-generators across Northern Europe.

Lockdowns delayed hundreds of municipal and commercial projects, inflating contractor order books to record highs entering 2025. As restrictions eased, simultaneous execution of deferred and new Green-Deal workstreams pushed utilization rates past historical ceilings. Rental day-rates for mid-range excavators climbed into double-digit premiums because contractors prioritized job completion over cost containment. The backlog convergence grants OEMs visibility on production runs through 2026, allowing them to localize component sourcing and justify regional battery pack assembly lines that shorten delivery lead-times.

European rental turnover grow by over 2% in 2024 and continues to outpace construction GDP, with certain aerial platform categories now achieving over 80% rental penetration. Consolidators acquire regional depots, centralize procurement, and negotiate volume discounts that depress OEM line-item margins. As contractors shift toward variable costs, manufacturers pivot to servicing agreements and residual-value guarantees, but unit sales still temper as fleets sweat assets over longer cycles.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Excavators generated 58.10% of Europe construction equipment market revenue in 2025 and are forecasted for an 11.3% CAGR, illustrating how versatile boom-and-bucket platforms absorb many tasks once assigned to specialized machines. Agile mini models maneuver through tight urban sites subject to zero-emission ordinances, while 45-ton units tackle rail embankment cuts and offshore wind foundation work. Integrated tilt-rotators and quick-coupler systems shrink attachment change-over to seconds, amplifying utilization across day-parts. As OEMs embed machine-control software and over-the-air calibration, excavators evolve into autonomous workstations capable of centimeter-level grading guided by 3D site files. Remote-operation cabs stationed offsite improve safety and widen labor pools, a critical benefit amid an aging European workforce.

Skid steers, wheel loaders, and backhoes maintain relevance in material loading and multi-purpose municipal duties, yet their growth lags because excavators fitted with grapple or pallet-fork attachments can achieve similar throughput. High reach demolition excavators with telescopic booms are seeing increased demand as cities modernize post-war housing blocks. Telescopic handlers blur category lines further, as telematics measure fork-load angles in real time, assisting operators and satisfying insurer requirements. This convergence underscores why Europe construction equipment market participants redesign portfolios around modular platforms rather than traditional siloed categories.

Diesel/hydraulic systems still account for 92.70% of Europe construction equipment market size, but electric models' 19.1% CAGR reinforces that the tipping point has shifted from speculative to inevitable. Early adoption focused on <3 ton minis where duty cycles align with current battery density; today OEM roadmaps list 10-14 ton excavators and 6 m3 wheel loaders with shift-able swappable packs. Public agencies procure electric skid steers for noise-sensitive night work, citing operator health benefits and neighborhood acceptance. Grid-tethered cable machines re-emerge in quarries, linking regenerative braking to onsite crushers and improving energy efficiency.

Hybrid diesel-electric variants fill an interim niche on long-duration civil engineering jobs far from charging depots. Fuel-cell prototypes field-tested in Scandinavian mines demonstrate eight-hour runtimes without performance drop-off, though hydrogen supply chains remain nascent. The drive-type spectrum signals that the Europe construction equipment market is transitioning into a multi-energy landscape, where fleet managers weigh local emission rules, duty cycles, and total-energy pricing before specifying powertrains.

The Europe Excavator and Loaders Market Report is Segmented by Machinery Type (Excavators and Loaders), Drive Type (Diesel/Hydraulic, Electric, and More), Operating Weight (Below 6t, 6 To 14t, and More), End-Use Industry (Construction, Mining and Quarrying, and More), Application (Excavation and Earthmoving and More), and Country (Germany and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).